Embed Size (px)

Citation preview

University of the Philippines Solar LaboratoryKabang Kalikasan ng Pilipinas (WWF Philippines)

U.P. Electrical and Electronics Engineering Foundation

PPOOWWEERR SSWWIITTCCHH!! SScceennaarr iiooss aanndd SSttrraatteeggiieess ffoorr CClleeaann PPoowweerr DDeevvee llooppmmeenntt iinn tthhee

PPhhiilliippppiinneess

Prepared by: Prof. Rowaldo R. del Mundo Charito M. Isidro Remife L.Villarino-de Guzman Fidelpio V. Ferraris

With inputs from: Rafael Señga Ina Pozon Liam Salter

2003, Kabang Kalikasan ng Pilipinas (WWF Philippines) / University of the

Philippines Solar Laboratory This report was produced by the University of the Philippines Solar Laboratory for the Kabang Kalikasan ng Pilipinas. No part of this publication may be reproduced in any form or means without the prior written permission of the Kabang Kalikasan ng Pilipinas and the University of the Philippines Solar Laboratory.

University of the Philippines Solar Laboratory (UPSL) German Yia Hall, University of the Philippines Diliman, Quezon City Tel. No. (632) 924-4150 Fax No. (632) 434-3660 Email: [email protected] Web: http://www.upd.edu.ph/~solar

Kabang Kalikasan ng Pilipinas WWF Philippines LBI Building # 57 Kalayaan Avenue, Quezon City Tel. No. (632) 433-3220 to 22

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page i Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

TABLE OF CONTENTS

LIST OF FIGURES...........................................................................................................iii

LIST OF TABLES.............................................................................................................vi

LIST OF APPENDICES.................................................................................................viii

LIST OF ABBREVIATIONS ............................................................................................ix

EXECUTIVE SUMMARY .................................................................................................x

1 EXECUTIVE SUMMARY.................................................................................... 1

1.1 Introduction................................................................................................ 1

1.2 Technology and Resource Assessment

for Clean Power Development ............................................................... 1

1.3 Historical Performance of the Philippine Power Sector ..................... 4

1.4 Scenarios under the Philippine Energy Plan 2003-2012 ................... 7

1.5 Clean Power Development for the Philippines .................................... 8

1.6 Conclusions and Recommendations ...................................................10

2 ENERGY TECHNOLOGIES AND RESOURCES FOR

CLEAN POWER.................................................................................................13

2.1 Clean Energy Technologies .................................................................14

2.2 Resource Assessment...........................................................................20

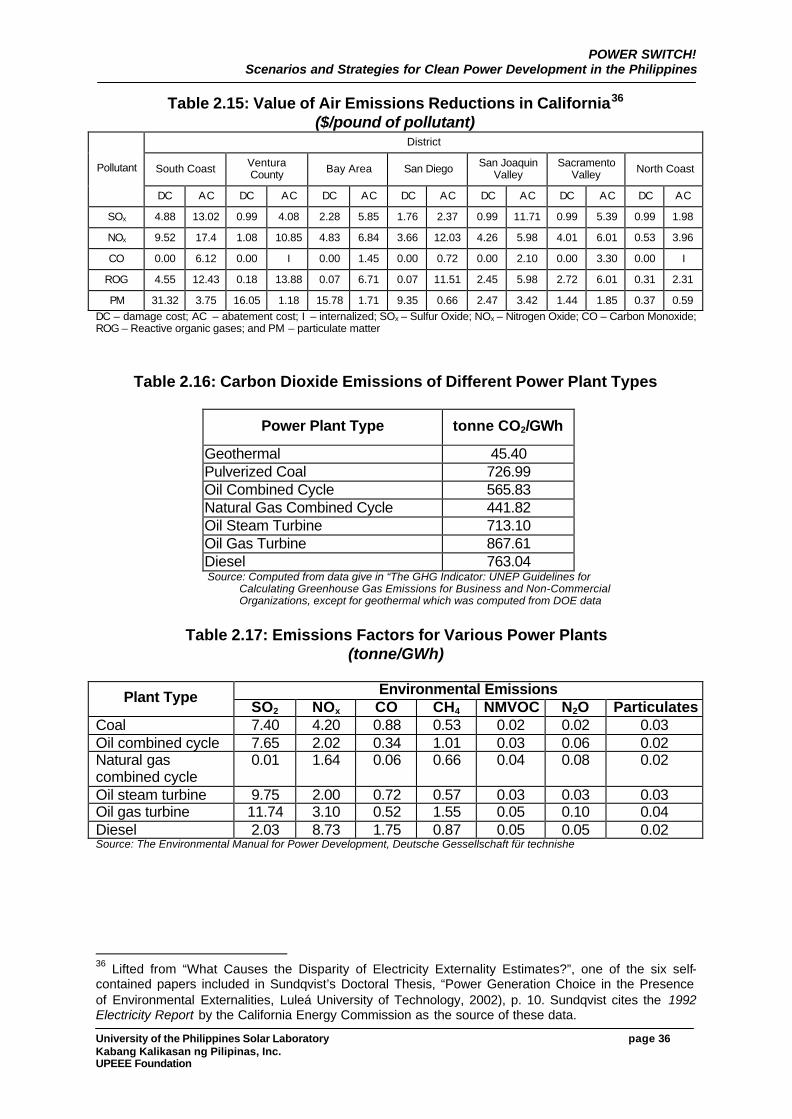

2.3 Cost Comparison of Power Generation Technologies .....................32

2.4 Environmental Externalities ..................................................................35

2.5 Mitigation Options ...................................................................................37

3 HISTORICAL PERFORMANCE OF THE

PHILIPPINE POWER SECTOR ......................................................................38

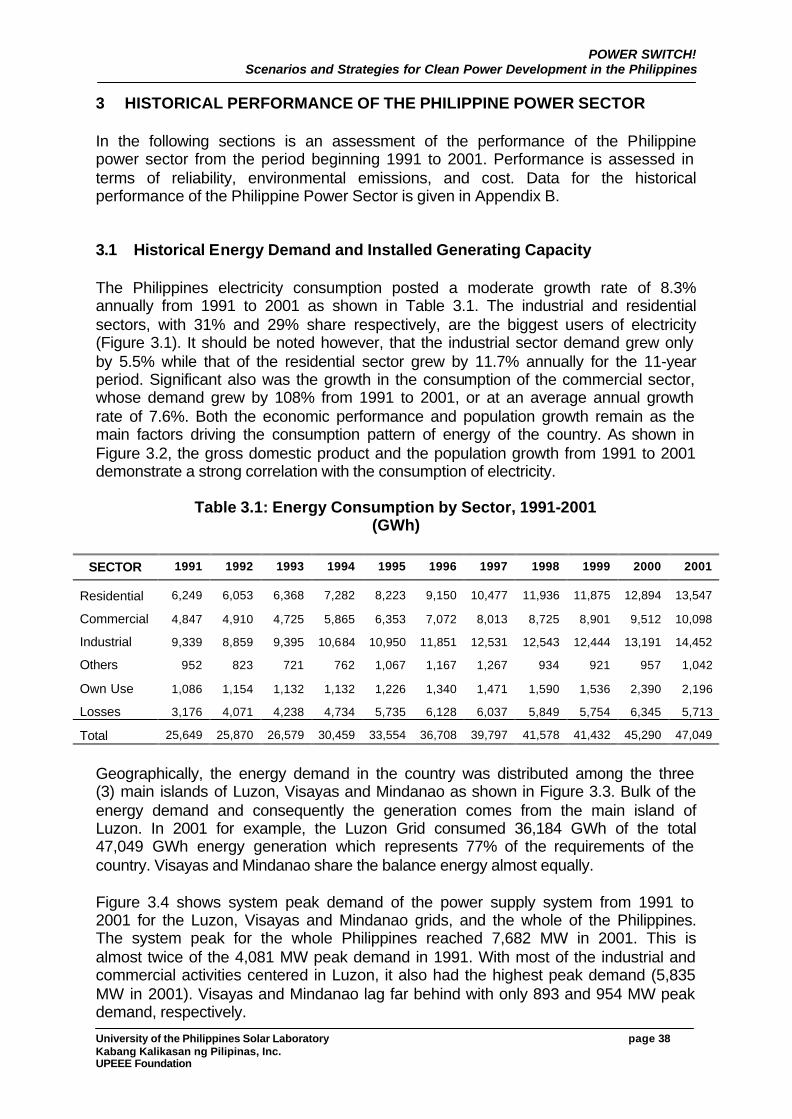

3.1 Historical Energy Demand and

Installed Generating Capacity ..............................................................38

3.2 Historical Reliability Performance........................................................41

3.3 Historical Environmental Performance ...............................................42

3.4 Cost of Electricity....................................................................................46

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page ii Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

