Embed Size (px)

Citation preview

Technische Universität Braunschweig Institut für Wirtschaftswissenschaften

Abteilung für Volkswirtschaftslehre Prof. Dr. Franz Peter Lang

Dr. Johannes Laser

University of Nebraska at Omaha College of Business Administration

Department of Economics Prof. Dr. Michael O'Hara

Diplomarbeit

Concentration and Contestability in the Deregulated

United States Airline Industry

Jens Blechschmidt Rehrbrinkstr. 26

30890 Barsinghausen

Diplom-Wirtschaftsingenieurwesen Studienrichtung Elektrotechnik

Matr. Nr. 2338895 SS 1995

Technische Universität Braunschweig University of Nebraska at Omaha institut für Wirtschaftswissenschaften College of Business Administration Abteilung für Volksuvirtschaftslehre Department of Economics Professor Dr. Lang Professor Dr. O'Hara

Diplomarbeit Es wurde mit

Herrn Jens Blechschmidt, Rehrbrinkstr. 26, 30890 Barsinghausen, Wirtschaftsingenieurwesen/Elektrotechnik, Matr.Nr. 2338895

folgendes Thema für eine sechsmonatige Diplomarbeit vereinbart:

Concentration and Contestability in the Deregulated United States Airline Industry

Die Aufgabenstellung umfaßt folgende Teilaufgaben: • Darstellung der historischen Entwicklung des ordnungspolitischen Rahmens des

Luftverkehrs in den Vereinigten Staaten • Darstellung und Analyse der volkswirtschaftlichen Theorien, die der Deregulierung

des Luftverkehrs zugrunde liegen • Analyse der Auswirkungen der Deregulierung, insbesondere auf die

Marktkonzentration im inneramerikanischen Linien-Passagierluftverkehr gberprüfung der Anwendbarkeit der genannten Theorien auf die spezielle Marktstruktur des Luftverkehrs

• Diskussion eventuell notwendiger ordnungspolitischer Eingriffe und Entwicklung eines adäquaten Wettbewerbskonzepts für den Luftverkehr

Die Arbeit wird am Institut für Volkswirtschaftslehre der TU Braunschweig in Kooperation mit dem College of Business Administration der University of Nebraska at Omaha (USA) angefertigt.

Betreuer in Omaha: Professor Dr. Michael O’Hara Betreuer in Braunschweig: Professor Dr. Franz-Peter Lang Beginn der Arbeit: 30, Juni 1995 _____________________ (Prof. Dr. M. O'Hara) Abgabe der Arbeit: ______________ ______________________ (Datum) (Unterschrift)

EIDESSTATTLICHE ERKLÄRUNG Hermit versichere ich, daß ich die vorliegende Arbeit selbständig and ohne fremde Hilfe

angefertigt habe. Außer den angegebenen Quellen wurden keine weiteren Hilfsmlttel

verwendet.

Omaha, den 17. November, 1995

__________________________

(Jens Blechschmidt)

v

TABLE OF CONTENTS List of Figures . ..........................................................................................................................vii List of Tables ............................................................................................................................viii CHAPTER I. OVERVIEW AND PURPOSE OF THE STUDY.............................................. 1 CHAPTER II. PUBLIC POLICY FROM REGULATION TO DEREGULATION IN THE U.S. AIRLINE INDUSTRY .......................................................... 3 A. Theoretical Backgrounds ........................................................................................... 3 1. Main Market Structures . .......................................................................................... 4 2. The Perfect Competition Theory ............................................................................ 4 a) Definition of Perfect Competition . ................................................................... 5 b) Perfect Competition and Economic Efficiency ............................................. 5 3. The Contestable Market Theory ............................................................................ 7 a) Conditions for Perfect Contestability .............................................................. 7 b) Contestability and Industry Equilibrium ......................................................... 9 4. Perfect Contestability Contrasted with Perfect Competition ............................10 5. Reasons for Regulatory Activities ........................................................................11 a) Economies of Scale and Scope and Natural Monopolies ........................11 b) Universal Service ............................................................................................13 c) Destructive Competition .................................................................................13 d) Protection Against Misinformation ................................................................14 e) Abolishment of Entry Barriers .......................................................................14 B. The Regulatory Framework Before 1978 ..................................................................14 1. The History of the U.S. Airline Industry ...............................................................15 2. The Civil Aeronautics Act of 1938 .......................................................................16 a) The Civil Aeronautics Board ..........................................................................16 b) Regulated Market Parameters ......................................................................16 3. The Federal Aviation Act of 1958 . .......................................................................18 C. Rationale for Deregulation .......................................................................................19 1. No Economies of Scale Effects Expected ..........................................................20 2. Ease of Entry and Exit . ..........................................................................................20 3. The Texas and California Experience .................................................................21 D. The Airline Deregulation Act of 1978 ....................................................................21 1. Important Changes in Public Law ........................................................................22 2. Dwindling Authority of the Civil Aeronautics Board ..........................................23 3. The Resulting Open Market ..................................................................................24 CHAPTER Ill. CHANGES IN THE U.S. AIRLINE INDUSTRY ..........................................25 A. Market Developments and Industry Structure ....................................................25 1. Types of Airlines . ....................................................................................................25 2. Branch Specific Parameters .................................................................................28 3. Industry Developments 1945 - 1994 . ..................................................................30

vi

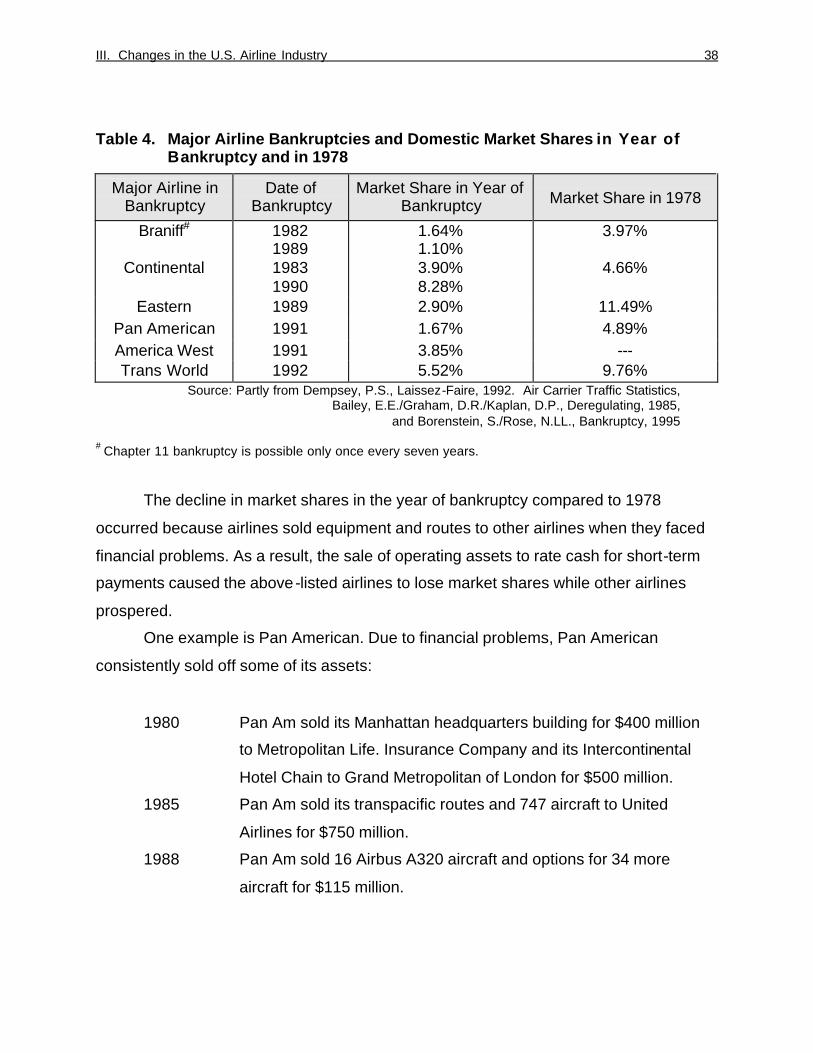

4. Major Acquisitions and Mergers ...........................................................................33 5. Bankruptcies Since Deregulation .........................................................................37 6. Hub-and-Spoke Route Systems . .........................................................................39 B. Concentration ..............................................................................................................44 1. The Herfindahl-Hirschman-Index .........................................................................45 2. Concentration in the Domestic U.S. Airline Industry ........................................47 3. Concentration at Large Hub-Airports ..................................................................50 4. Comparison of Hub- and Industry Concentration ..............................................61 5. Concentration and Air Fares .................................................................................63 C. Conclusion ....................................................................................................................64 1. The Failure of Perfect Competition ......................................................................65 2. The Failure of Contestability .................................................................................66 CHAPTER IV. THE CONTESTABLE MARKET THEORY AS A GUIDE FOR A NEW COMPETITION CONCEPT .............................................................................69 A. Entry Barriers ..............................................................................................................69 1. Frequent Flier Programs (FFP) ............................................................................70 2. Computer Reservation Systems (CRS) ..............................................................71 3. Travel Agent Commission Overrides (TACO) . ..................................................72 4. Code-Sharing ................................................................................................74 5. Facility Constraints .................................................................................................75 6. Landing Slots . .........................................................................................................75 7. Price Matching ........................................................................................................76 B. The Concept..................................................................................................................76 1. Overview of the Concept ...... ................................................................................78 2. A New Independent Transportation Commission .............................................80 3. Policy Options for Regulation ............ .............................................................80 CHAPTER V. SUMMARY AND FUTURE WORK ...............................................................84 APPENDICES ...........................................................................................................................86 Appendix Table I. Traffic Summary 1560 -1994 U.S. Scheduled Airlines ................87 Appendix Table II. Load Factor- U.S. Scheduled Airlines 1945 -1994 ......................88 Appendix Table Ill. HHI of the Domestic U.S. Airline Industry From 1970 - 1983 . .............................................................................................................89 Appendix Table IV. HHI of the Domestic U.S. Airline Industry From 1987 - 1994 ..............................................................................................................94 Appendix Table V. HHI of Twelve Large Hub-Airports in the United States 1972 - 1993 .....................................................................................97 REFERENCES ........................................................................................................................120

