Embed Size (px)

Citation preview

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING Symposium 2006 : Marktchancen Home- Printing

26. Januar 2006

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Agenda

1 Unternehmensportrait

2 HomeprintingWer nutzt die Chance?

3 Zusammenfassung

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

1 Unternehmensportrait

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Wichtige Stationen der GfK-Geschichte

Mai 2005 Übernahme von NOP World

September 1999

1990

1967

1949

1934

Im Amtlichen Handel der Börse notiert

Umwandlung in eine Aktiengesellschaft

Start der Internationalisierung

Wiederaufbau der GfK

Gründung des GfK-Nürnberg e.V.

1925 Gründung: Institut für Wirtschafts-beobachtung der deutschen Fertigware

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

GfK Gruppe: Charakteristika (I)

Services

Mitarbeiter

Umsatz672 Millionen Euro im Jahr 2004 ohne NOP World

Steigerung zum Vorjahr: 12,8 %

990+ Millionen Euro im Jahr 2004 inklusive NOP World (pro forma)

über 7.600 Vollzeitbeschäftigte inklusive NOP World

etwa 80% davon außerhalb Deutschlands

Umfassende Informationen zu Konsumgüter-, Healthcare- und Dienstleistungsmärkten

Marktforschungs-Know-how

Marketingberatung

Netzwerk Rund 130 Tochtergesellschaften, Niederlassungen und Beteiligungen in 63 Ländern auf fünf Kontinenten

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

GfK Gruppe: Charakteristika (II)

USP

Marktposition

KerngeschäftAls reines Marktforschungsunternehmen liefert die GfK Informationsservices an führende Dienstleister, Konsumgüter- und Pharmahersteller weltweit

Größtes Marktforschungsunternehmen in Deutschland, in Europa auf Platz 4 und weltweit auf Platz 4

Synergien in fünf Geschäftsfeldern:

31 der 50 Top-Kunden konsultieren die GfK in mindestens drei Geschäftsfeldern

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

GfK Retail and Technology - WW Coverage

Western EuropeEastern Europe

Japan/Asia-PacificAfrica/Middle East

North/South America

AlgeriaAustraliaAustriaAzerbaijanBahrainBelgiumBosnia-HerzegovinaBrazilBulgariaCambodiaCanadaChile

SyriaTaiwanThailandTurkeyUkraineUnited Arab EmiratesUnited KingdomUSAVietnamYemen

ChinaCroatiaCzech RepublicDenmarkEgyptEstoniaFinlandFranceGermanyGreeceHong KongHungary

IndiaIndonesiaIranIrelandIsraelItalyJapanJordanKazakhstanKoreaKuwaitLebanon

LithuaniaMalaysiaMexicoMoroccoNetherlandsNew ZealandNorwayOmanPhilippinesPolandPortugalQatar

RomaniaRussiaSaudi-ArabiaSerbia and MontenegroSingaporeSlovakiaSloveniaSouth AfricaSpainSwedenSwitzerland

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Consumerbuying behaviour

Sales out information on all consumer technology markets

Media consumption and audiencemeasurement

Tailor-madeservices addressingspecificmarketing issues

Key Info

Continuous data collection

Continuous data collection

Continuous data collection, tests

Interviews,tests

Type of measures

ConsumerTracking

Retail and Technology MediaCustom

Research HealthCare

EuropeGlobal GlobalGlobalCoverage Global

Customresearchinformation on the pharma, healthcareand veterinarymarkets

Interviews, continuous data collection

11 %21 % 13 %41 %Sales1) 13 %

GfK Group, offering you all possible research technologies

1) incl. NOP World

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

GfK R&T audit methodologyProduct Flow

Manufacturers

Wholesalers

Resellers / Retailers

Corporate buyers / Consumers

ImportExport

GfK Channel Audit

• defined distribution channels

• defined product groups

• representative samples

• regular data collection

- by single articles

- selling-out, selling-in, stocks, price, etc.