4 SCENARIOS UNDER THE PHILIPPINE ENERGY PLAN

FOR 2003-2012.................................................................................................3.1

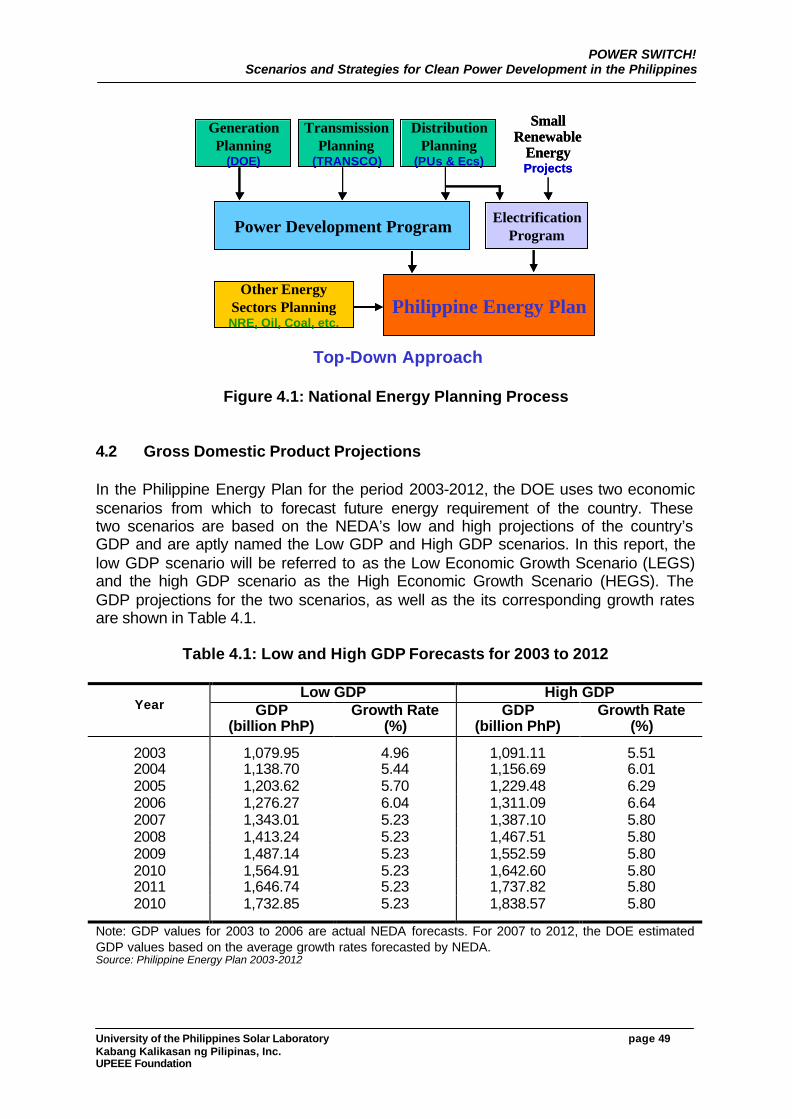

4.1 National Energy Planning Process ......................................................48

4.2 Gross Domestic Product Projections ..................................................49

4.3 DOE Plan for the Low Economic Growth Scenario ..........................50

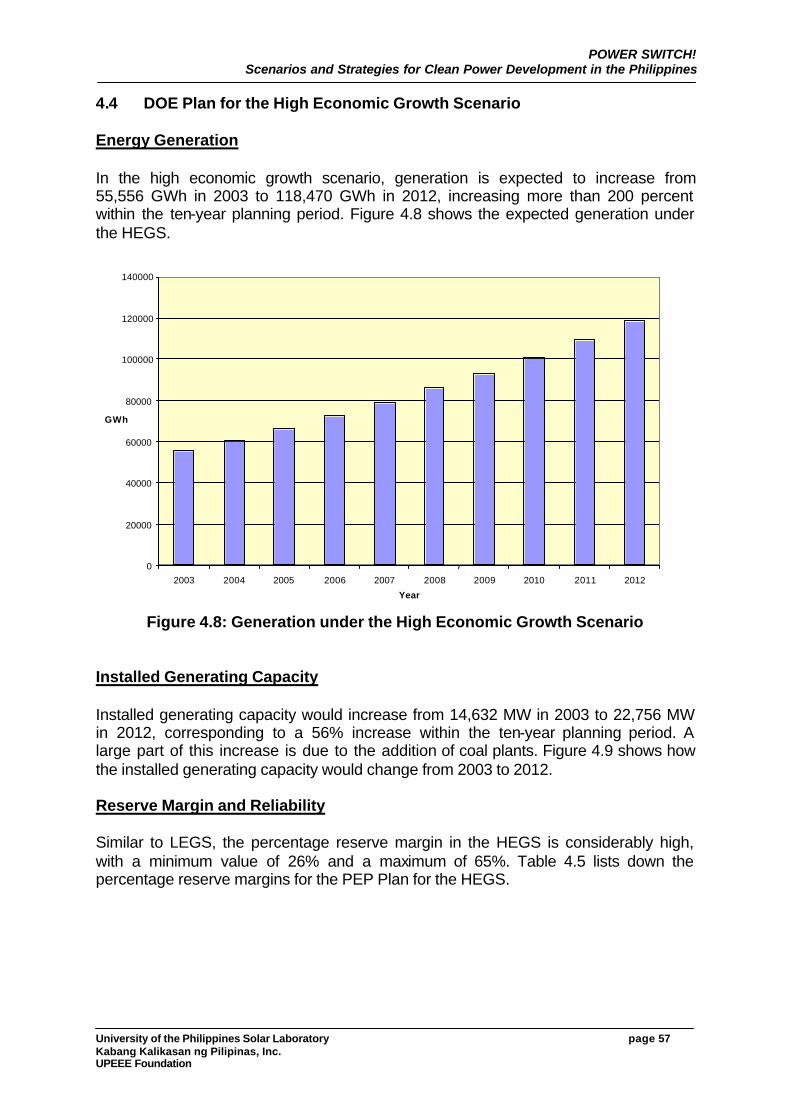

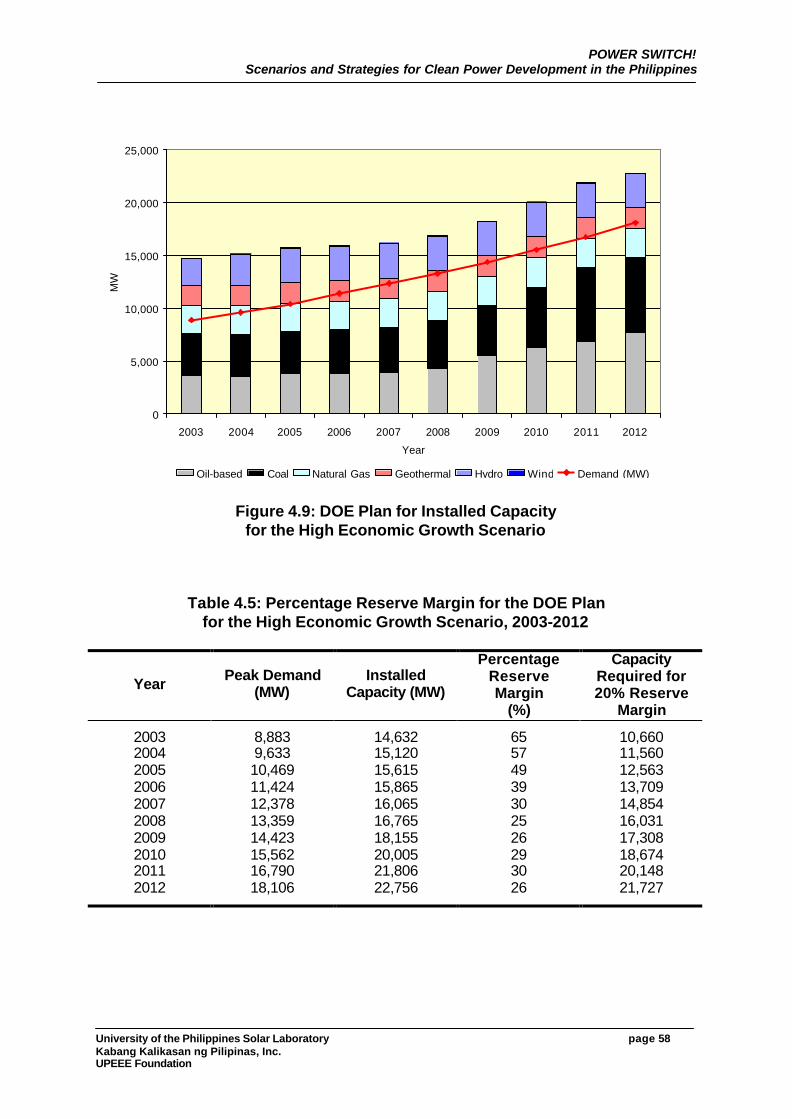

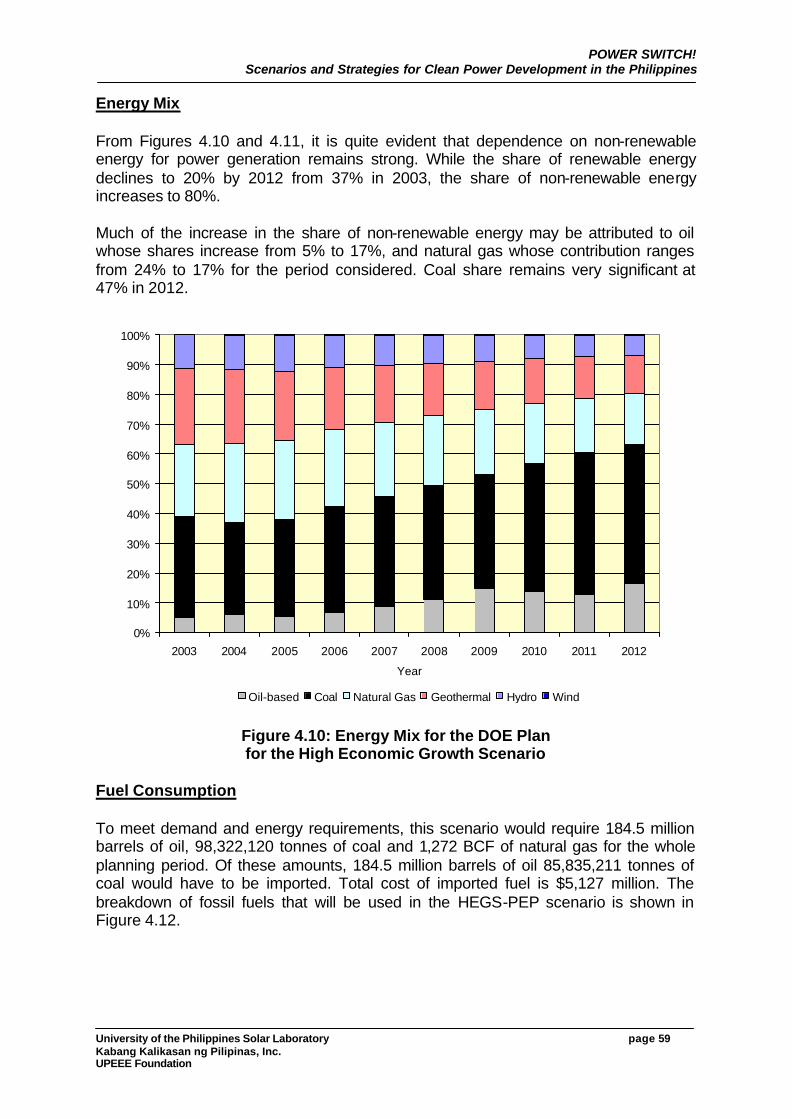

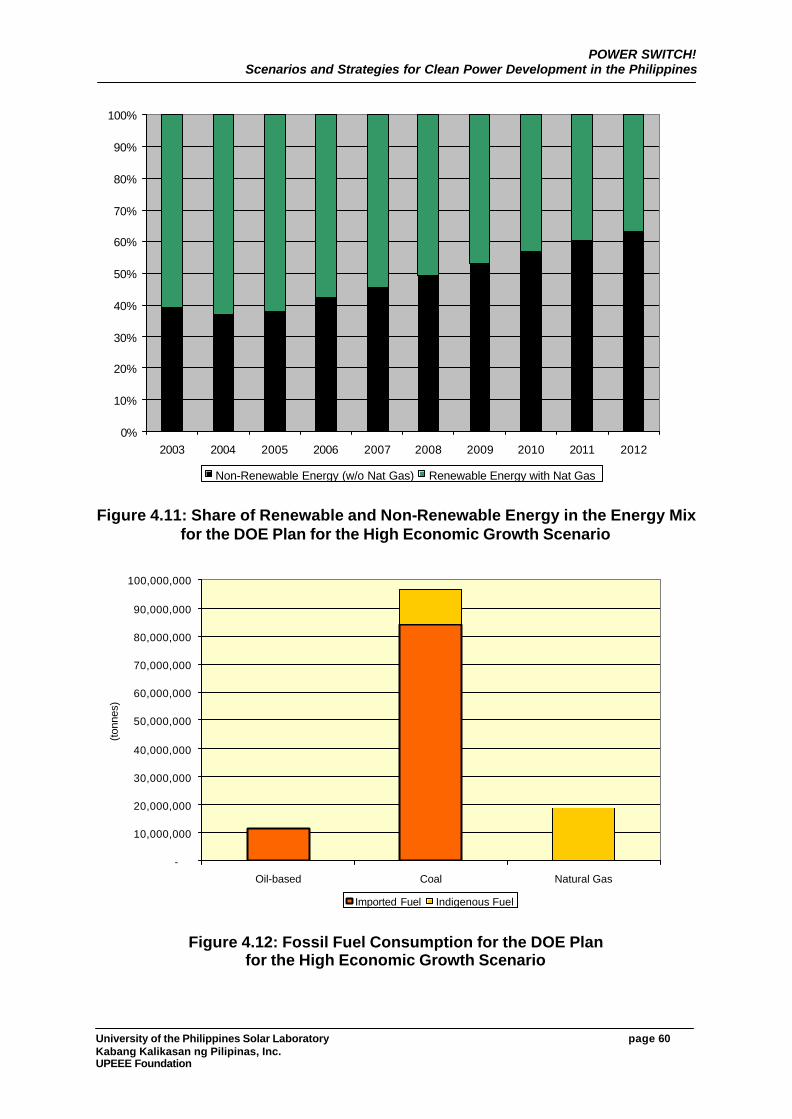

4.4 DOE Plan for the High Economic Growth Scenario .........................57

5 CLEAN POWER DEVELOPMENT OPTIONS..............................................63

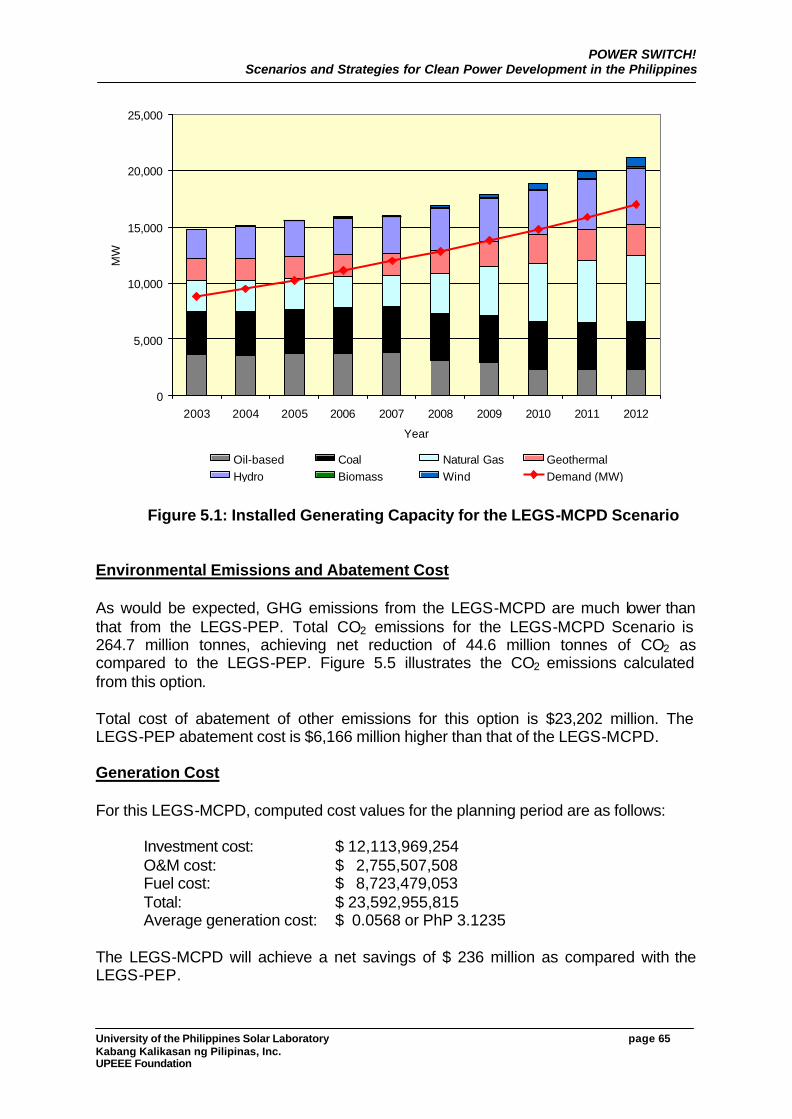

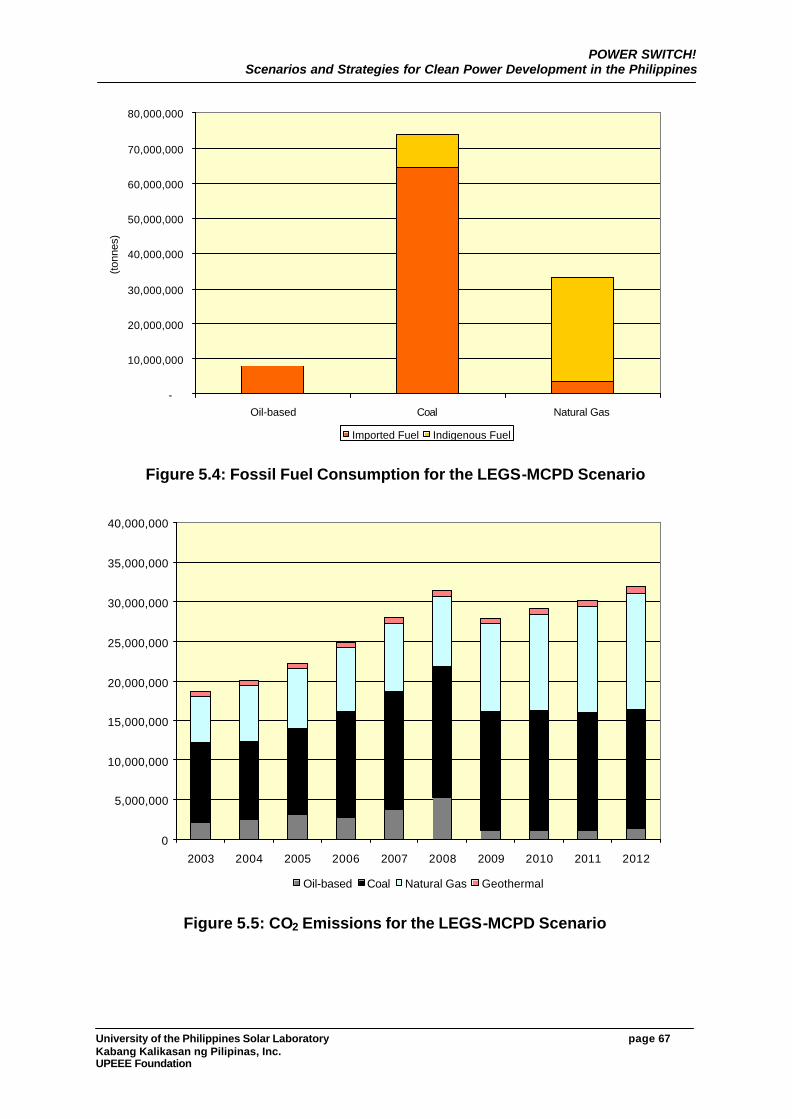

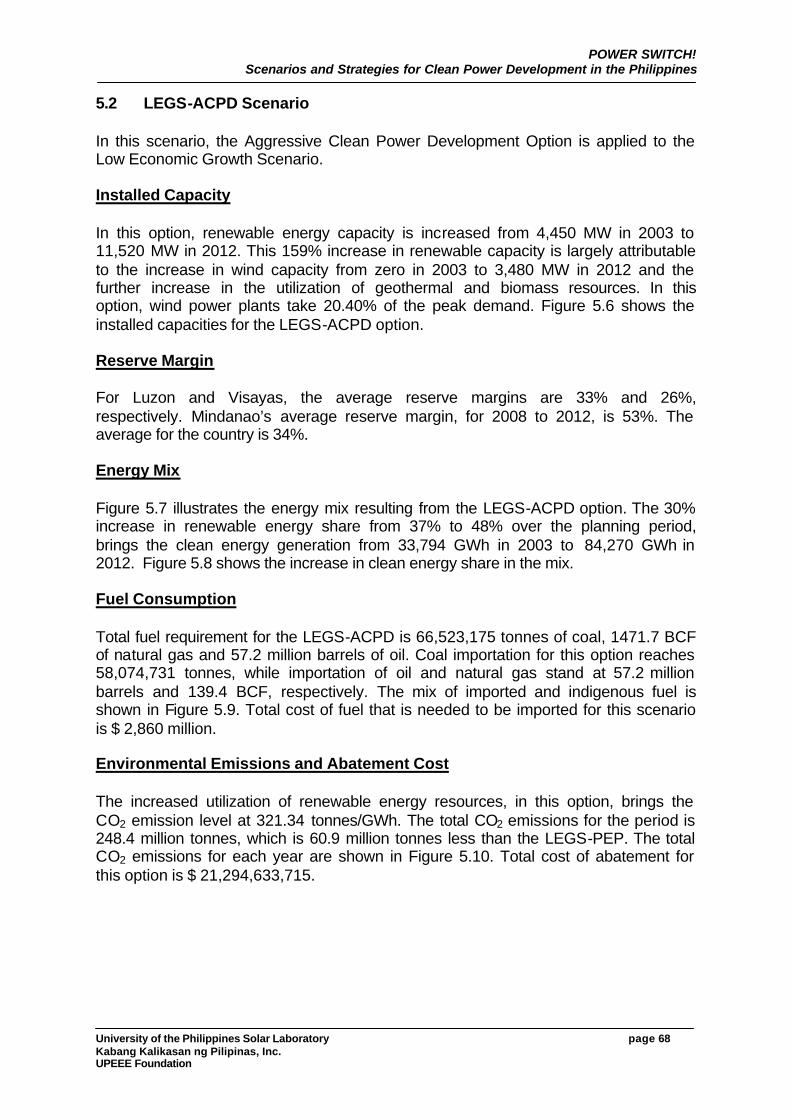

5.1 LEGS-MCPD Scenario..........................................................................64

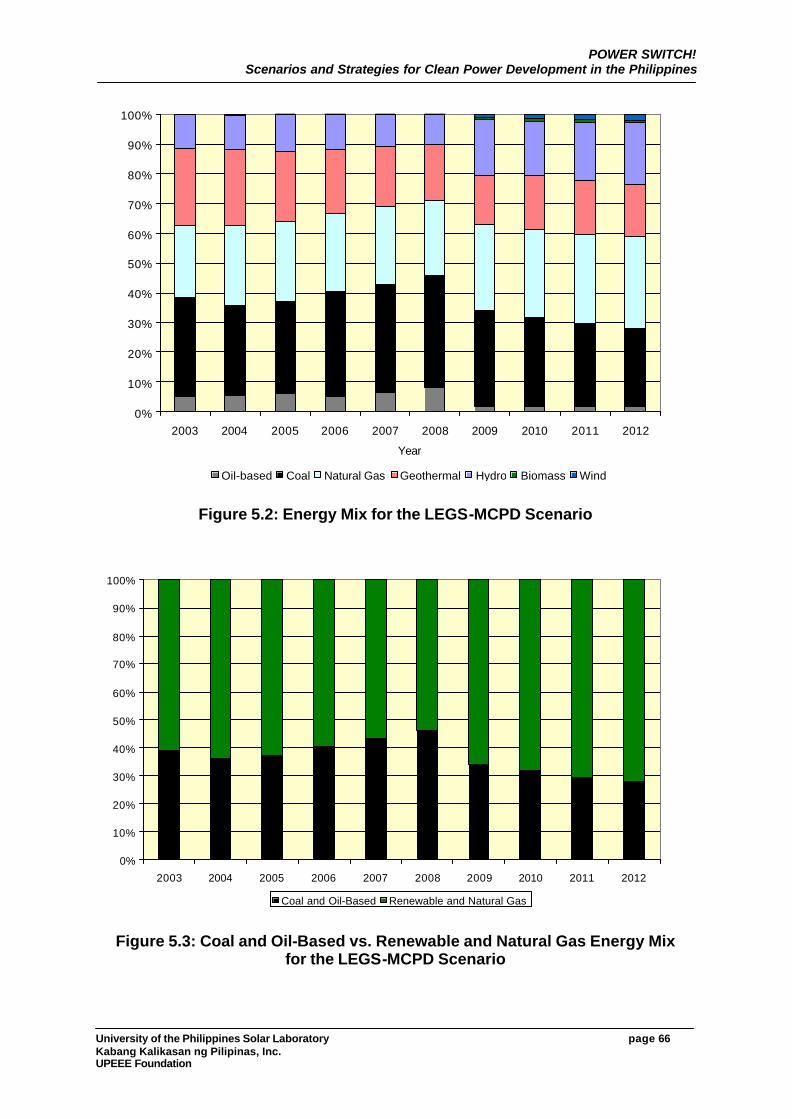

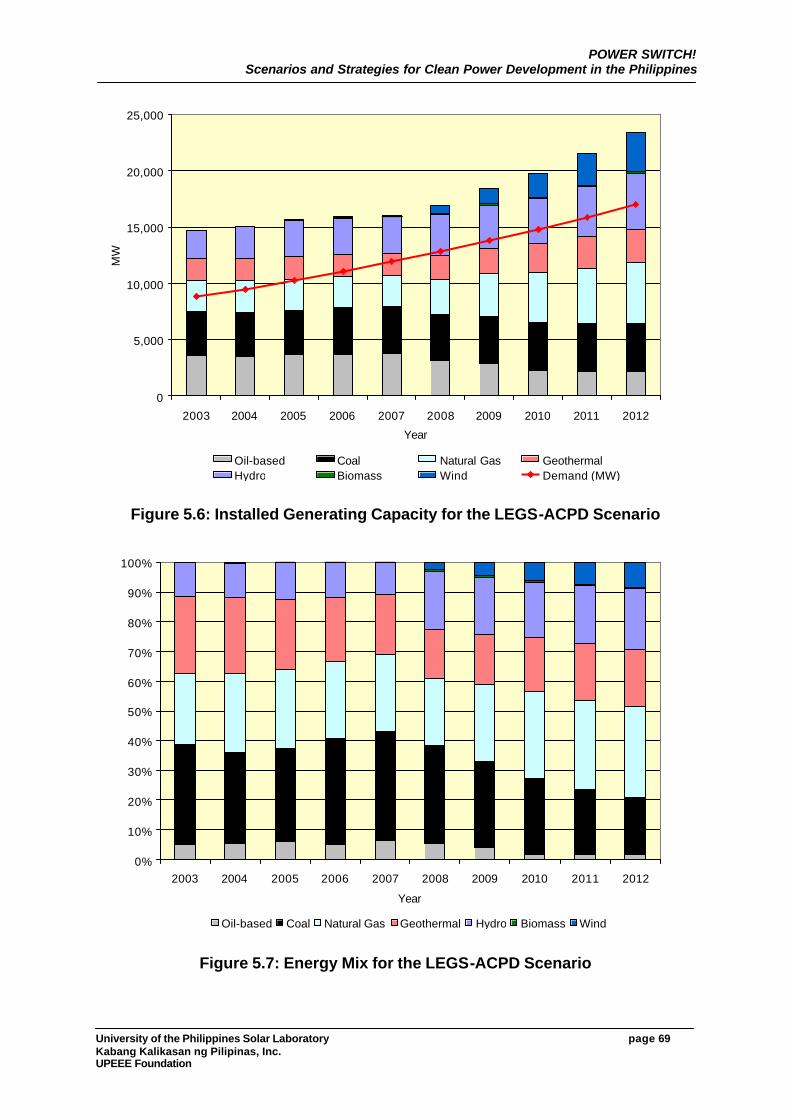

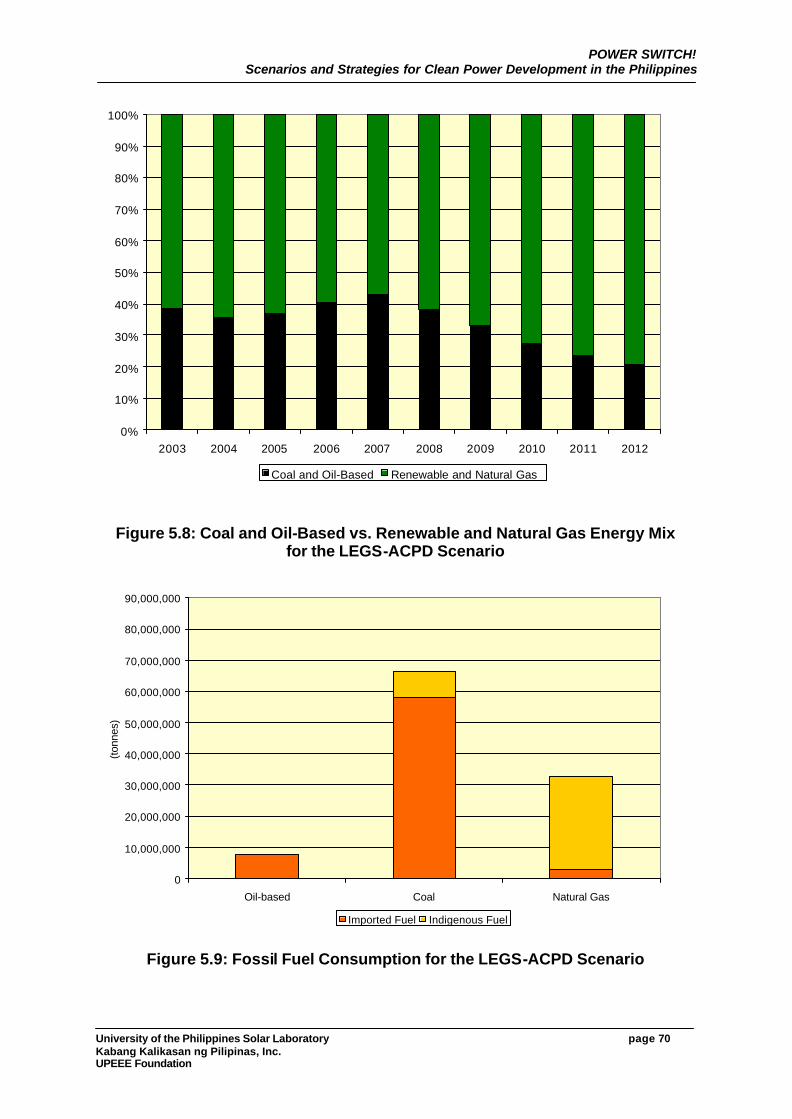

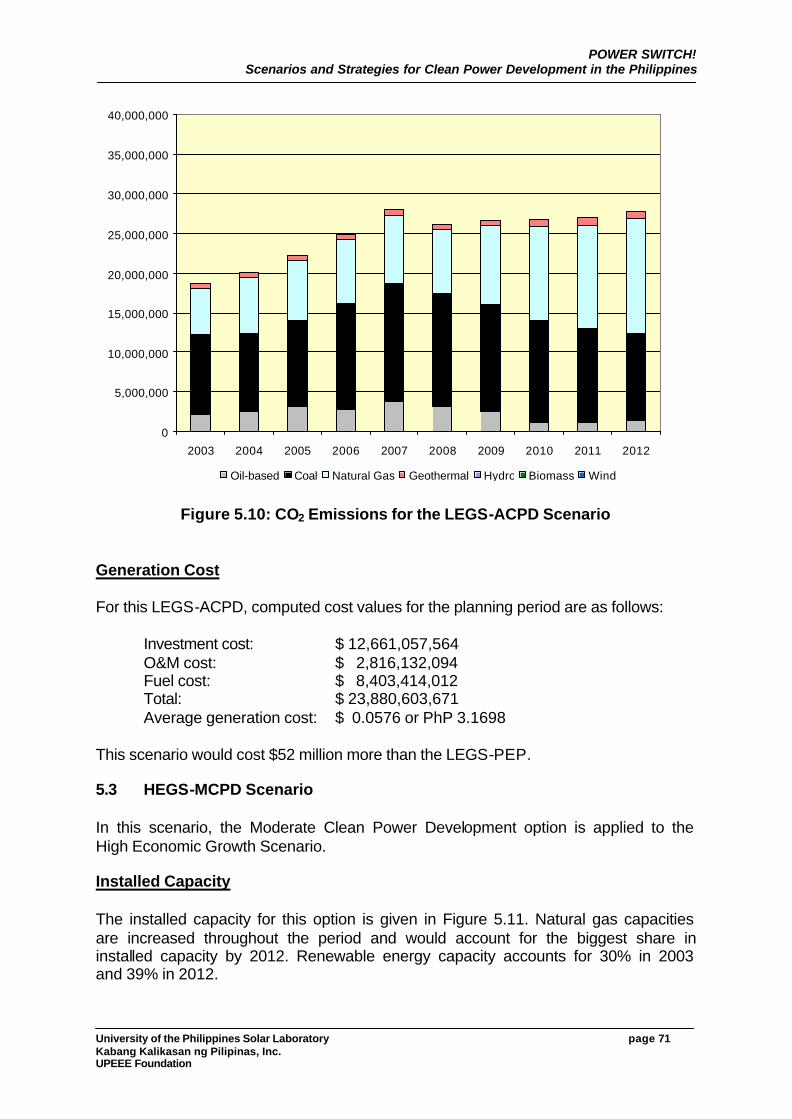

5.2 LEGS-ACPD Scenario...........................................................................68

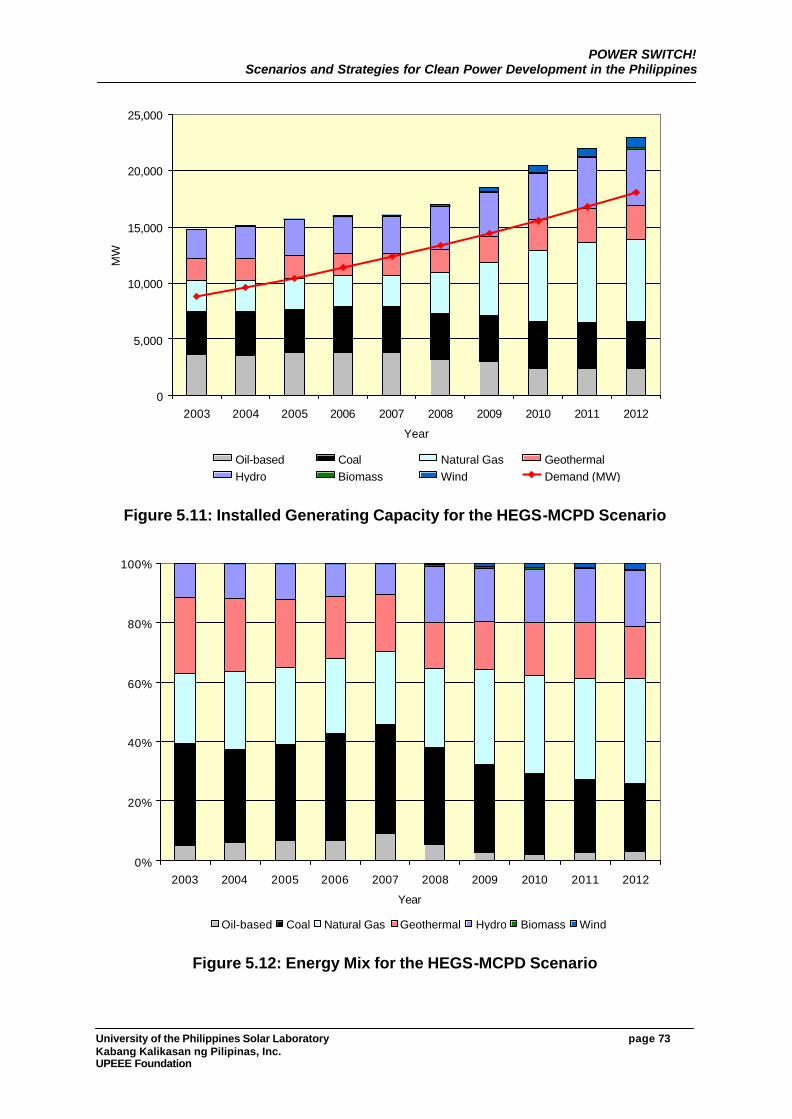

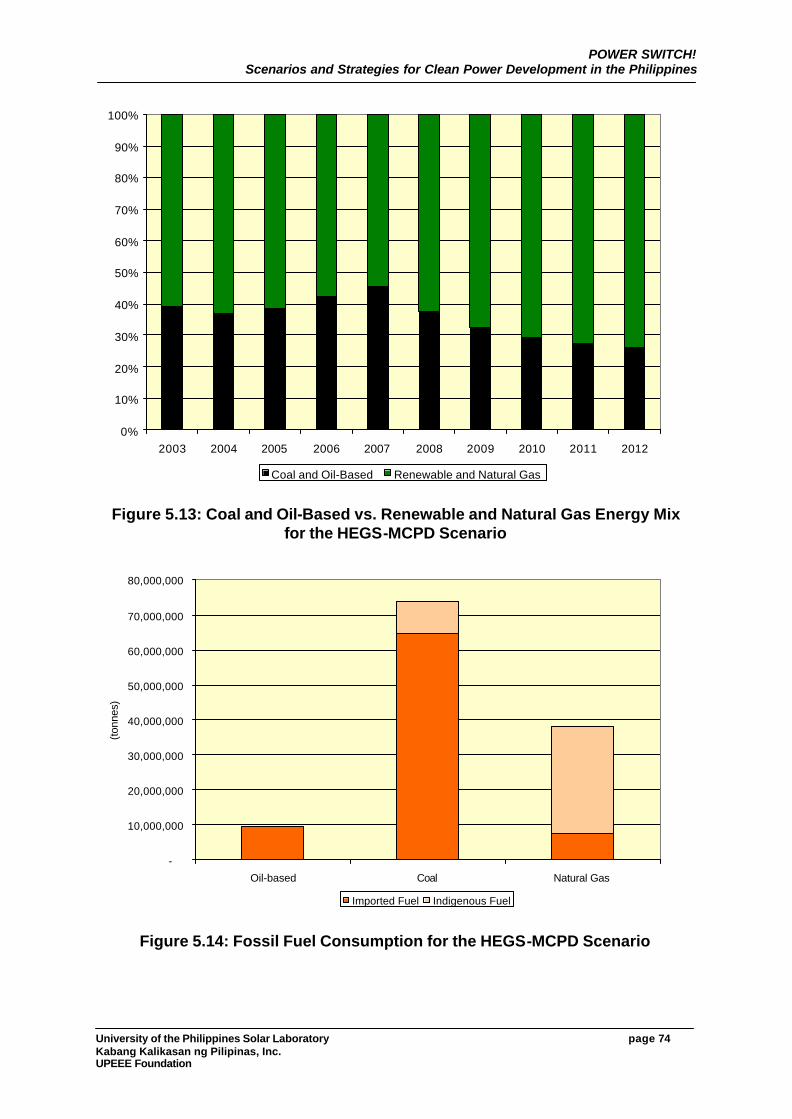

5.3 HEGS-MCPD Scenario .........................................................................71

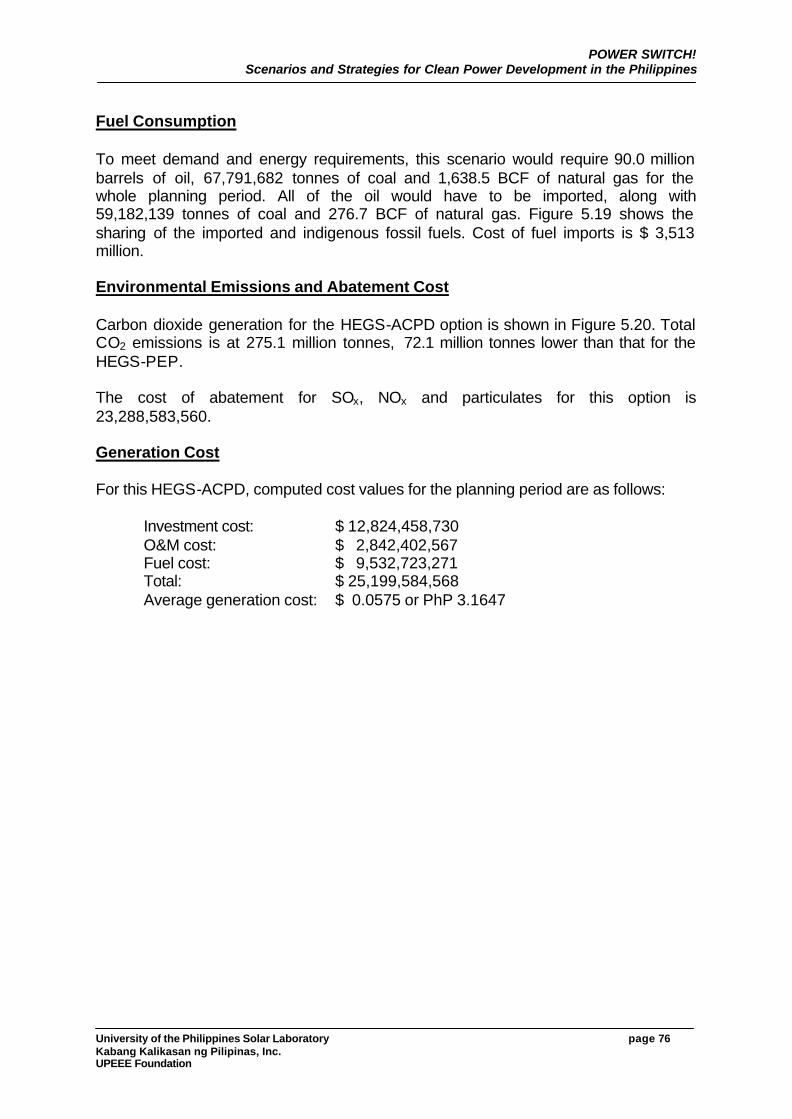

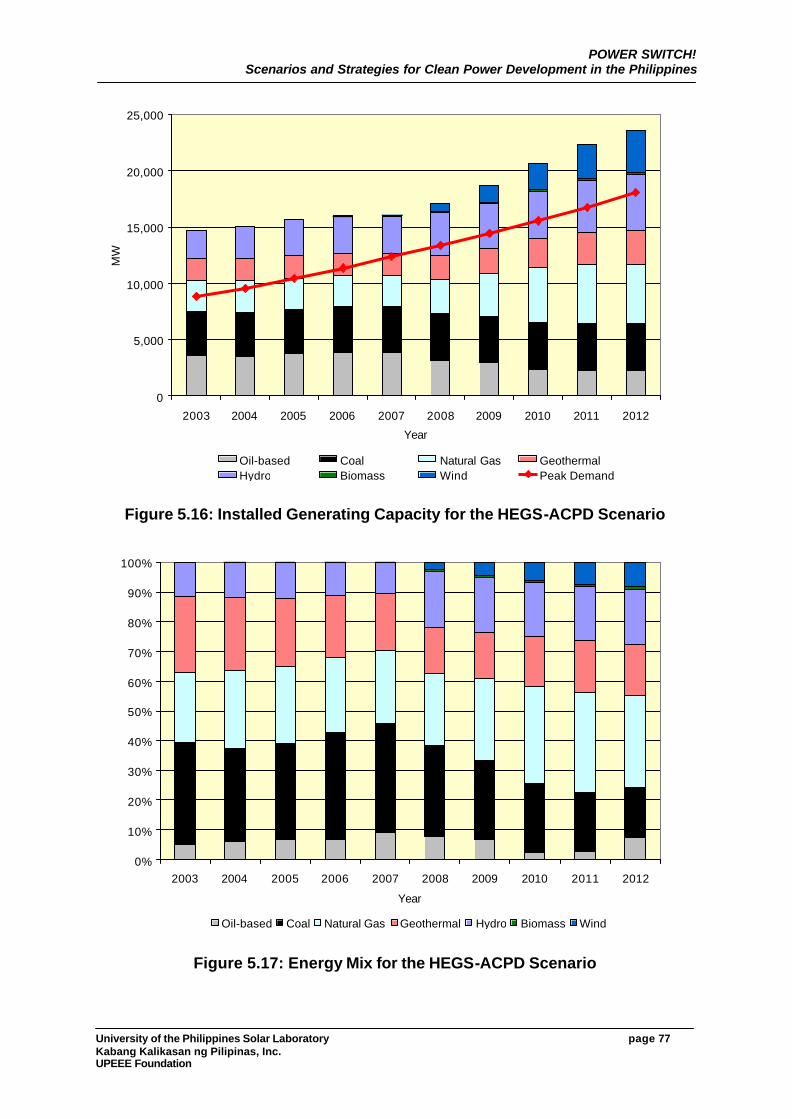

5.4 HEGS-ACPD Scenario..........................................................................75

6 CONCLUSIONS AND RECOMMENDATIONS............................................81

6.1 Energy Planning .....................................................................................81

6.2 Transmission and Distribution Development .....................................82

6.3 Rules and Regulation ............................................................................82

6.4 Incentive Programs ................................................................................83

7 REFERENCES ...................................................................................................84

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page iii Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