vii

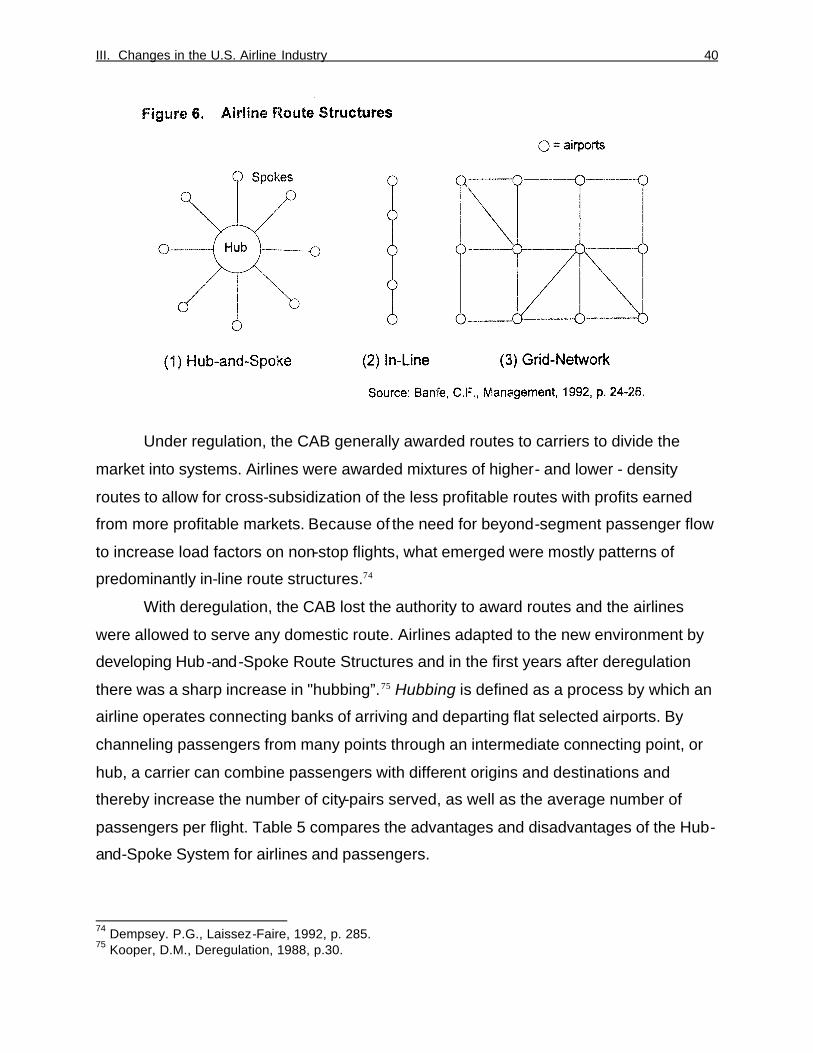

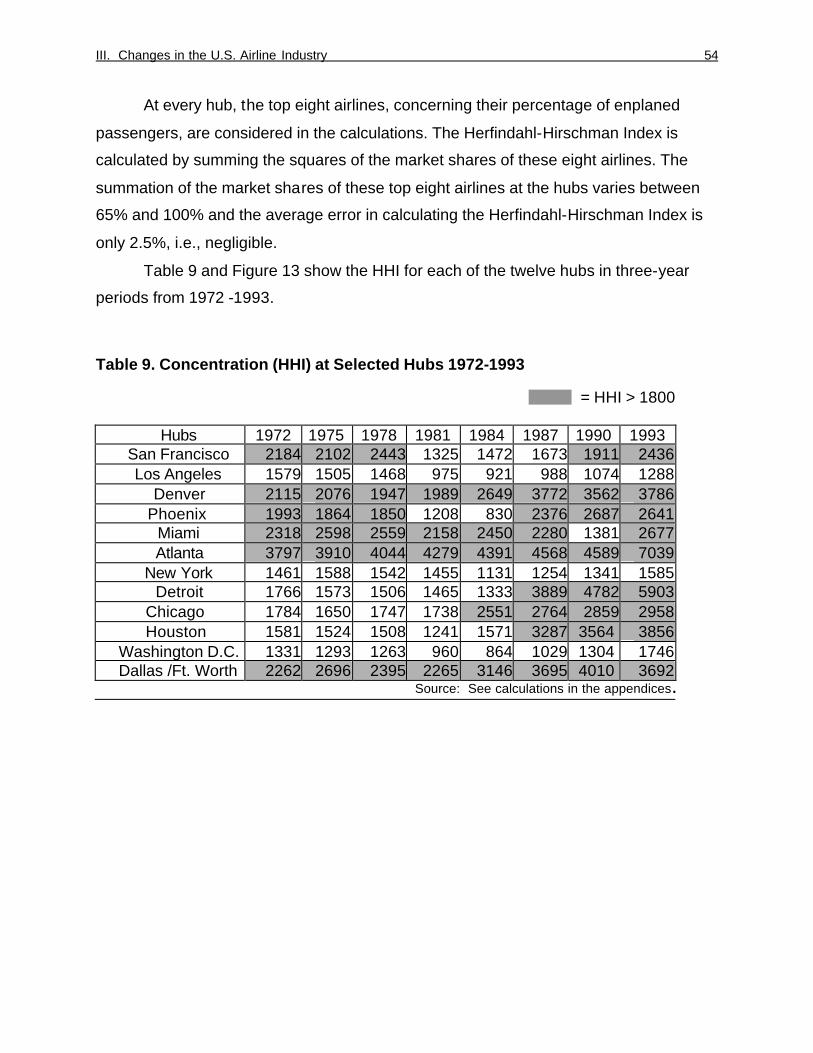

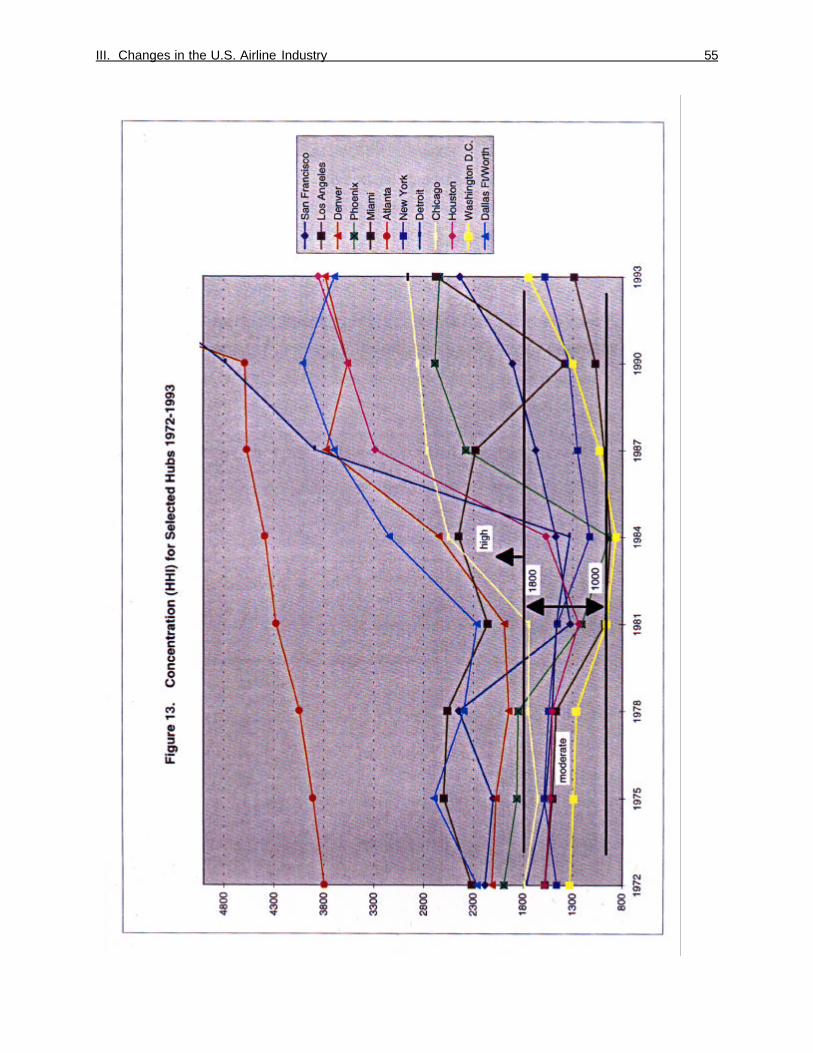

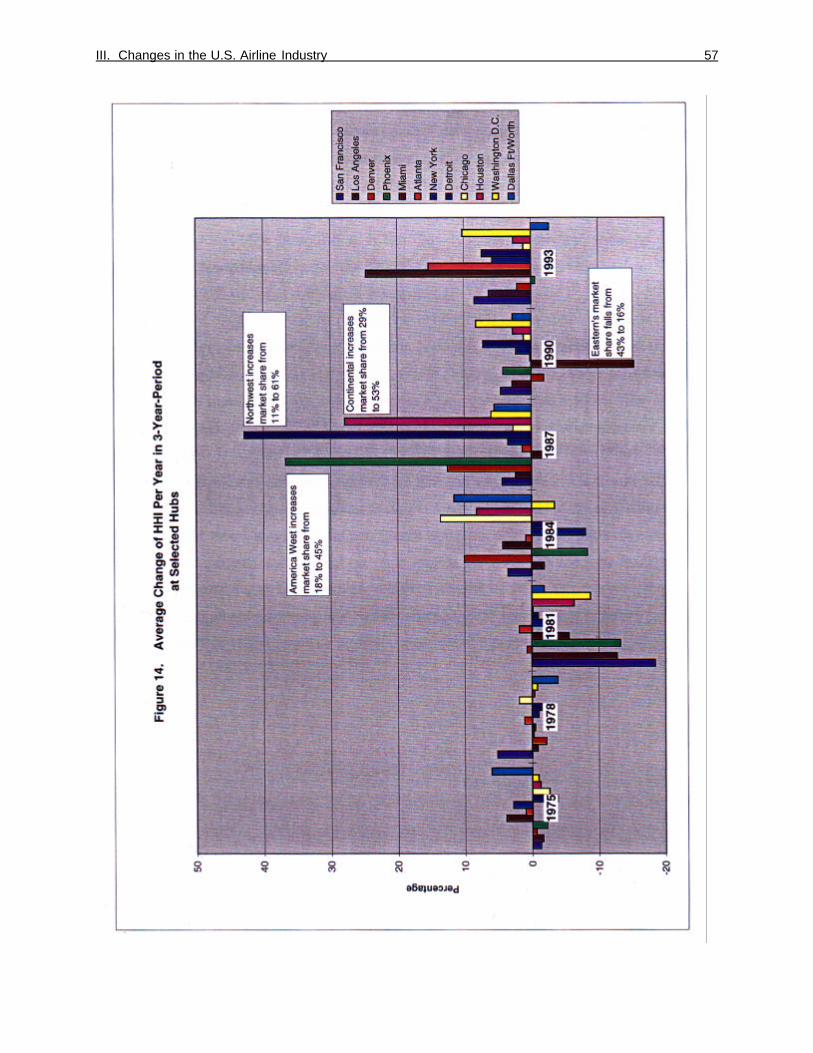

LIST OF FIGURES Figure 1. Long-Run Equilibrium of the Competitive Firm and Industry ....................... 6 Figure 2. Price Sustainability for Natural Monopolies ..................................................10 Figure 3. Domestic Market Shares of Major Airlines 1978 vs. 1994...........................28 Figure 4. Developments in the Domestic Airline Industry 1945-1994 .......................31 Figure 5. Major Acquisitions and Mergers Since Deregulation ...................................36 Figure 6. Airline Route Structures ...................................................................................40 Figure 7. Route System Before Deregulation ................................................................43 Figure 8. Hub-and-Spoke Route System After Deregulation ......................................43 Figure 9. Percentages of Domestic and International Traffic of the U.S. Airline Industry in 1978 and in 1994 .......................................................44 Figure 10. Concentration in the Domestic U.S. Airline Industry 1970-94 ....................48 Figure 11. Percentage of International Passengers Enplaned at Selected Hubs by U.S. Carriers in 1989 ...................................................................................52 Figure 12. Geographical Location of Air Traffic Hubs in the United States ................53 Figure 13. Concentration (HHI) for Selected Hubs 1972-1993 .....................................55 Figure 14. Average Change of HHI per Year in 3-Year-Periods at Selected Hubs ....57 Figure 15. Market Shares of the Two Dominant Airlines at Denver-Hub in 1972 and in 1993 .........................................................................................................59 Figure 16. Market Shares of the Two Dominant Airlines at Houston-Hub in 1972 and in 1993 .........................................................................................................59 Figure 17. Market Shares of the Two Dominant Airlines at Atlanta -Hub in 1972 and in 1993..........................................................................................................60 Figure 18. Market Shares of the Two Dominant Airlines at Detroit-Hub in 1972 and in 1993 . .......................................................................................................60 Figure 19. Average Industry HHI Compared to Average Hub HHl ...............................62 Figure 20. U.S. Airline Market Entry Barriers . .................................................................70 Figure 21. A Concept For Increased Contestability in the U.S. Airline Industry..........79

viii

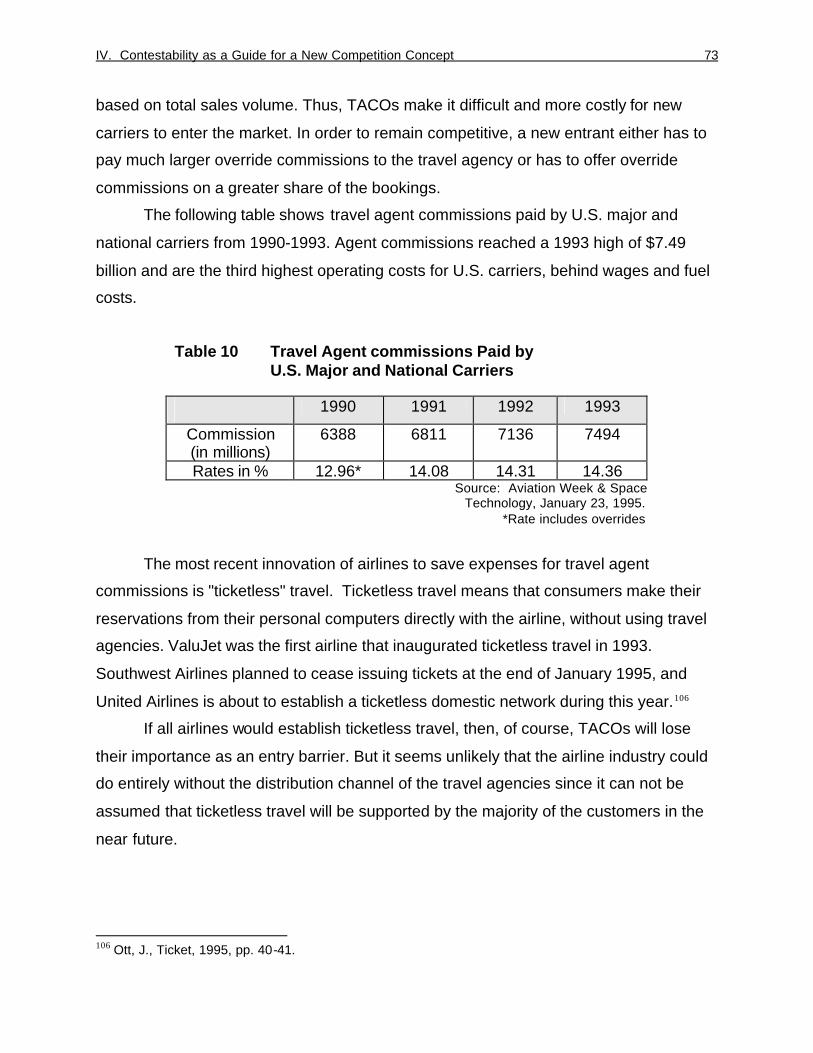

LIST OF TABLES Table 1. Variety of Market Structures ............................................................................... 4 Table 2. Dwindling Authority of the Civil Aeronautics Board.......................................24 Table 3. Major Airlines (Passenger) and Their Domestic Market Share in 1978 and 1994 ...................................................................................................27 Table 4. Major Airline Bankruptcies and Domestic Market Shares in Year of Bankruptcy and in 1978 ..................................................................38 Table 5. Advantages and Disadvantages of Hub-and-Spoke Route Structuring for Both Airlines and Passengers ...................................................................41 Table 6. Interpretation of HHI . ........................................................................................46 Table 7. Examples for HHI for Different Numbers of Firms of Equal Size ...............47 Table 8. Tendencies of Changes in Concentration (HHI) From 1970-1994.............49 Table 9. Concentration (HHI) at Selected Hubs 1972-1993 ......................................54 Table 10. Travel Agent Commissions Paid by U.S. Major and National Carriers .....73

CHAPTER I

OVERVIEW AND PURPOSE OF THE STUDY

Today, the airline industry is radically different from what it was prior to 1978. Before

1978 it resembled a public utility, with a government agency, the Civil Aeronautics

Board (CAB), determining the routes each airline flew and overseeing the prices they

charged. Now, without regulation, the airlines have complete freedom to choose their

own route structure and to fix ticket prices.

Responsible for this abrupt turn was the Airline Deregulation Act, approved by

Congress on October 24, 1978 and signed into law by President Jimmy Carter. The

primary justification for airline deregulation was the expectation by leading economists

(e.g., Elisabeth Bailey, William Baumol and Alfred Kahn) that the airline industry would

be highly competitive or at least would have the characteristics of a "contestable"

market. A perfectly contestable market, referring to the original theory developed by

Baumol, Panzar and Willig in the late 1970s, forces firms (even monopolies) to set the

price equal to cost. Therefore, this theory was supposed to be the adequate concept to

replace inefficient regulation that caused high airfares and excess capacity.

Since the Airline Deregulation Act of 1978 was passed, the industry was shaken

by mergers and bankruptcies and the new situation led to significant changes in the

performance of the airline industry. In the 1980s, several studies analyzed the effects of

deregulation, most of them with the result that the airline industry is not as "contestable"

as predicted. However, none of these studies presented a possible competition concept

based on the Contestable Market Theory.

The purpose of this study is to describe changes, in the airline industry since

deregulation, to analyze why the U.S. airline industry today is neither "competitive" nor

"contestable" and to suggest a possible concept to increase contestability in this market.

The analysis of the concentration of both the entire airline industry and the individual

markets (hub-airports) is crucial for the rejection or acceptance of contestability and

perfect competition, and therefore constitutes an important element in this project.

The project starts with Chapter II, which presents background information about

the Perfect Competition Theory and the Contestable Market Theory, describes the

I. Overview and Purpose of the Study 2

regulatory framework prior to deregulation, and explains why deregulation proponents

voted for the abolishment of any regulatory activity in the U.S. airline industry. This

chapter ends with a brief description of the impact of the Airline Deregulation Act of

1978 on the airline industry.

Chapter III provides an overview of the domestic U.S. passenger airline industry

from 1945-1994, concerning the developments of traffic, capacity and efficiency. Next,

the concentration of the domestic U.S. passenger airline industry and twelve large

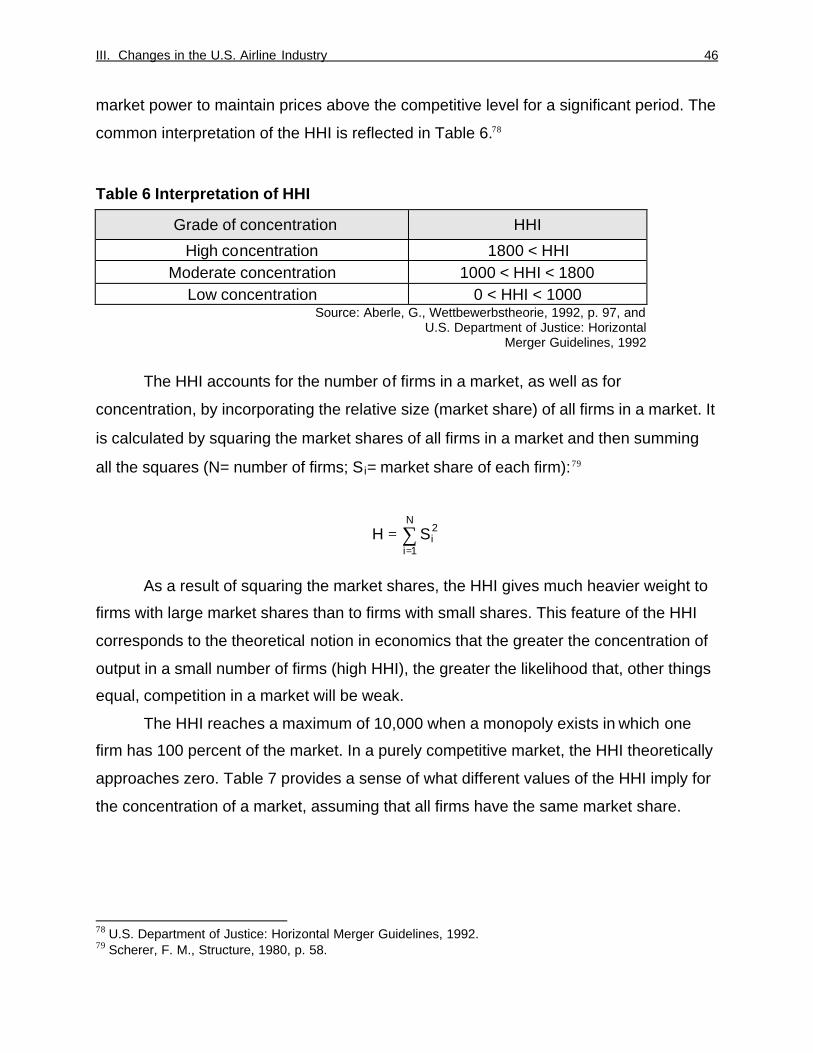

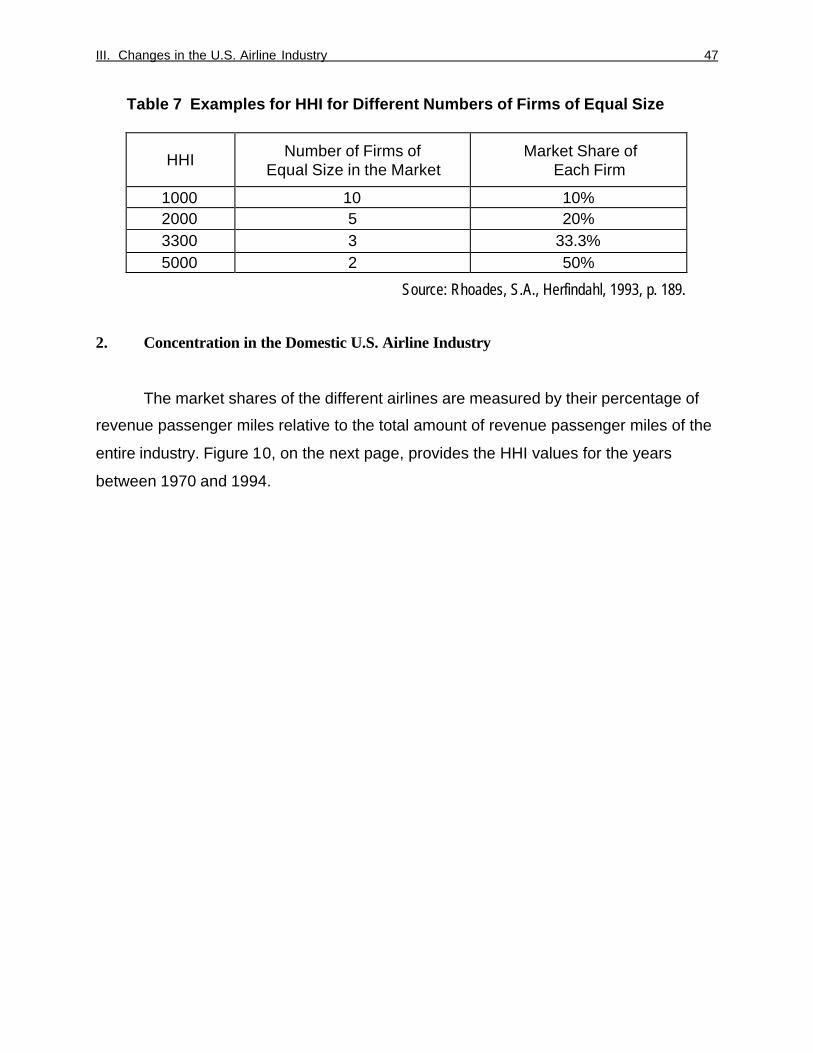

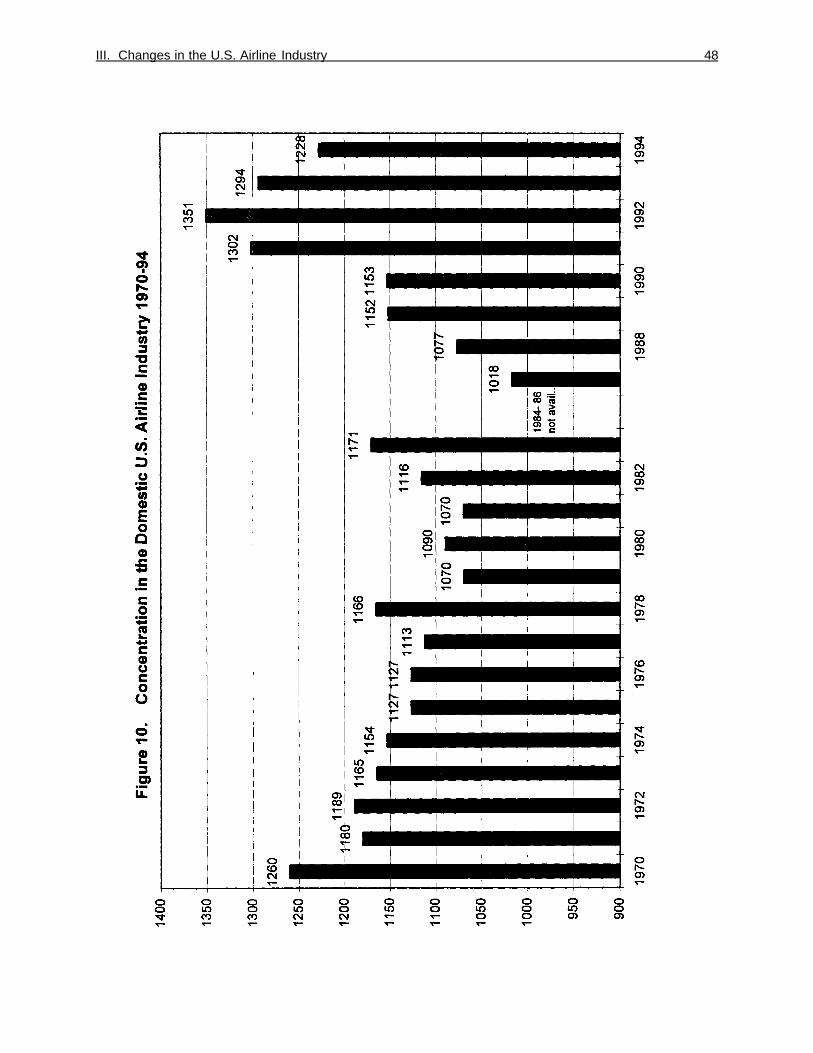

hub-airports in the United States from 1972 to 1994 are analyzed. The results of this

analysis and its effects on both the Perfect Competition Theory and the Contestable

Market Theory are discussed in the conclusion.