• extrapolation by distributionchannel (GfK Panel Market)

• reporting & presentationsfor customers

direct

Not tracked

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

2 HomeprintingWer nutzt die Chance?

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING WORLD MARKETSSales Volume 2005

Printing Devices*DSC

96 MIO ? 96 MIO ?

*Include business

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

30000

9000

17000

40000

23000

10000

13000

31000

Europe America Japan ROW

17000

90006000

18000

World Market - Digital CamerasSales Volumes 2002 - 2005

2004

36 %34 %

18 %12 %

50 Mill.(+ 64%)

2003 2005 **

40 %30 %

13 %17 %

77 Mill.(+ 54%)

Europe the largest Market for DSC in the World!

96 Mill.(+ 25%)

18 %

42 %31 %

9%

**estimates Nov .2005

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING WORLD MARKETSSales Volume DSC 2005

DSC

D-SLR4% =3,8 Mio?

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING WORLD MARKETSSales Volumes Printing Devices 2005

Small Photo Printer4% (7% in West Eu/ 1% in Asia/China)

Printing Devices

MFD37%

Printer59%

96 MIO

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING WORLD MARKETSSales Volumes 2005

Printing DevicesDSC

Europe40 MIO ?

Europe34 MIO ?

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

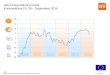

IMAGING MARKETS EU-7-DSC/Printer/Small Photo Printer in Home

3,8

7,3

15,3

23,4

28,7

2,52,31,61,10,8 2,40,90,20,080,02

2001 2002 2003 2004 2005

Digital Cameras Inkjet Photo Printer Small Photo Printer

2,7%

DSC Inkjet Small Photo Printer

2001

37,5%

4,3%

0,9%

DSC Inkjet Small Photo Printer

2005Penetration

Volume Sales 100%

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING MARKETSMarket Volumes / HomesSpring 2005

11,5%15,0%

8,0%3,00%

32,4%

50,3%34,2%

21,8%48,5%

35,7%

39,9%5,7%

37,5%W.EUROPE(7)

E.EUROPE(4)

GERMANY

FRANCE

GREAT BRITAIN

ITALY

SPAIN

NETHERLANDS

BELGIUM

RUSSIA

POLAND

CZECHIA

HUNGARY

0,08%0,03%

0,05%

0,54%

0,70%0,29%0,37%

2,53%0,77%

0,4%0,05%

0,86%

DSC SMALL PHOTO PRINTER

including Data 2001-2004

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING MARKETSMarket Volumes / HomesSpring 2005

11,5%15,0%

8,0%3,00%

32,4%

50,3%34,2%

21,8%48,5%

35,7%

39,9%5,7%

37,5%W.EUROPE(7)

E.EUROPE(4)

GERMANY

FRANCE

GREAT BRITAIN

ITALY

SPAIN

NETHERLANDS

BELGIUM

RUSSIA

POLAND

CZECHIA

HUNGARY

1,0%0,6%

0,7%

4,0%

4,8%2,5%

4,3%8,1%

4,5%2,3%0,7%

4,3%

DSC INKJET PHOTO PRINTER

including Data 2001-2004

6,2%

2,5%0,3%

16,6%

19,1%12,9%

8,2%

16,1%16,9%

12,8%1,0%

13,8%

MFD

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

41

MFD

Small PhotoPrinter

Inkjet PhotoPrinter

Printer Total

Growth Rate 2005 VS. 2000

++++++++

++++++

++++++

++++++++

++++++++

Growth Rate 2005 VS. 2001

++++++++

++++++++

EU 71) EE 42)

IMAGING MARKETSMARKETTRENDS VOLUME GfK PanelmarketGrowth Rate(%)

Growth 2005 Growth 2005Average Growth Average Growth

+1198%

+217%

+29%

+74%

+405%

+212%

+218%

+294%

(+ 30%)

(+187%)

(+ 4%)

(+33%)