LIST OF FIGURES

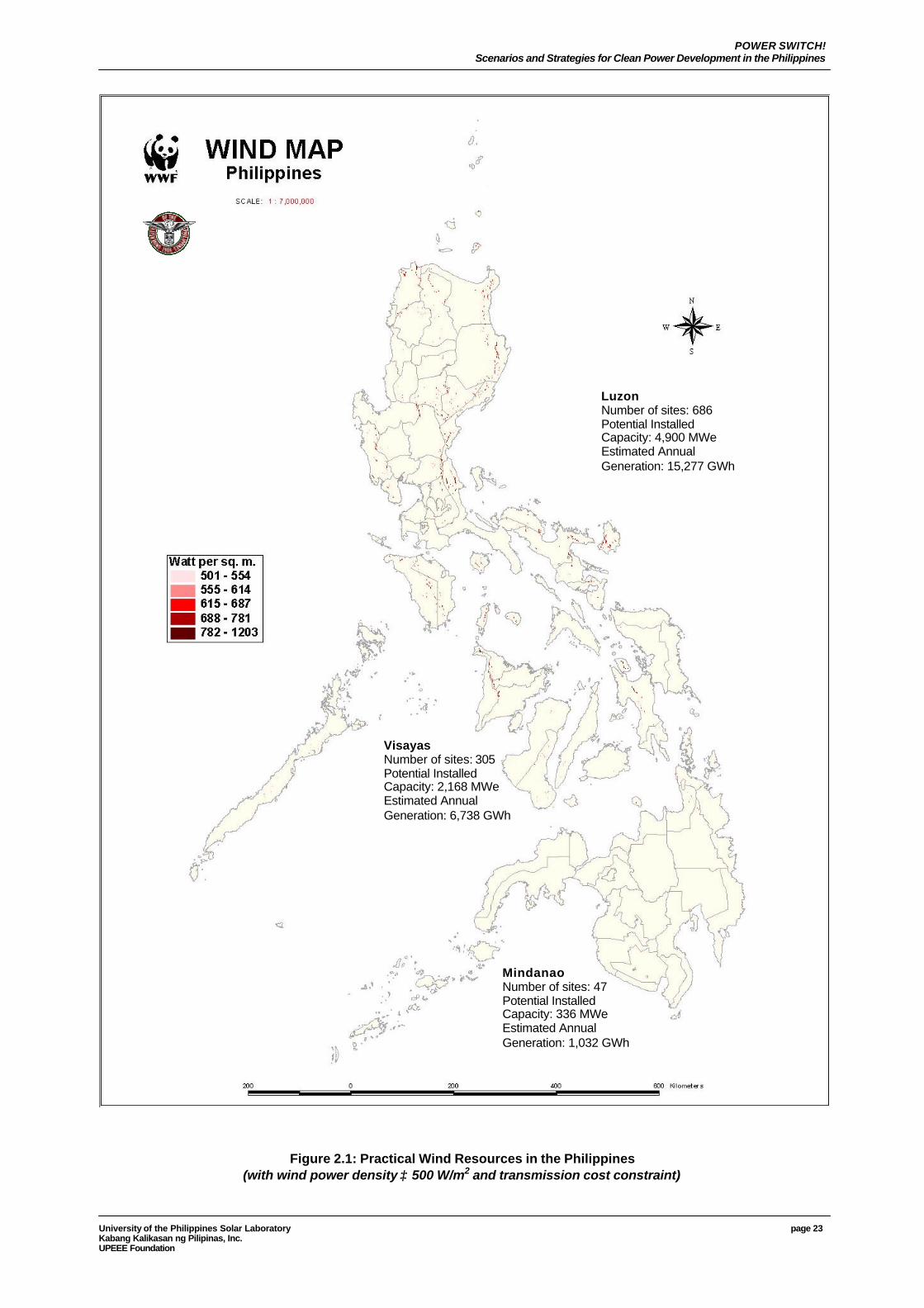

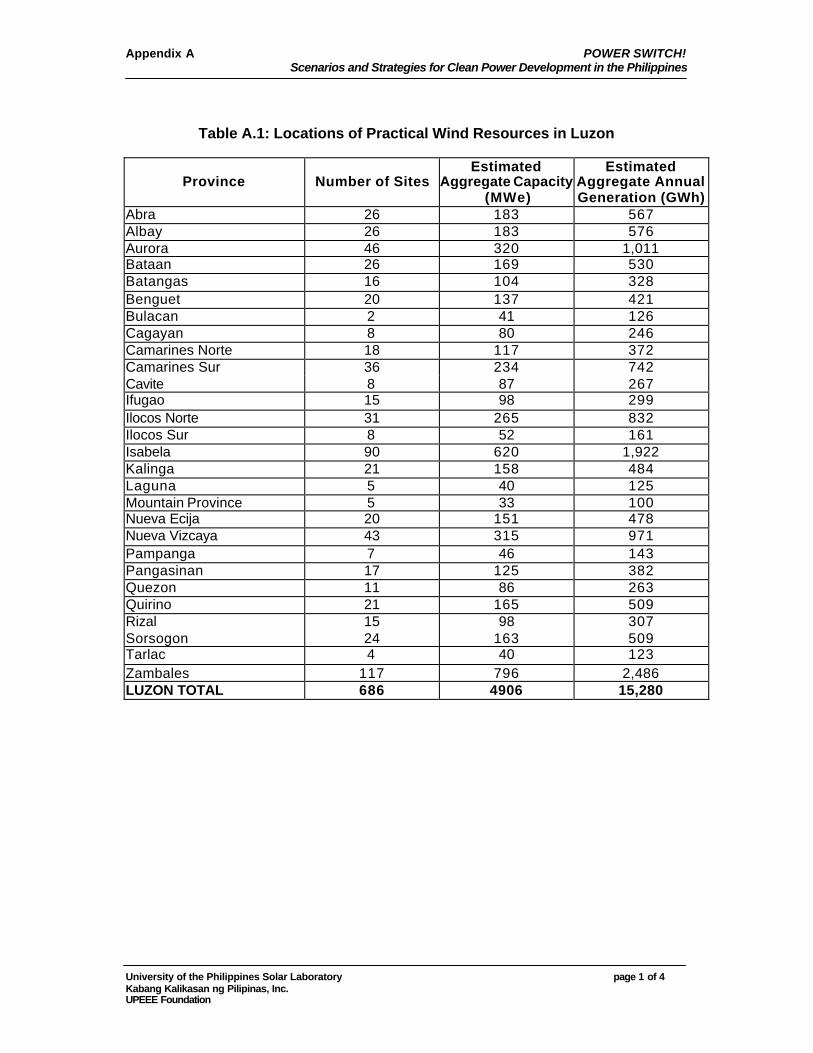

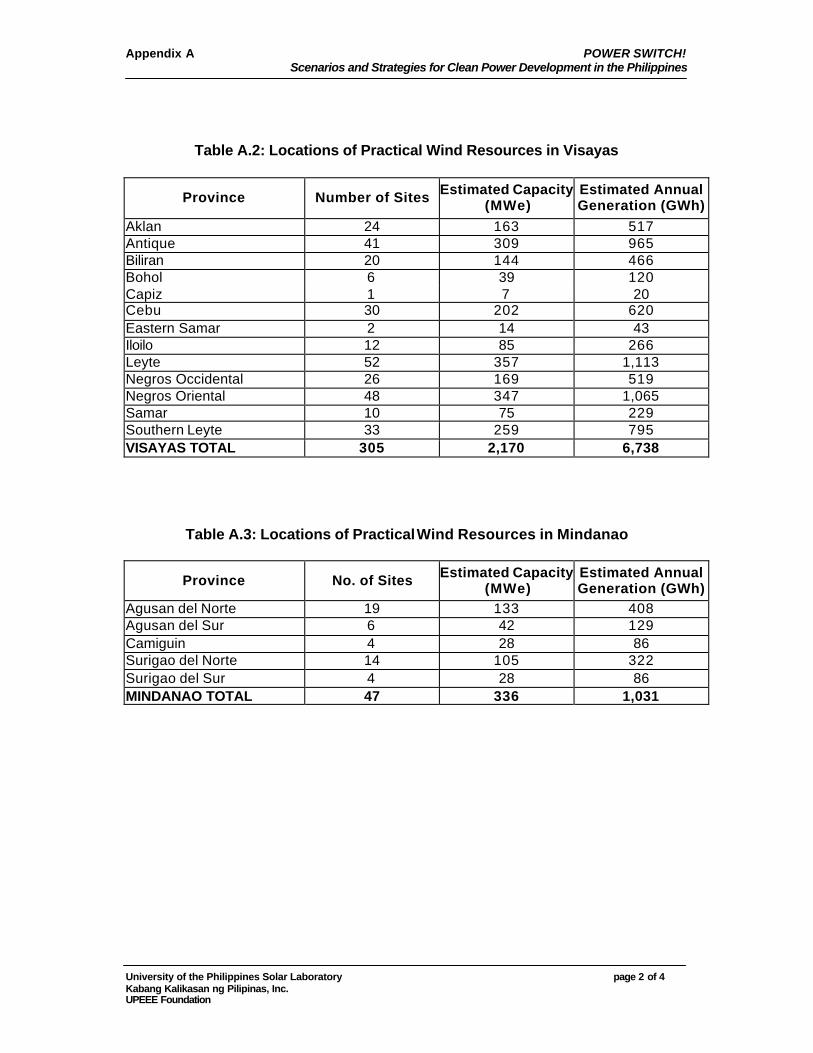

Figure 2.1 Practical Wind Resources in the Philippines .....................................23

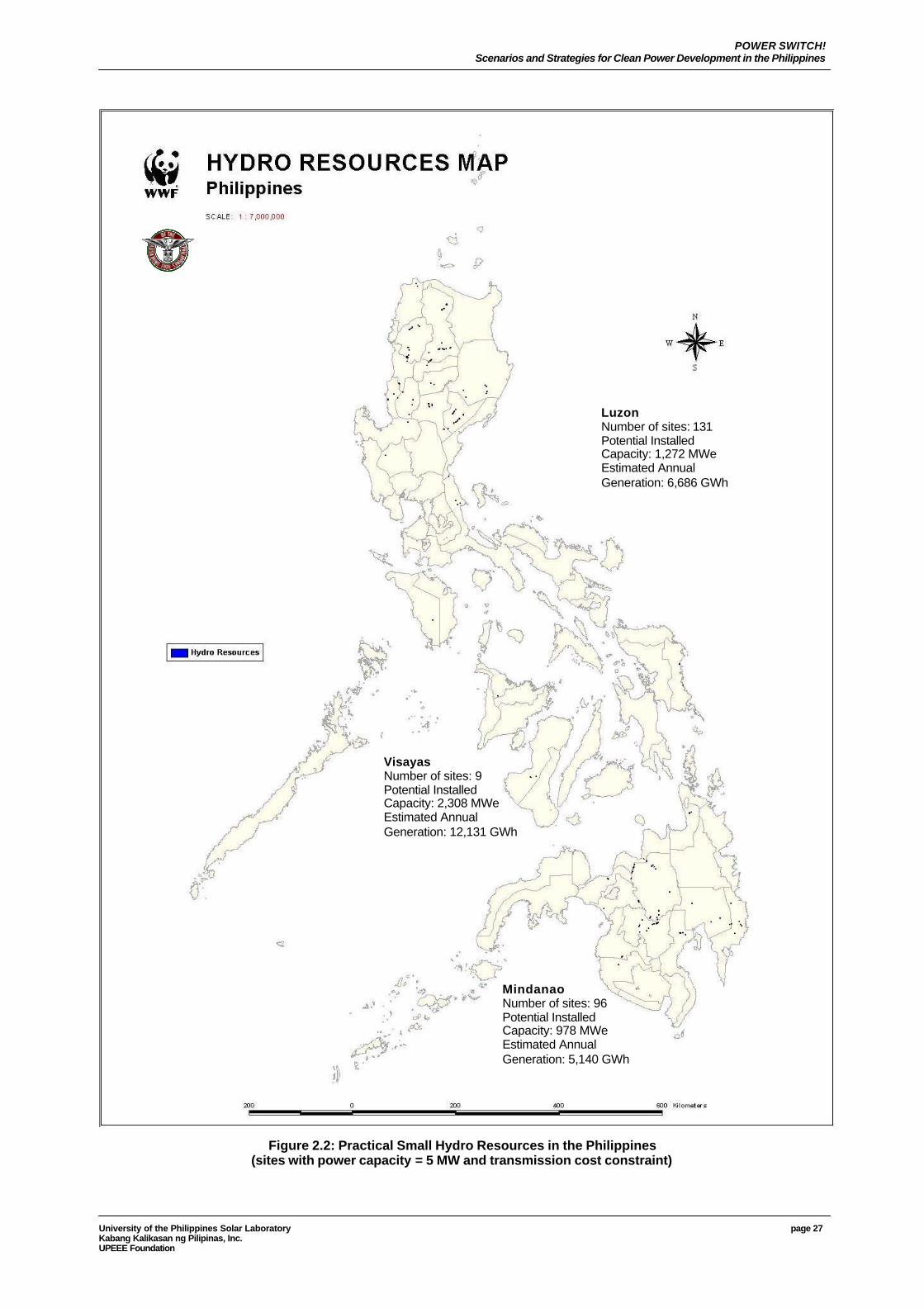

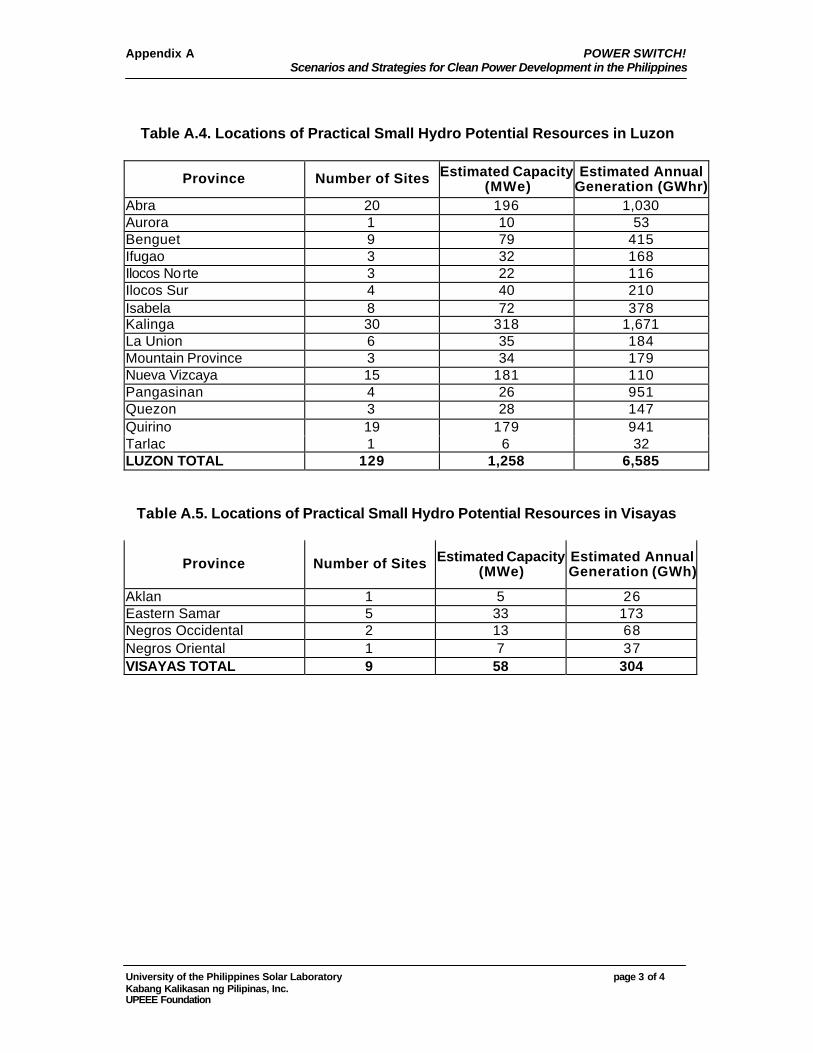

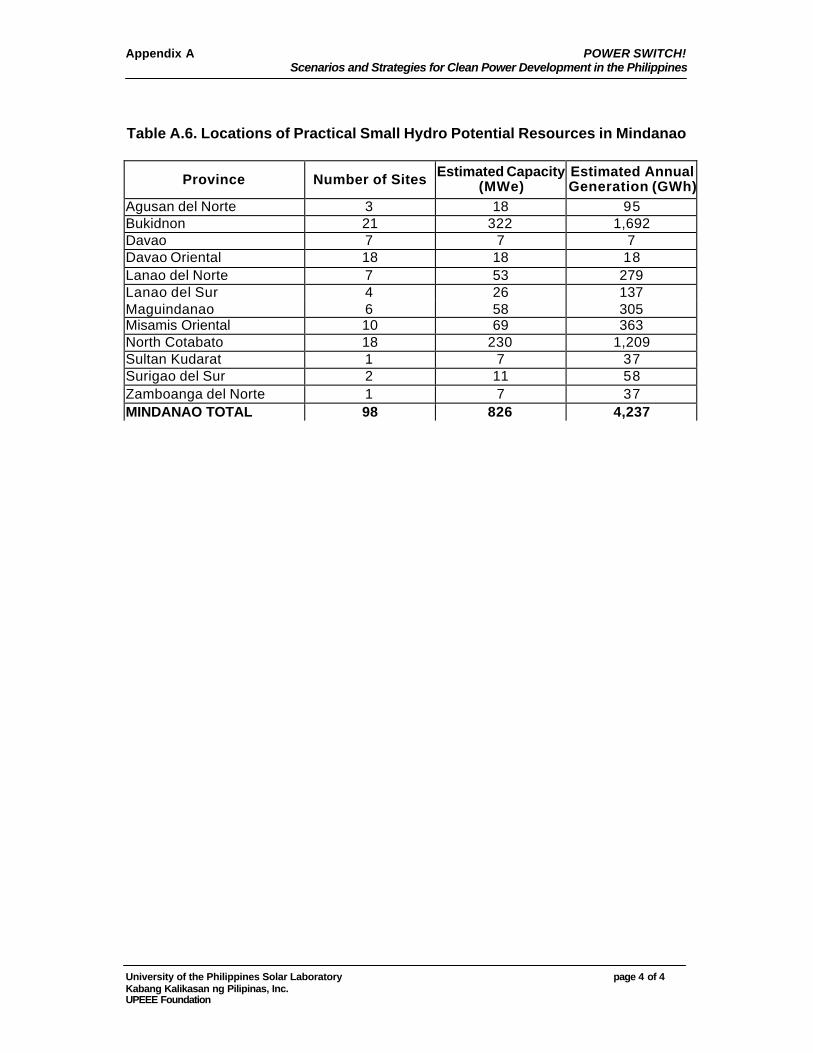

Figure 2.2 Practical Small Hydro Resources in the Philippines.........................27

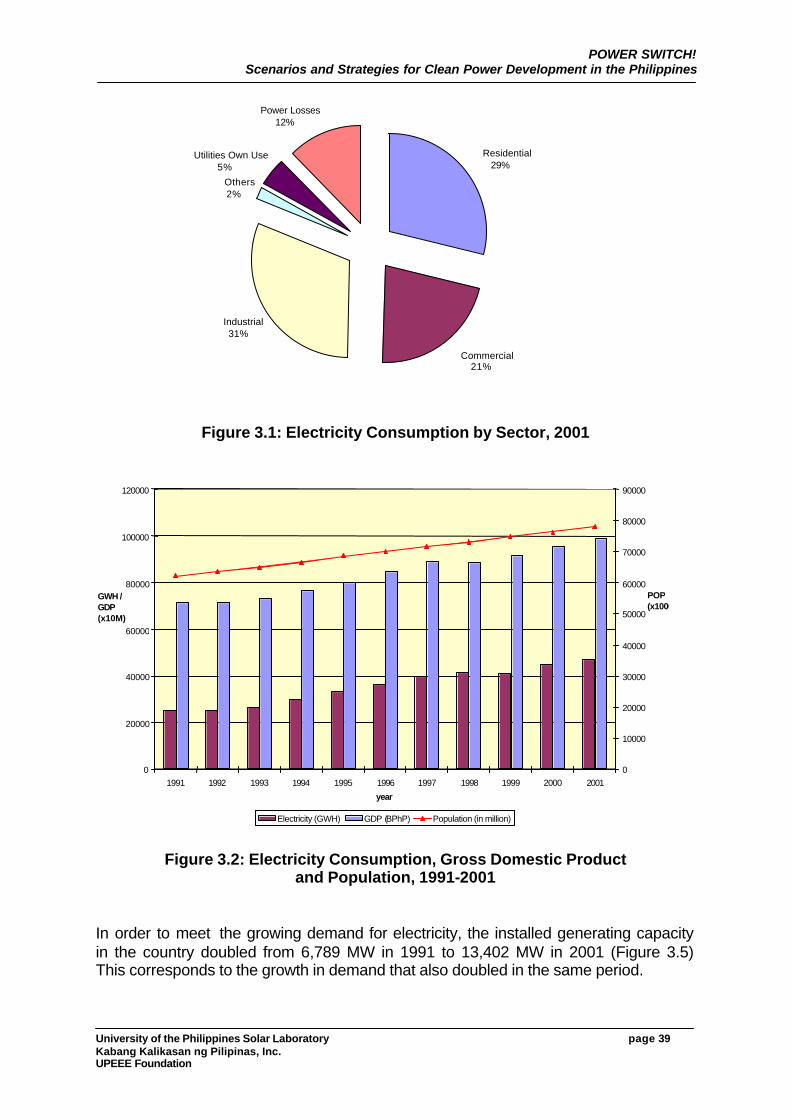

Figure 3.1 Electricity Consumption by Sector, 2001............................................39

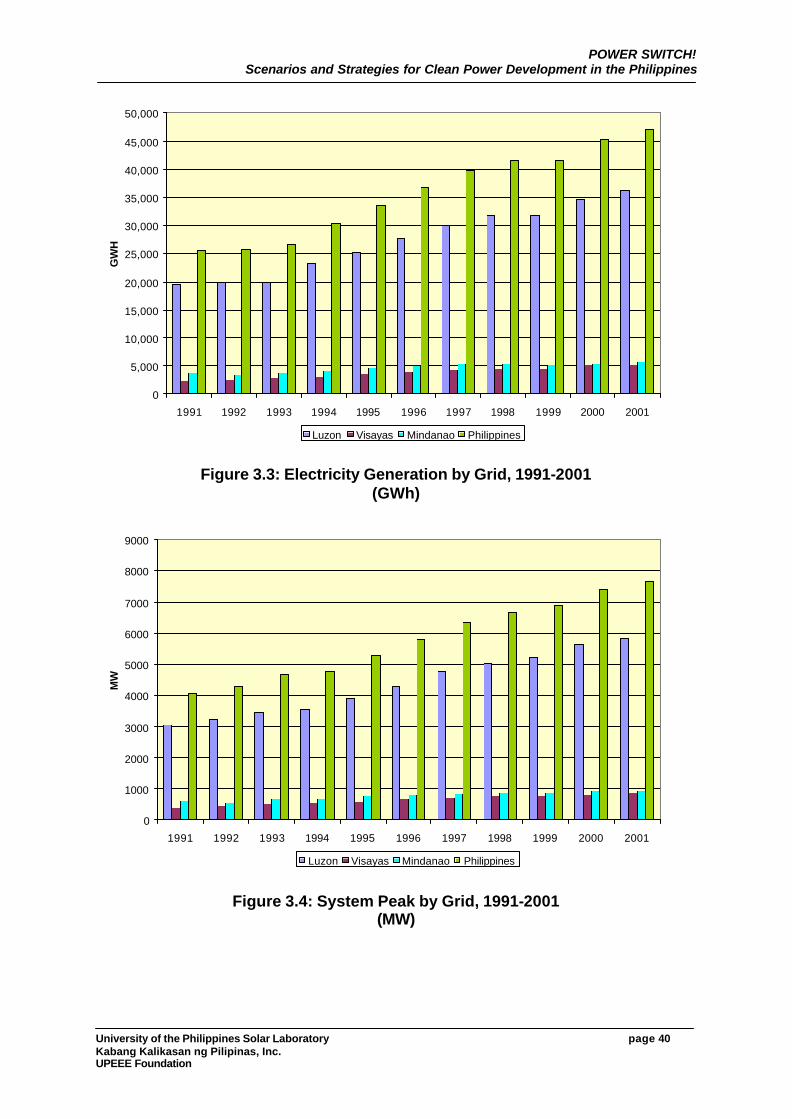

Figure 3.2 Electricity Consumption, Gross Domestic Product and Population, 1991-2001 ..........................................................................39

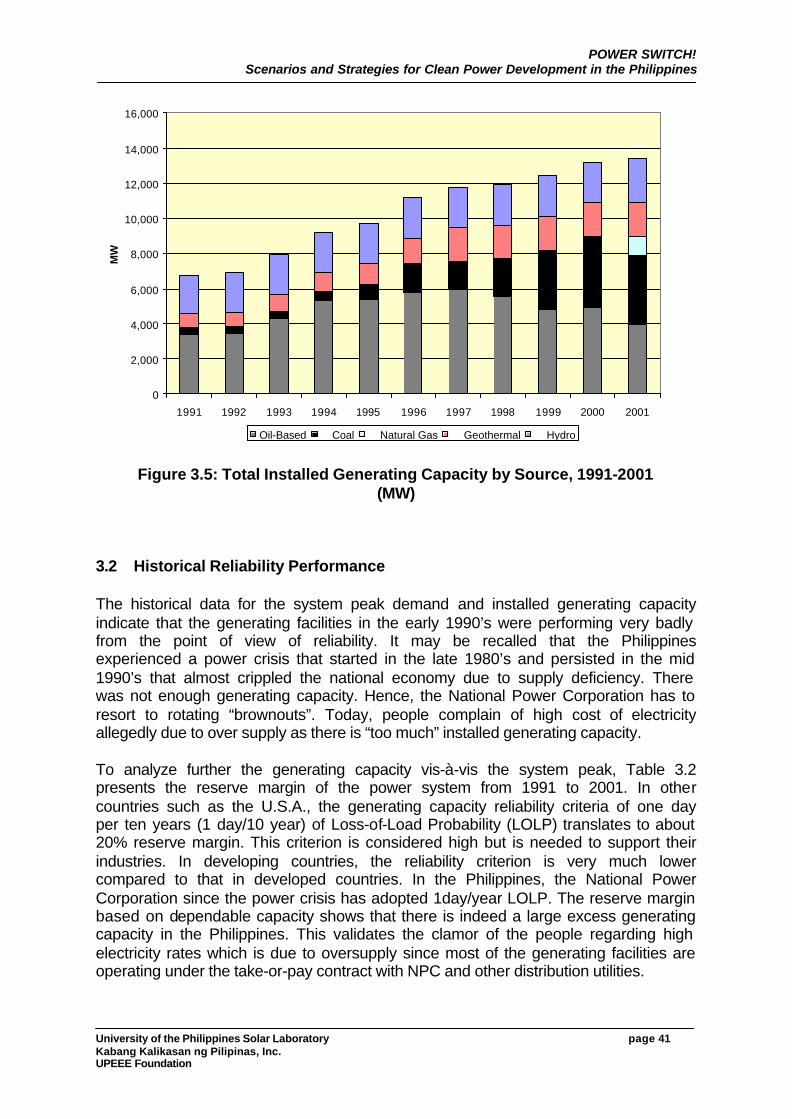

Figure 3.3 Electricity Generation by Grid, 1991-2001 .........................................40