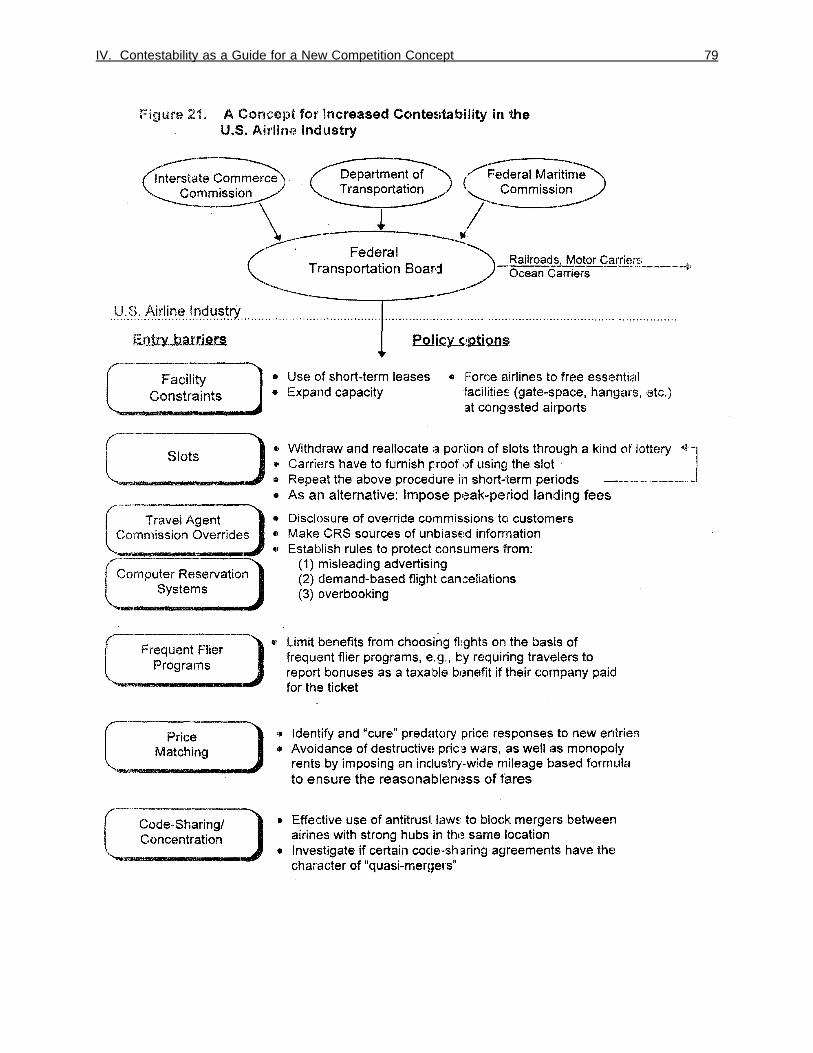

In Chapter IV, a possible competition concept is suggested that rests on the

belief that the Contestable Market Theory is applicable to the airline industry if entry

barriers, which impede contestability today, are abolished by temporary regulatory

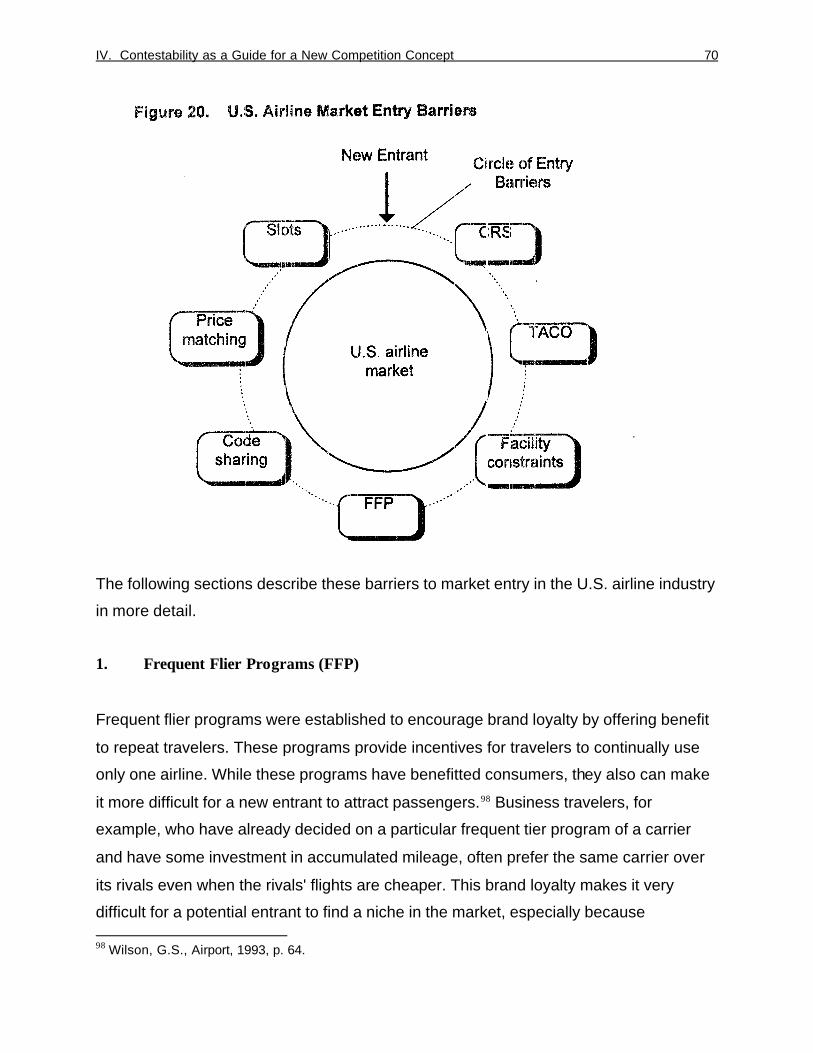

activities. These entry barriers are described in detail in the beginning of this chapter.

The results of this study are summarized in Chapter V. An overall conclusion and

suggestions for further research are presented.

CHAPTER II

PUBLIC POLICY FROM REGULATION TO DEREGULATION OF THE U.S. AIRLINE INDUSTRY

Chapter II describes the change in the public policy from regulation to deregulation

concerning the U.S. airline industry. Section A contains some general theoretical

information about the Perfect Competition Theory and the Contestable Market Theory

and explain the necessity of regulatory activities if the premises of perfect competition or

perfect contestability are not fulfilled by the industry itself. Section B will provide a

retrospective view of the time prior to airline deregulation, including the essential laws ,

institutions and the parameters that have been regulated by government. Section C

deals with the rationale for deregulation as viewed by the Civil Aeronautics Board.1

Section D will provide detailed information of the Airline Deregulation Act of 1978 and

will show the decline of the Civil Aeronautics Board.

A. Theoretical Backgrounds

To fully comprehend this study, it is necessary to have a basic understanding of

the economic theories that are the pillars of regulatory and deregulatory policy

in the United States: The Perfect Competition Theory and the Contestable

Market Theory.

This Section begins with a short overview of the "classical" market structures

applied by academic economists. In the following subsections, the Perfect Competition

Theory and the Contestable Market Theory are described and contrasted. Directly

derived from these theories is the reasoning behind regulatory activities, which is

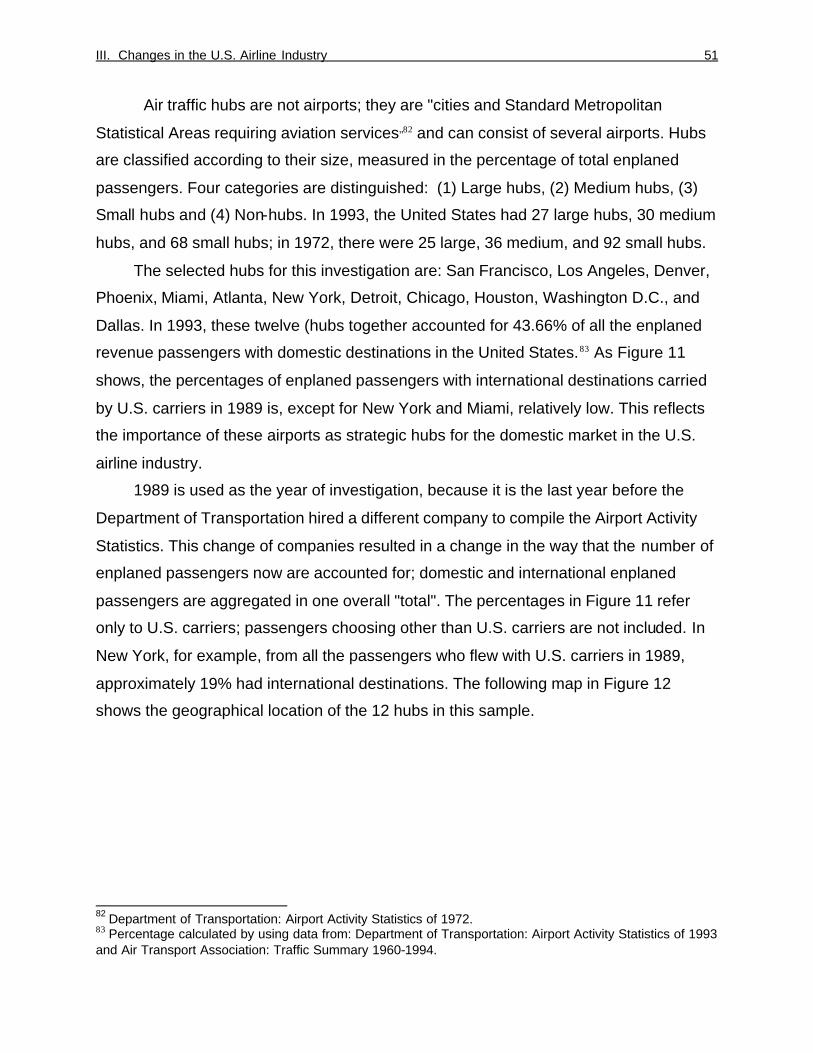

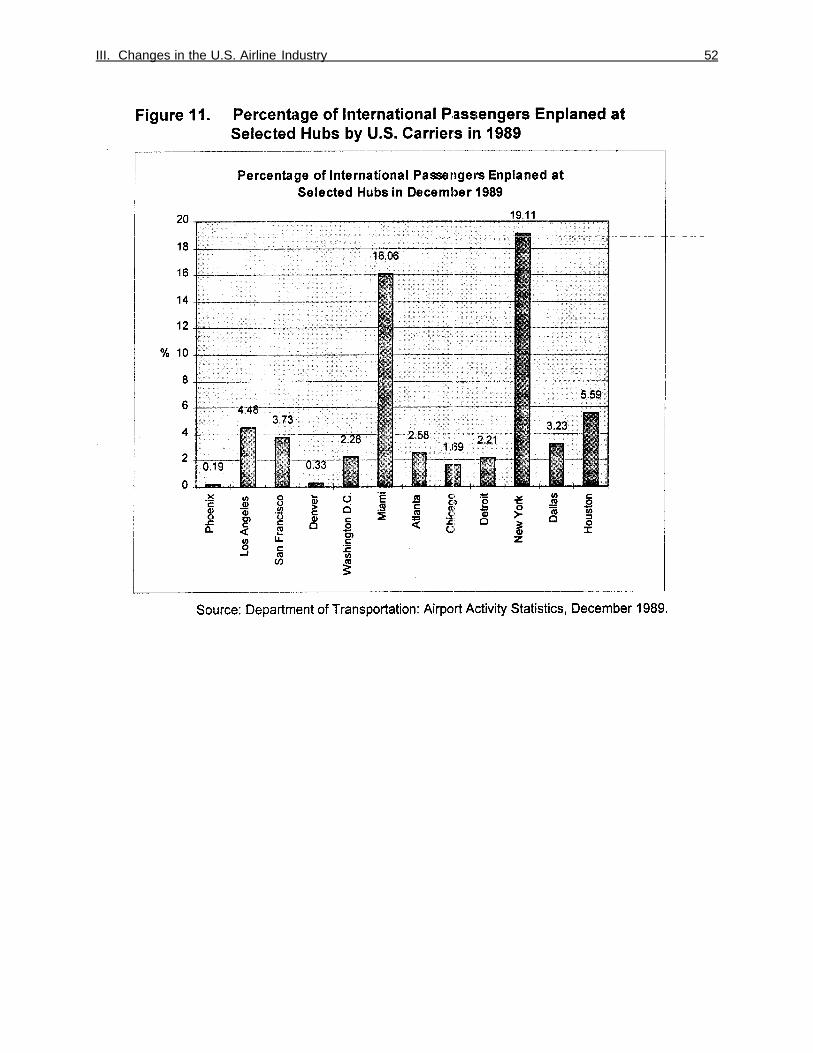

explained at the end of this section. The theoretical background provided in Section A

does not refer specifically to the airline industry. It also can be applied to any other

industry or market.

1 The Civil Aeronautics Board was the government institution that regulated the airline industry for 40 years, from 1938 to 1978.

II. Public Policy from Regulation to Deregulation 4

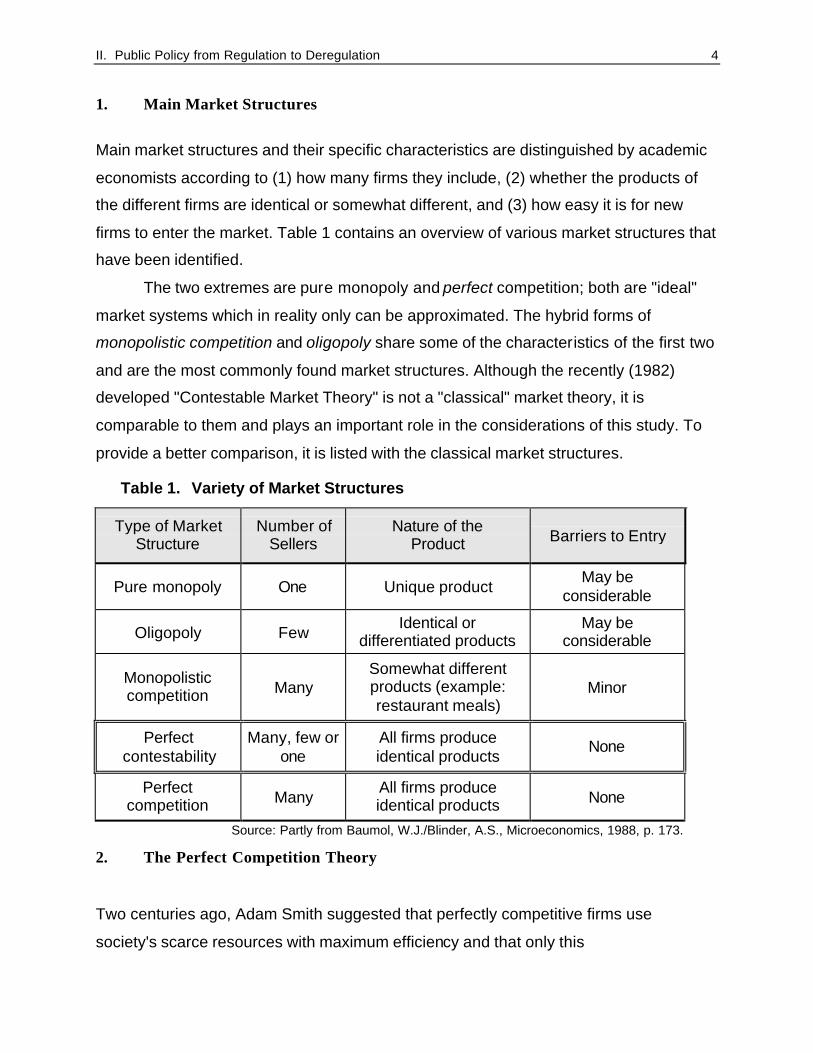

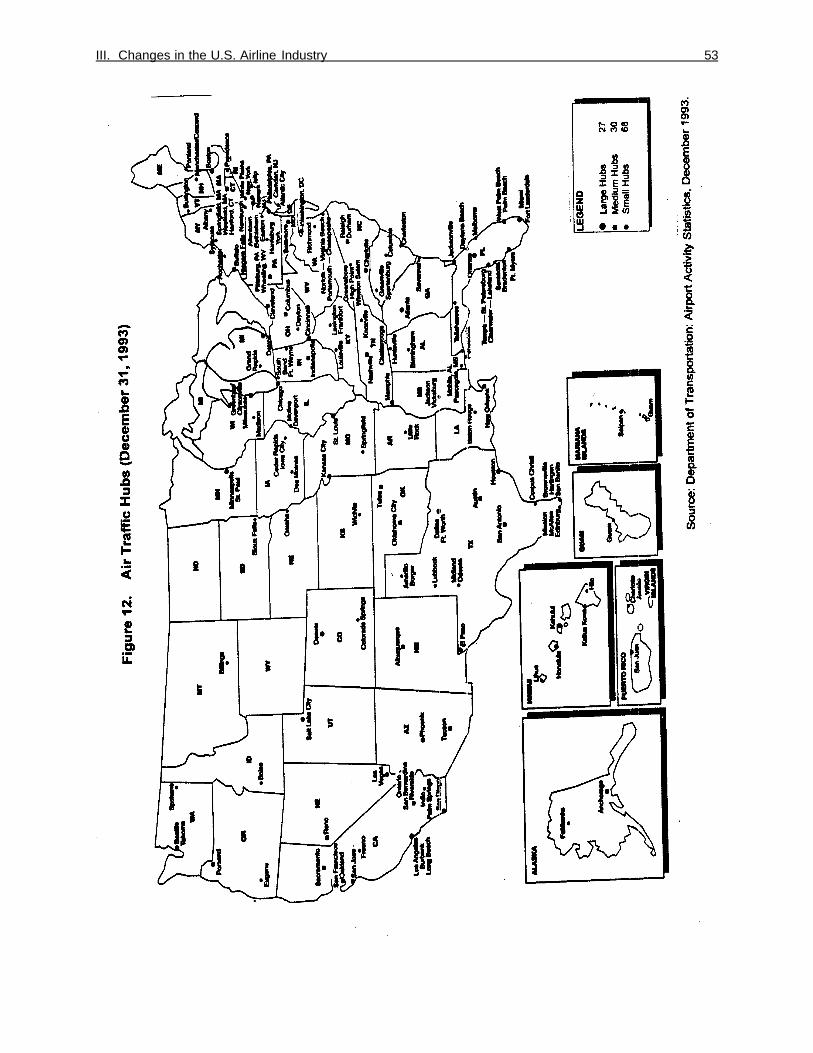

1. Main Market Structures

Main market structures and their specific characteristics are distinguished by academic

economists according to (1) how many firms they include, (2) whether the products of

the different firms are identical or somewhat different, and (3) how easy it is for new

firms to enter the market. Table 1 contains an overview of various market structures that

have been identified.