(+154%)

(+207)

(+ 29%)

(+108%)

1)EU7=BE,NL,DE,FR,GB,IT,ES 2)EE4=RU,PL,CZ,HUGrowth Rates: +++=101-999% ++++=1000-9999% +++++=10000-99999% ++++++=100000-999999% +++++++=<1Mio

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

13

MFD

Small PhotoPrinter

Inkjet PhotoPrinter

Printer Total

Growth Rate 2005 VS. 2000

++++++++

++++++

++++++

++++++++

++++++++

Growth Rate 2005 VS. 2001

++++++

++++++

EU 71) EE 42)

IMAGING MARKETSMARKETTRENDS VALUE GfK PanelmarketGrowth Rate(%)

Growth 2005 Growth 2005Average Growth Average Growth

+ 78%

+155%

+13%

+49%

+2645%

+116%

+165%

+205%

(+ 7%)

(+122%)

(- 4%)

(+10%)

(+105%)

(+68%)

(+ 20%)

(+75%)

1)EU7=BE,NL,DE,FR,GB,IT,ES 2)EE4=RU,PL,CZ,HUGrowth Rates: +++=101-999% ++++=1000-9999% +++++=10000-99999% ++++++=100000-999999% +++++++=<1Mio

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

90

7366

5072

4038

IMAGING MARKETSPRICE INDICATORS GfK PanelmarketIndex 2000(EU7) 2001(EE4)= 100%

Flashes

Lenses

CRT/Flat Total

Cartridges

Inkjetpaper

Mobilephones Total

Still Films

PC

Smartphones

Still Cameras

Camcorder

Printer Total

Digital Cameras

Memorycards

Beamer

135129

115109

1029189

656361

5746

413936

*Lenses and Flashes DE only

> 200

EU 71) EE 42)

1)EU7=BE,NL,DE,FR,GB,IT,ES 2)EE4=RU,PL,CZ,HUGrowth Rates: +++=101-999% ++++=1000-9999% +++++=10000-99999% ++++++=100000-999999% +++++++=<1Mio

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

IMAGING MARKETSProductgroups

Memorycards Still Films

Digital Cameras Still Cameras

Flashes Lenses

Printers MFD

Small Photo Printers Inkjet Photo Printer

Inkjetpaper Cartridges

Mobilephones Smartphones

Camcorder CRT/Flat TV

Beamer PC

GfK Group Retail and Technology

IMAGING & COMMUNICATIONPRODUCT SHARE2003 - 2005 RR VALUE

.GfK-Panelmarket GERMANY

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\photo\PRS\PRS0141\CH105243.TXT (001)1/2006

2003 2004 F-NOV04 F-NOV05 FM04 AM04 JJ04 AS04 ON04 DJ05 FM05 AM05 JJ05 AS05 ON05

6378 7597 6011 6392 1157 1205 1248 1149 1252 1585 1265 1282 1361 1222 1263SAL.EURO IN MIO.

34

4

56

92

3

9

5

19

3

30

43

57

1

4

19

6

19

1

31

44

57

1

4

19

6

18

1

31

52

46

12

23

6

18

33

4

3

48

2

4

18

6

16

2

31

44

57

1

3

20

5

17

1

29

5456

1

4

19

5

19

2

30

54

56

1

4

19

6

18

2

31

42

47

1

4

19

6

18

1

25

52

57

1

4

21

6

22

1

30

42

4

71

3

24

6

17

30

52

46

13

25

6

17

1

30

63

55

12

22

5

19

32

53

45

12

23

6

17

33

42

4

612

23

6

17

CARTRIDGESINKJETPAPERMEMORYCARDSSTILL FILMSCAMCORDERCOLOR PRINTERSCANNERPDACAMPHONESMFDDSCANALOG CAMERAS

GfK Group Retail and Technology

IMAGING & COMMUNICATIONDISTRIBUTION SHARE IMAGING Index TOTAL2003 - 2005 RR VALUE

.GfK-Panelmarket GERMANY

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\photo\PRS\PRS0141\CH105245.TXT (001)1/2006

2003 2004 F-NOV04 F-NOV05 FM04 AM04 JJ04 AS04 ON04 DJ05 FM05 AM05 JJ05 AS05 ON05

6378 7597 6011 6392 1157 1205 1248 1149 1252 1585 1265 1282 1361 1222 1263SAL.EURO IN MIO.