Figure 3.4 System Peak by Grid, 1991-2001........................................................40

Figure 3.5 Total Installed Generating Capacity by Source, 1999-2001..........................................................................................................41

Figure 3.6 Carbon Dioxide Emissions by Fuel Type, 1999-2001 ......................43

Figure 3.7 Energy Mix, 1999-2001 .........................................................................44

Figure 3.8 Share of Renewable and Non-Renewable Energy in the Energy Mix, 1999-2001...................................................................45

Figure 3.9 Energy Mix and Carbon Dioxide Emissions, 1991-2001..........................................................................................................45

Figure 4.1 National Energy Planning Process ......................................................49

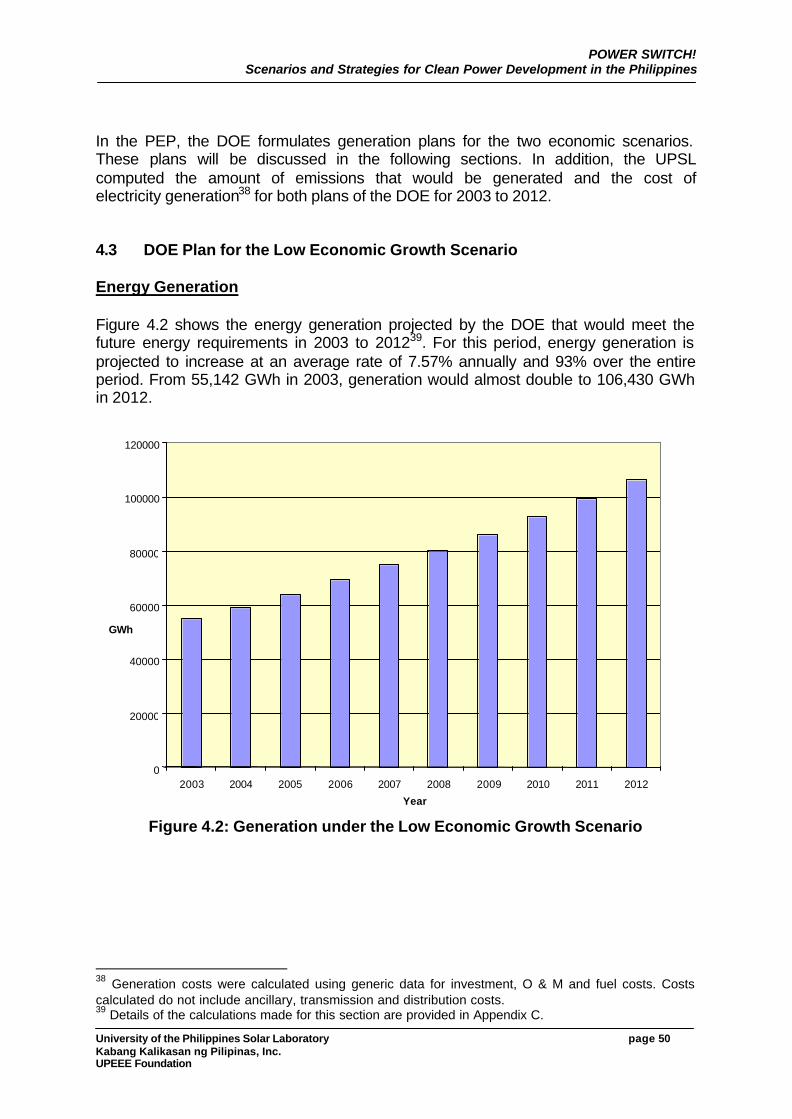

Figure 4.2 Generation under the Low Economic Growth Scenario...................50

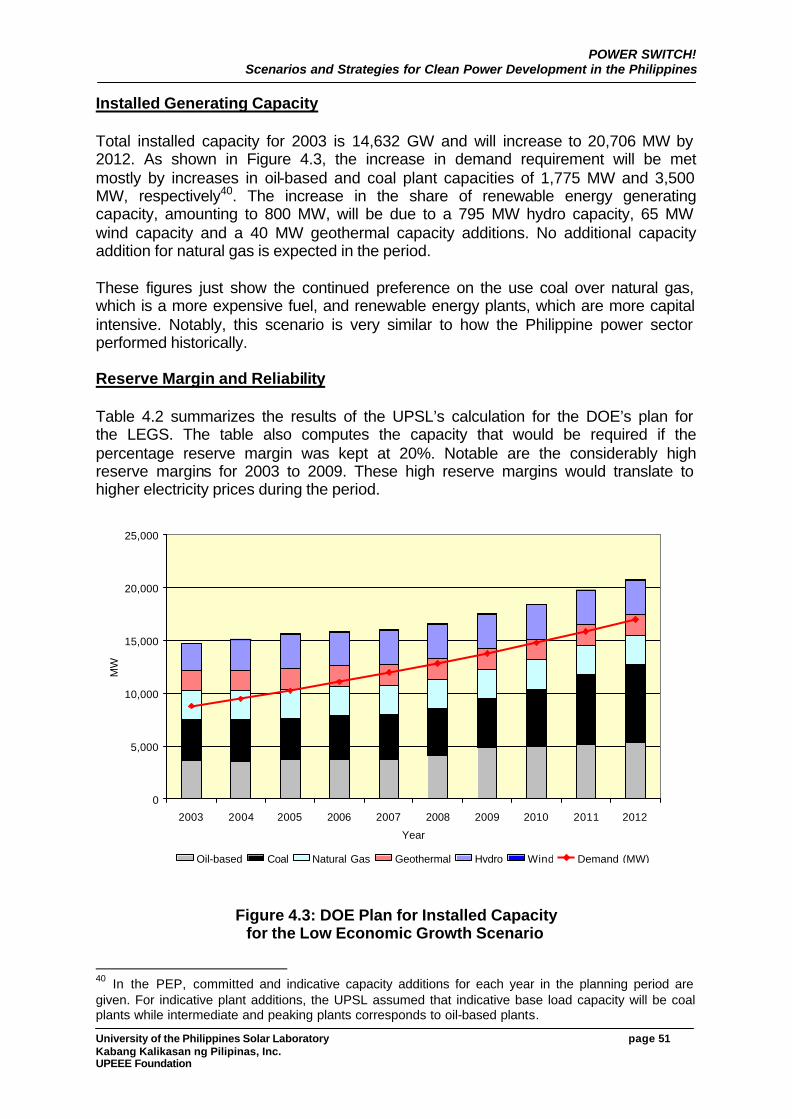

Figure 4.3 DOE Plan for Installed Capacity for the Low Economic Growth Scenario.....................................................................................51

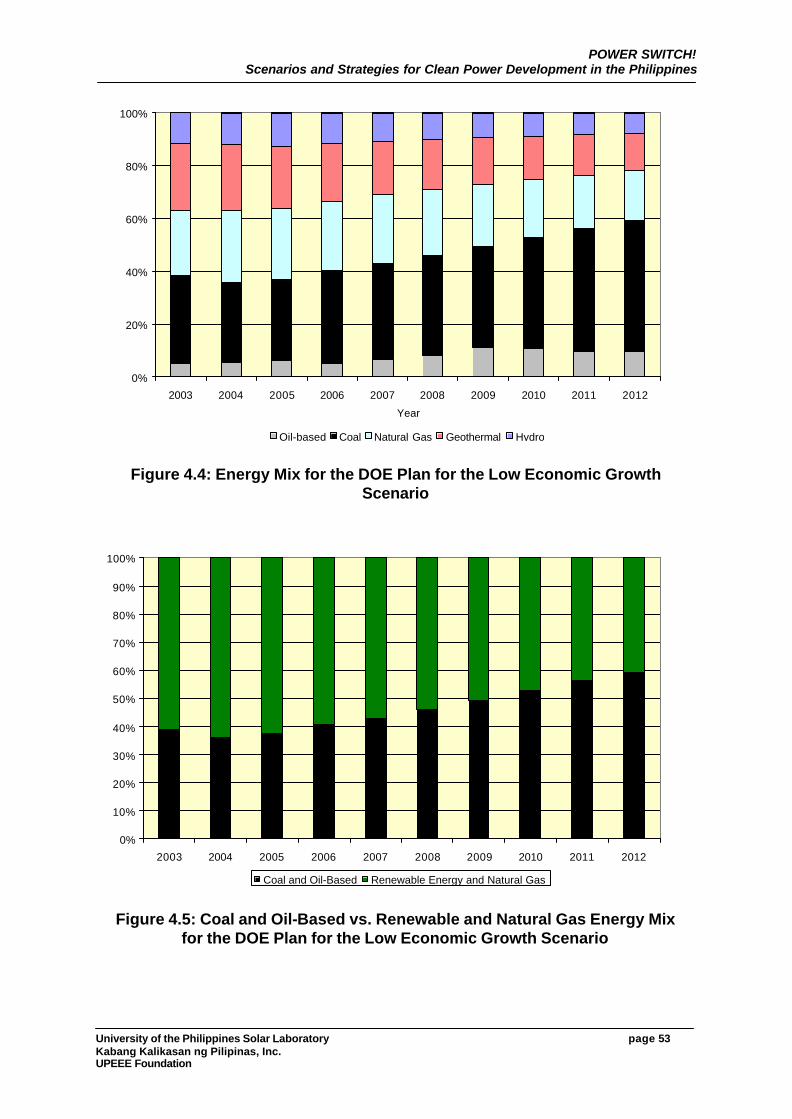

Figure 4.4 Energy Mix for the DOE Plan for the Low Economic Growth Scenario.....................................................................................53

Figure 4.5 Coal and Oil-Based vs. Renewable and Natural Gas Energy Mix for the DOE Plan for the Low Economic Growth Scenario.....................................................................................53

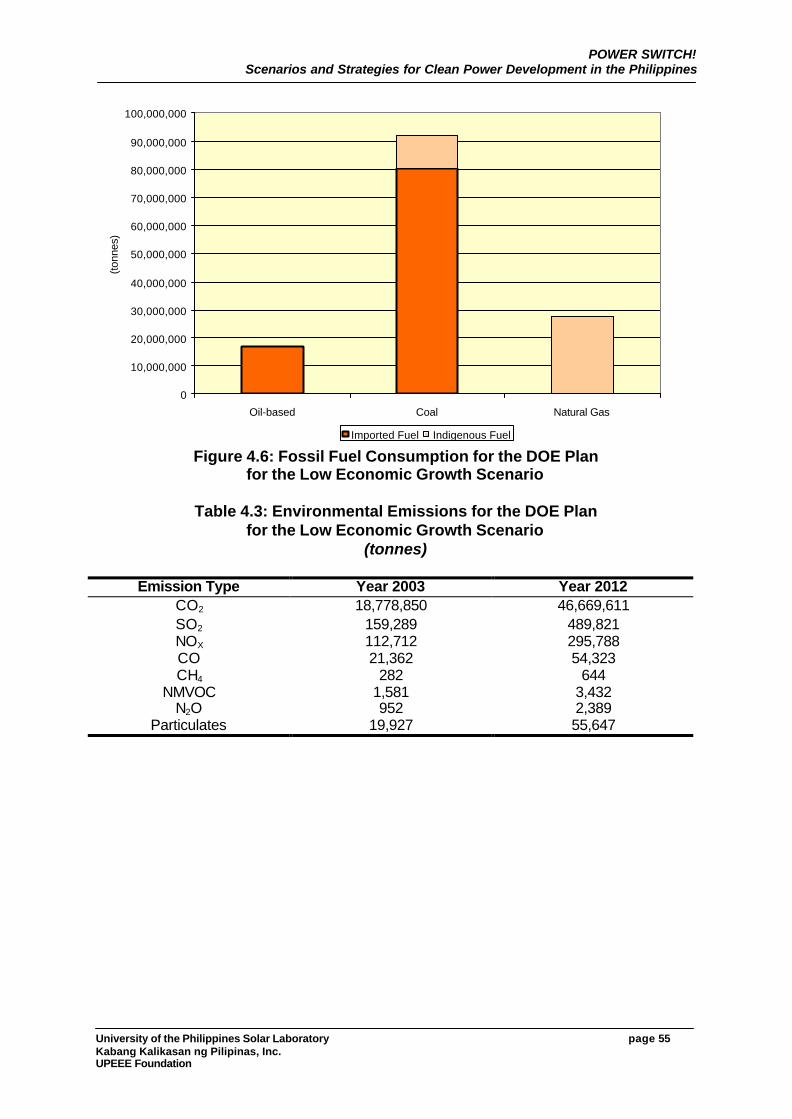

Figure 4.6 Fossil Fuel Consumption for the DOE Plan for the Low Economic Growth Scenario..........................................................55

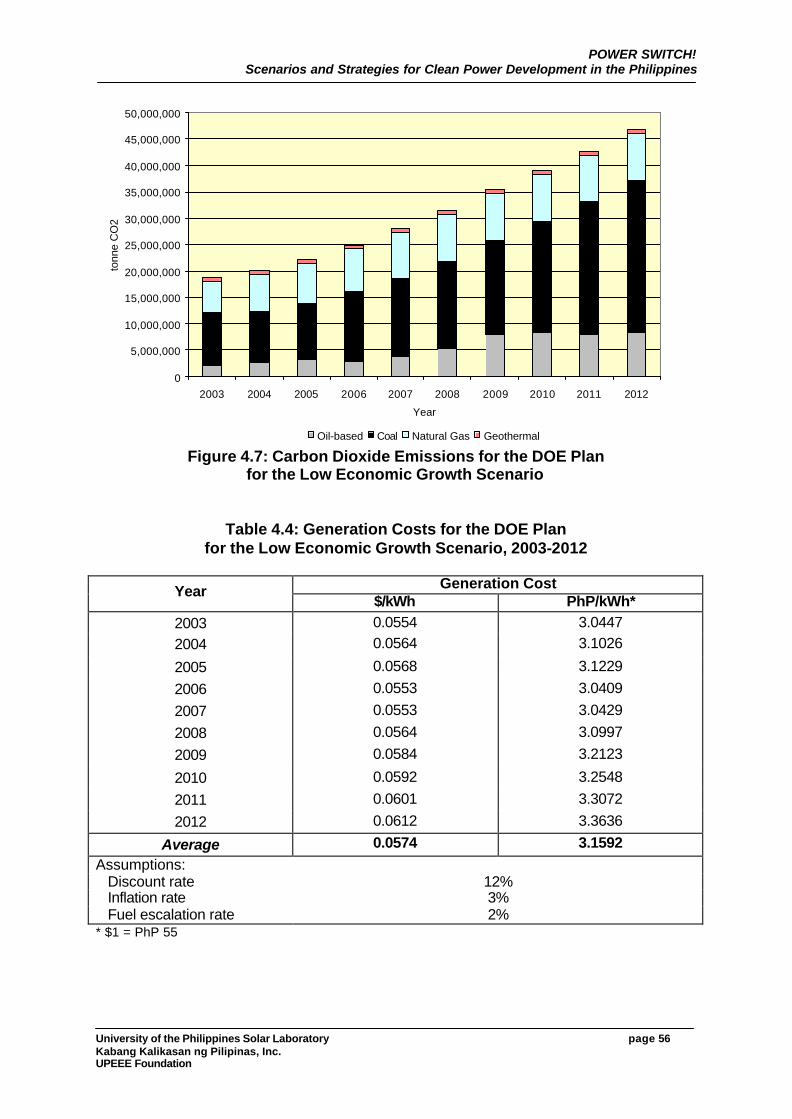

Figure 4.7 Carbon Dioxide Emissions for the DOE Plan for the Low Economic Growth Scenario..........................................................56

Figure 4.8 Generation under the High Economic Growth Scenario...................................................................................................57

Figure 4.9 DOE Plan for Installed Capacity for the High Economic Growth Scenario ..................................................................58

Figure 4.10 Energy Mix for the DOE Plan for the High Economic Growth Scenario.....................................................................................59

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page iv Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Figure 4.11 Share of Renewable and Non-Renewable Energy in the Energy Mix for the DOE Plan for the High Economic Growth Scenario ..................................................................60

Figure 4.12 Fossil Fuel Consumption for the DOE Plan for the High Economic Growth Scenario.........................................................60

Figure 4.13 Carbon Dioxide Emissions for the DOE Plan for the High Economic Growth Scenario.........................................................62

Figure 5.1 Installed Generating Capacity for the LEGS-MCPD Scenario...................................................................................................65

Figure 5.2 Energy Mix for the LEGS-MCPD Scenario ........................................66

Figure 5.3 Coal and Oil-Based vs. Renewable and Natural Gas Energy Mix for the LEGS-MCPD Scenario ........................................66

Figure 5.4 Fossil Fuel Consumption for the LEGS-MCPD Scenario...................................................................................................67

Figure 5.5 CO2 Emissions for the LEGS-MCPD Scenario..................................67

Figure 5.6 Installed Generating Capacity for the LEGS-ACPD Scenario...................................................................................................69

Figure 5.7 Energy Mix for the LEGS-ACPD Scenario .........................................69

Figure 5.8 Coal and Oil-Based vs. Renewable and Natural Gas Energy Mix for the LEGS-ACPD Scenario .........................................70

Figure 5.9 Fossil Fuel Consumption for the LEGS-ACPD Scenario...................................................................................................70

Figure 5.10 CO2 Emissions for the LEGS-ACPD Scenario ..................................71

Figure 5.11 Installed Generating Capacity for the HEGS-MWPP Scenario...................................................................................................73

Figure 5.12 Energy Mix for the HEGS-MCPD Scenario........................................73

Figure 5.13 Coal and Oil-Based vs. Renewable and Natural Gas Energy Mix for the HEGS-MCPD Scenario........................................74

Figure 5.14 Fossil Fuel Consumption for the HEGS-MCPD Scenario...................................................................................................74

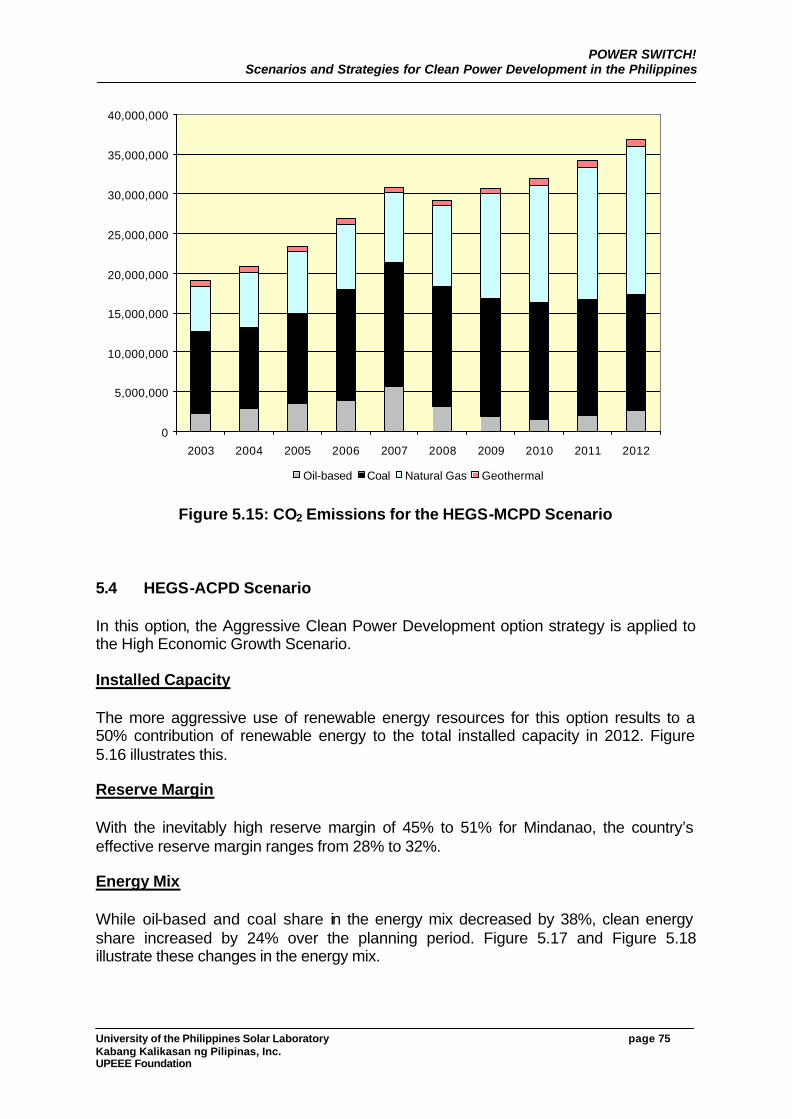

Figure 5.15 CO2 Emissions for the HEGS-MCPD Scenario.................................75

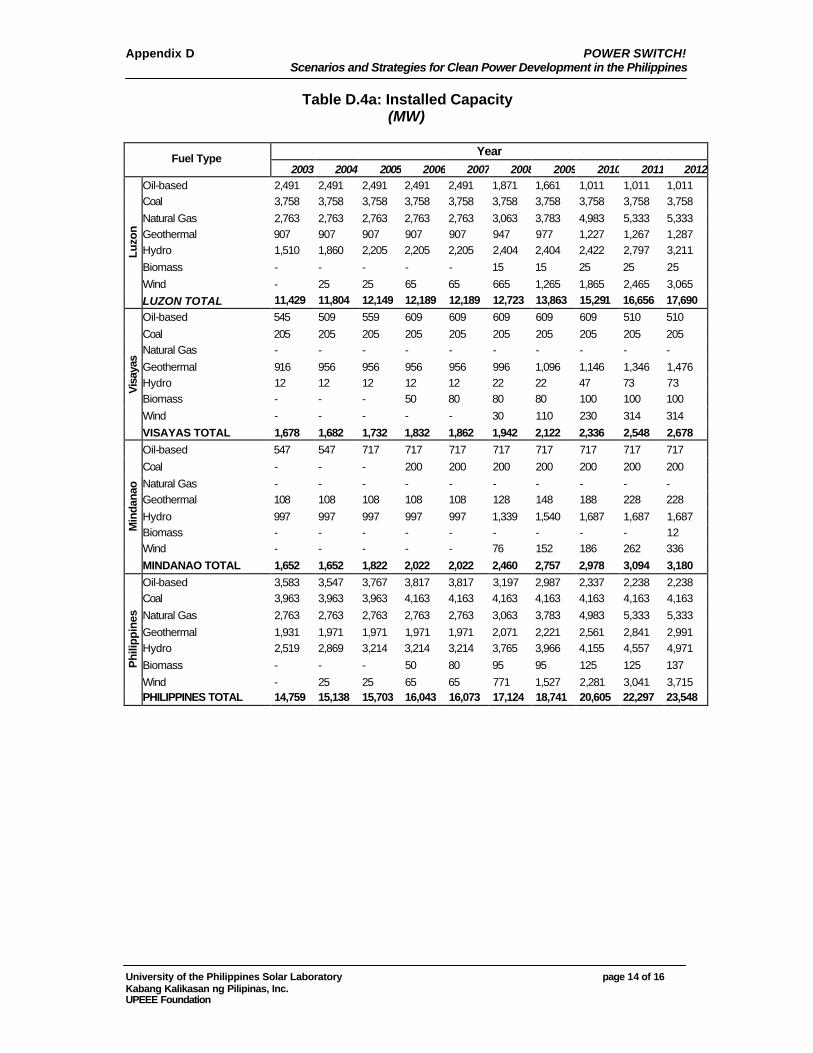

Figure 5.16 Installed Generating Capacity for the HEGS-ACPD Scenario...................................................................................................77

Figure 5.17 Energy Mix for the HEGS-ACPD Scenario ........................................77

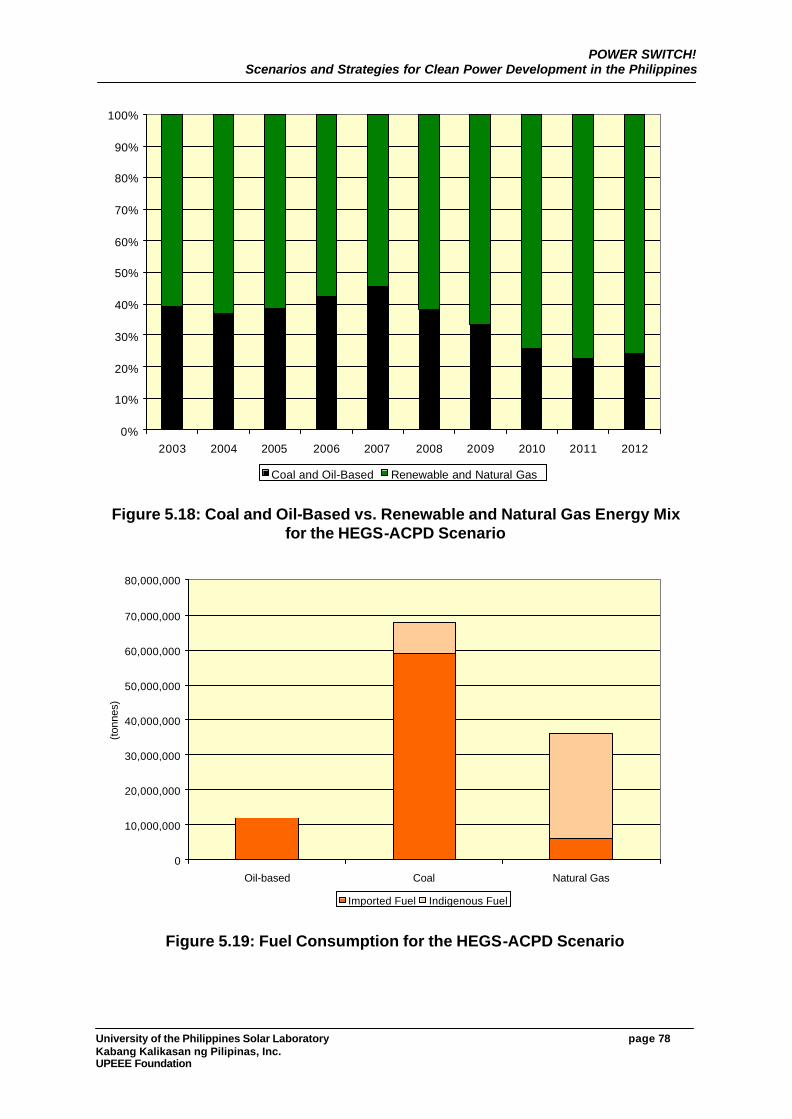

Figure 5.18 Coal and Oil-Based vs. Renewable and Natural Gas Energy Mix for the HEGS-ACPD Scenario ........................................78