The two extremes are pure monopoly and perfect competition; both are "ideal"

market systems which in reality only can be approximated. The hybrid forms of

monopolistic competition and oligopoly share some of the characteristics of the first two

and are the most commonly found market structures. Although the recently (1982)

developed "Contestable Market Theory" is not a "classical" market theory, it is

comparable to them and plays an important role in the considerations of this study. To

provide a better comparison, it is listed with the classical market structures.

Table 1. Variety of Market Structures

Type of Market Structure

Number of Sellers

Nature of the Product Barriers to Entry

Pure monopoly One Unique product May be

considerable

Oligopoly Few Identical or

differentiated products May be

considerable

Monopolistic competition Many

Somewhat different products (example: restaurant meals)

Minor

Perfect contestability

Many, few or one

All firms produce identical products

None

Perfect competition Many

All firms produce identical products None

Source: Partly from Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 173.

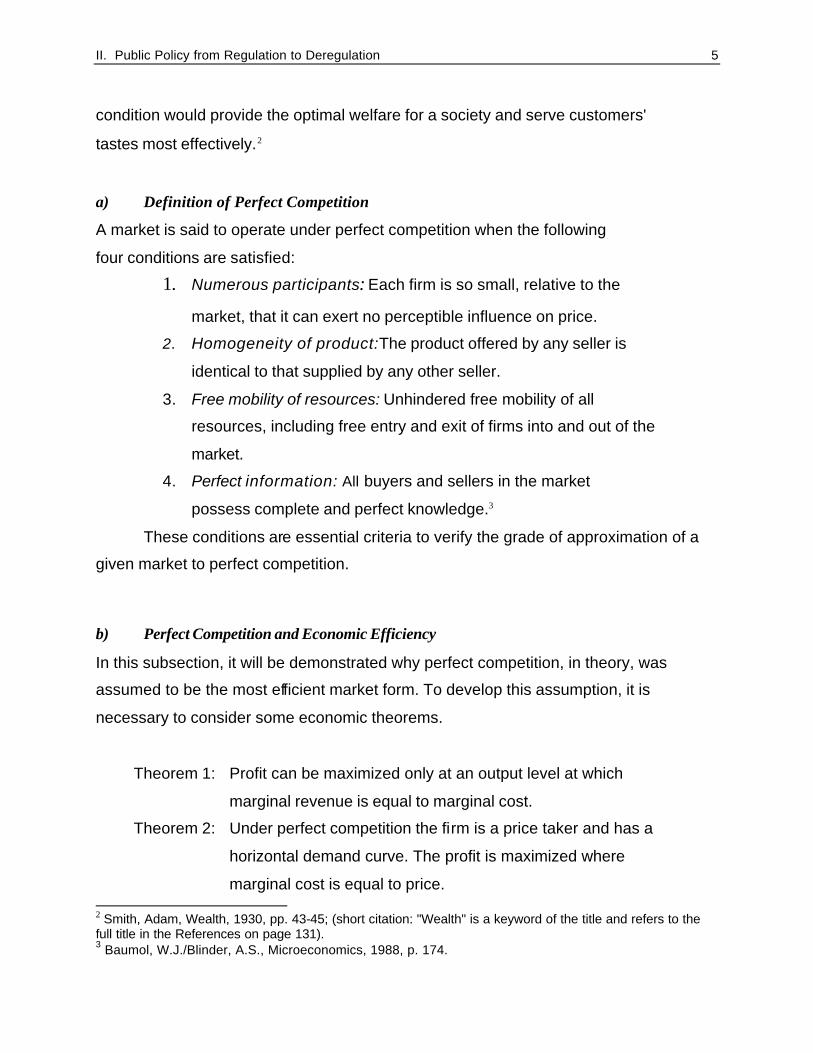

2. The Perfect Competition Theory

Two centuries ago, Adam Smith suggested that perfectly competitive firms use

society's scarce resources with maximum efficiency and that only this

II. Public Policy from Regulation to Deregulation 5

condition would provide the optimal welfare for a society and serve customers'

tastes most effectively.2

a) Definition of Perfect Competition

A market is said to operate under perfect competition when the following

four conditions are satisfied:

1. Numerous participants: Each firm is so small, relative to the

market, that it can exert no perceptible influence on price.

2. Homogeneity of product:The product offered by any seller is

identical to that supplied by any other seller.

3. Free mobility of resources: Unhindered free mobility of all

resources, including free entry and exit of firms into and out of the

market.

4. Perfect information: All buyers and sellers in the market

possess complete and perfect knowledge.3

These conditions are essential criteria to verify the grade of approximation of a

given market to perfect competition.

b) Perfect Competition and Economic Efficiency

In this subsection, it will be demonstrated why perfect competition, in theory, was

assumed to be the most efficient market form. To develop this assumption, it is

necessary to consider some economic theorems.

Theorem 1: Profit can be maximized only at an output level at which

marginal revenue is equal to marginal cost.

Theorem 2: Under perfect competition the firm is a price taker and has a

horizontal demand curve. The profit is maximized where

marginal cost is equal to price. 2 Smith, Adam, Wealth, 1930, pp. 43-45; (short citation: "Wealth" is a keyword of the title and refers to the full title in the References on page 131). 3 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 174.

II. Public Policy from Regulation to Deregulation 6

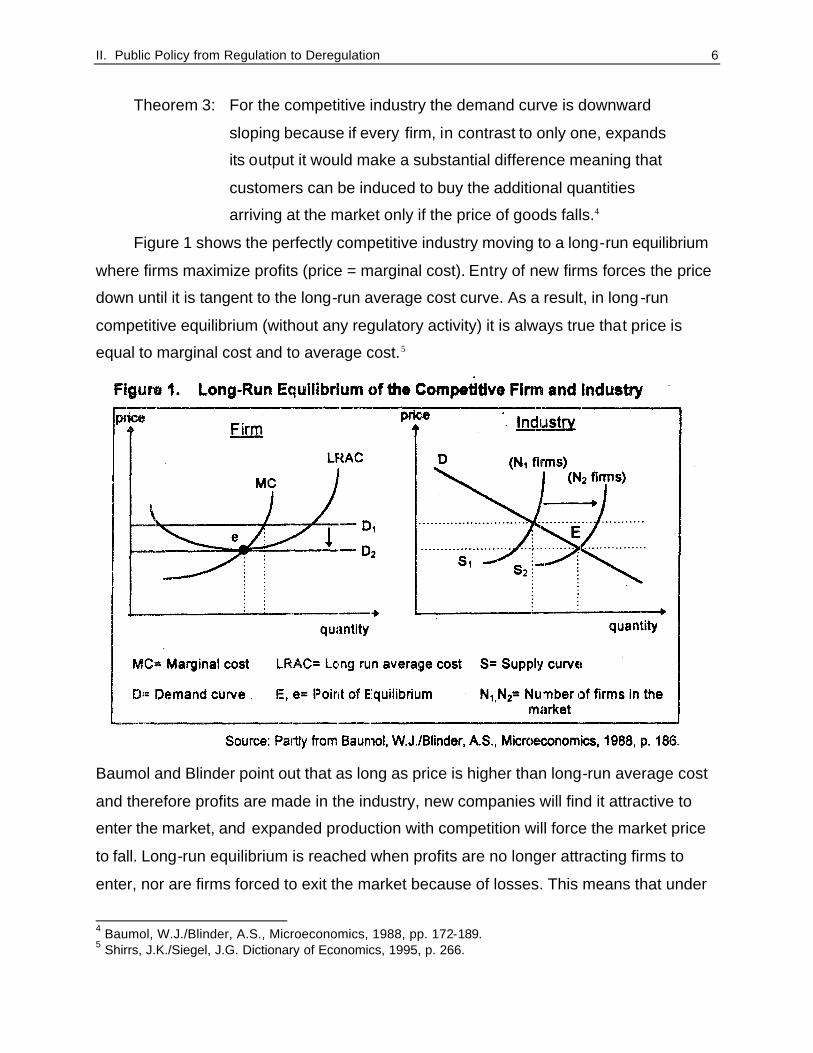

Theorem 3: For the competitive industry the demand curve is downward

sloping because if every firm, in contrast to only one, expands

its output it would make a substantial difference meaning that

customers can be induced to buy the additional quantities

arriving at the market only if the price of goods falls.4

Figure 1 shows the perfectly competitive industry moving to a long-run equilibrium

where firms maximize profits (price = marginal cost). Entry of new firms forces the price

down until it is tangent to the long-run average cost curve. As a result, in long-run

competitive equilibrium (without any regulatory activity) it is always true that price is

equal to marginal cost and to average cost.5

Baumol and Blinder point out that as long as price is higher than long-run average cost

and therefore profits are made in the industry, new companies will find it attractive to

enter the market, and expanded production with competition will force the market price

to fall. Long-run equilibrium is reached when profits are no longer attracting firms to

enter, nor are firms forced to exit the market because of losses. This means that under

4 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, pp. 172-189. 5 Shirrs, J.K./Siegel, J.G. Dictionary of Economics, 1995, p. 266.

II. Public Policy from Regulation to Deregulation 7

perfect competition, in long-run equilibrium, firms work with zero economic profit in the

economic sense. Of course, firms may earn profits in the accounting sense, because

the average cost curve includes the cost of all inputs, including the opportunity cost of

the capital which forces the firm to earn the normal economic-wide rate of profit to make

sure that investors do not exit the business with their invested capital.6

The conclusion is that in long-run equilibrium under perfect competition, every firm

produces at the minimum point on its average cost curve. Thus the outputs of competitive

industries are produced at the lowest possible cost to society and the industry reaches its

maximum efficiency.

3. The Contestable Market Theory

In the late 1970s and early 1980s, William Baumol, John Panzar, and Robert Willig

attempted to formalize the conditions under which natural monopolies could be

expected to reach efficient equilibria without regulation. They argued that optimal

price and output conditions would be achieved in any market having certain

characteristics which made it "perfectly contestable".7 They finally formulated a

general theory of contestability in 1982, four years after Congress promulgated the

Airline Deregulation Act of 1978.

a) Conditions for Perfect Contestability

Essentially, four conditions have to be fulfilled so that a market may be

considered perfectly contestable:

1. Equal Access to Economies of Scale

The first condition is that all firms in a market and potential entrants have equal

access to economies of scale and to the same technology, whether expressed as

access to competitive levels of unit costs or as equivalent access to product 6 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 184-189. 7 Baumol, W.J./Panzar, J.C./Willig, R.D., Markets, 1988.

II. Public Policy from Regulation to Deregulation 8

quality.8 The Contestable Market Theory permits natural monopolies as a

result of economies of scale.

2. Free Entry and Exit

The second condition is that a firm can enter and exit a market without entry and exit

costs, and that "sunk costs" are not present. Sunk costs are costs of resources that

have already been incurred at some point in the past whose total will not be affected by

any decision made in the present or future. For example, advertising costs during

market entry constitute sunk costs . 9 The requirement of free market entry and exit

implies that there are no "entry barriers" erected by governmental regulations or by

other firms in the market.

3. Price Sustainability

The third condition for contestability is that consumers can respond to a price reduction

set by a new firm entering the market more quickly than the incumbent firm's can

respond with a matching price cut.10 If this condition is not fulfilled, the new entrant can

not attract consumers with a lower price and therefore will find it difficult to gain market

share.

4. The "Threat of Potential Entry"

The essential point of the Contestable Market Theory is the "threat of potential entry". It

was assumed by Baumol and Blinder that if a new firm can enter and exit a market

without costs, even a natural monopolist would be forced to price at cost because of this

"threat of potential entry". If the price, of the natural monopolist were to be higher than

costs, the potential entrant would enter and offer lower prices to the consumers, Thus

8 Levine, M.E., Competition, 1987, p. 404. 9 Shim, J.EC./Siegel, J.G. Dictionary of Economics, 1995, p. 321. 10 Dempsey, P.S., Laissez-Faire, 1992, p. 222.

II. Public Policy from Regulation to Deregulation 9

the entrant would make profits before the incumbent could match the price and could go

out of business when the monopolist reacts in pricing downwards.11

b) Contestability and Industry Equilibrium

Industry equilibrium in a perfectly contestable market dominated by a natural monopoly

is only possible if the natural monopolist chooses a price that is sustainable. A

necessary premise for sustainability is "price subadditivity". Subadditivity means that it

is more expensive for two or more firms to produce an output y than it is for a natural

monopoly to produce the same output (the cost of producing the whole is less than the

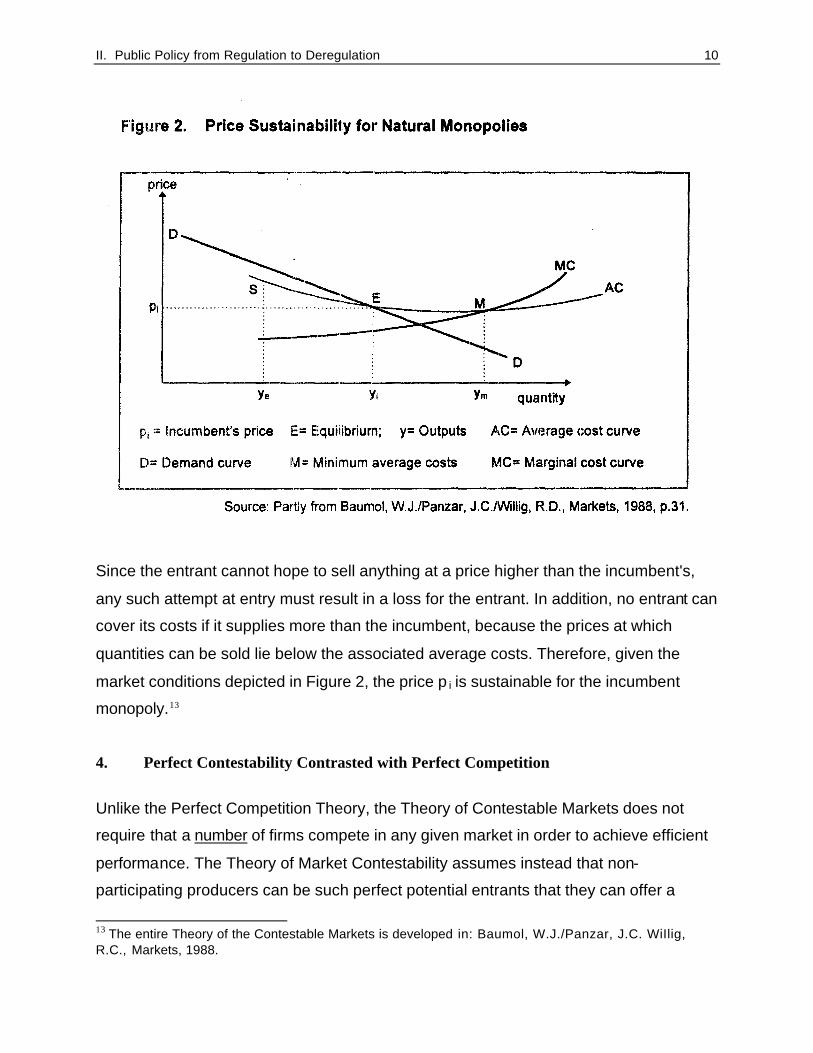

sum of the costs of producing parts). Figure 2 illustrates how, in theory, a natural

monopoly will be able to find a stationary price that covers its own costs and yet

protects it from entry.

Baumol, Panzar and Willig point out that in the case of a natural monopoly, the

rule MC < p = AC emerges as a necessary condition for equilibrium in perfectly

contestable markets.12 The price nearest MC that yields a non negative profit to the

supplier is p=AC at point E, where the demand curve intersects the average cost curve.

The authors mention that for a single-product firm, this is the rule for second-best

pricing under a zero-profit constraint (the best pricing would be the one under perfect

competition with MC=AC). In Figure 2, the demand curve cuts the average cost curve to

the left of point M, of minimum average cost. In that case, if the monopoly selects the

price p i at which the average cost curve and the demand curve intersect, any entrant

attempting to capture a segment of the market by supplying some smaller output ye

must incur an average cost S that is above the incumbent's price p i.

11 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 244. 12 Baumol, W.J./Panzar, J.C./Willig, R.D., Markets, 1988, p. 28.

II. Public Policy from Regulation to Deregulation 10

Since the entrant cannot hope to sell anything at a price higher than the incumbent's,

any such attempt at entry must result in a loss for the entrant. In addition, no entrant can

cover its costs if it supplies more than the incumbent, because the prices at which

quantities can be sold lie below the associated average costs. Therefore, given the

market conditions depicted in Figure 2, the price p i is sustainable for the incumbent

monopoly.13

4. Perfect Contestability Contrasted with Perfect Competition

Unlike the Perfect Competition Theory, the Theory of Contestable Markets does not

require that a number of firms compete in any given market in order to achieve efficient

performance. The Theory of Market Contestability assumes instead that non-

participating producers can be such perfect potential entrants that they can offer a

13 The entire Theory of the Contestable Markets is developed in: Baumol, W.J./Panzar, J.C. WiIlig, R.C., Markets, 1988.

II. Public Policy from Regulation to Deregulation 11

supply response when monopolists charge higher than competitive prices and produce

lower than competitive output. This supply response would force monopolists to

produce the optimal output and price characteristics of competitive markets.14

The Contestable Market Theory, in contrast to the Perfect Competition Theory

allows for economies of scale and natural monopolies and for only a small number of

firms. Markets which contain a few relatively large firms can be highly contestable,

though they are certainly not perfectly competitive.15 However, both market theories

claim to provide maximum efficiency and maximum welfare to society, if working under

ideal conditions, because firms are forced to price at (average) cost.