38

39

13

82

36

35

12

162

35

36

12

152

35

35

10

18

2

33

39

12

152

35

36

11

17

2

37

33

12

162

36

35

12

152

36

36

12

152

40

30

12

161

34

35

11

19

2

35

35

10

19

1

37

35

11

172

35

36

10

18

2

36

37

10

172

CESCSS/OERMASS M.TCROthers

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Imaging MarketsAssortment /Developement (example Germany)January 2001 vs. September 2005

2001 2005 2001 2005 2001 2005 2001 2005Still Films 64 54 1.619 1.039 119 46 0 0Memory Cards 61 145 340 340 20 114 1 2Still Cameras 82 62 1.142 538 97 22 5 1Digital Cameras 41 121 206 961 20 123 5 11 - SLR 5 8 5 26 2 7 - - - Compact Cameras 41 120 201 935 22 118 - - - Compact>=5-6 MP CCD - 42 - 225 - 42 - -

Lenses 28 20 518 267 31 19 3 2

El. Flashes 39 26 139 97 11 8 1 1

Camcorder 21 17 329 277 21 34 6 5

Mobilephones 27 35 333 874 34 110 1 4 -Cameraphones - 20 - 462 - 68 - -Smartphones 3 18 5 79 1 5 0 1CRT-TV 86 83 1.773 1.267 153 96 23 8Flat /TV 30 104 116 878 11 104 40 41Beamer - 45 - 388 20 8 0 4Computers 123 119 1.639 2.953 27 46 13 14MFD 25 22 94 297 6 33 1 2Small Photo Printer 12 14 12 43 2 9 0 0Printer Inkjet 4 4 20 41 4 10 0 1Inkjetpaper 53 103 397 1.192 16 106 0 2Cartridges 53 150 1.051 6.439 63 397 1 4

100% 100%7%

Photostores >5 Mio. Turnover Average AssortmentGfK Total Market

Photostores >5 Mio. Turnover

Number of Brands

Number of Selling Items Stocks Value in%Number of Items

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Digital Still Cameras/Printer Germany

Sales units in %

Februar-November 2005

Total Photo-Spec. TecSSt. CS El.EH. C OER SH Dept./Mo. Hyp./C&C

Feb.-Nov. 05 Feb.-Nov. 05 Feb.-Nov. 05 Feb.-Nov. 05 Feb.-Nov. 05NFeb.-Nov. 05 Feb.-Nov. 05 Feb.-Nov. 05 Feb.-Nov. 05in % in % in % in % in % n in % in % in % in %

DSC 100 24 41 3 5 1 2 15 9

Small Photo Printer 100 16 46 3 5 1 3 24 2

Photo Printer ded. 100 3 54 9 6 2 15 8 4

Photo Printer ded. incl. Pictbridge 100 2 46 9 9 6 14 7 6

No Photo Printer wo. Pictbridge 100 0 29 9 4 9 41 2 4

MFD Photo Printer 100 0 59 5 9 5 7 10 3

Inkjetpapier+150 Gr. ( Sheets ) 100 3 34 4 3 20 2 6 16

Thermalpapier ( Sheets ) 100 46 28 3 5 2 1 11 3

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

DSC/Small Photopapier/Inkjet +150 Gr./Thermalpapier Germany

Distr. November 2004/2005 (ungew Distr.%)Anzahl der Geschäfte die das Produkt führen in %

OER

04 05 04 05 04 05 04 04 05

unw. unw. unw. unw. unw. unw.wg unw. unw.