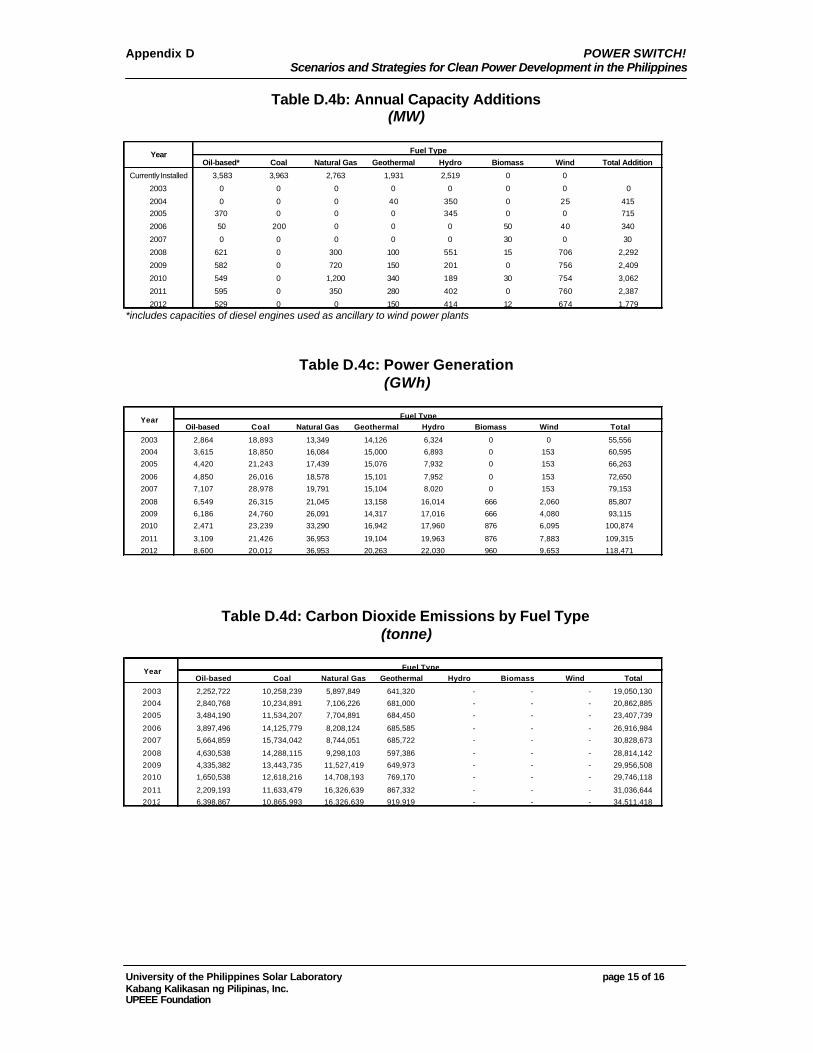

Figure 5.19 Fuel Consumption for the HEGS-ACPD Scenario............................78

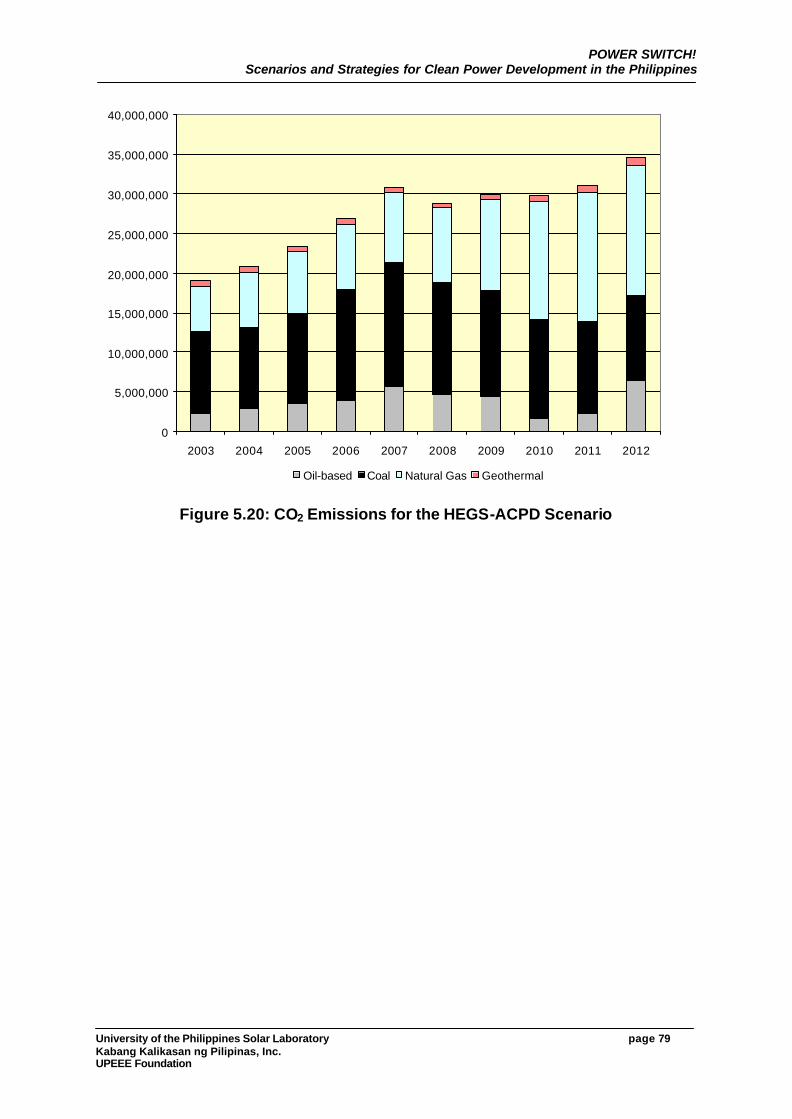

Figure 5.20 CO2 Emissions for the HEGS-ACPD Scenario..................................79

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page v Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

LIST OF TABLES

Table 1.1 Cost Comparison of Power Plants......................................................... 2

Table 1.2 Typical Capacity Factors of Power Plants

and Levelized Generation Costs............................................................ 2

Table 2.1 1994 Philippine Greenhouse Gas Emissions by Sector ..................13

Table 2.2 1994 Greenhouse Gas Emissions from the

Philippine Energy Sector .......................................................................13

Table 2.3 Philippine Wind Electric Potential ........................................................22

Table 2.4 Practical Wind Resources in the Philippines .....................................22

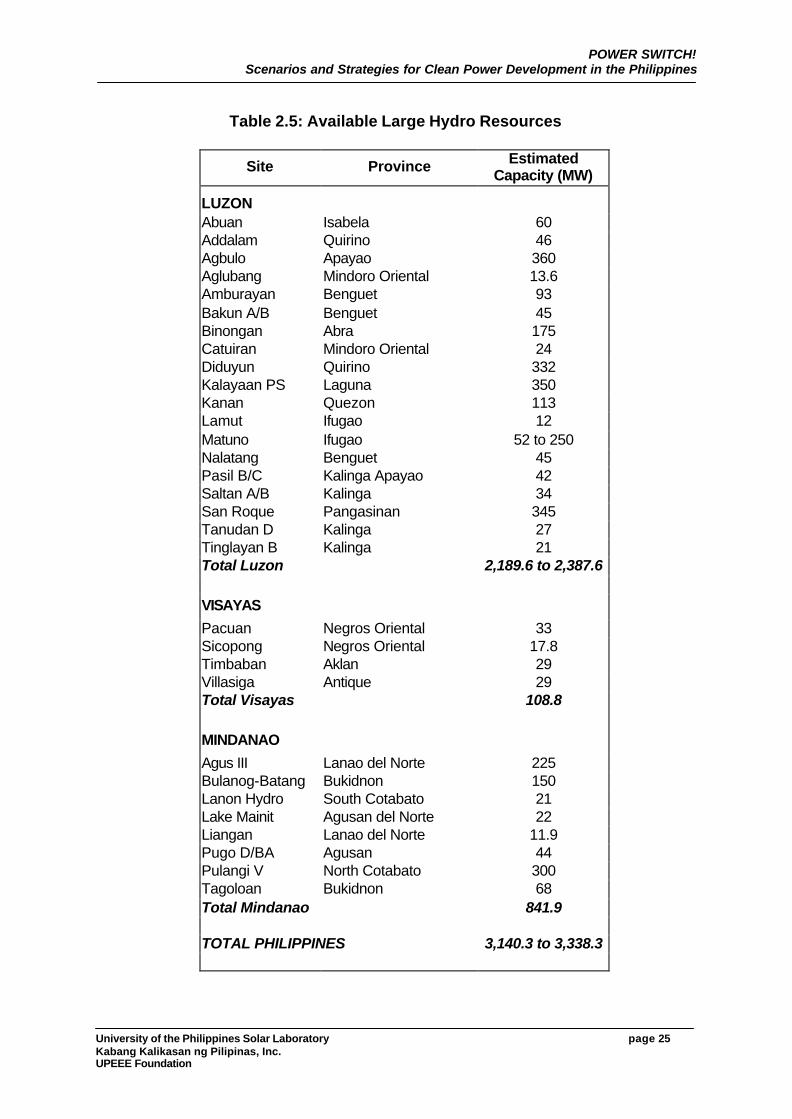

Table 2.5 Available Large Hydro Resources .......................................................25

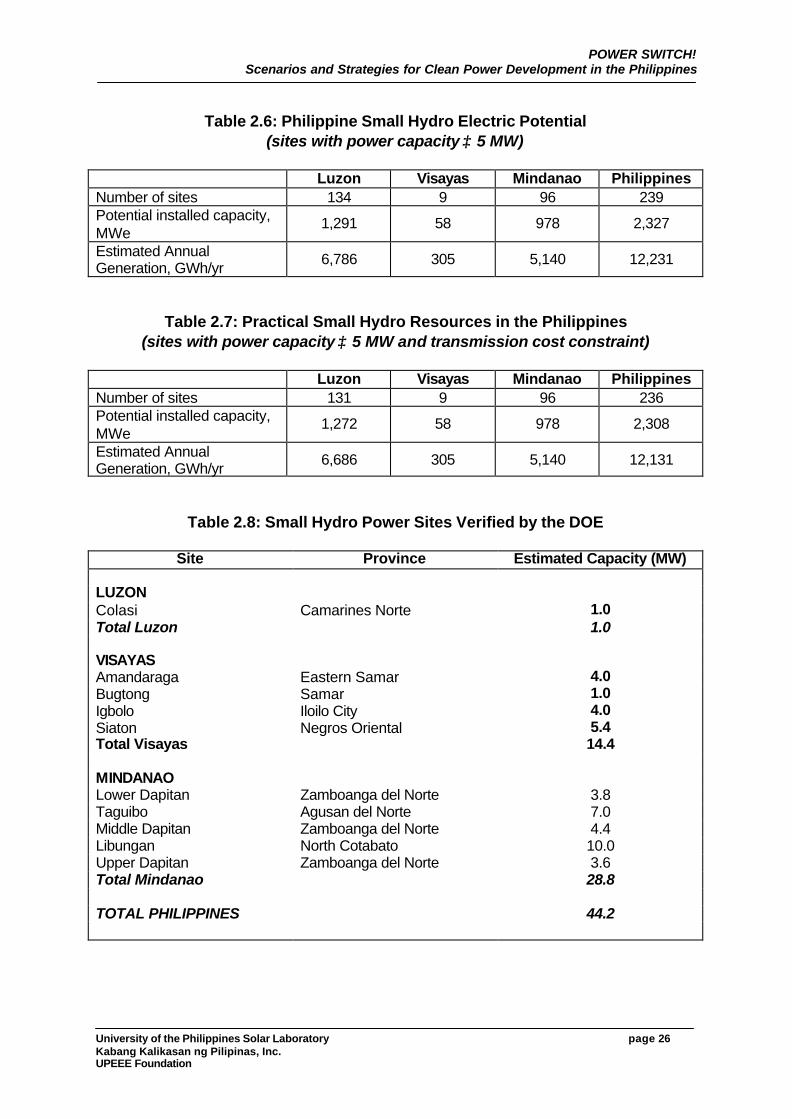

Table 2.6 Philippine Small Hydro Electric Potential ...........................................26

Table 2.7 Practical Small Hydro Resources in the Philippines.........................26

Table 2.8 Small Hydro Power Sites Verified by the DOE ..................................26

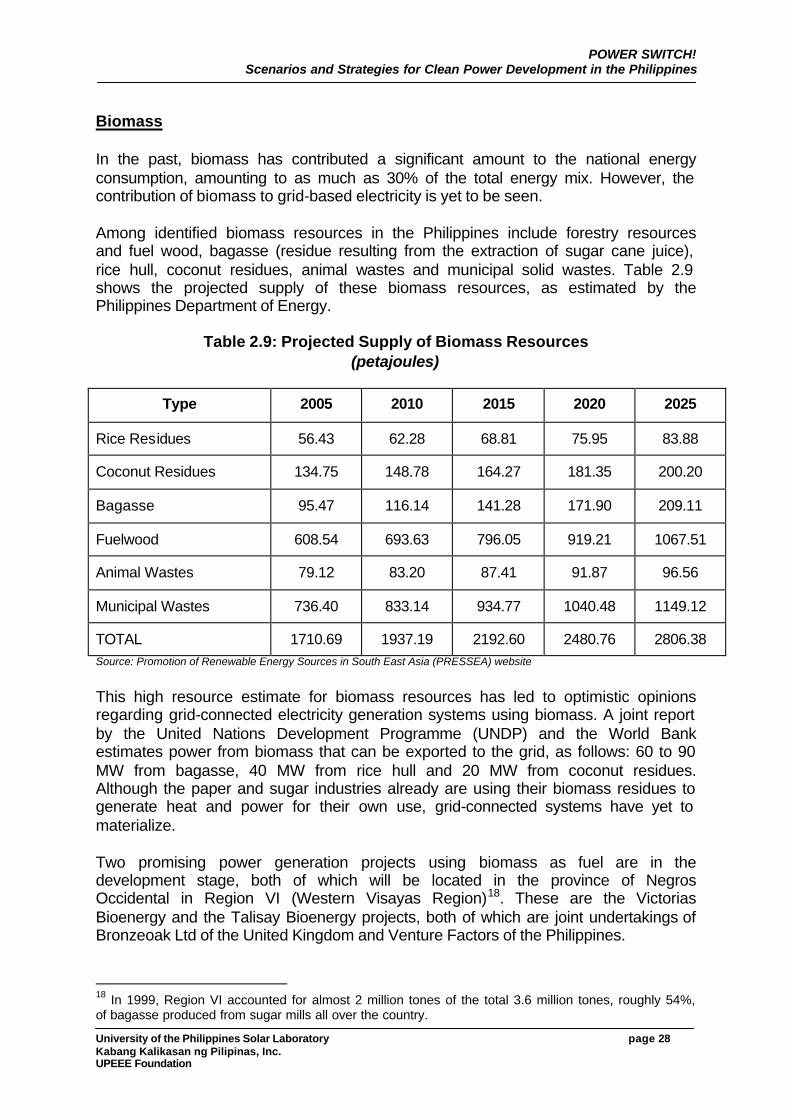

Table 2.9 Projected Supply of Biomass Resources ...........................................28

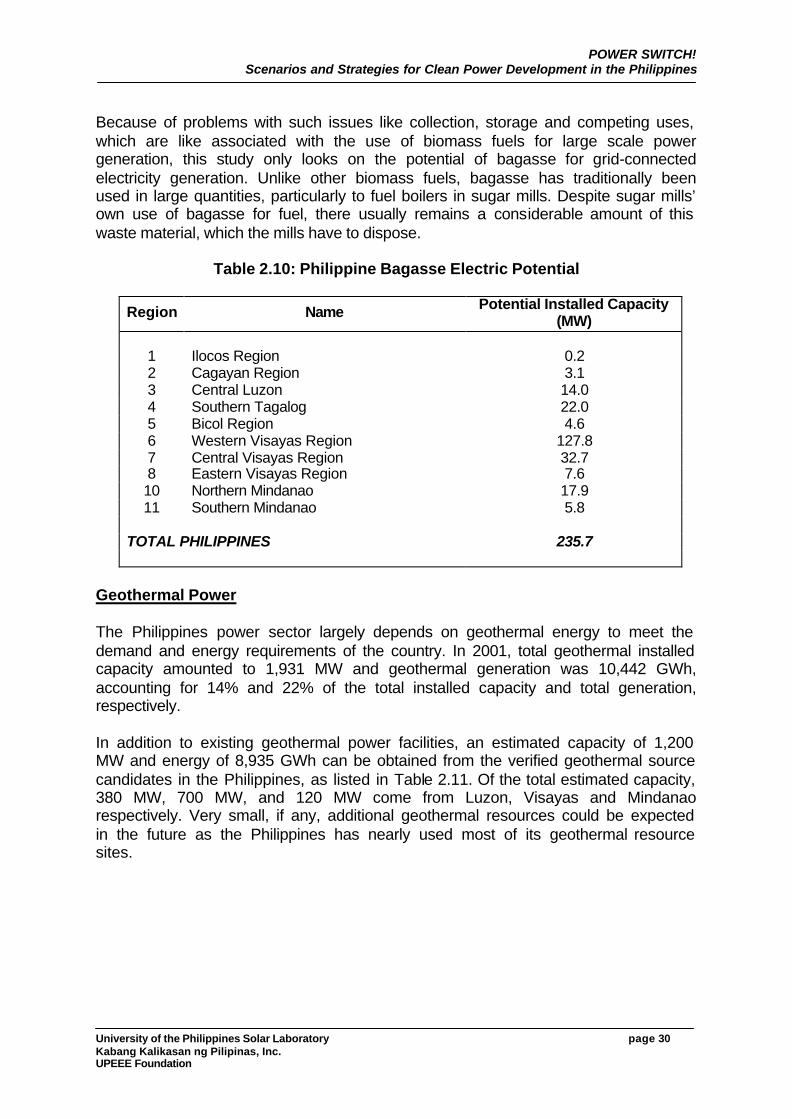

Table 2.10 Philippine Bagasse Electric Potential..................................................30

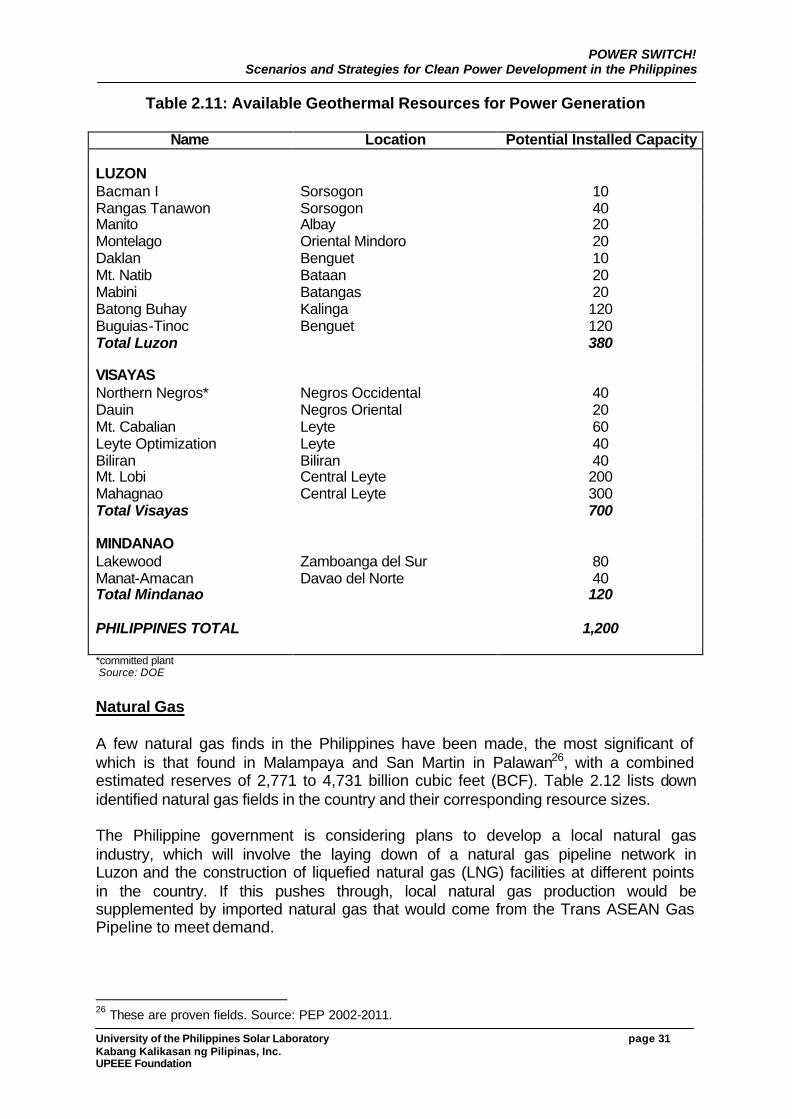

Table 2.11 Available Geothermal Resources for Power Generation.................31

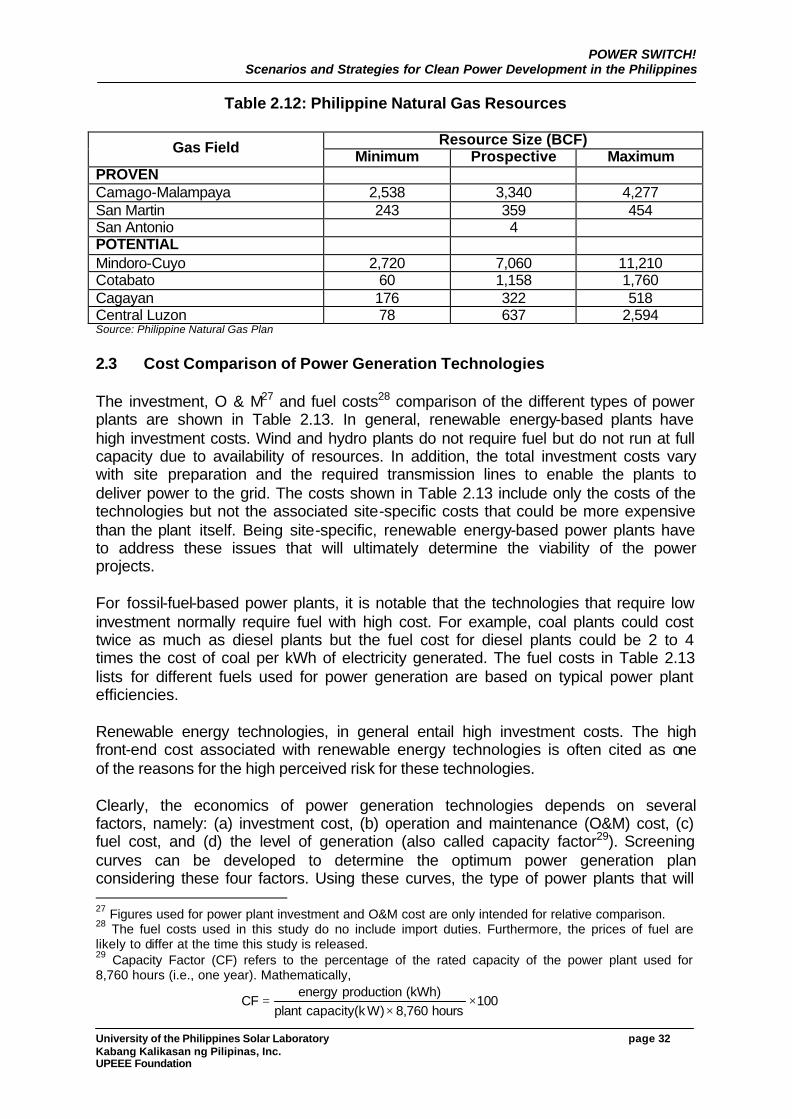

Table 2.12 Philippine Natural Gas Resources.......................................................32

Table 2.13 Cost Comparison of Power Plants.......................................................33

Table 2.14 Typical Capacity Factors of Power Plants

and Levelized Generation Costs..........................................................34

Table 2.15 Value of Air Emissions Reductions in California ...............................36

Table 2.16 Carbon Dioxide Emissions of Different Power Plant Types ............36

Table 2.17 Emission Factors for Various Power Plants .......................................36

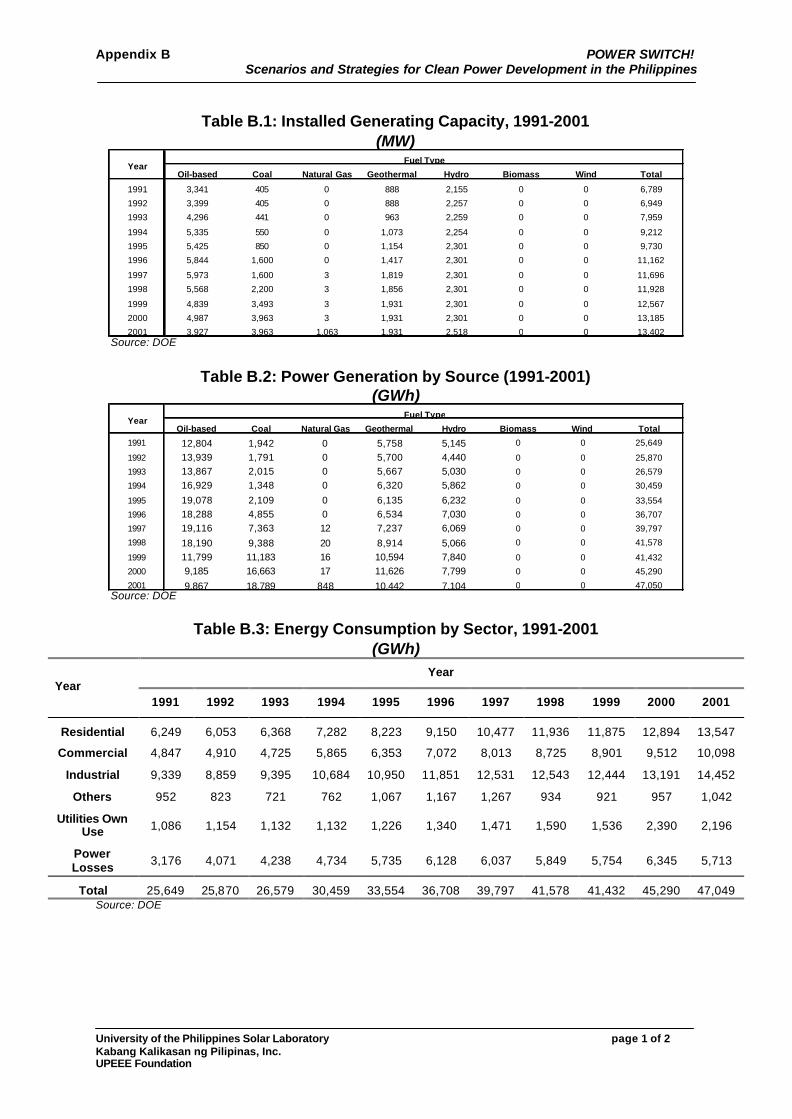

Table 3.1 Energy Consumption by Sector, 1991-2001 ......................................38