5. Reasons for Regulatory Activities

Because the market systems of perfect competition or perfect contestability may not

function ideally, governments frequently intervene in these areas. The main reasons for

regulatory activities based on the Perfect Competition Theory are (a) the

phenomenon of natural monopoly that leads to concentration, (b) the desire for.

universal service, (c) to prevent destructive competition and (d) the protection against

misinformation.16 As mentioned previously, the Contestable Market Theory has been

developed to show that a market can work efficiently without regulation, even if some of

the above phenomena (which would make regulation necessary, according to the

Perfect Competition Theory) are present. However, one reason for regulation based on

the Contestable Market Theory is the abolishment of entry barriers.

a) Economies of Scale and Scope and Natural Monopolies

One of the main reasons to regulate an industry, according to the Perfect

Competition Theory, is the existence of a natural monopoly:

14 Levine, M.E., Competition, 1987, p. 404. 15 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 244. 16 Daneke, G. A./Lemak, D.J., Reform, 1985, pp. 4-10 and Baumol, W.J./Blinder, A.S., Microeconomics, 1988, pp. 292-300.

II. Public Policy from Regulation to Deregulation 12

"A natural monopoly is an industry in which advantages of large-scale production make it possible for a single firm to produce the entire output of the market at lower average cost than a number of firms each producing a smaller quantity."17

The cost advantages of large-scale production basically stern from two effects

that can take place in a market: economies of scale and economies of scope effects.

1. Economies of Scale

Economies of scale are savings that are acquired through increases in quantities

produced. The reasons for these savings are (1) increased specialization and division of

labor and (2) use of more efficient or high-tech machinery and equipment. As the scale

of production grows, the enterprise becomes more efficient and simultaneously, the unit

costs decrease.18

2. Economies of Scope

A concept related to economies of scale is economies of scope. Economies of scope

are savings that are made possible by the simultaneous production of many different

products. The unit cost of producing one more item may be diminished when the scope

of activity broadens. An example of economies of scope in the airline industry is

advertising costs. Advertising costs per unit of serving a particular city-pair market are

lower the more city-pair markets are served, due to quantity discounts in media

purchasing.19

In industries where there are great economies of scale and scope, society will

obviously incur a significant cost penalty if it insists on maintaining a large number of

firms. If a monopoly can provide a less expensive product, it is in the society's best-

interest not to sustain free competition. If the market system is based on the Perfect

17 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 215. 18 Shim, J.K./Siegel, J.G. Dictionary of Economics, 1995, p. 118. 19 Dempsey, P.S., Laissez-Faire, 1992, p.:238.

II. Public Policy from Regulation to Deregulation 13

Competition Theory, then regulation is the adequate means to avoid exploitation by the

monopolistic firm.20

b) Universal Service

Another reason for regulation is the desire for universal service, which means the

availability of service at reasonable prices even to small communities where the small

scale of operation makes costs extremely high. In such cases, regulation can

encourage a public utility to supply services to consumers at a financial loss, permitting

at the same time higher profits on other sales. This cross-subsidization is possible only

if the firm is protected from price competition and free entry of new competitors in its

more profitable markets.21 If that protection is not provided, many new firms would enter

the business and cause prices to be driven down in those markets, with the effect that

the original supplier can no longer subsidize the unprofitable markets and small

communities would be left abandoned.

c) Destructive Competition

The third reason for regulation under perfect competition is to prevent the market from

destructive price competition in multifirm industries with large capital costs and low

marginal costs. The risk is that price competition drives the firms' prices down toward to

their marginal costs and that average costs are higher than marginal costs. As in most

industries where economies of scale are present, the average cost curve in general is

declining, which indicates that marginal costs are below average costs for one particular

output. If price is lower than average cost, the firm cannot pay its total costs in the long-

run and will go bankrupt. To prevent the firms from going bankrupt, under destructive

competition, regulation is opportune because the price can be set by regulatory

agencies.

Regulators can generally set the price in two ways: (1) they can set the price

equal to marginal cost (marginal cost pricing) or (2) they can set the price equal to

20 Baumol, W,J./Blinder, A.S., Microeconomics, 1988, p. 296. 21 Dempsey, P.S., Laissez-Faire, 19x2, p.:249.

II. Public Policy from Regulation to Deregulation 14

average cost. The latter is not desirable because, as explained in Theorem 1, firms

would not produce at that point where profits are maximized (marginal cost = marginal

revenue) and, even more importantly, the industry would not produce at its most

efficient level. The first method indicates that subsidies (government and/or cross-

subsidizing) have to be paid to the firms to avoid their bankruptcy. 22

d) Protection Against Misinformation

A final reason for regulation is to protect the environment (e.g. consumers, employees,

etc.) from being misinformed or cheated by firms and unscrupulous sellers. This is

especially true in the airline industry concerning overbooking of planes, flight

cancellations because of low passenger demand, and misleading advertising that

promises low fares for only an infinitely small number of seats.

e) Abolishment of Entry Barriers

A criterion where regulatory activities concerning the Contestable Market Theory could

be necessary is the abolishment of entry barriers. Bailey and Baumol point out that

regulators should be aware of entry barriers erected by firms or by government, and

should take steps to discourage the maintenance of those barriers. In case there are

entry barriers that arise out of technological circumstances that require heavy sunk

investments, the government should ensure equal access to the sunk facility and, if the

sunk facility is privately owned, the government should require that all firms seeking to

use the facility are given access to it, so that all users are charged the same price.23

B. Regulatory Framework Before 1978

After having given a brief overview of the reasons for regulatory activities, the regulatory

framework of the U.S. airline industry before deregulation in 1978 will now be explored.

The time before deregulation can be divided into two significant phases: (1) the phases

22 Baumol, W.J./Blinder, A.S., Microeconomics, 1988, p. 302. 23 Bailey, E. E./Baumol, W. J., Deregulation, 1984, pp. 123-125.

II. Public Policy from Regulation to Deregulation 15

without any economic regulation (from the beginning of the air transportation industry in

1918 to 1938), and (2) the phases of strict government regulation (from 1938 to 1978).

1. The History of the U.S. Airline Industry

Following is a short overview of some important acts concerning the airline industry

which were promulgated before 1978:

1918 The history of air transportation in the U.S. started in 1918 when airmail

service was inaugurated by the Army.

1925 The Kelly Act (Air Mail Act of 1925) established air transportation

autonomous from the military by permitting the postmaster general to award

contracts to private airlines for the movement of mail.

1926 The Air Commerce Act of 1926 gave jurisdiction over safety and the

maintenance of airways and navigation facilities to the Secretary of

Commerce.

1930 The McNary-Waters Act of 1930 established a formula for airmail payments

based on the amount of mail transported.

1938 In 1938 the government started the regulation era of the airline industry by

passing the Civil Aeronautics Act of 1938, the predecessor of the

1958 Federal Aviation Act of 1958. The intent of these acts was to prevent the

airline industry from suffering the effects of destructive competition that had

already occurred in the rail and motor carrier industry (the Motor Carrier Act

was passed in 1935 to stop this).24 Actually, the Federal Aviation Act of 1958

did not mean a significant amendment concerning the regulatory era.

1978 The Airline Deregulation Act of 1978 was passed by Congress.

Since the Civil Aeronautics Act of 1938, and the Airline (Deregulation Act of 1978

changed the framework of the airline industry, significantly, these acts are described in

further detail.

24 Dempsey, P.S., Laissez -Faire, 1992, pp. 159-163.

II. Public Policy from Regulation to Deregulation 16

2. The Civil Aeronautics Act of 1938

The Civil Aeronautics Act of 1938, signed into law by President Roosevelt, established

the Civil Aeronautics Authority and the Air Safety Board as independent regulatory

agencies designed to provide regulation over the air transportation industry. Essentially,

these agencies were given the authority to regulate (1) rates, (2) entry, exit, and routes,

(3) antitrust, and (4) safety.

a) The Civil Aeronautics Board

In 1940 the functions of the Air Safety Board were consolidated with the functions of the

Civil Aeronautics Authority and a new agency, the Civil Aeronautics Board , was

constituted.25 This agency regulated the airline industry until the Airline Deregulation Act

of 1978 was promulgated. After 1978 it continued regulating the airline industry with

reduced authority until 1985, when it disappeared completely. Some of its functions

were transferred to the U.S. Department of Transportation and to the Department of

Justice.

b) Regulated Market Parameters

1. Rates:

The Civil Aeronautics Board was given the authority to suspend or establish air fares

and determine whether proposed rates were "just and reasonable".26 The Board's

regulation of fare levels can be divided into four distinct phases:27

1. In the first phase, airfares were conventionally set at the prevailing first-

class rail fare.

25 U.S. Public Law: Reorganization Plan No. IV of 1940, Section 7 (a) and (b). 26 U.S. Public Law: Civil Aeronautics Act of 1938, Sec. 403 (a) to (d) and Sec. 404 (a) to (c). 27 Bailey, E.E./Graham, D.R./Kaplan, D.P., Deregulating, 1985, p. 16.

II. Public Policy from Regulation to Deregulation 17

2. In the second, after the first formal review of fares in 1942, the

Board approved fare increases but without any formal guidance

as to the desired level of earnings for the industry.

3. In the third, fares were set to achieve an average 10.5 percent rate of

return for the industry based on actual industry operating costs.

4. In the fourth, the Board set fares to get a 12 percent return

based on standard industry load factors and seating density and

standardized accounting conventions.28

In all four phases the Board's focus was on overall industry profitability rather

than on the relationship between fares and costs in particular markets.

2. Entry, Exit and Routes:

The Civil Aeronautics Board was authorized to prescribe which routes should be flown,

which communities would receive air service, and to designate the specific carriers

which would be permitted to serve such markets. The Board could grant or deny

certificates of "public convenience or necessity".29

As internal entry criteria of the Civil Aeronautics Board, the following four

questions were to be considered in any application for new service:

1. Will the new service usefully serve the public, and be responsive to the

public need?

2. Can and will this service be served adequately by existing routes or

carriers?

3. Can the new service be served by the applicant without impairing the

operations of existing carriers contrary to the public interest?

4. Will any cost of the proposed service to the government be outweighed by

the benefit that will accrue to the public from the new service?30

In fact, between 1938 and 1978, the Civil Aeronautics Board granted no new

authority to domestic "trunk carriers"31 in the belief that it would reduce the possibility of

28 Dempsey, P.S., Laissez-Faire, 1992, p. 167. 29 U.S. Public Law: Civil Aeronautics Act of 1938, Sec. 401 (a) to (n) and Sec. 402 (a) to (h). 30 Dempsey, P.S., Laissez-Faire, 1992, p. 168.

II. Public Policy from Regulation to Deregulation 18

destructive competition among airlines.32 Exit of firms out of the market was controlled

by the Civil Aeronautics Board, as well. Actually, the Board did not permit a single exit

or bankruptcy among the trunk carriers in the four decades of regulation.

3. Antitrust:

The Civil Aeronautics Board also had the authority to approve or disapprove intercarrier

transactions, such as consolidations, mergers and acquisitions. 33 It permitted, for

example, the mergers of the 16 trunk carriers of 1938 into the 11 that existed in 1978

and the mergers of 19 local-service carriers into the 8 in 1978.34

4. Safety:

After the Civil Aeronautics Authority was consolidated with the Air Safety Board to

become the Civil Aeronautics Board (CAB) in 1940, the CAB was given the authority to

set minimum safety standards and to issue air carrier operating certificates. Its duty was

also to inspect the maintenance of equipment in air transportation.

3. The Federal Aviation Act of 1958

The Federal Aviation Act of 1958 was promulgated for the following purpose:

"To continue the Civil Aeronautics Board as an agency of the United States, to create a Federal Aviation Agency, to provide for the regulation and promotion of civil aviation in such manner as to best foster its development and safety, and to provide for the safe and efficient use of the airspace by both civil and military aircraft, and for other purposes.35 In general, the Federal Aviation Act of 1958 did not mean a change in the

economic regulatory era of the airline industry. The Civil Aeronautics Board continued its

work and another agency, the Federal Aviation Agency, was created to execute the

regulation of the airline industry with special focus on safety concerns. The laws

31 "Trunk carriers" were classified by the Civil Aeronautics Board as the airlines which were granted permanent operating rights between any two cities within the United States. In 1981 they were renamed "major carriers". 32 Wilson, G.S., Airport, 1993, pp. 7-9. 33 U.S. Public Law: Civil Aeronautics Act of 1938: Sec 408. 34 Dempsey, P.S., Laissez-Faire, 1992, p. 174. 35 U.S. Public Law 85-726: The Federal Aviation Act of 1958: August 23.1958: Introduction.

II. Public Policy from Regulation to Deregulation 19

concerning the economic regulation of the airlines remained unchanged, compared to the

Civil Aeronautics Act of 1938.

C. Rationale for Deregulation

This section examines the criticisms of regulation in the airline industry and describes the

rationale of the Civil Aeronautics Board in the late 1970s to deregulate the domestic

aviation industry. Congressional scrutiny of arguments for deregulating the airline industry

began with a series of hearing in 1975 under a Senate subcommittee chaired by Edward

Kennedy. The principal criticism concerning the economic regulation in the airline industry

was that pricing and entry restrictions resulted in:36

• insufficient price competition

• excessive service

• inflated airline costs

• less than adequate profits

• high airfares

• misallocation of resources

• encouraged carrier inefficiencies

• excess capacity

• artificial barriers to entry

The Civil Aeronautics Board, under Alfred Kahn as its Chairman, considered the airline

market performance without regulatory intervention as a market with approximately "perfect

competition".37 The Kennedy Subcommittee concluded:

"The airline industry is potentially highly competitive, but the Board's system of regulation discourages the airlines from competing in price and virtually forecloses new firms from entering the industry. The result does not mean high profits. Instead, the airlines - prevented from competing in price - simply channeled their competitive energies toward costier service: more flights, more planes, more frills. ... "38

36 Wilson, G.S., Airport, 1993, p. 9. 37 Levine, M.E., Competition, 1987, p. 400. 38 S e n a t e Subcommittee on Administrative Practice and Procedure of the-Judiciary Committee, 94th Congress, 1st Session, Civil Aeronautics Board Practices and Procedures, pp. 207-8 (1976) (As cited by: Dempsey, P.S., Laissez -Faire, 1992).

II. Public Policy from Regulation to Deregulation 20

On its way towards, an economically deregulated airline industry, the Civil Aeronautics

Board made several assumptions to justify the application of the Perfect Competition Theory.

These assumptions are described in the following sections.

1. No Economies of Scale Effects Expected

The main assumptions of the economists employed by the Civil Aeronautics Board was

that in the airline industry there were no significant economies of scale. As previously

explained, economies of scale effects would lead to "natural monopolies" and prohibit

perfect competition. The Civil Aeronautics Board argued that in the absence of any cost

advantages of big firms over small, there would be no motive to merge and the Board

denied that the air transport industry was a natural monopoly due to falling unit costs.39

Some deregulation proponents insisted that even if there would be natural

monopoly effects in the airline industry, these characteristics need not be a problem,

because according to the Contestable Market Theory, a natural monopolist would be

forced to price at cost because of the "threat of potential entry".

2. Ease of Entry and Exit

As aircraft are highly mobile inputs of the airline industry, the Civil Aeronautics Board

emphasized the ease of entry and exit of that industry which is an important condition

for the application of the Perfect Competition Theory. It was argued that aircraft could

be acquired for market entry (1) by reassigning them from a less attractive market, (2)

by acquiring them from a firm which was using them less profitably, or (3) by leasing

them. 40 These aircraft could then be operated using public airports and airways, while

airlines organized or rented the necessary ground services. If commercial results would

not justify continued operations by a particular firm in a particular market, aircraft could

be sold or returned to lessors easily. Ground services as well could easily be dismantled

and therefore exit from a market would then occur with a minimum of losses from sunk

costs. 39 Dempsey, P.S., Laissez-Faire, 1992, p. 221. 40 Levine, M.E., Competition, 1987, p 400.

II. Public Policy from Regulation to Deregulation 21

3. The Texas and California Experience

In Texas and California, two states in which entry was not regulated as strictly as in the

other states (in other areas, however, they were regulated as strict as the other states),

"new entrant" operators, such as Southwest Airlines or Pacific Southwest Airlines had

significantly lower air fares and higher load factors. California did not control entry at all

until 1965 and the Texas Aeronautics Commission permitted entry by intrastate airlines

to compete with CAB-certificated airlines. Because of the favorable performance of

these two less-regulated markets and other already deregulated markets, the Civil

Aeronautics Board assumed that under deregulation, the entire airline industry in the

United States would be able to offer lower rates to passengers by reducing their costs

and increasing load factors.41 However, a difference between California and Texas and

the other states In the United States is that these two had a large amount of intrastate

traffic between Houston and Texas and Los Angeles and San Francisco.

All these factors led the Civil Aeronautics Board to predictions that price, output

and, by implication, firm selection behavior in deregulated airline markets, would

generally approximate that of perfect competition. Perfect competition implied (1) cost-

based pricing, (2) survival of low cost producers, and (3) disappearance of service

competition generated by regulated prices fixed at too high of levels. The conditions for

perfect contestability - equal access to economies of scale, few sunk costs and price

sustainability - also were seen to be fulfilled by the airline industry and there were no

doubts that a deregulation of the airline industry would be successful for both airline

companies and customers. In 1978 the Airline Deregulation Act was promulgated.42

D. The Airline Deregulation Act of 1978

In 1978, Congress passed and President Carter signed into law the Airline Deregulation

Act of 1978, which (1) dismantled the regulatory umbrella that had traditionally shielded

the industry from destructive competition, and (2) abolished the Civil Aeronautics Board

41 Dempsey, P.S., Laissez-Faire, 1992 and Levine, M.E., Competition, 1987, pp. 40 42 Levine, M.E., Competition, 1 9 8 7 , p . 4 0 3 .

II. Public Policy from Regulation to Deregulation 22

(as of 1985).43 The underlying theory of this legislation was that liberalized entry and

pricing would force carriers to adhere to the competitive pressures of the marketplace to

provide the range of price and service options desired by the public. The Airline

Deregulation Act of 1978 actually does not constitute a separate body of legislation but

instead amends several pieces of existing legislation, of which the Federal Aviation Act of

1958 (as the amended version of the Civil Aeronautics Act of 1988) is the most

significant.

l. Important Changes in Public Law

The Airline Deregulation Act of 1978 was promulgated for the following purpose:

"To amend the Federal Aviation Act of 1958, to encourage, develop, and attain an air transportation system which relies on competitive market forces to determine the quality, variety, and price of air services, and for other purposes.44

In summary, the most important immediate effects of the Airline Deregulation Act

of 1978 were:

1. Shifted Burden of Proof for Easy Market Entry

The burden of proof in route authority cases was shifted from the need for a positive

showing of the applicant that its entry is required by public convenience and

necessity, to a showing by opponents that entry of the applicant is inconsistent with

public convenience and necessity.