DSC 38 35 89 90 99 99 6 10

Small Photo Printer 10 12 27 44 89 94 3 2

Photo Printer ded. 15 10 14 20 96 92 8 8

Photo Printer ded. incl. Pictbridge 23 22 15 26 98 99 24 26

No Photo Printer wo. Pictbridge 36 33 12 14 99 99 51 49

MFD Photo Printer 17 16 7 3 99 98 28 18

Inkjetpapier+150 Gr. 31 37 36 70 97 99 58 61

Thermalpapier 3 7 9 46 26 81 1 2

Total Nov. 04/05 Photo-Spec. TecSSt.

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

2,1 2,352,472,653,3 3,6

4,1 4,2 4,3 4,5 4,7 4,8 5,055,155,25 5,04,3

3,9

0,750,5

ANALOG DIGITAL ML Digital/Kiosk Homeprinting

GERMAN AMATEUR PHOTOGRAPHIC MARKETCOLORPRINTS (100% COVERAGE) in Wholesalelabs incl. Homeprinting1987-2004

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

THOU.MILL. UNITS

0,75

5,2 Mrd Bilder in 2004+ 750 Mio Homeprints ???

1,0 Mrd digitale Prints im Großlabor in 2005?

2003: 4,8 /:4,3 Analog -7% und 0,5 digital

2004: 4,65( -3%) : 3,9 analog und 0,75 digital +750 Mio Homeprinting + ML/Kiosk 550 Mio incl analog total 5,2 – 2%

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Could you please estimate the percentage of paper-prints made from digital photos, which are …Group has made or has had made paper prints from digital photos (Q. 26)

50%

67%

55%49% 48%

40%49%

5%7%

6%

5%

9%

26%

18%

16% 25% 31%

38%

27%

18%11%

25%20%

16% 17% 15%

4%

6%

Oct 03 -March 04

(n=171) (n=110)(n=92)(n=39) (n=96) (n=79)

July 03 -Sept 03

Jan 03 -June 03

200220012000 and earlier

Ordered via Internet

Taken to a shop, which has prints made by a photofinisher, a specialist company

Made in a shop on their mini-lab or usage a kiosk

Made at home on a home-printer

Total

Date of buying of the first digital camera

ABER ICH MUSS EINEN BESITZEN!!!!

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

44) Reasons why the people were not satisfied with their digital photos (maximum of four answers)Group has made or has had made paper prints from digital photos (Q. 26) + is not satisfied with the digital photos (Q. 43)

47%

25%

12% 11%

46%

2% 2%

37%

19%

10%

19%

5% 5%

67%

33%

25%

17%

4% 4% 4%

50%

35%

9%

13%

17%

26%

44%

Digital prints from home-printer

Digital prints from a shop with mini-lab or kiosk

Digital prints from a shop where photos made by finisher

Digital prints ordered via the internet

Poor picture quality

Poor permanence

Incorrectformat

Ink ran out

Tooexpensive

Delivery too slow

Too difficult

No or not enough

guidance from shop staff

No statement

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

(n=585)

Prints fromDigital cameras

Quick to make / quick to order

Simple to make / simple to order

Short waiting time / quick delivery

Price / costs

Permanence

Printed image identical with that in viewfinder

Accurate colours

Detail

Picture Quality generally

39%

63%

24%

12%

62%

50%

88%

51%50%

Prints fromAnalogue cameras

(n=457)

22%

34%

68%

30%

13%

66%

33%

92%

34%

29) What is particularly important on prints from either digital oranalogue cameras (maximum of six reasons)Group has made or has had made paper prints from digital photos (Q. 26)

Digitalkameras: -Quick

-Simple

- Short

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Comparison of the existence of someone in the household who knows how to print digital prints on a home printer, order them in a shop, order them in a shop with production by a photofinisher, and order them on the internet;Group has made or has had made paper prints from digital photos (Q. 26)