Table 3.2 Reserve Margin, 1991-2001 .................................................................42

Table 3.3 Historical Environmental Emissions for

the Philippine Power Sector .................................................................42

Table 3.4 NPC Average Electricity Rates, 1991-2001 .......................................46

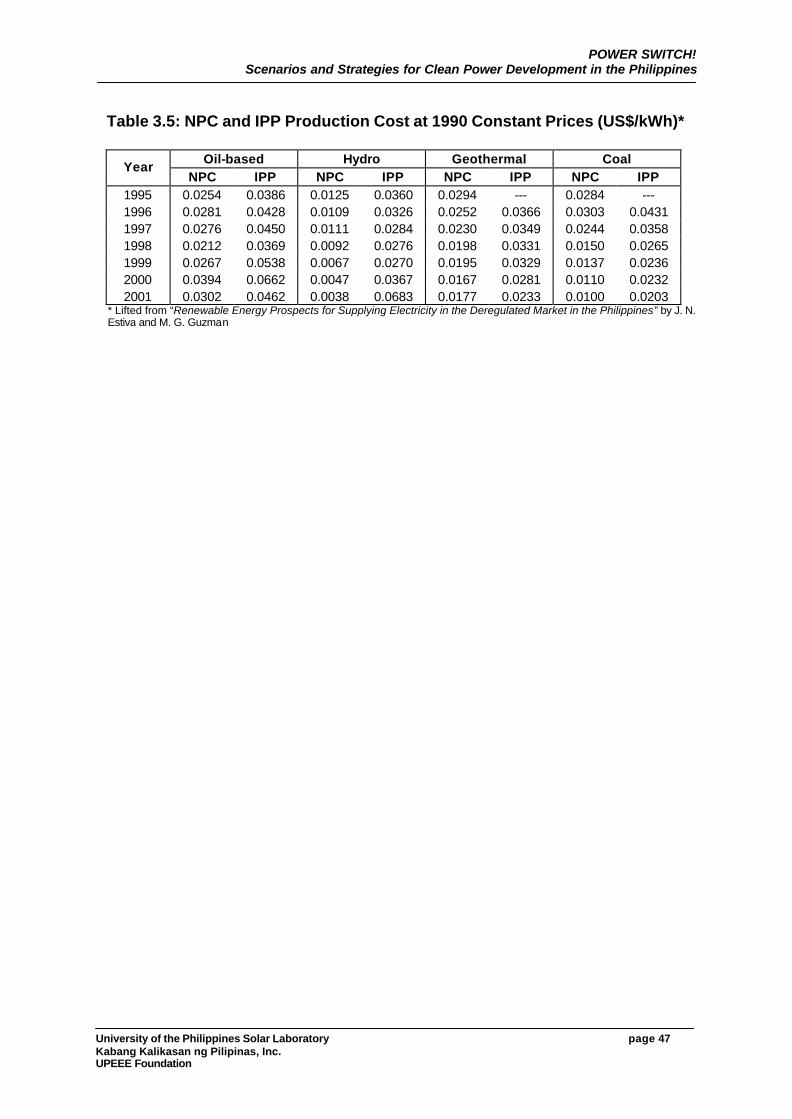

Table 3.5 NPC and IPP Production Cost at 1990 Constant Prices........................................................................................................47

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page vi Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Table 4.1 Low and High GDP Forecasts for 2003 to 2012 ...............................49

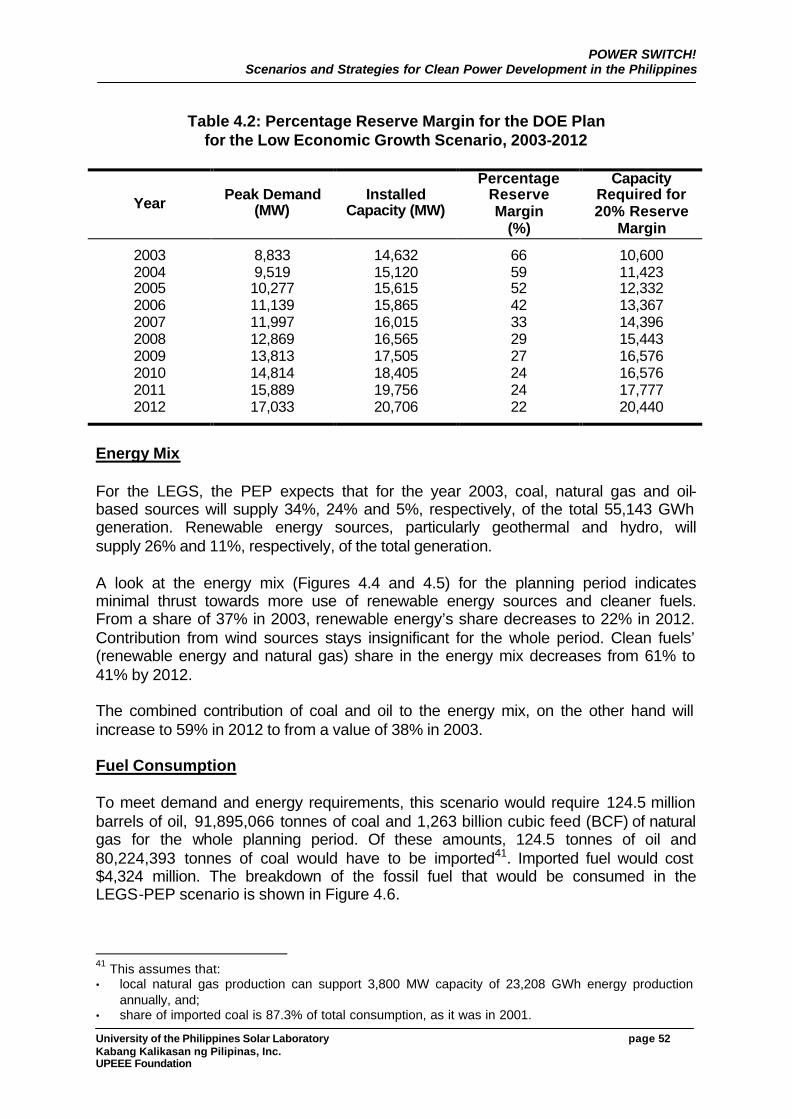

Table 4.2 Percentage Reserve Margin for the DOE Plan for the Low Economic Growth Scenario..........................................................52

Table 4.3 Environmental Emissions for the DOE Plan for the Low Economic Growth Scenario..........................................................55

Table 4.4 Generation Costs for the DOE Plan for the Low Economic Growth Scenario, 2003-2012.............................................56

Table 4.5 Percentage Reserve Margin for the DOE Plan for the High Economic Growth Scenario.........................................................58

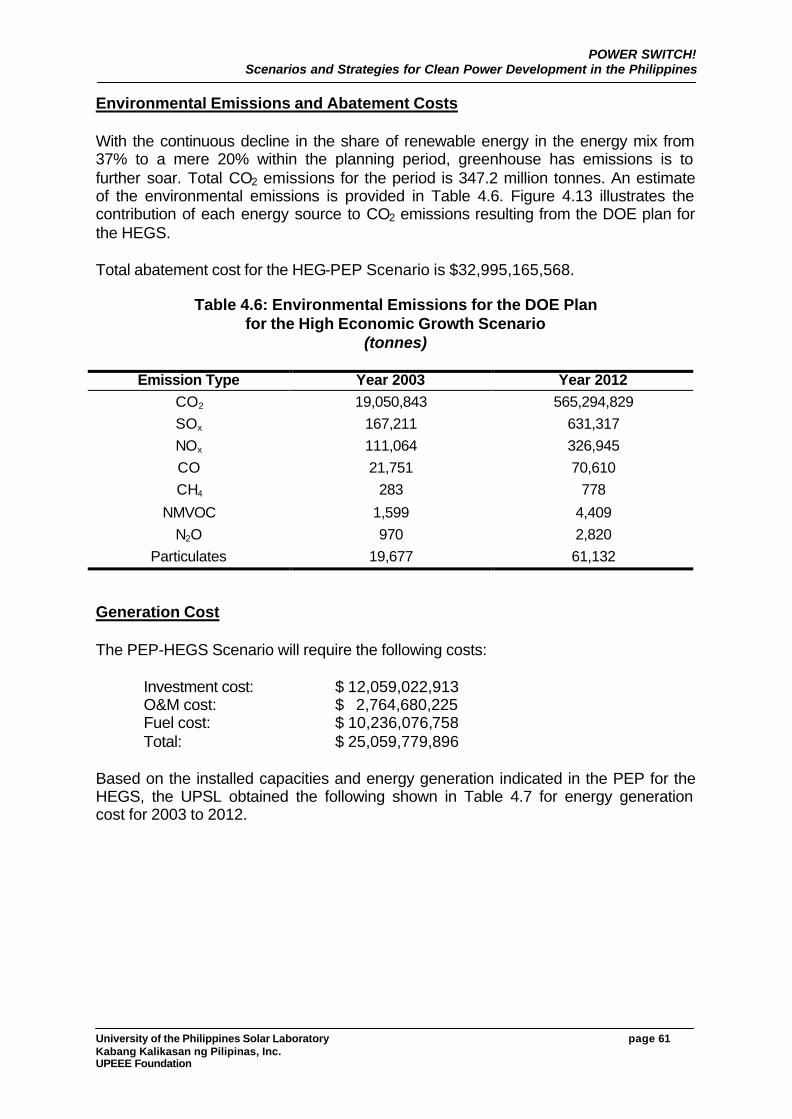

Table 4.6 Environmental Emissions for the DOE Plan for the High Economic Growth Scenario.........................................................61

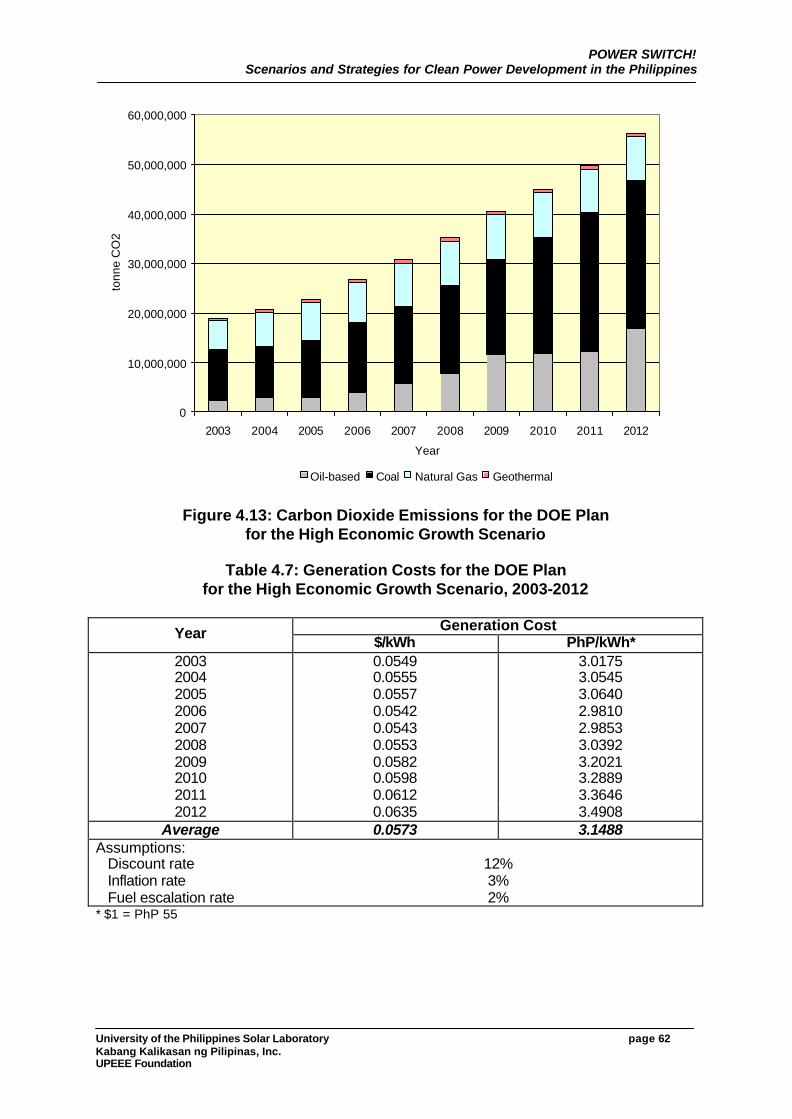

Table 4.7 Generation Costs for the DOE Plan for the High Economic Growth Scenario ..................................................................62

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page vii Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

LIST OF APPENDICES

Appendix A Wind and Hydro Potential in the Philippines

Appendix B Historical Performance of the Philippine Power Sector

1991-2001

Appendix C Economic Scenarios and DOE Plans for the Power Sector 2003-

2012

Appendix D Clean Power Development Options

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page viii Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

LIST OF ABBREVIATIONS

AWPP Aggressive Wind Power Penetration

BCF billion cubic feet

Btu British thermal unit

CC combined cycle power plant

CENECO Central Negros Electric Cooperative

CER Certificate of Emissions Reduction

CH4 methane

CO carbon monoxide

CO2 carbon dioxide

FFHC First Farmers Holdings Corporation

GHG greenhouse gas

GWh gigawatthour

HAEGS Historical Average Economic Growth Scenario

HEGS High Economic Growth Scenario

IPPs Independent Power Producers

ktonne kilotonne

kW kilowatt

LEGS Low Economic Growth Scenario

LOLP loss of load probability

MERALCO Manila Electric Company

MMBFOE million barrels of fuel oil equivalent

MWPP Moderate Wind Power Penetration

NMVOC non-methane volatile organic compound

NOx nitrogen oxides

NPC National Power Corporation

NREL National Renewable Energy Laboratory

N2O nitrous oxide

PPA purchased power adjustment

POWER SWITCH: Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page ix Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

SO2 sulfur dioxide

UNDP United Nations Development Programme

UPSL University of the Philippines Solar Laboratory

VMC Victorias Milling Company

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 1 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

1 EXECUTIVE SUMMARY 1.1 Introduction An area that has great potential for greenhouse gas (GHG) reduction is the power sector. In 1994, the energy sector accounted for 50.038 million tonnes of the 100.738 million tonnes, or roughly 47 percent, of total net GHG emissions in the country. Of the energy sector GHG emissions, the energy industries, mainly the power industry, accounts for more than thirty (30) percent as a result of the burning of fossil fuels. Although it ranks only second to the transport sub-sector in terms of GHG emissions, the power sub-sector represents a large opportunity for carbon emissions reduction and sequestration, given that clean energy technologies and resources are available. This study focuses on reliability, cost and environmental performance (particularly GHG emissions) of the power sector. In particular it looks into scenarios that would entail switching to clean energy technologies from conventional fossil fuel-based technologies for grid-connected power generation. 1.2 Technology and Resource Assessment for Clean Power Development This study has assessed the technologies and resources that could be used to pursue clean power development in the Philippines. Clean Energy Technologies For the clean energy technologies, the assessment focused on technology measures that reduce carbon intensity of energy (e.g., renewable energy technologies and cleaner fossil-based technologies such as natural gas). Despite the high potential of technology measures that reduce energy intensity, which could be treated as a resource in energy planning, it is not used in this study because data available in the Philippines is insufficient to do so. The following are the clean energy technologies that could be utilized for clean power development in the Philippines:

a) Wind Energy Conversion Systems;

b) Hydroelectric Power Plants;

c) Biomass Energy Conversion Systems;

d) Geothermal Power Plants; and

e) Natural Gas-Fired Power Plants. Improved coal technologies, such as the circulating fluidized bed combustion system, is considered as “relatively cleaner” only to pulverized coal plant technology. Hence, if considered in power development with the objective of pursuing environmental sustainability, these technologies will be at the bottom of the list. Other renewable energy technologies were excluded on the basis of cost competitiveness and/or maturity of technology.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 2 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

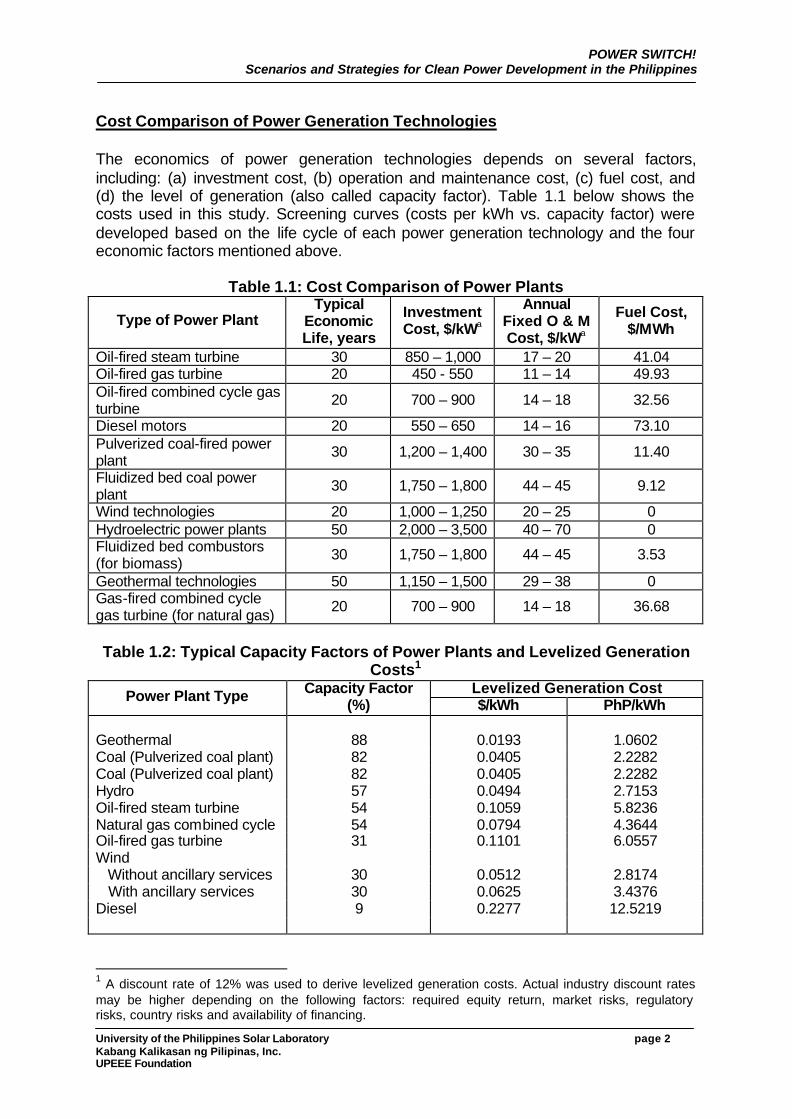

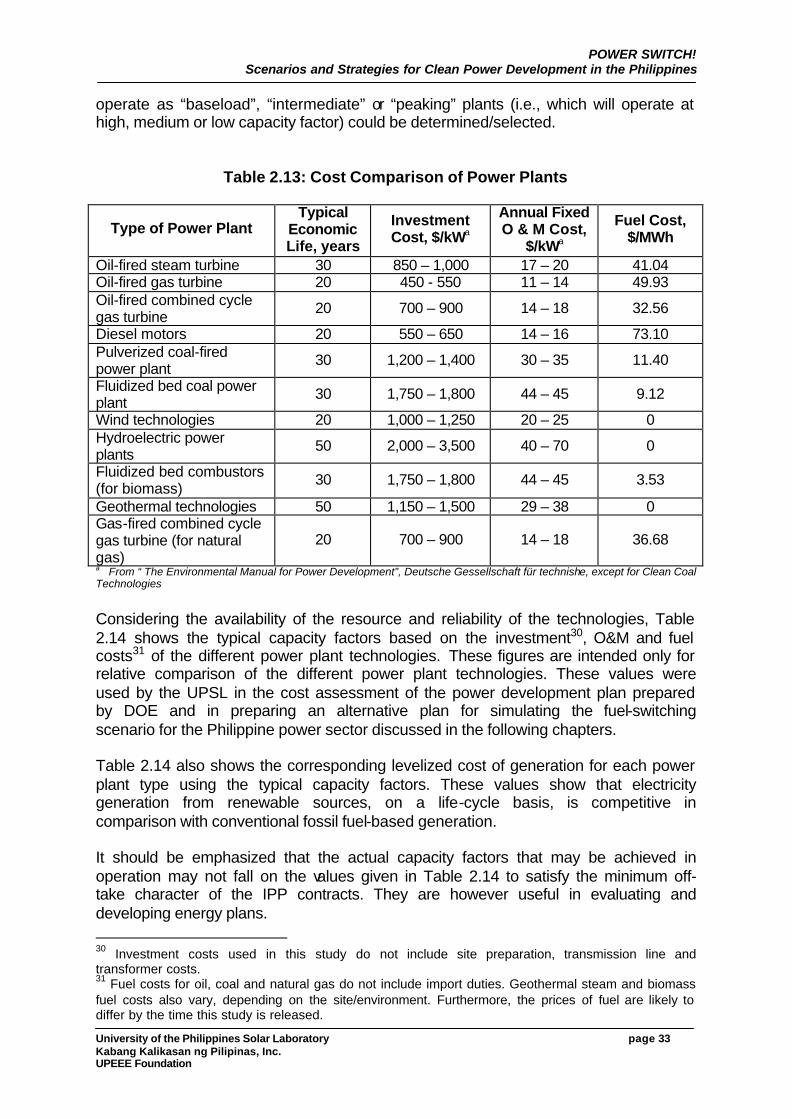

Cost Comparison of Power Generation Technologies The economics of power generation technologies depends on several factors, including: (a) investment cost, (b) operation and maintenance cost, (c) fuel cost, and (d) the level of generation (also called capacity factor). Table 1.1 below shows the costs used in this study. Screening curves (costs per kWh vs. capacity factor) were developed based on the life cycle of each power generation technology and the four economic factors mentioned above.

Table 1.1: Cost Comparison of Power Plants

Type of Power Plant Typical

Economic Life, years

Investment Cost, $/kWa

Annual Fixed O & M Cost, $/kWa

Fuel Cost, $/MWh

Oil-fired steam turbine 30 850 – 1,000 17 – 20 41.04 Oil-fired gas turbine 20 450 - 550 11 – 14 49.93 Oil-fired combined cycle gas turbine 20 700 – 900 14 – 18 32.56

Diesel motors 20 550 – 650 14 – 16 73.10 Pulverized coal-fired power plant 30 1,200 – 1,400 30 – 35 11.40

Fluidized bed coal power plant 30 1,750 – 1,800 44 – 45 9.12

Wind technologies 20 1,000 – 1,250 20 – 25 0 Hydroelectric power plants 50 2,000 – 3,500 40 – 70 0 Fluidized bed combustors (for biomass) 30 1,750 – 1,800 44 – 45 3.53

Geothermal technologies 50 1,150 – 1,500 29 – 38 0 Gas-fired combined cycle gas turbine (for natural gas) 20 700 – 900 14 – 18 36.68

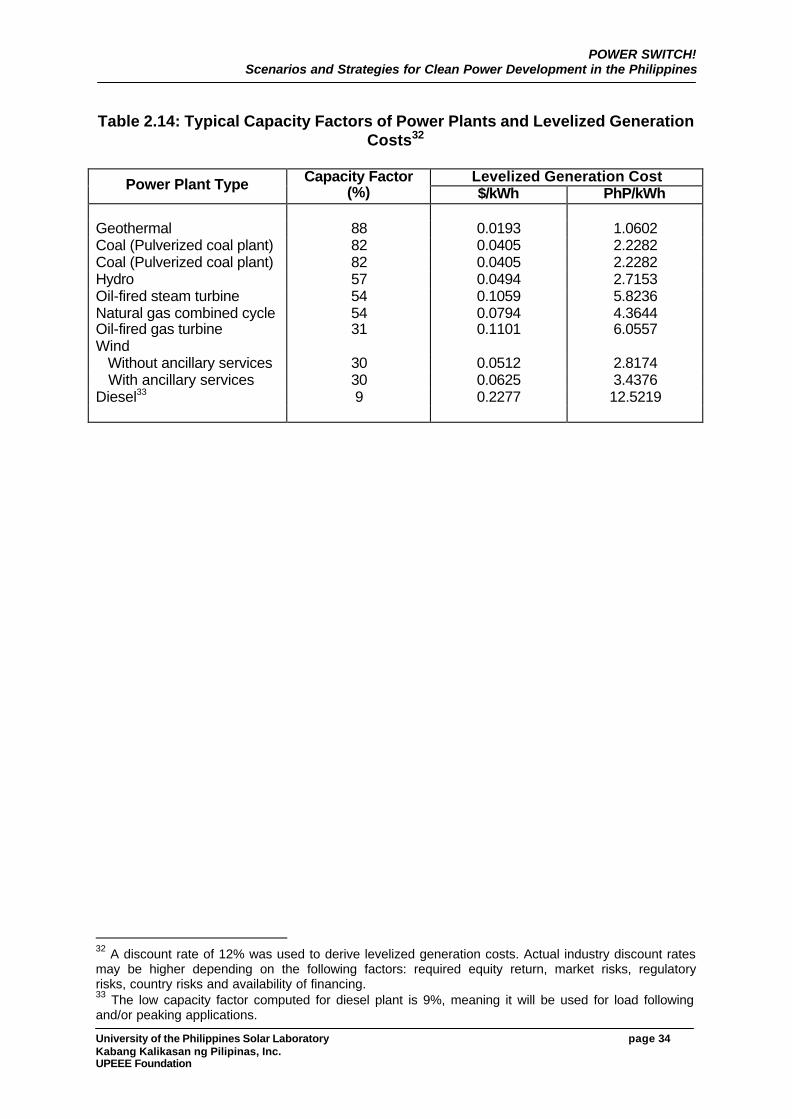

Table 1.2: Typical Capacity Factors of Power Plants and Levelized Generation

Costs1 Levelized Generation Cost Power Plant Type Capacity Factor

(%) $/kWh PhP/kWh Geothermal 88 0.0193 1.0602 Coal (Pulverized coal plant) 82 0.0405 2.2282 Coal (Pulverized coal plant) 82 0.0405 2.2282 Hydro 57 0.0494 2.7153 Oil-fired steam turbine 54 0.1059 5.8236 Natural gas combined cycle 54 0.0794 4.3644 Oil-fired gas turbine 31 0.1101 6.0557 Wind Without ancillary services 30 0.0512 2.8174 With ancillary services 30 0.0625 3.4376 Diesel 9 0.2277 12.5219 1 A discount rate of 12% was used to derive levelized generation costs. Actual industry discount rates may be higher depending on the following factors: required equity return, market risks, regulatory risks, country risks and availability of financing.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 3 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

