Embed Size (px)

Citation preview

ACCAspace

Provided byACCA Research Institute ACCA课程研究学院

ACCA P7 习题详解Advanced Audit and Assurance (AAA)

高级审计与鉴证业务 第三讲

ACCA Lecturer: Iris Nie

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 2

Syllabus

Business risks

Outsourcing

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 3

2014.June Q4 练习册Q8 36min

You are a manager in Ryder & Co, a firm of Chartered

Certified Accountants, and you have taken on the

responsibility for providing support and guidance to new

members of the firm. Ryder & Co has recently recruited

a new audit junior, Sam Tyler, who has come across

several issues in his first few months at the firm which

he would like your guidance on. Sam’s comments and

questions are shown below:

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 4

2014.June Q4 练习册Q8 36min

Required:

For each of the issues raised, respond to the audit

junior, explaining the ethical and professional matters

arising from the audit junior’s comments.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 5

(a) I know that auditors are required to assess risks of

material misstatement by developing an understanding

of the business risks of an audit client, but I am not clear

on the relationship between business risk and risk of

material misstatement. Can you explain the two types of

risk, and how identifying business risk relates to risk of

material misstatement?

(4 marks)

2014.June Q4 练习册Q8 36min

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 6

思考——

1. Explain the meaning of business risk and risk of

material misstatement

2. Business 分为 operational risk, financial risk,

compliance risk. / Risk of material misstatement 分为

inherent risk, control risk.

3. The relationship between the two risks—how

identifying business risk relates to risk of material

misstatement?

2014.June Q4 练习册Q8 36min

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 7

2014.June Q4 练习册Q8 36min

Answer——

Business risk is defined in ISA 315 Identifying

and Assessing the Risks of Material Misstatement

Through Understanding the Entity and its

Environment. The definition states that【business

risk is a risk resulting from significant conditions,

events, circumstances, actions or inactions which

could adversely affect an entity’s ability to achieve

its objectives and execute its strategies, or from the

setting of inappropriate objectives and strategies.】

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 8

2014.June Q4 练习册Q8 36min

Risk of material misstatement is defined in ISA

200 Overall Objectives of the Independent Auditor

and the Conduct of an Audit in Accordance with

ISAs as 【 the risk that the financial statements are

materially misstated prior to audit. 】Risk of

material misstatement comprises inherent risk and

control risk.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 9

2014.June Q4 练习册Q8 36min

ISA 315 states that the auditor shall perform risk

assessment procedures to provide a basis for the

identification and assessment of risks of material

misstatement at the financial statement and assertion

levels.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 10

2014.June Q4 练习册Q8 36min

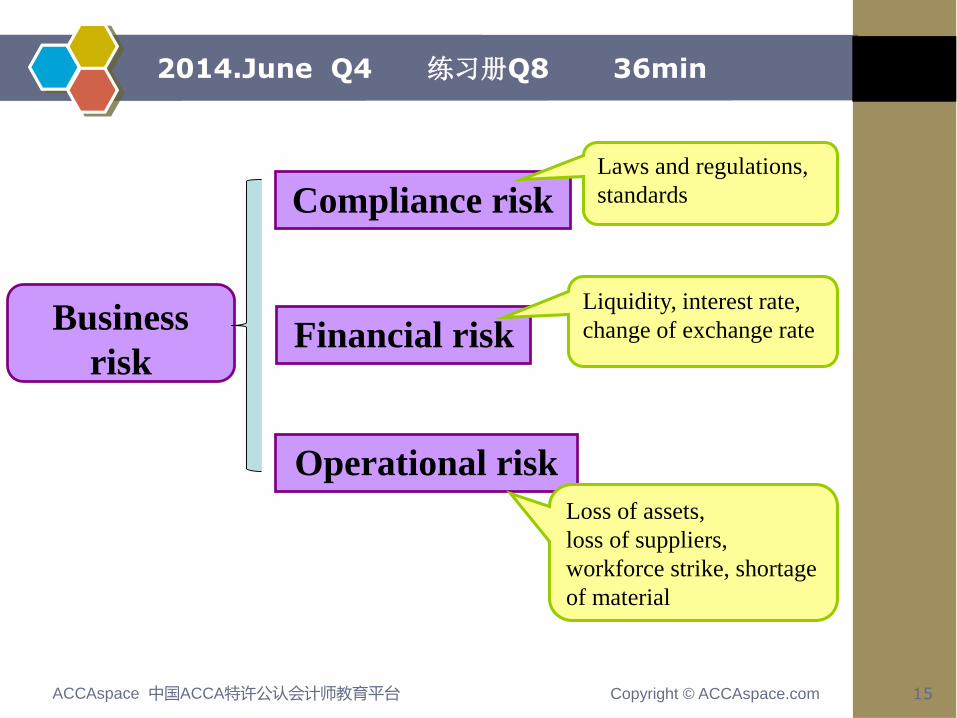

Business risks can be broken down into operational

risk, financial risk and compliance risk. Each of these

components can have a direct impact on the financial

statements, and therefore understanding the

components of business risk can help the auditor to

identify risks of misstatement, and to design a

response to that risk.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 11

2014.June Q4 练习册Q8 36min

Some business risks impact the inherent risk

component of risk of material misstatement. For

example, the auditor may have identified that an

audited entity has significant levels of debt with

covenants attached. The business risk is that the

covenants are breached and the debt recalled. An

associated inherent risk at the financial statement

level is that the financial statements could be

manipulated to avoid breaching the debt covenant.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 12