2. Automatic Market Entry Program

To a limited degree, automatic market entry was provided, which required no

Board review of approval. Airlines could enter the market with almost no

restriction.

43 Dempsey, P.S., Laissez -Faire, 1992, p. 193. 44 Public Law 95-504, Airline Deregulation Act of 1978, 92 STAT. 1705.

II. Public Policy from Regulation to Deregulation 23

3. Dormant Route Authority

Carriers were allowed to obtain route authority for routes tha t were not being

flown by the carriers that had been certified to fly them.

4. Fares

A statutory zone of reasonableness for fares was set, which was to be adjusted as

airline costs changed and within which airlines could vary fares without permission

from the Civil Aeronautics Board.

5. Small Community Service.

A ten-year Essential Air Service Program should ensure air service to small

communities, with government subsidies for local services to be phased out within six

years.45

The Airline Deregulation Act of 1978 determined a gradual relaxation of the

CAB's regulation of the industry, with full rate and route authority, although the fare

flexibility provisions, particularly with respect to discount fares, were less broad than

the fare policies the Board had already adopted. In the following years after

deregulation, the Civil Aeronautics Board successively lost its authority completely.

The fading authority of the Civil Aeronautics Board will be shown in the next section.

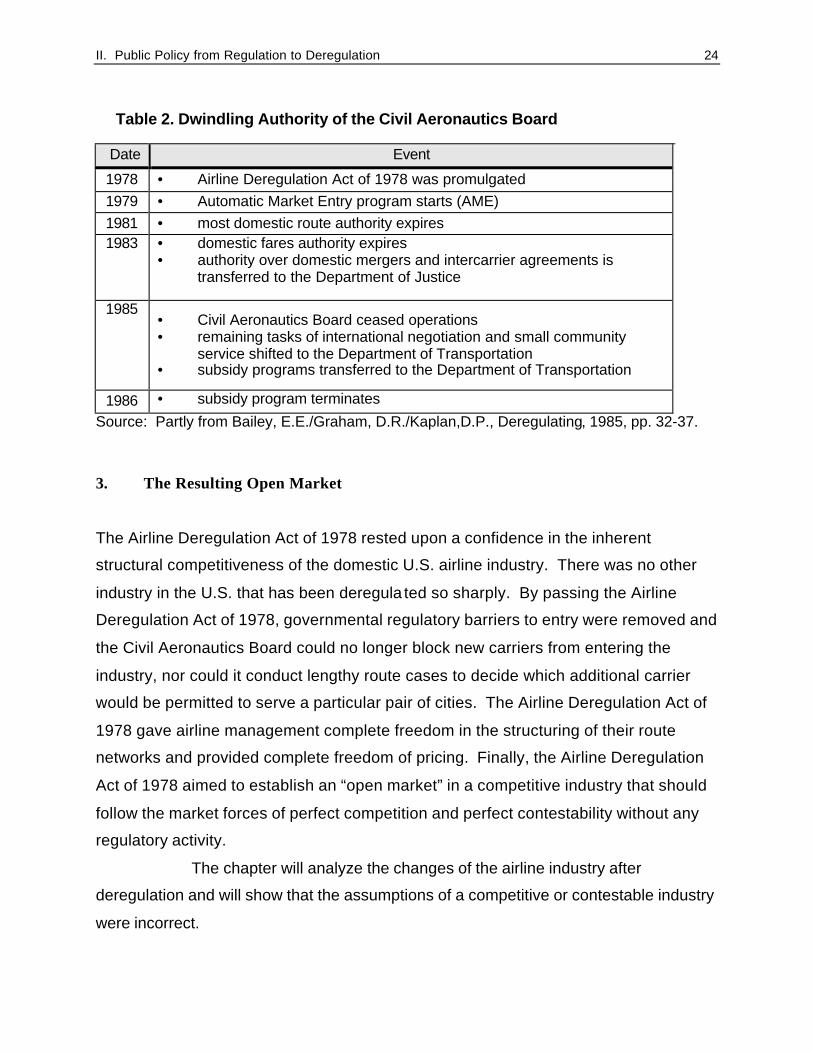

2. Dwindling Authority off the Civil Aeronautics Board

Table 2 shows the decline of the Civil Aeronautics Board from 1978 to January 1,

1985. During this period, the Board lost its authority over fares, subsidies and routes.

Some of the Boards' functions were transferred to the Department of Transportation

and the Department of Justice.

45 Bailey, E.E./Graham, D.R./Kaplan, D.P., Deregulating,1985, pp. 34ff

II. Public Policy from Regulation to Deregulation 24

Table 2. Dwindling Authority of the Civil Aeronautics Board

Date Event

1978 • Airline Deregulation Act of 1978 was promulgated 1979 • Automatic Market Entry program starts (AME) 1981 • most domestic route authority expires 1983 • domestic fares authority expires

• authority over domestic mergers and intercarrier agreements is transferred to the Department of Justice

1985

• Civil Aeronautics Board ceased operations • remaining tasks of international negotiation and small community

service shifted to the Department of Transportation • subsidy programs transferred to the Department of Transportation

1986 • subsidy program terminates _ Source: Partly from Bailey, E.E./Graham, D.R./Kaplan,D.P., Deregulating, 1985, pp. 32-37.

3. The Resulting Open Market

The Airline Deregulation Act of 1978 rested upon a confidence in the inherent

structural competitiveness of the domestic U.S. airline industry. There was no other

industry in the U.S. that has been deregula ted so sharply. By passing the Airline

Deregulation Act of 1978, governmental regulatory barriers to entry were removed and

the Civil Aeronautics Board could no longer block new carriers from entering the

industry, nor could it conduct lengthy route cases to decide which additional carrier

would be permitted to serve a particular pair of cities. The Airline Deregulation Act of

1978 gave airline management complete freedom in the structuring of their route

networks and provided complete freedom of pricing. Finally, the Airline Deregulation

Act of 1978 aimed to establish an “open market” in a competitive industry that should

follow the market forces of perfect competition and perfect contestability without any

regulatory activity.

The chapter will analyze the changes of the airline industry after

deregulation and will show that the assumptions of a competitive or contestable industry

were incorrect.

CHAPTER III

CHANGES IN THE U.S. AIRLINE INDUSTRY

In Chapter III, changes in the U.S. airline industry since deregulation are analyzed.

Section A examines the developments in the airline industry, seen as one market, and

provides an overview of the changes in the structure of the industry. Section B deals