The above screening curve table was used in preparing the alternative power development plans in this study. The figures used are only intended for relative comparison.2 It can be noted that on life-cycle basis, renewable energy technologies can be competitive with conventional fossil fuel-based technologies. However, most power developers are biased to fossil-based power plants because of its comparative advantage in terms of investment cost and shorter recovery period. Thus, the need for policy instruments and mechanisms that will create a more secured investment climate for renewable energy developers cannot be over-emphasized. Environmental Externalities A number of studies have attempted to put a cost on the various externalities caused by power generation using the abatement cost or the damage cost approach. The abatement cost approach uses the cost of pollution control as a proxy to the true externality cost. On the other hand, the damage cost approach puts a value on the damages that may be directly attributable to a particular pollutant. Studies vary in their estimation of externality costs because of a number of factors, including site specificity (e.g., geographical and climatological conditions), population density, emissions reduction policy, scope of analysis, among others. In this study, abatement cost values for the North Coast of California, which has the lowest abatement costs among the districts of California, were used to compute for the cost of externalities of the different power development plans. These figures were used in the absence of actual abatement cost assessment for the Philippines. Moreover, abatement technologies, if required in the Philippines’ power generation sector, will be imported from developed countries such as U.S.A or Europe. It is therefore deemed reasonable to use the lowest available value in developed countries for purposes of evaluating the prospective performance of a power development plan. It can be concluded that if environmental externalities will be considered, clean renewable energy technologies will be the least cost option for power development in the Philippines Clean Indigenous Energy Resources Energy resource assessment was conducted based on secondary data to quantify the available indigenous resources that can be utilized by the clean energy technologies as “fuel”. Assessment was made for wind, hydro, biomass, geothermal and natural gas resources for power development. Resource assessment and mapping conducted in the past for the Philippine archipelago have shown that the country has a big wind power potential. The National Renewable Energy Laboratory (NREL) has estimated that there are 76,600 MW of installed wind power capacity in the Philippines that can generate about 2 True costs will vary for a number of reasons, including variability of fuel costs, dollar discount rates, among other things. Further, these costs do not include site development costs, connection to the transmission system, transformer costs and taxes. These costs were derived using only the cost of the power plant technology, operations and maintenance cost and fuel costs.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 4 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

195,200 GWh of electricity per year. For the purposes of this study, a re-analysis of the NREL wind mapping data was conducted. Additional screening criteria were imposed to determine practical and viable wind power sites. This include considering only sites with power density of at least 500 W/m2. This first criterion reduced the number of wind sites to 2,092 with an aggregate potential of 14,323 MW. A second criterion that relates to grid connection costs was also used. The transmission system of the National Transmission Company (TransCo) was overlaid to the GIS-based wind resource map to determine the proximity of the sites to the grid. Only those sites whose connection (i.e., construction of transmission lines) will cost up to 25% of the total life-cycle cost were considered. The application of the second criterion further reduced the number of sites to 1,038 with 7,404 MW potential. A re-analysis of the NREL small hydro resource assessment was also conducted. Selecting only the sites with capacities of 5 MW or more as criterion, the UPSL identified 236 small hydro sites in the country with an aggregated capacity of about 2,308 MW. Using the second screening criterion similar to that use in the wind resource assessment, (i.e., limiting the transmission investment cost to 25% of total investment cost) resulted to the elimination of three sites from the small hydro resource pool. Of all the biomass resources in the country, UPSL considered only bagasse from sugarcane processing as practical resource for grid connection. Other biomass resources are still facing problems or issues like collection, storage, and competing uses to be viable for large-scale power generation. UPSL estimates the electric power potential of bagasse at 235.7 MW. This potential is spread all over the country where sugar centrals are situated. The Philippines power sector largely depends on geothermal energy to meet the demand and energy requirements of the country. In 2001, total geothermal installed capacity amounted to 1,931 MW, which generated a total of 10,442 GWh. This accounts for 14% and 22% of the total installed capacity and total generation, respectively in the country. In addition to existing geothermal power facilities, an estimated capacity of 1,200 MW that could generate about 8,935 GWh annually can be obtained from additional verified geothermal sites in the Philippines. A few natural gas finds in the Philippines have been made, the most significant of which is that found in Malampaya and San Martin in Palawan, with a combined estimated reserves of 2,771 to 4,731 billion cubic feet (BCF). The Philippine government is considering plans to develop a local natural gas industry. If this pushes through, local natural gas production would be supplemented by imported natural gas. 1.3 Historical Performance of the Philippine Power Sector The performance (in terms of reliability, cost and environmental emissions,) of the Philippine power sector from the period beginning 1991 to 2001 was also assessed in this study.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 5 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

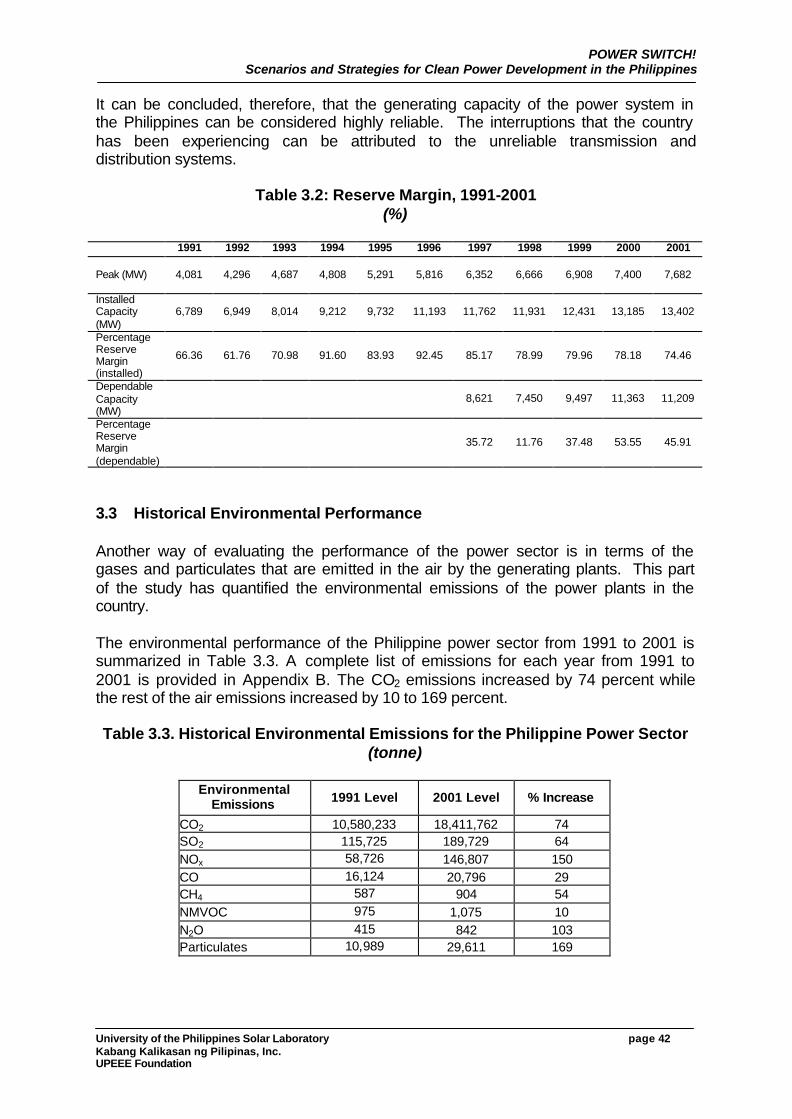

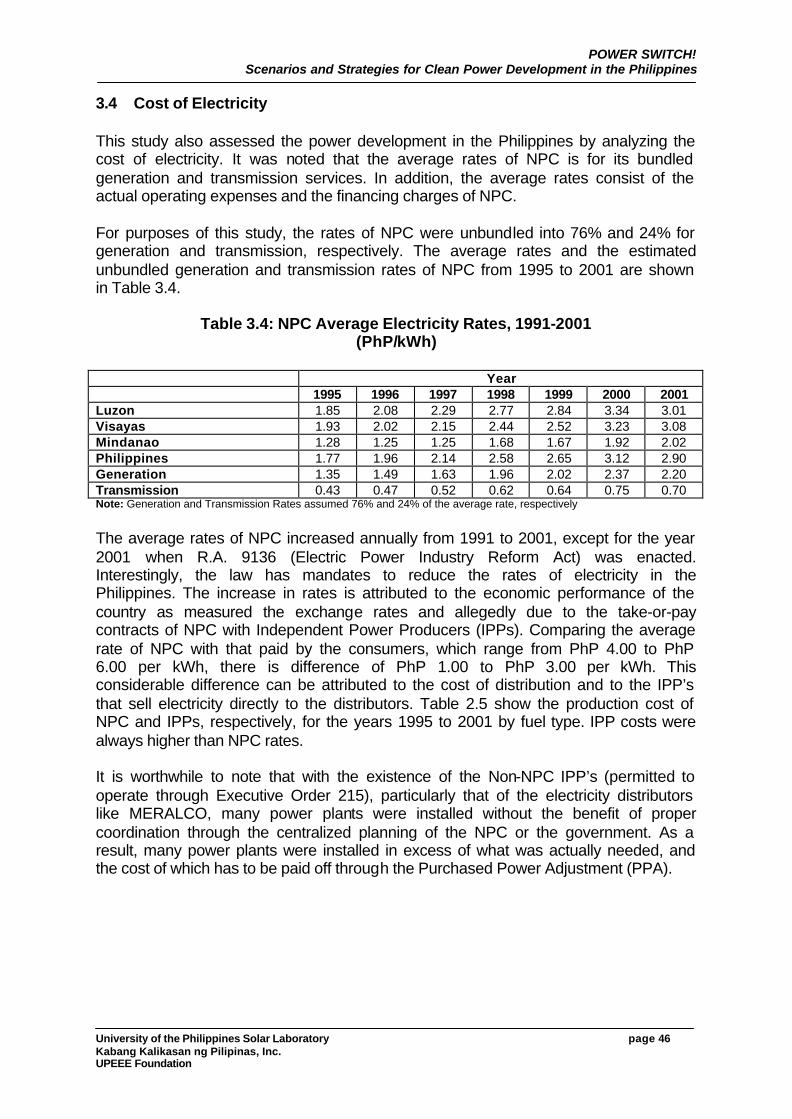

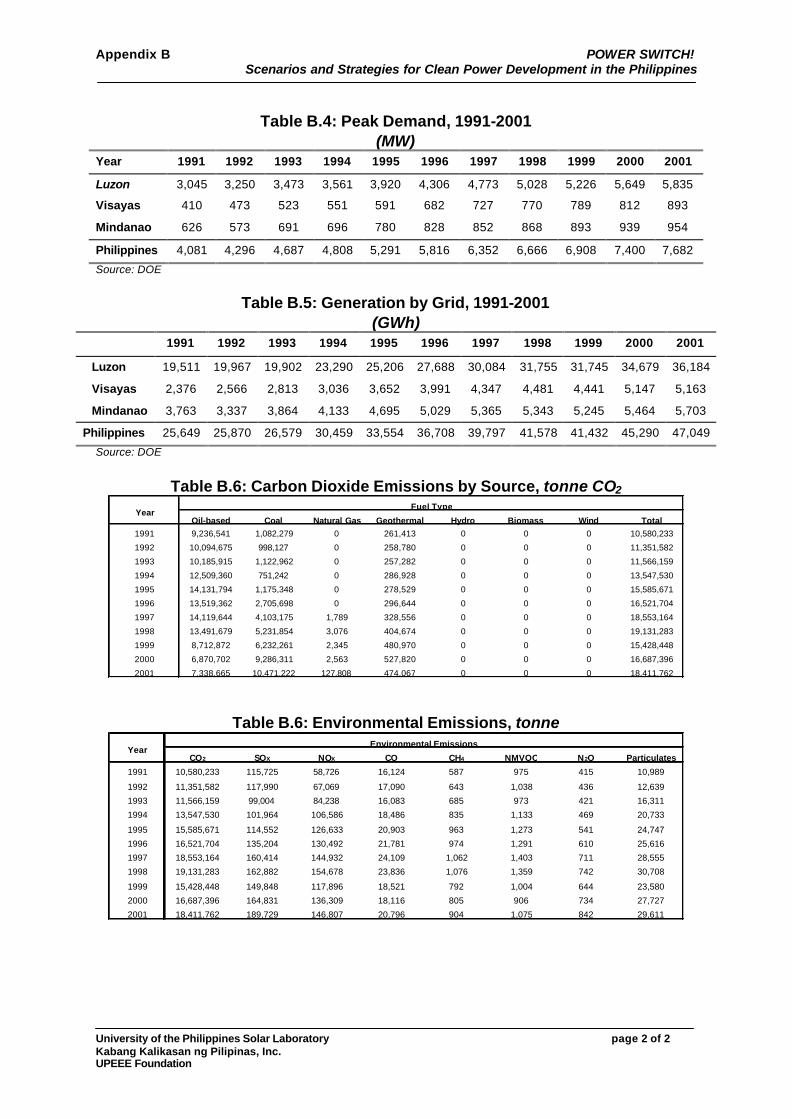

Energy Demand and Installed Capacity The Philippines electricity consumption posted a moderate growth rate of 8.3% annually from 1991 to 2001. The industrial and residential sectors, accounting for 31% and 29% energy share for the year 2001, respectively, are the biggest users of electricity. The commercial sector accounts for 21% of the total consumption for 2001. The rest are attributed to own use, losses and miscellaneous uses. It should be noted however, that the industrial sector demand grew only by 5.5% while that of the residential sector grew by 11.7% annually for the 11-year period. Geographically, the energy demand in the country was distributed among the three (3) main islands of Luzon, Visayas and Mindanao. Bulk of the energy demand and consequently the generation comes from the main island of Luzon. In 2001 for example, the Luzon Grid has a share of 36,184 GWh of the total 47,049 GWh energy generation which represents 77% of the requirements of the country. Visayas and Mindanao share the remaining balance almost equally. In order to meet the growing demand for electricity, the installed generating capacity in the country doubled in 11 years with 6,789 MW in 1991 to 13,402 MW in 2001. Historical Reliability Performance To analyze the reliability performance of the power system in the Philippines, the reserve margin (i.e., generating capacity compared to the system peak) from 1991 to 2001 was determined from historical data. The analysis has shown that the generating facilities in the early 1990’s were performing very badly from the point of view of reliability. However, from mid 1990’s onward, the Philippines power sector performance went to the other extreme of having excessive capacity compared to the demand. This validates the clamor of the people regarding high electricity rates which is due to oversupply since most of the generating facilities are operating under the take-or-pay contract with the National Power Corporation (NPC) and other distribution utilities. It can be concluded, therefore, that the generating capacity of the power system in the Philippines can be considered highly reliable. The interruptions that the country has been experiencing can be attributed to the unreliable transmission and distribution systems and their operations. Historical Cost Performance This study also assessed the power development in the Philippines by analyzing the cost of electricity. It was noted that the rates of NPC is for its bundled generation and transmission services. For purposes of this study, these rates were unbundled into 76% and 24% for generation and transmission, respectively. The rates of NPC appear to be increasing annually except for the year 2001 when R.A. 9136 (Electric Power Industry Reform Act) was enacted and the national government has intervened in the market due to the growing clamor against the Purchase Power Adjustments (PPA) in the electric bills. The increase in rates is attributed to the economic performance of the country (as exhibited by the exchange rates) and due to the take-or-pay contracts of NPC with Independent Power Producers (IPPs).

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 6 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Records also show that the production cost of IPPs were always higher than the NPC rates. This contradict the avoided cost principle of the NPC IPP Program that IPP power development project proposals will be accepted as it offer electricity at prices lower than or at least equal to NPC rates. Comparing the average rate of NPC with that paid by the consumers, which range from PhP 4.00 to PhP 6.00 per kWh, there is difference of PhP 1.00 to PhP 3.00 per kWh. This considerable difference can be attributed to the cost of distribution and to the PPA of IPP’s that sell electricity directly to the distributors. It is also worthwhile to note that with the existence of the Non-NPC IPPs (permitted to operate through Executive Order 215), particularly those owned by electricity distributors like Manila Electric Company (MERALCO), many power plants were installed even though there were already excess generation capacity in the system. The main culprit here is that the IPPs’ return on investments were guaranteed by the take-or-pay contracts with NPC and the distribution utilities. This indicates the poor coordination of the plans of the IPPs that deal directly with Distributors in the context of centralized planning of the government, particularly the NPC. Historical Environmental Performance The environmental performance of the Philippine power sector from 1991 to 2001 (measured in terms of the amount of gases and particulates that are emitted by the electric power generating plants) shows that CO2 emissions increased by 74 percent while the rest of the air emissions increased by 10 to 169 percent.

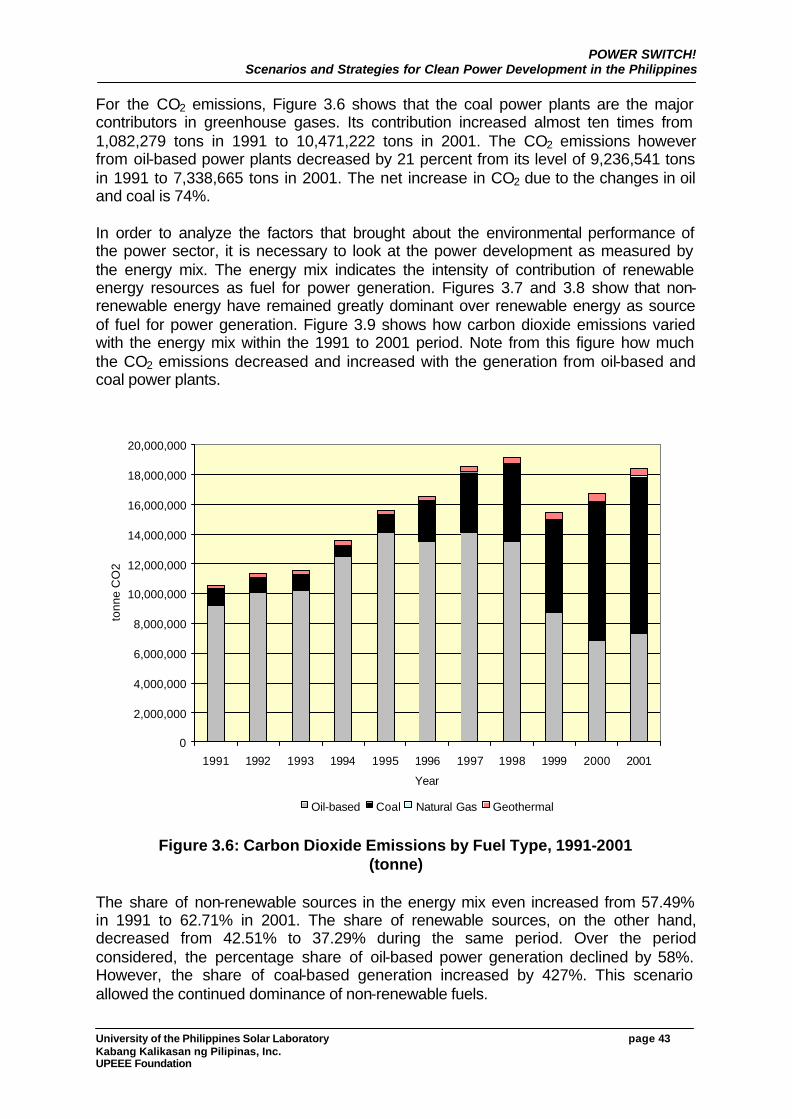

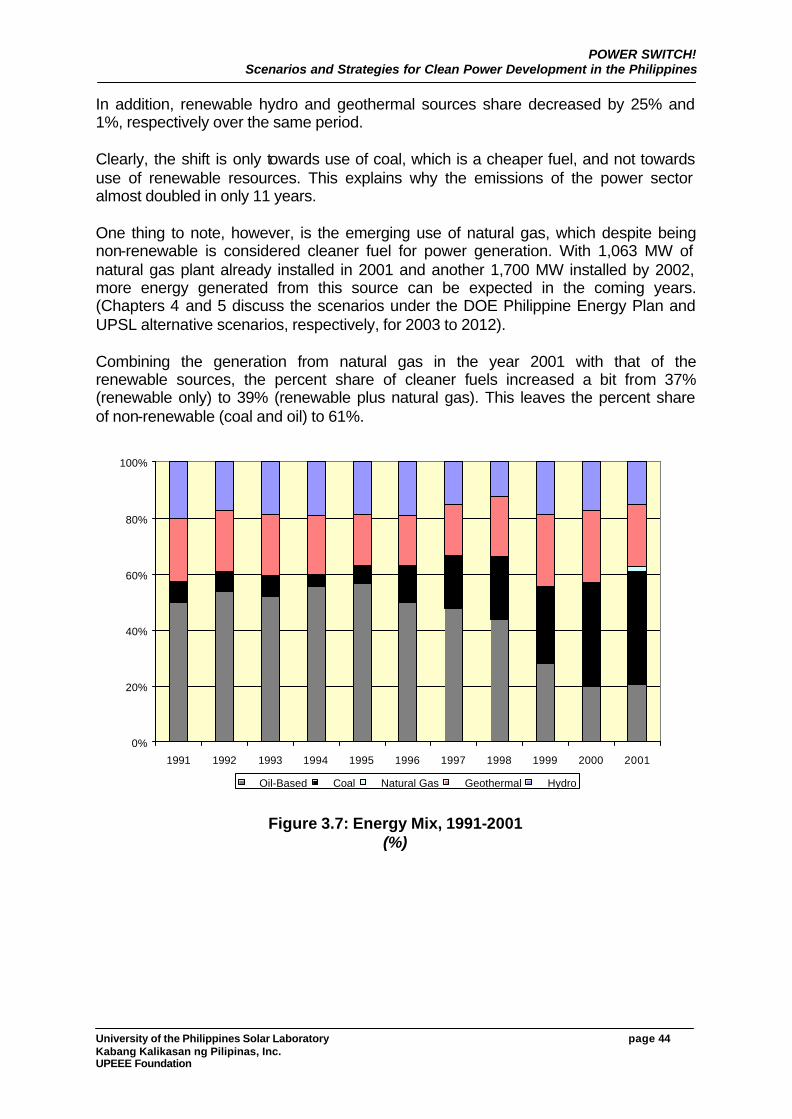

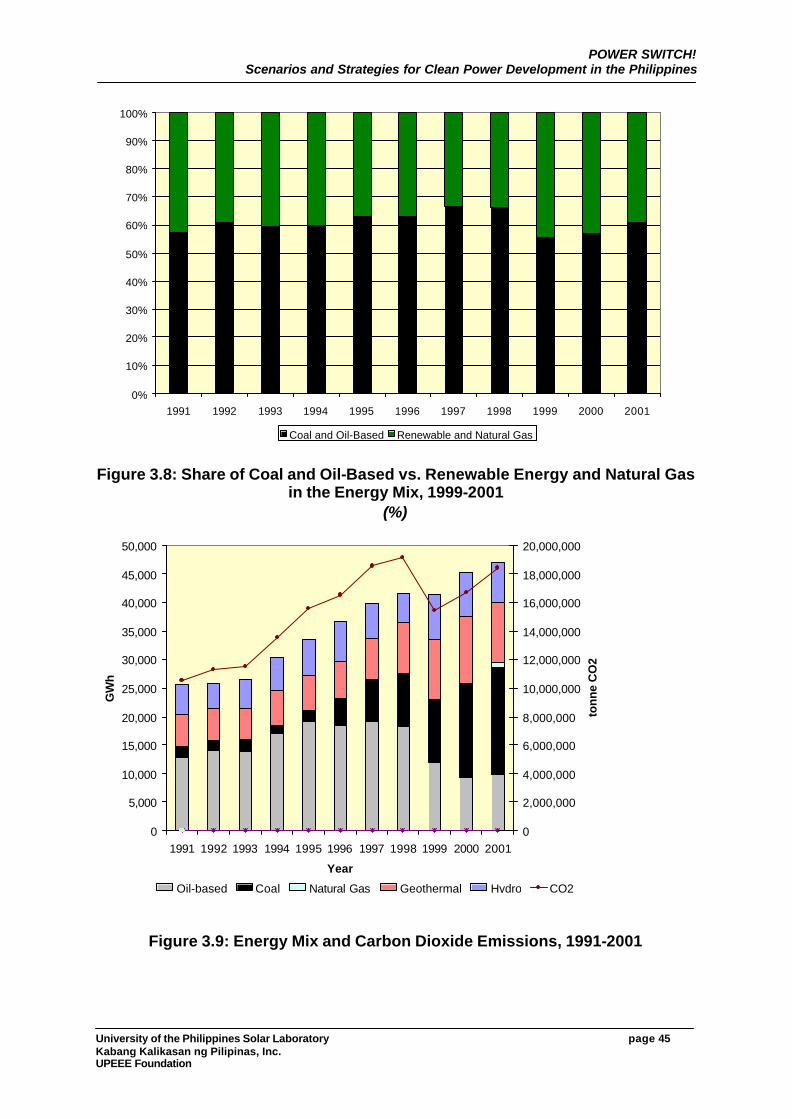

For the CO2 emissions, coal power plants are the major contributors. Its contribution increased almost ten times from 1,082,279 tons in 1991 to 10,471,222 tons in 2001. CO2 emissions from oil-based power plants, on the other hand, decreased by 21 percent from its level of 9,236,541 tons in 1991 to 7,338,665 tons in 2001. Accounting the changes in oil and coal, the net increase in CO2 for the 11-year period is 73%. Looking into the energy mix to link the environmental performance of the power sector, it can be concluded that that non-renewable energy have remained greatly dominant over renewable energy as source of fuel for power generation. The share of non-renewable sources in the energy mix even increased from 57.49% in 1991 to 62.71% in 2001. Over the period considered, generation share from oil-based power plants declined from 49.9% in 1991 to 21.9% in 2001. However, coal contribution increased more than fivefold, from 8% in 1991 to 40% in 2001. In addition, renewable hydro share decreased from 20% to 5% over the same period. This scenario allowed the continued dominance of non-renewable fuels. Clearly, the shift is only towards the use of coal, which emits more greenhouse gases, and not towards the utilization of renewable resources. This explains why the emissions of the power sector almost doubled in only 11 years.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 7 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