9%

41%

90%

53% 56%51%

48%44%

Someone in household has knowledge

No one in household has knowledge

No statement

Total: how to print photos on a home-

printer

Total: how to order photos in a shop

Total: how to order photos in shop +

production by photofinisher

Total: how to order photos on the

internet

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Wholesale lab printingVolume2003 - 2005

5 13 22 25

95 87 78 75

2003 2004Jan.-Oct

2005 S/O 2005

AnalogDigital

100% 100% 100% 100%

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Market Volumes Thermalpaper / Thermalprinter2004/ 2005

24

46

57

5438

62

11

41

42W.EUROPE(8)

GERMANY

SPAIN

FRANCE

GREAT BRITAIN

NETHERLANDS

BELGIUM

ITALY

PORTUGAL

Average print Thermalpaper in 2005 related to owned Thermalprinter

Base:Thermalprinter sales include Data 2003-2005

(6)

GfK Group Retail and Technology

PHOTOPAPER GERMANYSALES SHEET2004 - 2005 CUM.

GfK-Panelmarket+150 GSM

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\Photo\PRS\PRS0168\CH121595.TXT (001)1/2006

PM2004 JAN-NOV04 JAN-NOV05

CES2004 JAN-NOV04 JAN-NOV05

OER2004 JAN-NOV04 JAN-NOV05

MM2004 JAN-NOV04 JAN-NOV05

108,9100

96,6100

143,610049

44,941

39,241

62,14358

29,327

26,227

37,42643

24,623

2223

29,72135

Sal.Sheets in Mio.In % of P M

Growth Rate +/-LY

99 99 96

4

98

2

98

2

98 99 9992

8

100 100 97

3

INKJETTHERMALOthers

GfK Group Retail and Technology

PHOTOPAPER GERMANYSALES SHEETS/EUROLAST 7 MONTH GROWTH

GfK-PanelmarketTHERMAL TOTAL

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\Photo\PRS\PRS0168\CH121607.TXT (001)1/2006

SAL.UNIT SHEETSMAY05 JUN05 JUL05 AUG05 SEP05 OCT05 NOV05

VALUE EUROMAY05 JUN05 JUL05 AUG05 SEP05 OCT05 NOV05

0,7

2851

0,8

4490

0,9

3670

0,8

2087

0,8

2907

0,8

2784

0,9

2525

0,1

591

0,1

776

0,1

715

0,1

369

0,1

519

0,1

444

0,1

348UNIT SHEET/EURO IN MIO.

+/-

41

32

4

523

4

9

39

41

33

54

5

43

33

63

23

8

47

24

743

4

3

8

43

18

10

532

19

44

30

83

3

74

44

33

762

3

4

40

39

3

3223

8

41

41

23

4

3

5

39

40

64

22

7

46

28

74

3

32

7

36

21

104

32

24

42

31

84

3

74

41

36

852

3

5

PHOTTECSELSPCSSHOERHM/C&CDS/MO

GfK Group Retail and Technology

PHOTOPAPER GERMANYSALES SHEETS/EUROLAST 7 MONTH GROWTH

GfK-PanelmarketINKJET + 150GSM

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\Photo\PRS\PRS0168\CH121608.TXT (001)1/2006

SAL.UNIT SHEETSMAY05 JUN05 JUL05 AUG05 SEP05 OCT05 NOV05

VALUE EUROMAY05 JUN05 JUL05 AUG05 SEP05 OCT05 NOV05

12,145

11,138

14,245

13,659

12,852

14,861

14,465

3,39

3,16

3,69

3,317

3,28

3,717

3,516

UNIT SHEET/EURO IN MIO.+/-

2

41

3

42

23

15

6

3

39

3

52

26

14

6

2

39

3

43

24

15

7

2

36

3

72

24

16

6

3

35

4

82

24

15

6

2

42

3

62

22

14

7

2

38

4

72

24

13

6

3

37

2

44

31

12

6

3

32

2

43

37

11

5

3

34

3

3

3

34

12

6

3

33

3

4

4

35

12

5

4

32

3

52

36

11

5

4

36

3

4

3

32

11

6

4

33

3

43

35

10

6

PHOTTECSELSPCSSHOERHM/C&CDS/MO

GfK Group Retail and Technology

PHOTOPAPER GERMANYSALES UNIT SHEETSJAN.-NOV.2005

GfK-PanelmarketINKJET/THERMAL TOTAL

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\Photo\PRS\PRS0168\CH121612.TXT (001)1/2006