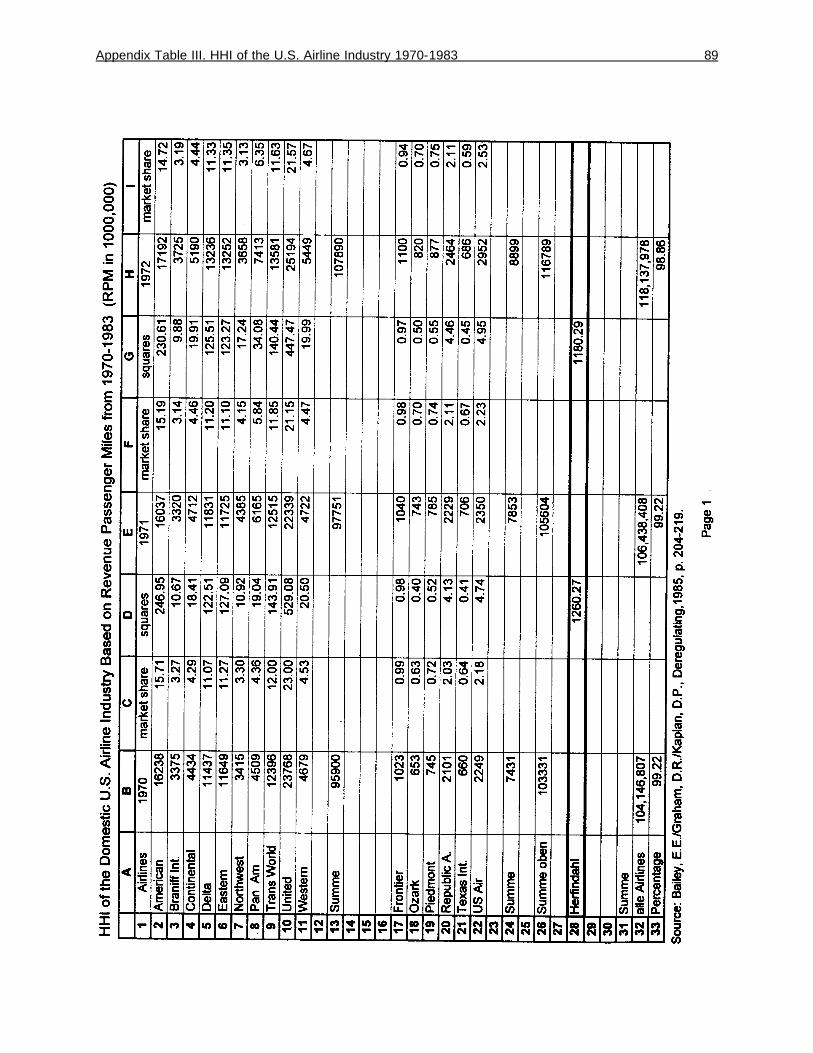

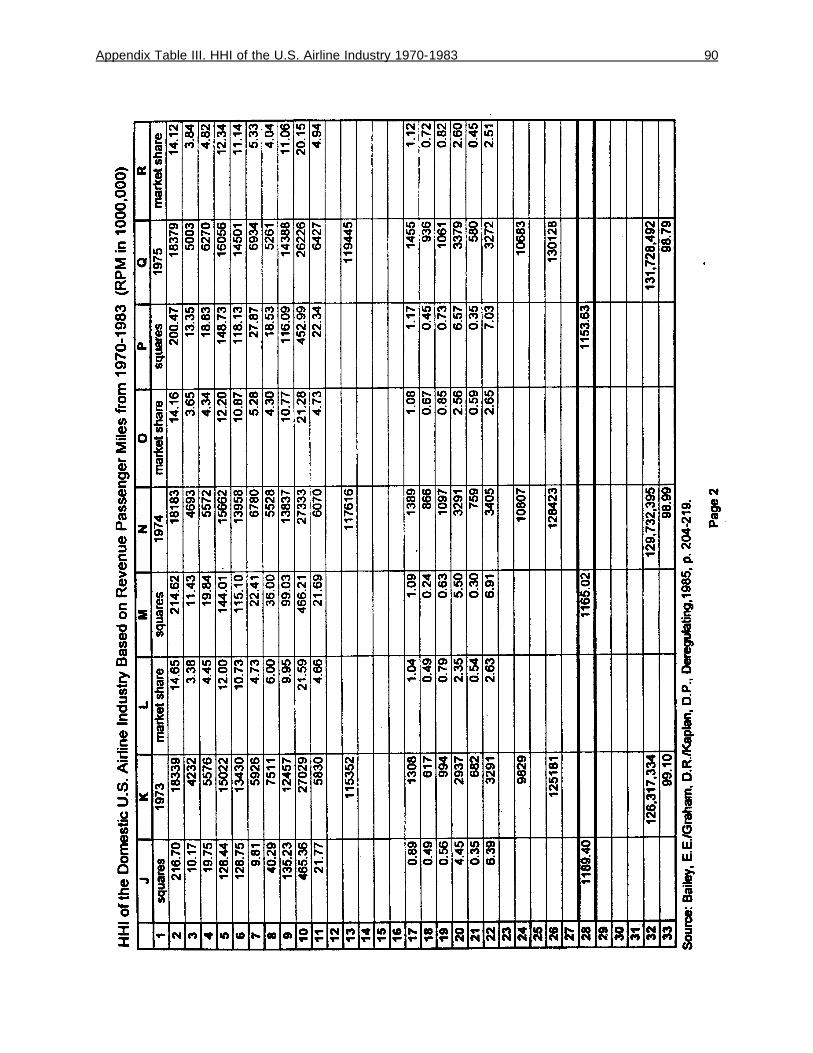

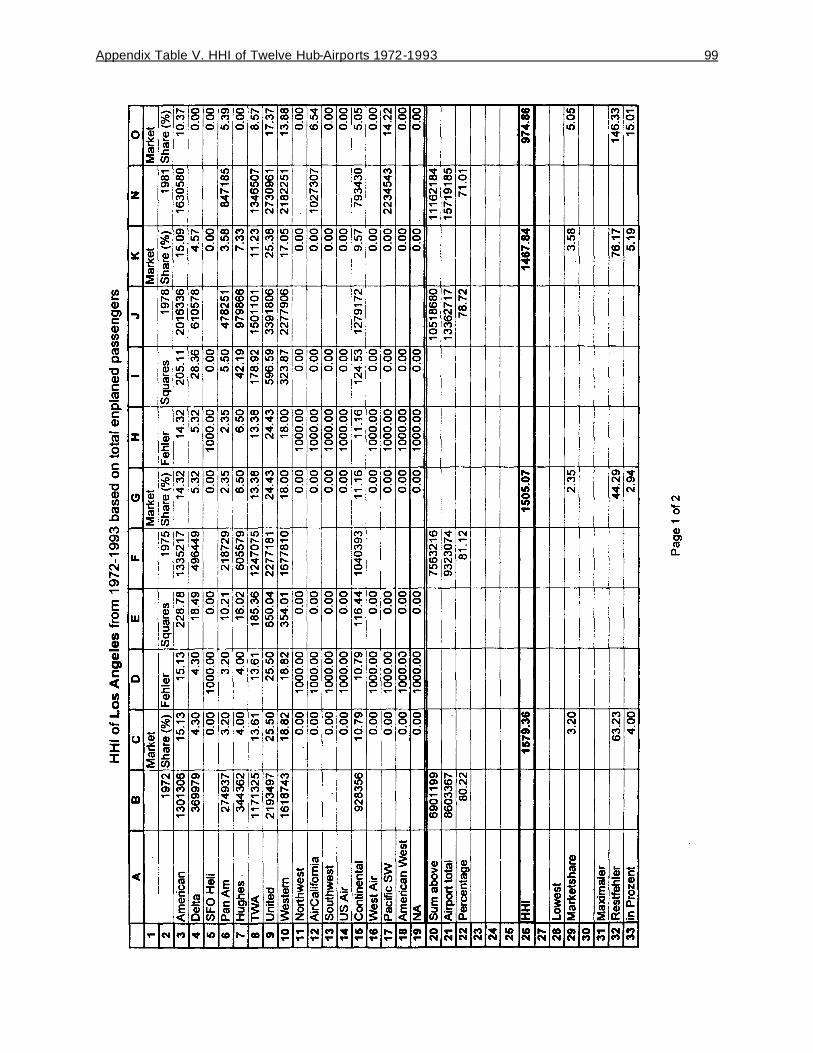

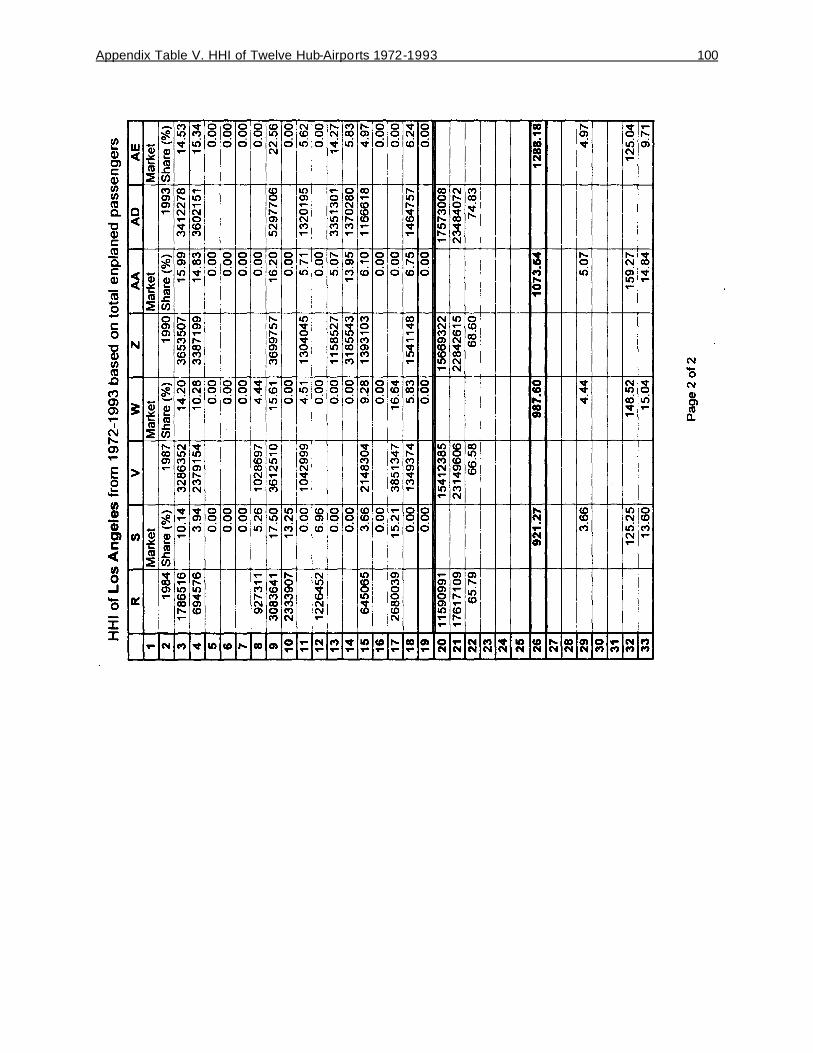

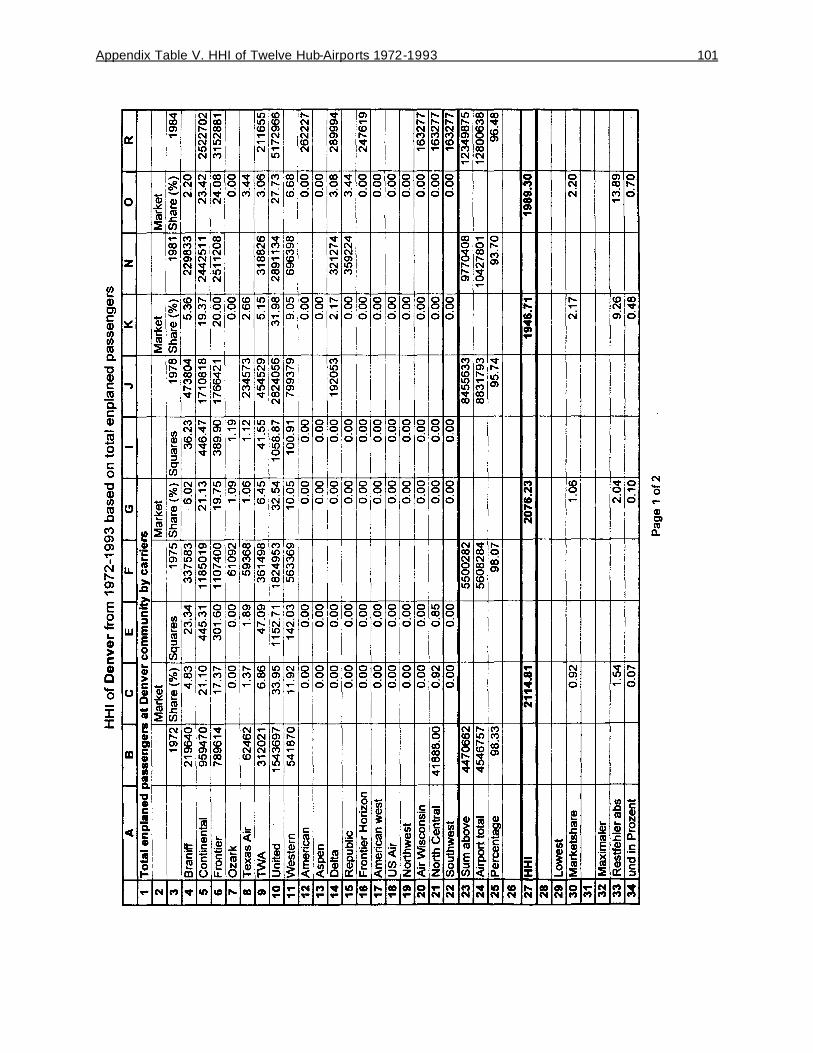

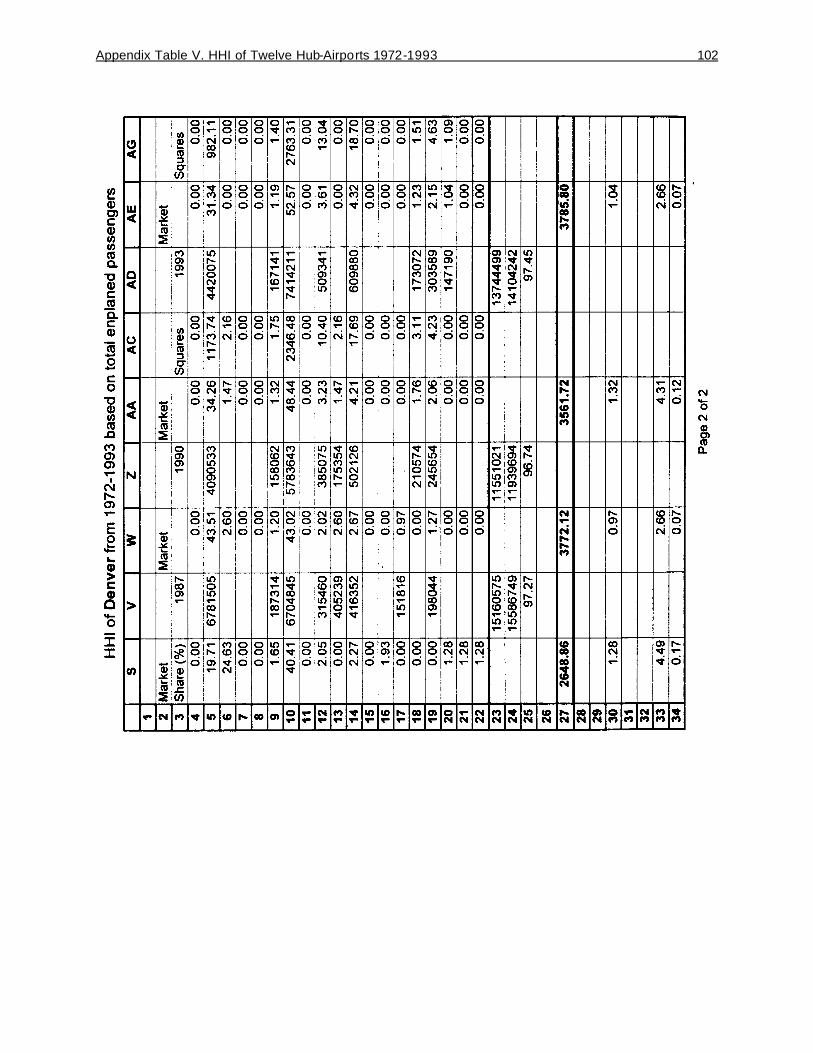

with the changes in concentration. Industry concentration, as well as the concentration

at twelve selected large hub-airports, are measured by the Herfindahl-Hirschman Index

to analyze tendencies towards higher concentration or monopolization.

A. Market Developments and Industry Structure

This section will focus on the tendencies of the airline industry in the United States

concerning growth, capacity and concentration, which are reflected by parameters such

as revenue passenger miles, available seat miles, and load factor. Merger activities,

acquisitions and bankruptcies in the airline industry led to significant changes in the

industry's structure. These activities, as well as an overview of the different types of

airlines in the United States today, will be regarded in this section.

The Hub-and-Spoke Route System is applied by all major airlines and constitutes

the dominating route structure system today. It has an impact on both passengers and

airline management. Advantages and disadvantages of this route structure system also

are explained briefly in this section.

1. Types of Airlines

Airlines in the United States are distinguished in different categories due to the amount

of their revenue. The different categories are "majors", "nationals" and "regionals".

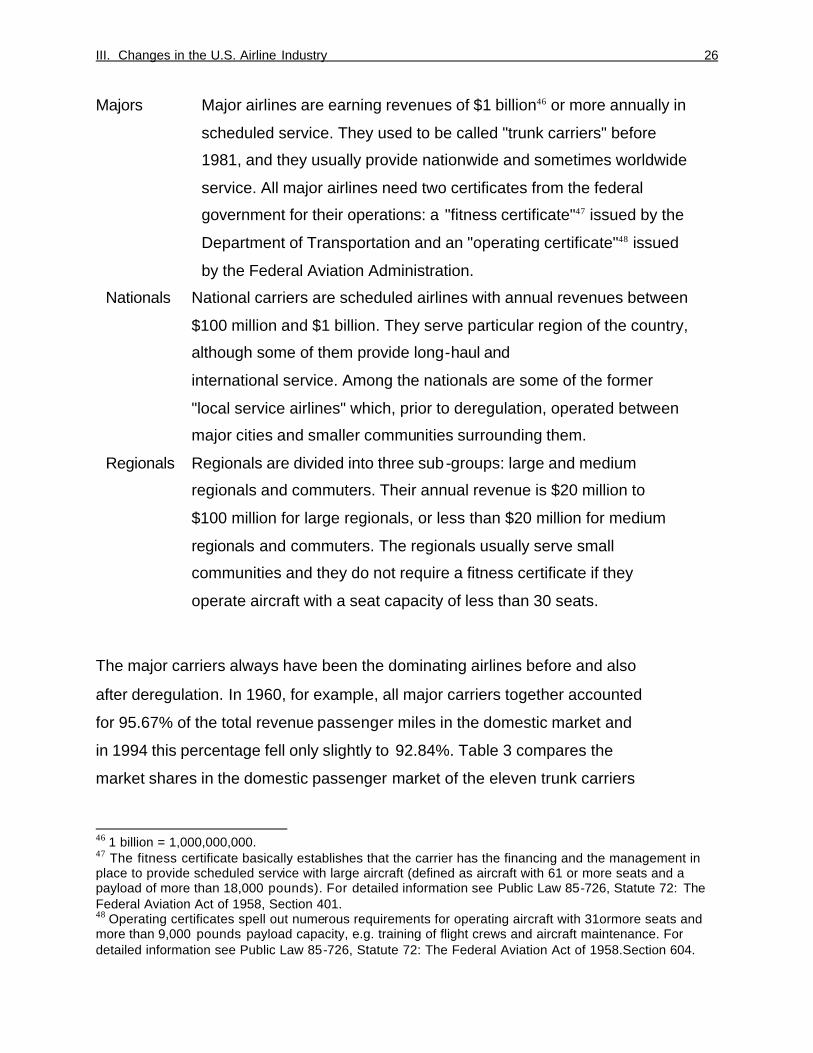

III. Changes in the U.S. Airline Industry 26

Majors Major airlines are earning revenues of $1 billion46 or more annually in

scheduled service. They used to be called "trunk carriers" before

1981, and they usually provide nationwide and sometimes worldwide

service. All major airlines need two certificates from the federal

government for their operations: a "fitness certificate"47 issued by the

Department of Transportation and an "operating certificate"48 issued

by the Federal Aviation Administration.

Nationals National carriers are scheduled airlines with annual revenues between

$100 million and $1 billion. They serve particular region of the country,

although some of them provide long-haul and

international service. Among the nationals are some of the former

"local service airlines" which, prior to deregulation, operated between

major cities and smaller communities surrounding them.

Regionals Regionals are divided into three sub-groups: large and medium

regionals and commuters. Their annual revenue is $20 million to

$100 million for large regionals, or less than $20 million for medium

regionals and commuters. The regionals usually serve small

communities and they do not require a fitness certificate if they

operate aircraft with a seat capacity of less than 30 seats.

The major carriers always have been the dominating airlines before and also

after deregulation. In 1960, for example, all major carriers together accounted

for 95.67% of the total revenue passenger miles in the domestic market and

in 1994 this percentage fell only slightly to 92.84%. Table 3 compares the

market shares in the domestic passenger market of the eleven trunk carriers

46 1 billion = 1,000,000,000. 47 The fitness certificate basically establishes that the carrier has the financing and the management in place to provide scheduled service with large aircraft (defined as aircraft with 61 or more seats and a payload of more than 18,000 pounds). For detailed information see Public Law 85-726, Statute 72: The Federal Aviation Act of 1958, Section 401. 48 Operating certificates spell out numerous requirements for operating aircraft with 31ormore seats and more than 9,000 pounds payload capacity, e.g. training of flight crews and aircraft maintenance. For detailed information see Public Law 85-726, Statute 72: The Federal Aviation Act of 1958.Section 604.

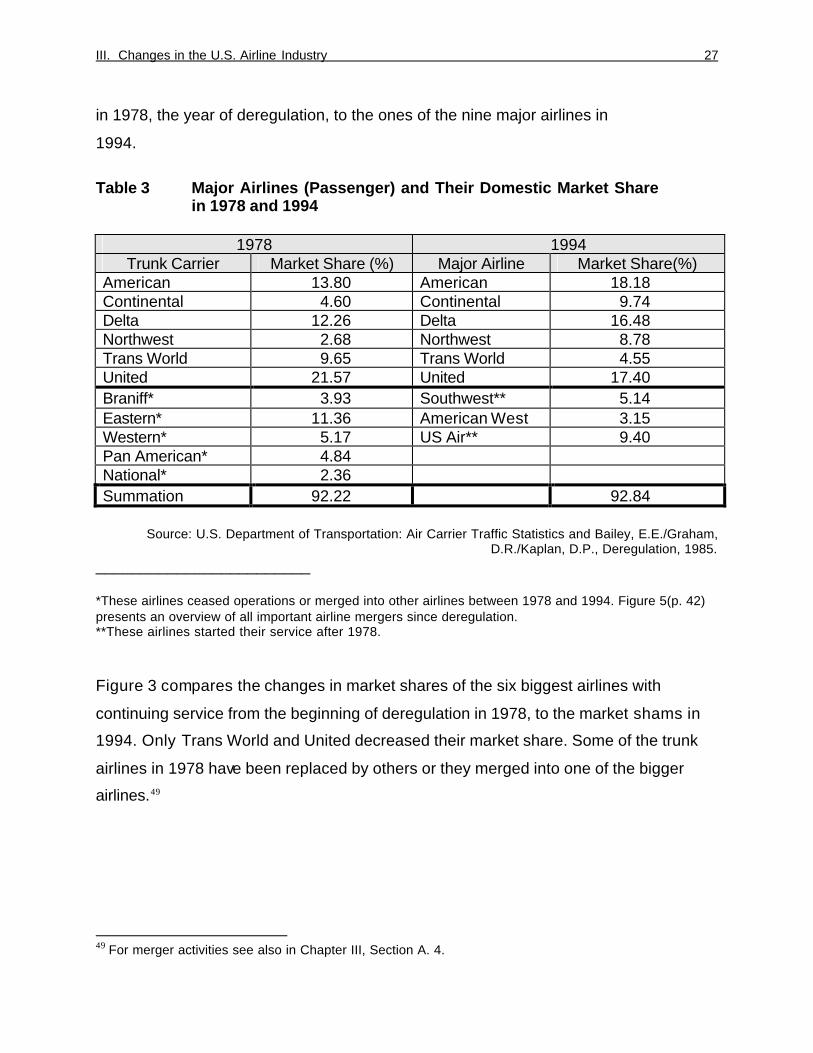

III. Changes in the U.S. Airline Industry 27

in 1978, the year of deregulation, to the ones of the nine major airlines in

1994.

Table 3 Major Airlines (Passenger) and Their Domestic Market Share in 1978 and 1994

1978 1994 Trunk Carrier Market Share (%) Major Airline Market Share(%)

American 13.80 American 18.18 Continental 4.60 Continental 9.74 Delta 12.26 Delta 16.48 Northwest 2.68 Northwest 8.78 Trans World 9.65 Trans World 4.55 United 21.57 United 17.40 Braniff* 3.93 Southwest** 5.14 Eastern* 11.36 American West 3.15 Western* 5.17 US Air** 9.40 Pan American* 4.84 National* 2.36 Summation 92.22 92.84

Source: U.S. Department of Transportation: Air Carrier Traffic Statistics and Bailey, E.E./Graham,

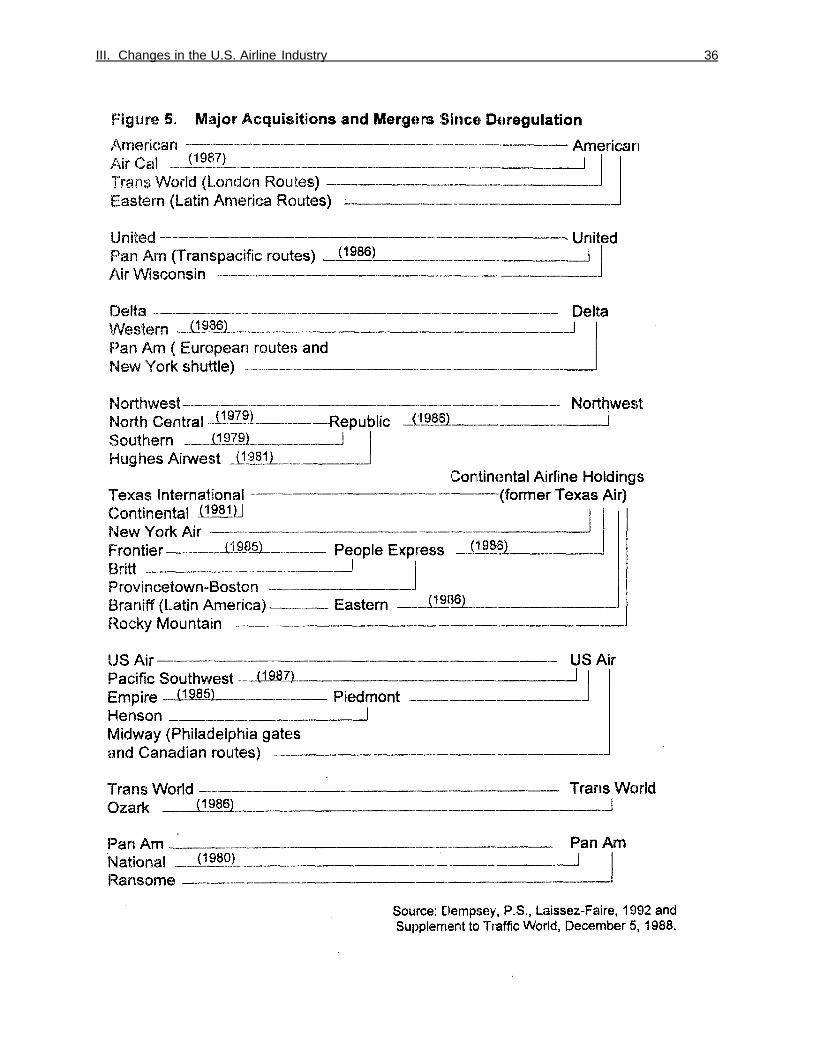

D.R./Kaplan, D.P., Deregulation, 1985. ________________________ *These airlines ceased operations or merged into other airlines between 1978 and 1994. Figure 5(p. 42) presents an overview of all important airline mergers since deregulation. **These airlines started their service after 1978.

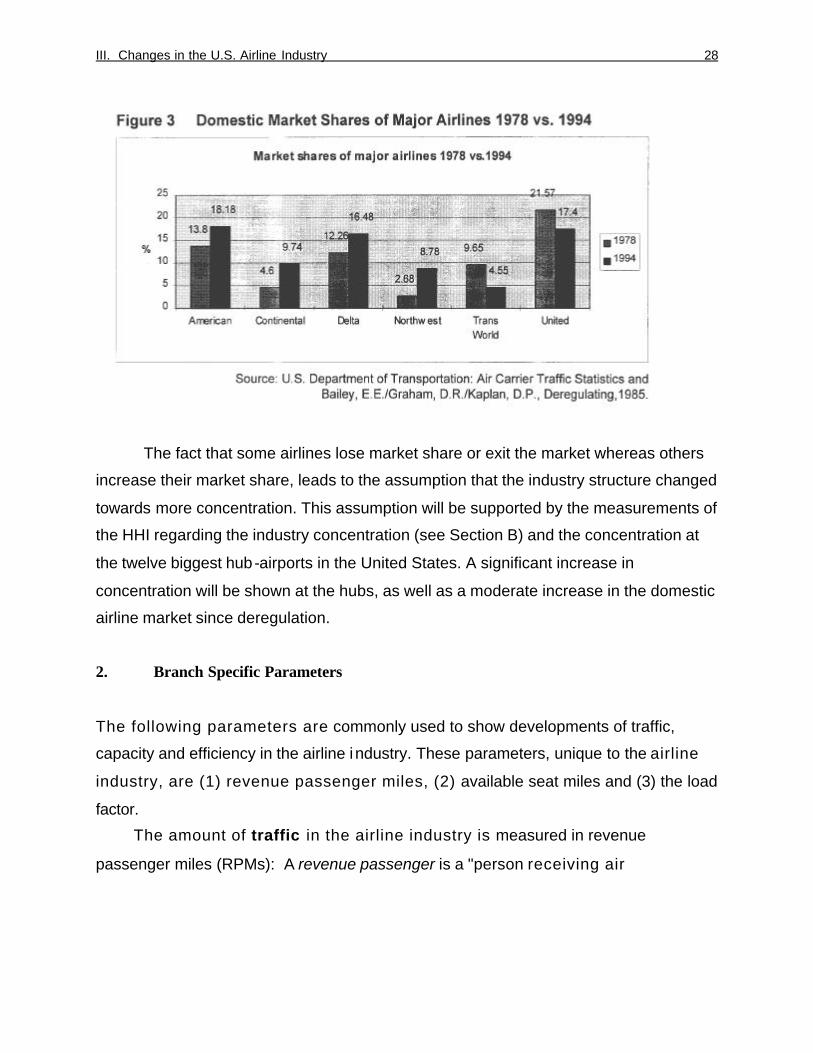

Figure 3 compares the changes in market shares of the six biggest airlines with

continuing service from the beginning of deregulation in 1978, to the market shams in

1994. Only Trans World and United decreased their market share. Some of the trunk

airlines in 1978 have been replaced by others or they merged into one of the bigger

airlines.49

49 For merger activities see also in Chapter III, Section A. 4.

III. Changes in the U.S. Airline Industry 28

The fact that some airlines lose market share or exit the market whereas others

increase their market share, leads to the assumption that the industry structure changed

towards more concentration. This assumption will be supported by the measurements of

the HHI regarding the industry concentration (see Section B) and the concentration at

the twelve biggest hub-airports in the United States. A significant increase in

concentration will be shown at the hubs, as well as a moderate increase in the domestic

airline market since deregulation.