2014.June Q4 练习册Q8 36min

Other business risks impact on the control risk

component of risk of material misstatement. For

example, the auditor may have identified that an

audited entity has a business risk due to having lost

key members of personnel in the accounting

department. This has a clear impact on control risk,

as it means the accounting department is short of

competent staff and errors are likely to go undetected

and uncorrected.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 13

2014.June Q4 练习册Q8 36min

Therefore the ISAs’ approach to planning an audit is

underpinned by the concept that it is essential for an

auditor to understand the business risks of an audited

entity in order to effectively identify and respond to risks

of material misstatement.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 14

2014.June Q4 练习册Q8 36min

评分标准——

(a) Risk assessment

– Definition of business risk (1 mark)

– Definition of risk of material misstatement (1 mark)

– Business risks impact on the financial statements

and therefore risk of material misstatement

– Business risk impacts inherent risk

– Business risk impacts control risk

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 15

2014.June Q4 练习册Q8 36min

Compliance risk

Financial risk

Operational risk

Liquidity, interest rate,

change of exchange rate

Loss of assets,

loss of suppliers,

workforce strike, shortage

of material

Business

risk

Laws and regulations,

standards

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 16

2014.June Q4 练习册Q8 36min

Examples of business risks——

• The risk that products may become technologically

obsolete.

• The risk of losing key staff.

• The risk of a catastrophic failure of IT systems.

• The risk of changes in government policy.

• The risk of fire or natural disaster.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 17

2014.June Q4 练习册Q8 36min

Ultimately these business risks can lead to

complications and deficiencies in the accounting

process, which could lead to fraud, error or omission.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 18

2014.June Q4 练习册Q8 36min

(b) I worked on the interim audit of Crow Co, a

manufacturing company which outsources its payroll

function. I know that for Crow Co payroll is material.

How does the outsourcing of payroll affect our audit

planning?

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 19

思考——

1. Definition

2. Affect audit planning → Obtaining an understanding

of the business → Materiality / Audit risk

3. Relevant control (both user organisation and

service organisation )

4. Means of obtaining understanding

2014.June Q4 练习册Q8 36min

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 20

2014.June Q4 练习册Q8 36min

Answer——

【 Outsourcing is when certain functions within a

business are contracted out to third parties known as

service organisations. 】 It is common for companies

to outsource one or more of it functions, with payroll,

IT and human resources being examples of functions

which are typically outsourced.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 21

2014.June Q4 练习册Q8 36min

Outsourcing does have an impact on audit planning.

ISA 402 Audit Considerations Relating to an Entity

Using a Service Organisation requires the auditor to

obtain an understanding of how the audited entity

(also known as the user entity) uses the services of a

service organisation in the user entity’s operations,

including the following matters:

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 22

2014.June Q4 练习册Q8 36min

– The nature of the services provided by the

service organisation and the significance of those

services to the audited entity, including the effect on

internal control;

– The nature and materiality of the transactions

processed or accounts or financial reporting

processes affected by the service organisation;

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 23

2014.June Q4 练习册Q8 36min

– The degree of interaction between the activities

of the service organisation and those of the audited

entity;

– The nature of the relationship between the

audited entity and the service organisation, including

the relevant contractual terms.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 24

2014.June Q4 练习册Q8 36min

The reasons for the auditor being required to

understand these matters is so that any risk of

material misstatement created by the use of the

service organisation can be identified and an

appropriate response planned.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 25

2014.June Q4 练习册Q8 36min

The auditor is also required under ISA 402 to

evaluate the design and implementation of relevant

controls at the audited entity which relate to the

services provided by the service organisation,

including those which are applied to the transactions

processed by the service organisation.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 26

2014.June Q4 练习册Q8 36min

This is to obtain understanding of the control risk

associated with the outsourced function, for example,

whether the transactions and information provided by

the service organisation is monitored and whether

checks are performed prior to inclusion in the financial

statements.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 27

2014.June Q4 练习册Q8 36min

Information should be available from the audited

entity to enable the understanding outlined above to

be obtained, for example, through reports received

from the service organisation, technical manuals and

the contract between the audited entity and the

service organisation.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 28

2014.June Q4 练习册Q8 36min

The auditor may decide that further work is

necessary in order to evaluate the risk of material

misstatement associated with the outsourcing

arrangement’s impact on the financial statements. It

is common for a report on the description and design

of controls at a service organisation to be obtained.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 29

2014.June Q4 练习册Q8 36min

A type 1 report focuses on the description and

design of controls, whereas a type 2 report also

covers the operating effectiveness of the controls.

This type of report can provide some assurance over

the controls which should have operated at the

service organisation.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 30

2014.June Q4 练习册Q8 36min

Alternatively, the auditor may decide to contact the

service organisation to request specific information, to

visit the service organisation and perform procedures,

probably tests on controls, or to use another auditor to

perform such procedures. All of these methods of

evaluating the service organisation’s controls require

permission from the client and can be time consuming

to perform.

Copyright © ACCAspace.comACCAspace 中国ACCA特许公认会计师教育平台 31

2014.June Q4 练习册Q8 36min

The purpose of obtaining the understanding above

is to help the auditor to determine the level of

competence of the service organisation, and whether

it is independent of the audited entity. This will then

impact on the risk of material misstatement assessed

for the outsourced function.

ACCAspace

![[Table Title] 借鉴历史上牛市 3 浪 - HTSEC.COM€¦ · 主升浪。19 年以来我们一直重申两个判断:2019 年2440 点=05 年998 点, 牛市有三个阶段。上证综指2440-3288-2733](https://img.pdfslide.org/doc/110x75/5f7b6270eee8fe431c5b66d6/table-title-ec-3-htseccom-19-ceci2019.jpg)