DIN A4PM

JAN-NOV05

CESJAN-NOV05

OERJAN-NOV05

MMJAN-NOV05

DIN A6PM

JAN-NOV05

CESJAN-NOV05

OERJAN-NOV05

MMJAN-NOV05

157,110015

4410014

58,21009

24,7100-14

63,140135

40,392130

6,611137

11,346131

Sal.Sheets in Mio.In % of P M

Growth Rate +/-LY

11

62

23

22

6

15

12

12

9

25

13

511

20

3

66

25

15

8

22

12

24

4

3

33

3

12

665

2

133

25

77

26

22

11

152

25

5

7

25

43

13

2

152

5

19

25

7

20

3

585

33

63

28

9

1-9 SHEETS10 SHEETS11-14 SHEETS15 SHEETS16-19 SHEETS20 SHEETS21-24 SHEETS25 SHEETS26-49 SHEETS50 SHEETS51-74 SHEETS75 SHEETS76-99 SHEETS100 SHEETS101-199 SHEETS200-249 SHEETS+250 SHEETSOthers

GfK Group Retail and Technology

PHOTOPAPER GERMANYSALES UNIT SHEETSJAN.-NOV.2005

GfK-PanelmarketINKJET/THERMAL TOTAL

© by GfK MS, www.gfkms.com \\nwcaf\msprod\data\cobras\Photo\PRS\PRS0168\CH121603.TXT (001)1/2006

DIN A4PM

JAN-NOV05

PHOTJAN-NOV05

TECSJAN-NOV05

ELSPJAN-NOV05

DIN A6PM

JAN-NOV05

PHOTJAN-NOV05

TECSJAN-NOV05

ELSPJAN-NOV05

157,110015

310043

3510010

610027

63,140135

4,2142239

33,896122

2,338106

Sal.Sheets in Mio.In % of P M

Growth Rate +/-LY

1162

23

22

6

15

12

3

33

6

22

59

19

10

10

28

14

6

11

16

144

132

84

2

50

2

133

25

77

26

22

11

8

1022

5

71

16

27

5

8

28

4

3

6

9

14

23

103

19

17

1-9 SHEETS10 SHEETS11-14 SHEETS15 SHEETS16-19 SHEETS20 SHEETS21-24 SHEETS25 SHEETS26-49 SHEETS50 SHEETS51-74 SHEETS75 SHEETS76-99 SHEETS100 SHEETS101-199 SHEETS200-249 SHEETS+250 SHEETSOthers

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Zusammenfassung

1Die Marktchancen sind für alle Absatzkanäle vielfältig und müssen bzgl des Produktangebotes individuell definiert werden ( persönliche Zieldefinition).

Der Homeprinting Markt muss noch gestaltet und entwickelt werden, er ist noch in der Anfangsphase –und steht im Wettbewerb zu anderen Printmodalitätenaber auch Bildpräsentationsmedien!

2

3Die Bedeutung des Bildes nimmt zu

* words don‘t come easy- pictures do!*

Der Konsument muss einfach und unkompliziert Bilder printen können!

30. Januar 2006GfK Gruppe *Imaging Symposium 2006* Sprecher: Marion KnocheRetail and Technology

Vielen Dank für Ihr Interesse!

Besuchen Sie die GfK auf der photokina 2006in Köln!

-Im Messebüro und bei den

-GfK Market Briefings!

-Kontact: [email protected]