2. Branch Specific Parameters

The following parameters are commonly used to show developments of traffic,

capacity and efficiency in the airline industry. These parameters, unique to the airline

industry, are (1) revenue passenger miles, (2) available seat miles and (3) the load

factor.

The amount of traffic in the airline industry is measured in revenue

passenger miles (RPMs): A revenue passenger is a "person receiving air

III. Changes in the U.S. Airline Industry 29

transportation for an air carrier for which remuneration is received by the carrier."

People who receive reduced air fares are not included in this definition.50

One revenue passenger mile is one revenue passenger transported one mile

in revenue service. Revenue passenger miles are computed by summation of the

products of the revenue aircraft miles flown on each inter-airport hop multiplied by the

number of revenue passengers carried on that hop. The revenue passenger miles are

generally used to measure the amount of traffic in the airline industry and to compare

the industry growth throughout the years. They are used as well to calculate the market

shares of each airline in a particular market. The market shares are concluded as the

percentage revenue passenger miles flown by a specific airline divided by the total

amount of revenue passenger miles in the industry.

Another area of interest is the development of capacity. The standard measure

of capacity used by the Department of Transportation, is the available seat mile.

Available seat miles are "the aircraft miles flown in each inter-airport hop multiplied by

the number of seats available on that hop for revenue passenger use."51 If an airline for

example uses an aircraft with a capacity of 200 seats, available for revenue passengers

for a flight of 500 miles, the available seat miles are 100,000. This parameter gives

information about the capacity of an airline on a particular flight or on a certain route. It

also is used to measure the capacity of the whole airline industry as the aggregation of

all airlines in a market.

The load factor is the ratio of revenue passenger miles to available seat miles. It

represents the average percentage of seats occupied by revenue-producing

passengers. Decreasing load factors indicate that capacity is being utilized less than

before. In that case the airline is carrying fewer passengers relative to available

capacity. 52 The load factor is an important parameter to measure the efficiency of

airlines. A significant low load factor would indicate that an airline (or the entire airline

industry) is utilizing resources in an inefficient way, producing higher costs to society

due to the expenses of the unused, excess capacity.

50 U.S. Department of Transportation: Air Carrier Traffic Statistics, July 1994, p. 203. 51 Ibid. p. 301. 52 Banfe, C.F., Management, 1992, pp. 164-165.

III. Changes in the U.S. Airline Industry 30

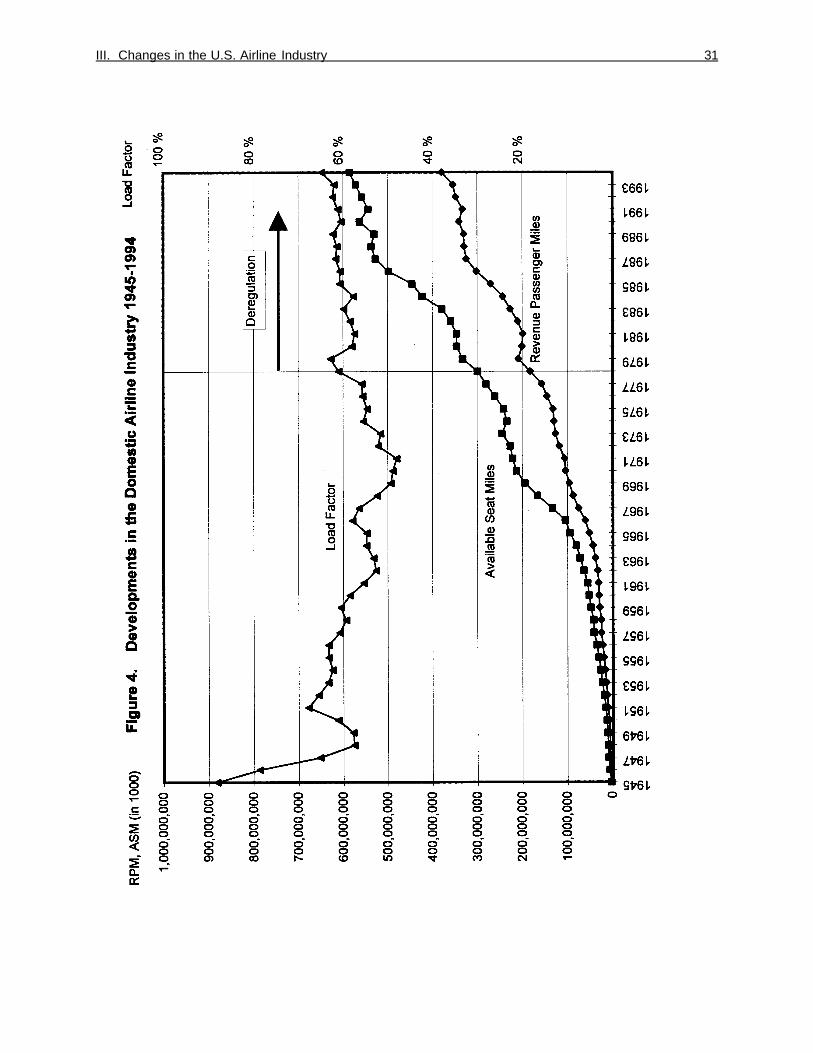

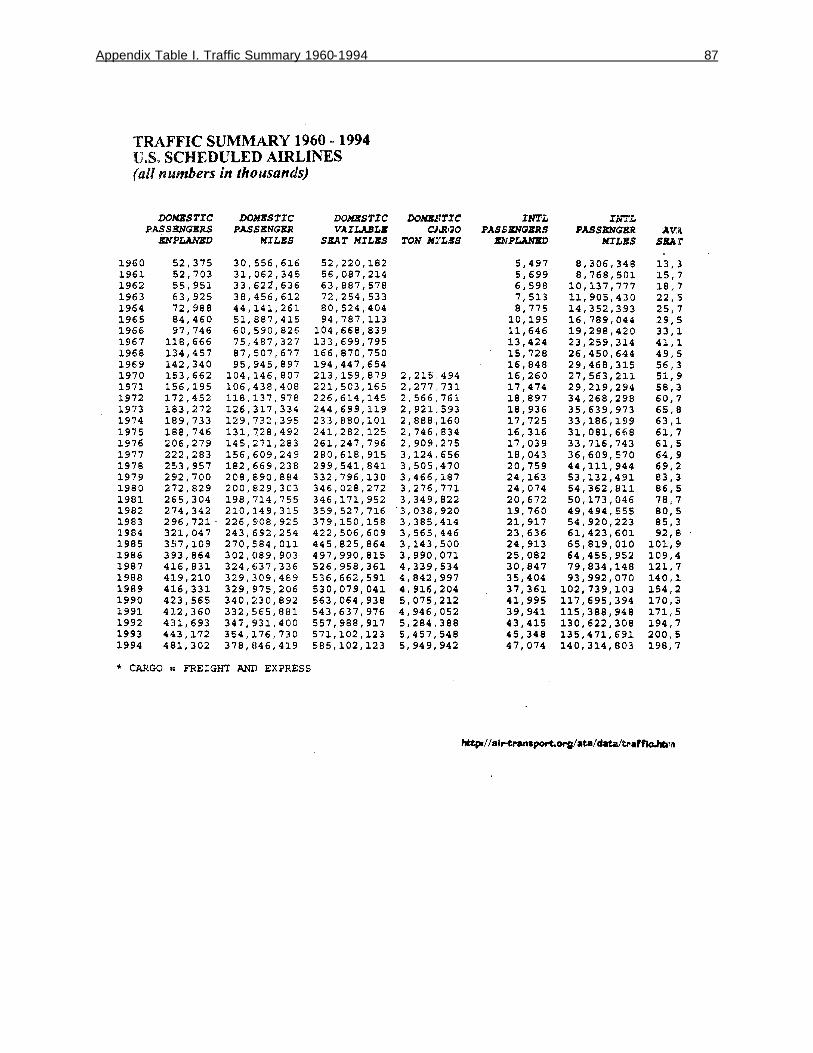

3. Industry Developments 1945 -1994

Figure 4 contains the summation of the revenue passenger miles and the available seat

miles from all scheduled passenger airlines in the domestic market of the United States.

The load factor, which appears in the graphic, is the average load factor for the entire

airline industry. The time period from 1945 until 1994 was chosen to demonstrate the

trends that originated prior to deregulation in 1978.

As shown in Figure 4, the airline industry grow constantly from 1945 to 1994.

Despite the many restrictions of the CAB route and pricing policies, the airline industry

grew rapidly, as the increasing values of revenue passenger miles and available seat

miles indicate.

This growth is due primarily to technological improvements that increased travel

convenience and made reduced fares possible. During the first wave of growth in the

late 1940s and 1950s which was inspired by the introduction of long-haul propeller

aircraft, the CAB encouraged carriers to expand their scheduled service to every city of

appreciable size in the United States. In addition, the CAB authorized competitive

services in most of the denser routes and permitted carriers to offer selective discounts

to expand their customer base to include price sensitive vacation and family travelers.

In the late 1950s and early 1960s, the available passenger miles increased

significantly. Responsible for this dramatic increase was the introduction of jet aircraft

that offered more seat capacity, increased the convenience of air travel, and at the

same time reduced costs. The revenue passenger miles increased as well, but less

spectacularly.53

53 Bailey, E.E./Graham, D.R./Kaplan, D.P., Deregulation, 1985.

III. Changes in the U.S. Airline Industry 31

III. Changes in the U.S. Airline Industry 32

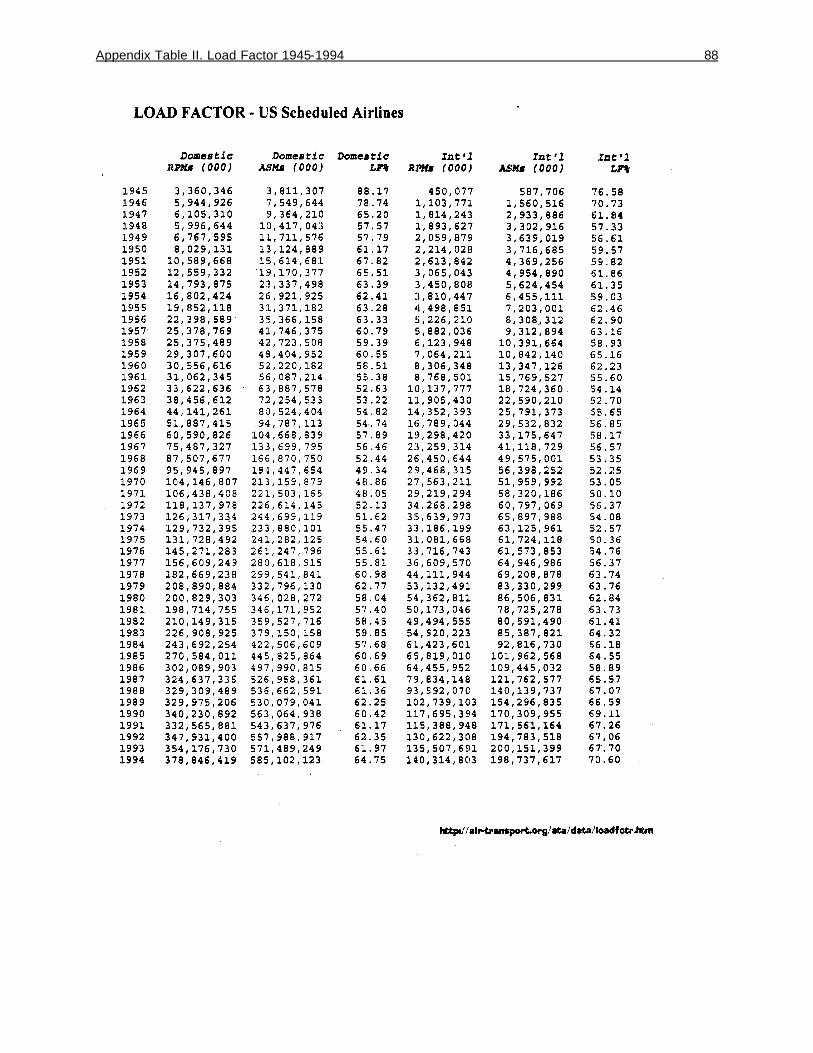

While revenue passenger miles and available seat miles increased, load factor

decreased constantly until 1971. This decrease was caused by the nonprice competition

of the airlines in this period. The operating economies of the long-haul propeller aircraft

and jets over the older planes they replaced led to a growing disparity between fares

(fixed by the CAB) and costs. This gave carriers in competitive markets strong

incentives to engage in inefficient nonprice competition, such as offering additional

flights or roomier seating, thus increasing the proportion of unfilled seats per flight (i.e.

reducing the load factor). Through much of the regulation period, declining load factors

offset some of the cost advantages of the new aircraft.54

One of the most important arguments of deregulation proponents who claimed

that under regulation the U.S. domestic airline industry was producing excess capacity

was the fact that available seat miles were almost doubt the revenue passenger miles in

the 1970s. Since deregulation in 1978, the available seat miles continue to exceed the

passenger revenue miles, but the trend is going towards less excess capacity and

increasing load factors as airlines try to cut costs.

It can be concluded that since its inception, the U.S. domestic airline industry has

been a growth industry. The assumption that the Airline Deregulation Act of 1978 is

responsible for the growth in this industry is false, as the historical data shows the same

growth-rate prior to deregulation. The time period from 1971 to 1978, in particular,

demonstrates the same characteristics as the post deregulation period: growing traffic

and increasing capacity, as well as increasing load factors.

Of course, there were effects that are not reflected by the fact that the airline

industry has continuously grown, for example, the effects on pricing. Prices fell radically

after deregulation, producing a positive effect on consumer demand and public welfare.

It should be mentioned that price reductions in the airline industry today are chosen by

the companies. Investigations in recent years gave evidence to the assumption of a

dependence of prices in correlation with an increase of concentration and monopoly

power, e.g. due to hub dominance of airlines at large airports.55

54 Bailey, E.E./Graham, D.R./Kaplan, D.P., Deregulation, 1985, pp. 16-21. 55 Peteraf, M. A./Reed. R., Pricing, 1994, p.196 and Abunassar, W./Koford, K.. Airline Fares, 1994, p. 374.

III. Changes in the U.S. Airline Industry 33

Another considerable aspect that is not reflected by this statistic is the

development of service-quality. Gaynor and Trapani concluded in their study that

deregulation resulted in a welfare loss due to decreased quality of service. One result of

their study is that from 1971 to 1979, unadjusted consumer surplus 56 increased on the

average of $4.3 million per city-pair market due to deregulation of fares and entry,

whereas quality adjusted consumer surplus increased only $2.07 million.57

4. Major Acquisitions and Mergers

Prior to deregulation, the Federal Aviation Act of 1958 gave the CAB a broad discretion

to approve or disapprove mergers based on a “public interest" test.58 In the first decade

of regulation, from 1938 to 1950, the Board denied all proposed mergers between trunk

carriers. In the mid-1950s it swung to the other extreme and approved mergers on

public interest grounds even when they had anticompetitive effects. From 1956 to 1978

the CAB reverted to its earlier, restrictive posture and approved only four mergers.59

Most often mergers took place to avoid a bankruptcy, which could result in the

discontinuation or reduction of service.60

With the Airline Deregulation Act of 1978, Congress amended Section 408,

concerning mergers, to state that the Board's merger decisions should be governed by

the forces of the market place, not by federal economic regulations.61 Section 408 (b) of

the Airline Deregulation Act of 1978 required the CAB, and later on, the Department of

Transportation, to approve any merger, unless…

“the Board finds that the transaction will not be consistent with the public interest or that the conditions of this section will not be fulfilled.”62

56 Consumer surplus is the extra satisfaction or utility gained by consumers from paying actual prices for goods lower than the consumers would have been prepared to pay. In theory, consumers’ surplus is maximized only in perfect competition. 57 Gaynor, M./Trapani, J.M., Welfare, 1994. 58 Public Law 85-726, Federal Aviation Act of 1958, Section 408 (b). 59 These mergers were: United and Capital Airlines, Northwest and Northeast Airlines, Allegheny and Mohawk Airlines, Delta and Northeast Airlines. See also: Bailey, E.E./Graham, D.R./Kaplan, D.P., Deregulating, 1985, p. 174. 60 Banfe, C.F., Management, 1992, p. 72. 61 Until 1985, the CAB still had the power to approve mergers. After 1985, this function was transferred to the Department of Transportation. 62 Public Law 95-504, Airline Deregulation Act of 1978, Section 408 (b).

III. Changes in the U.S. Airline Industry 34

Section 408 (b) continues by stating the conditions under which the Board should not

approve a merger:

"...the Board shall not approve such transaction - (A) if it [the merger] would result in a monopoly or would be in furtherance of any combination or conspiracy to monopolize or to attempt to monopolize the business of air transportation in any region of the United States; or (B) the effect of which in any region of the United States may be to substantially lessen competition, or to tend to create a monopoly.…” The following part of the same section determines that the Board, and in