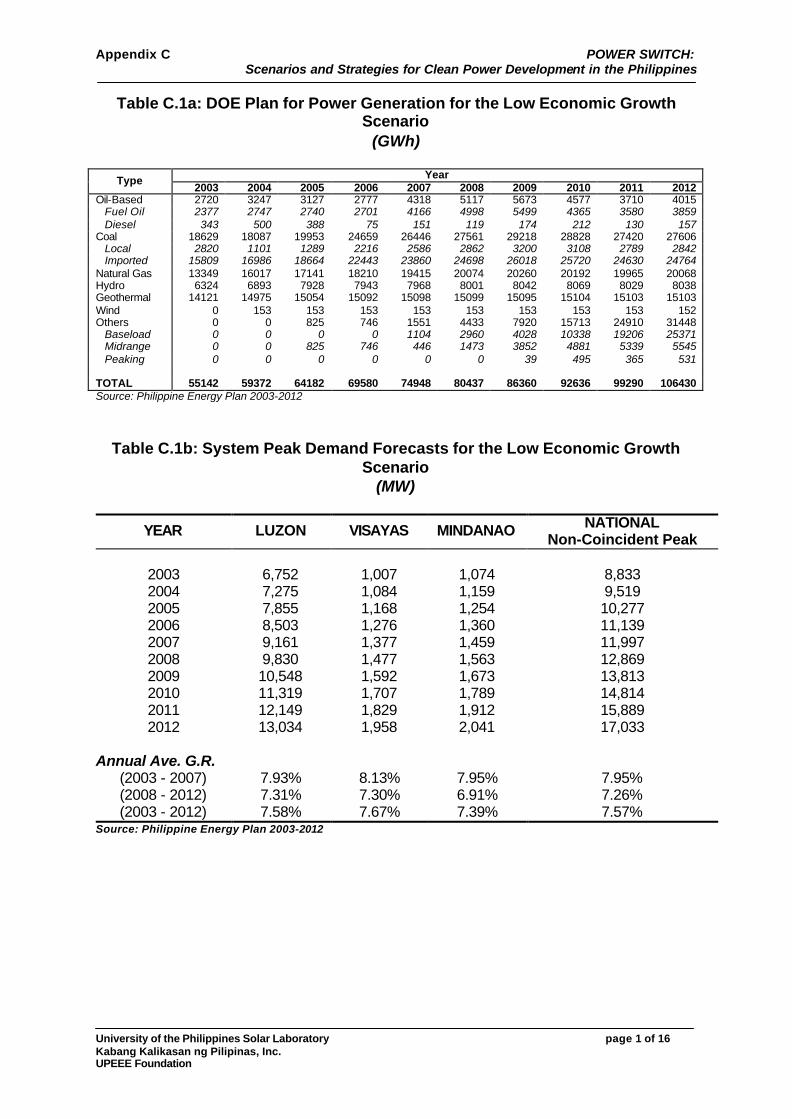

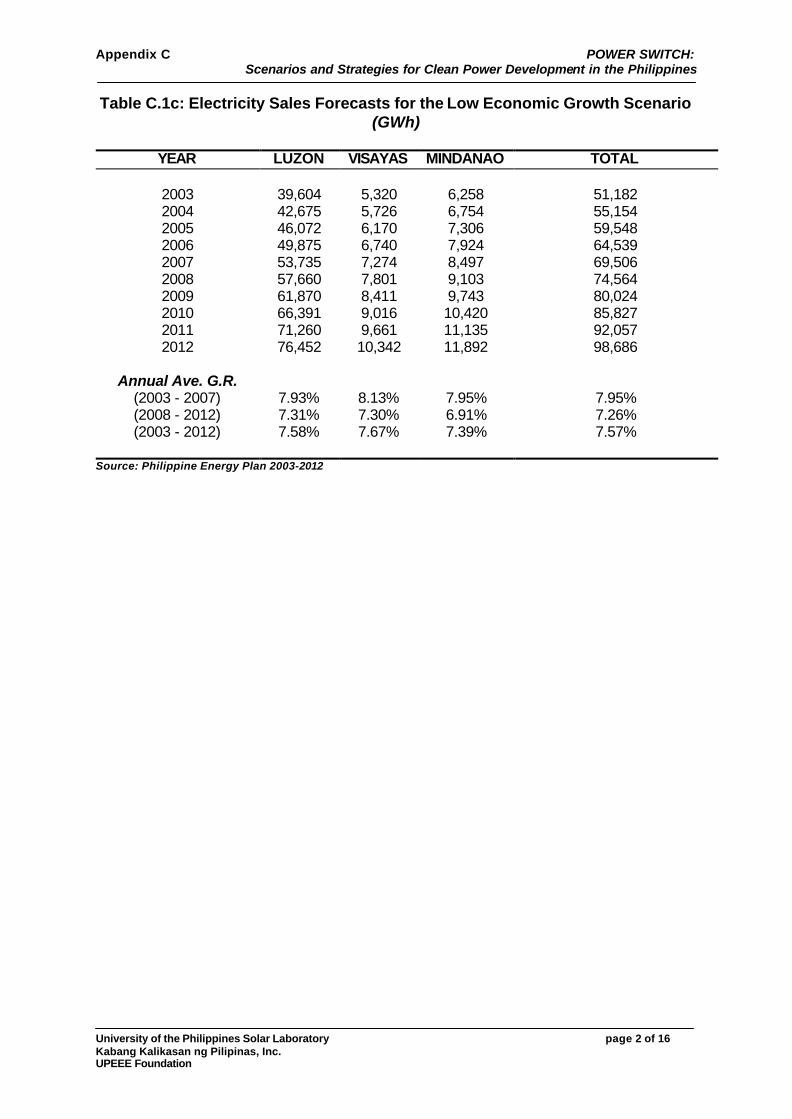

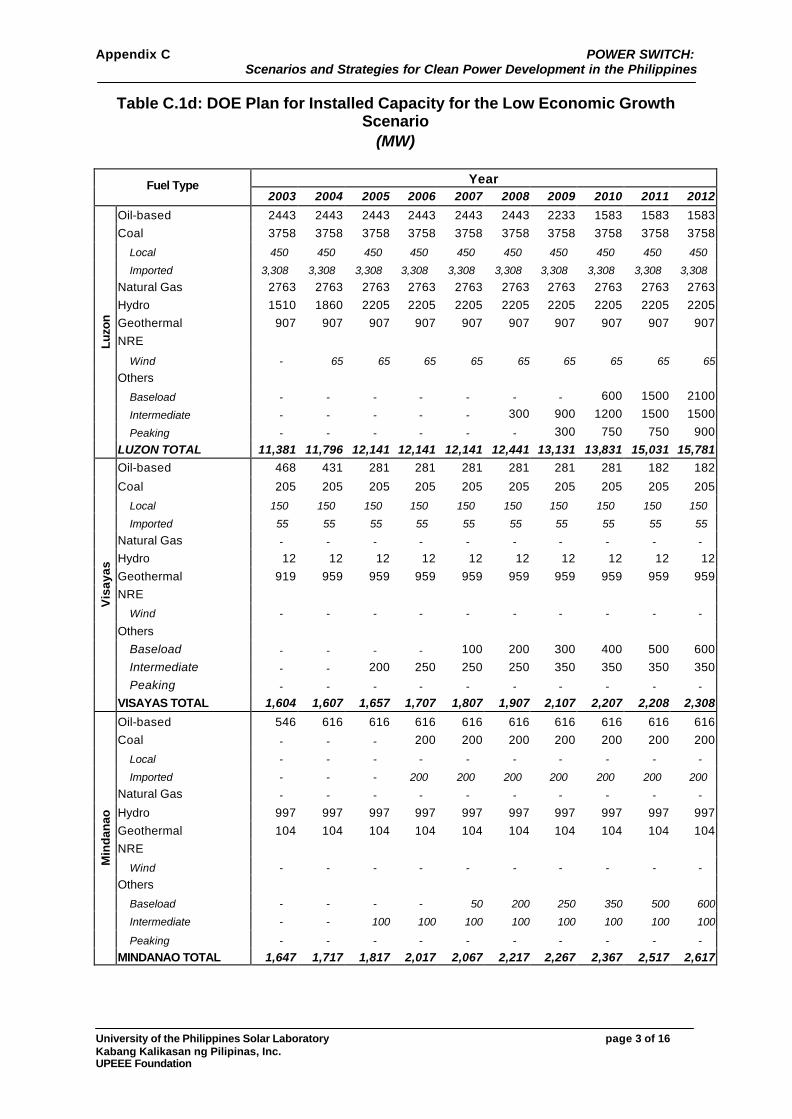

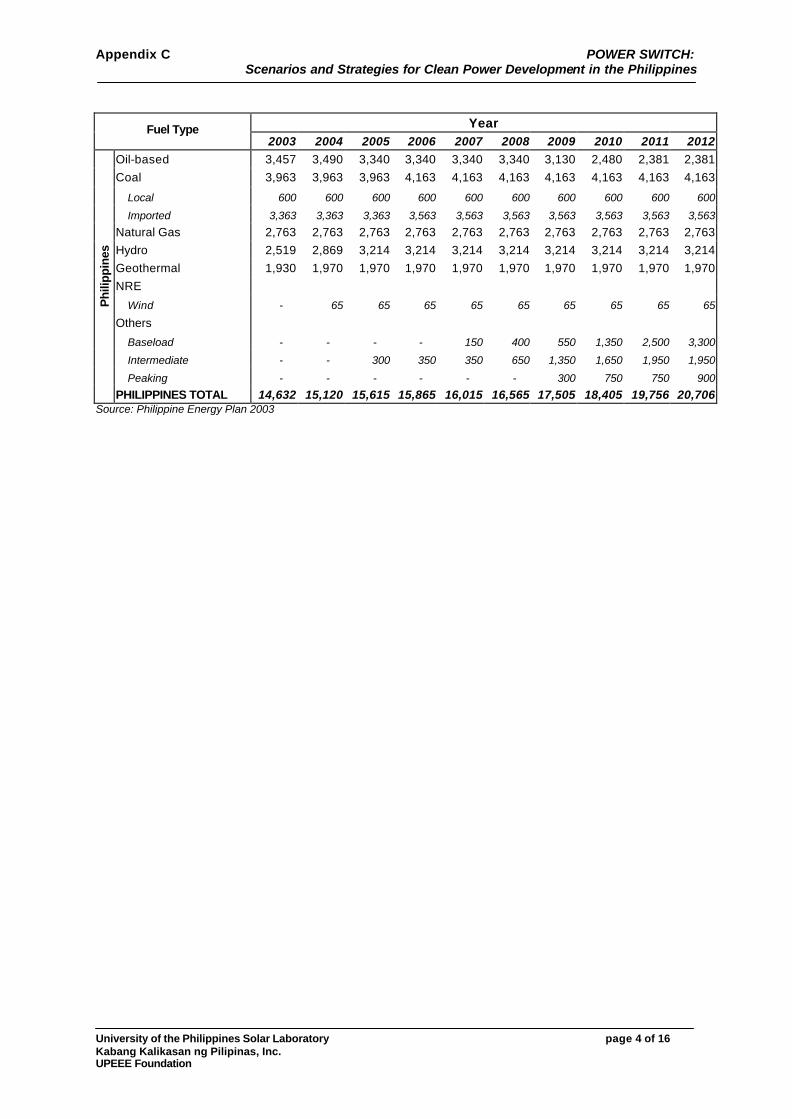

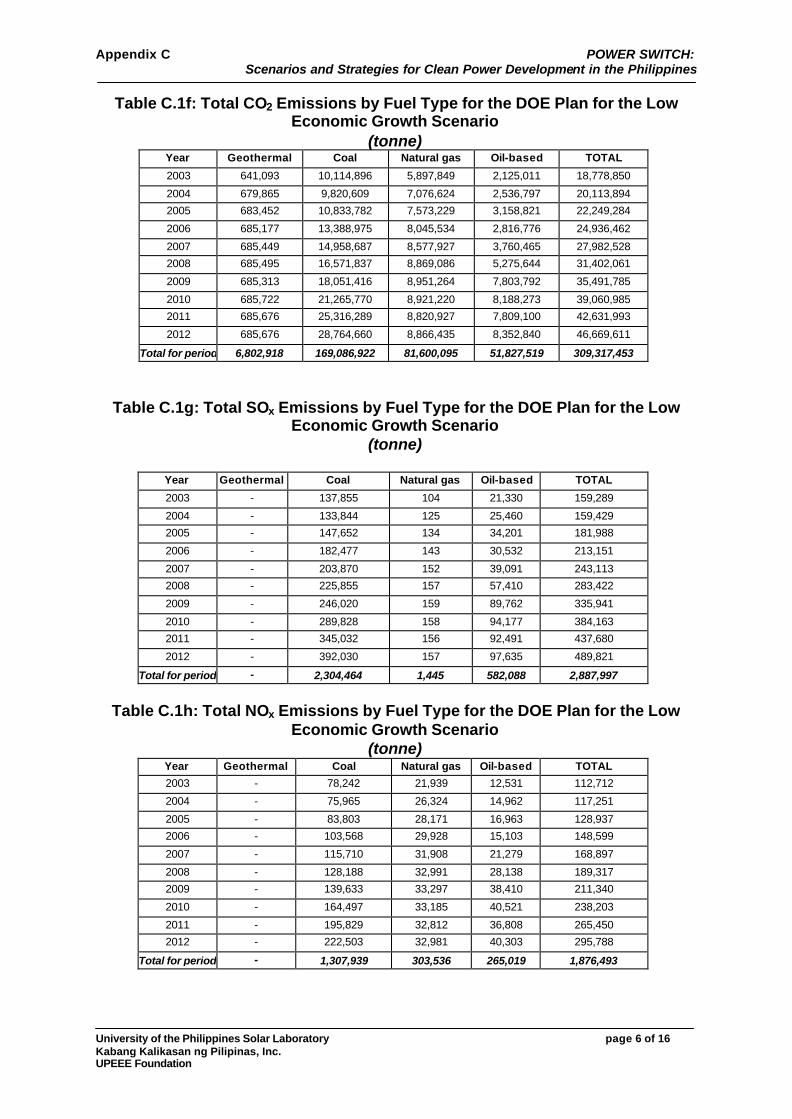

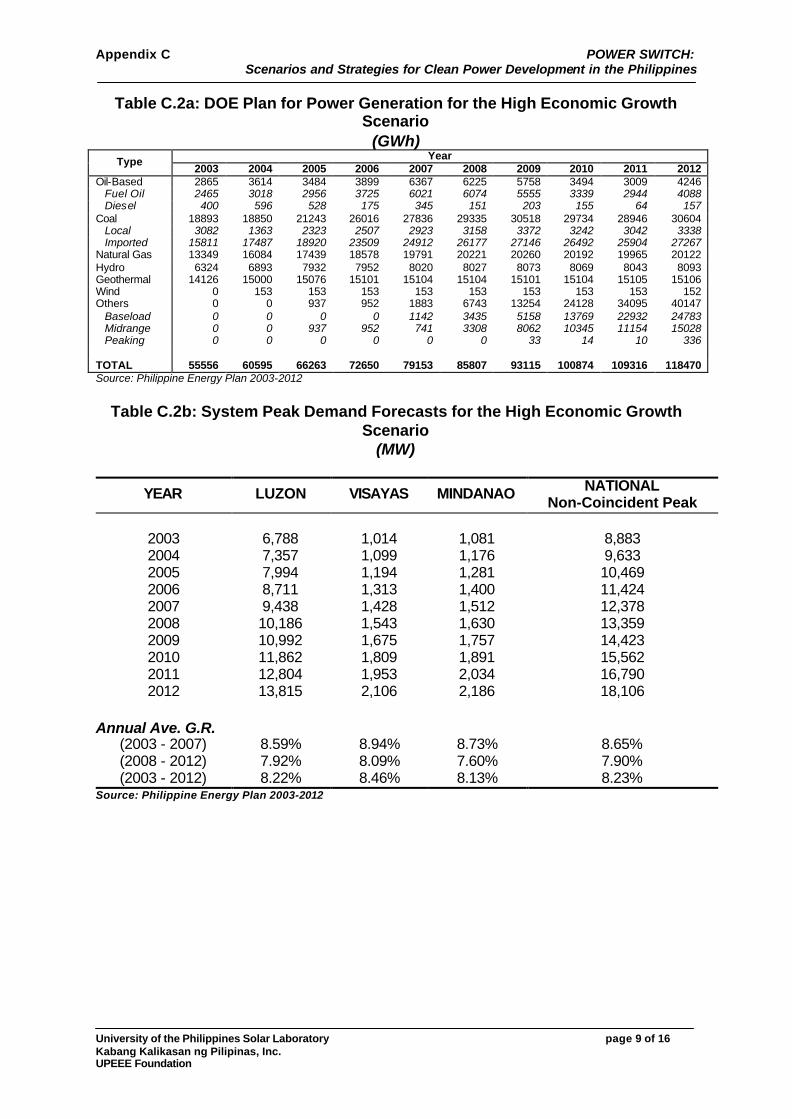

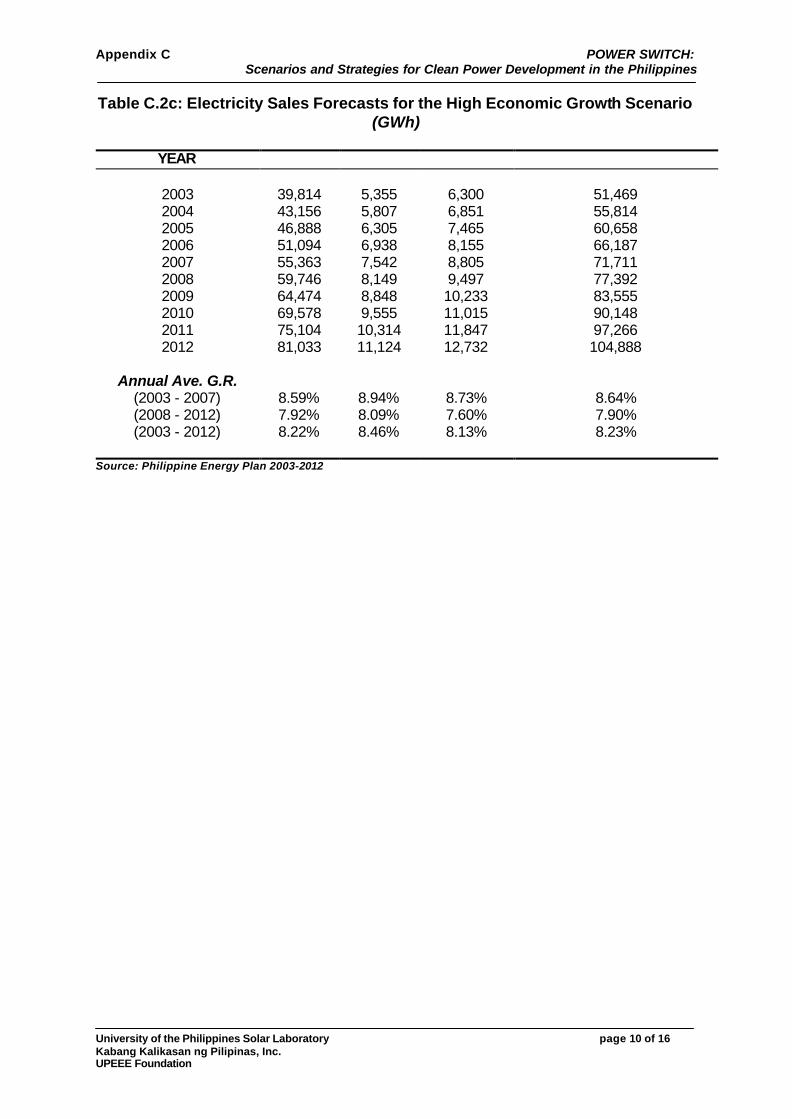

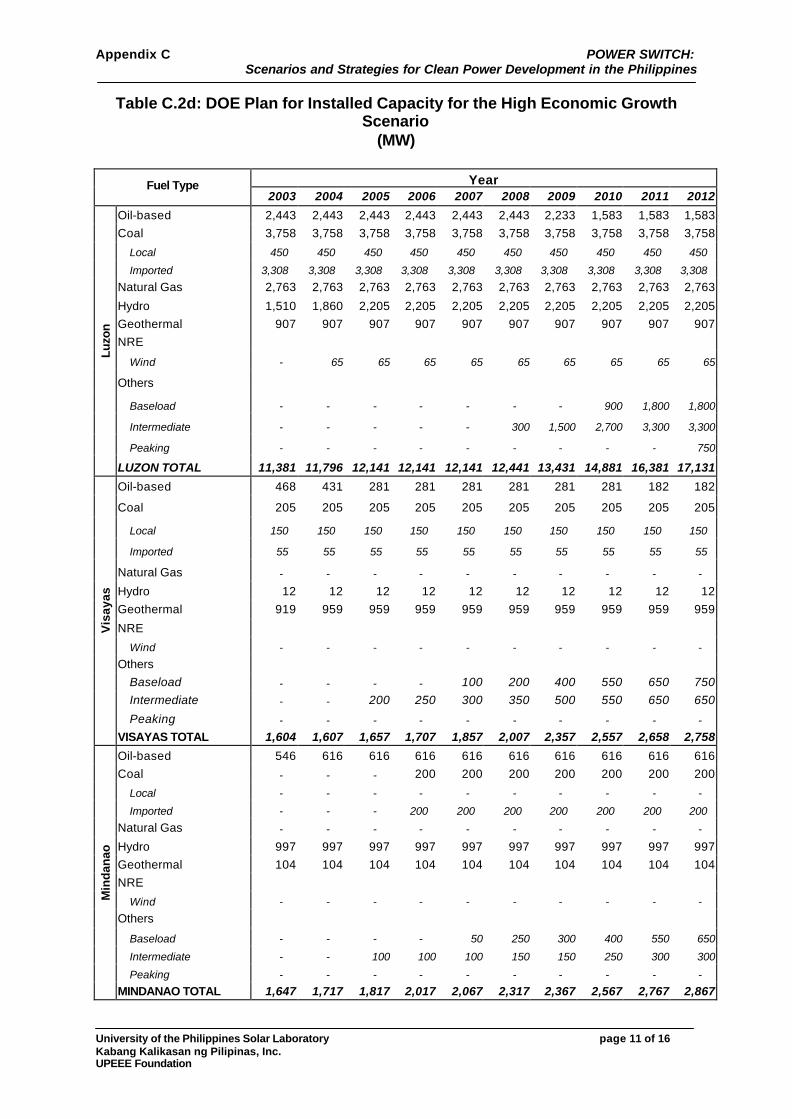

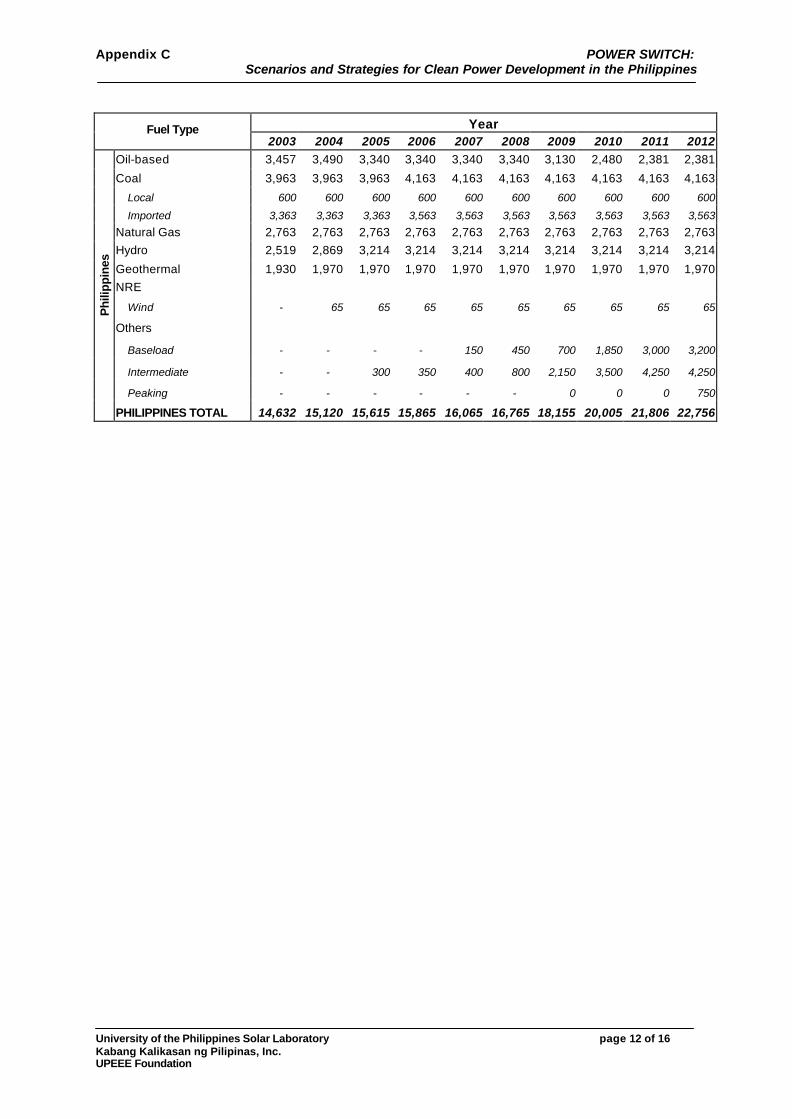

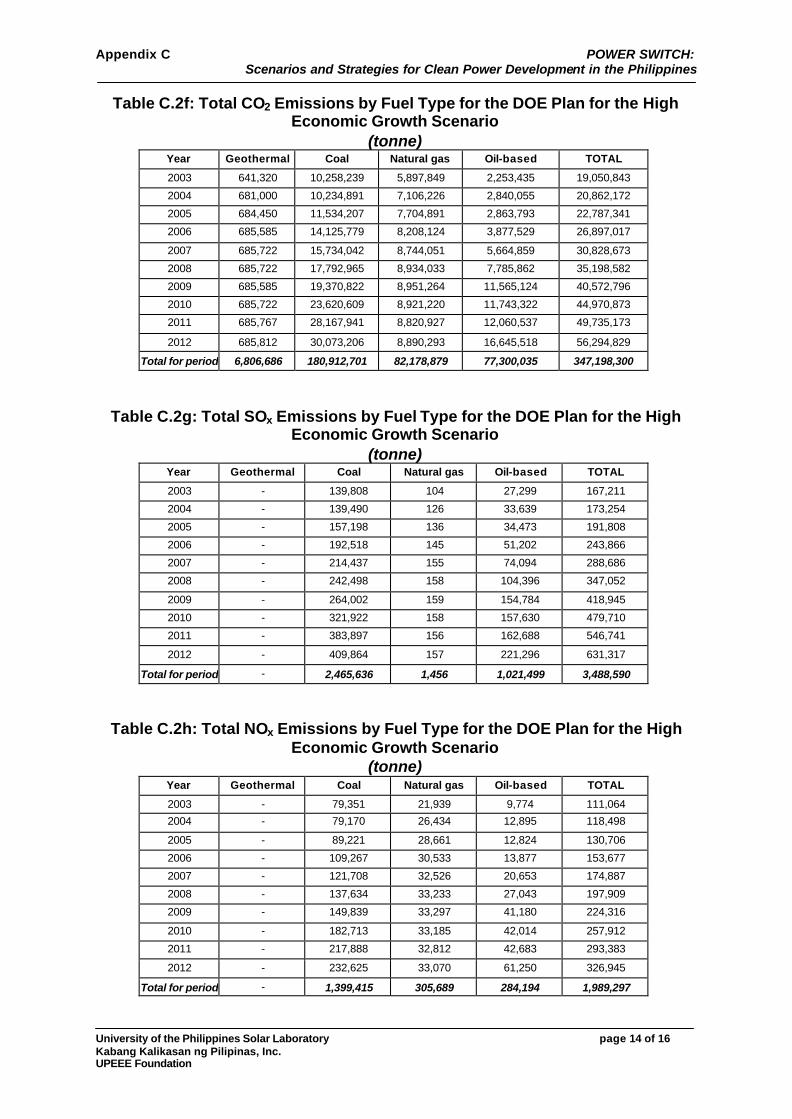

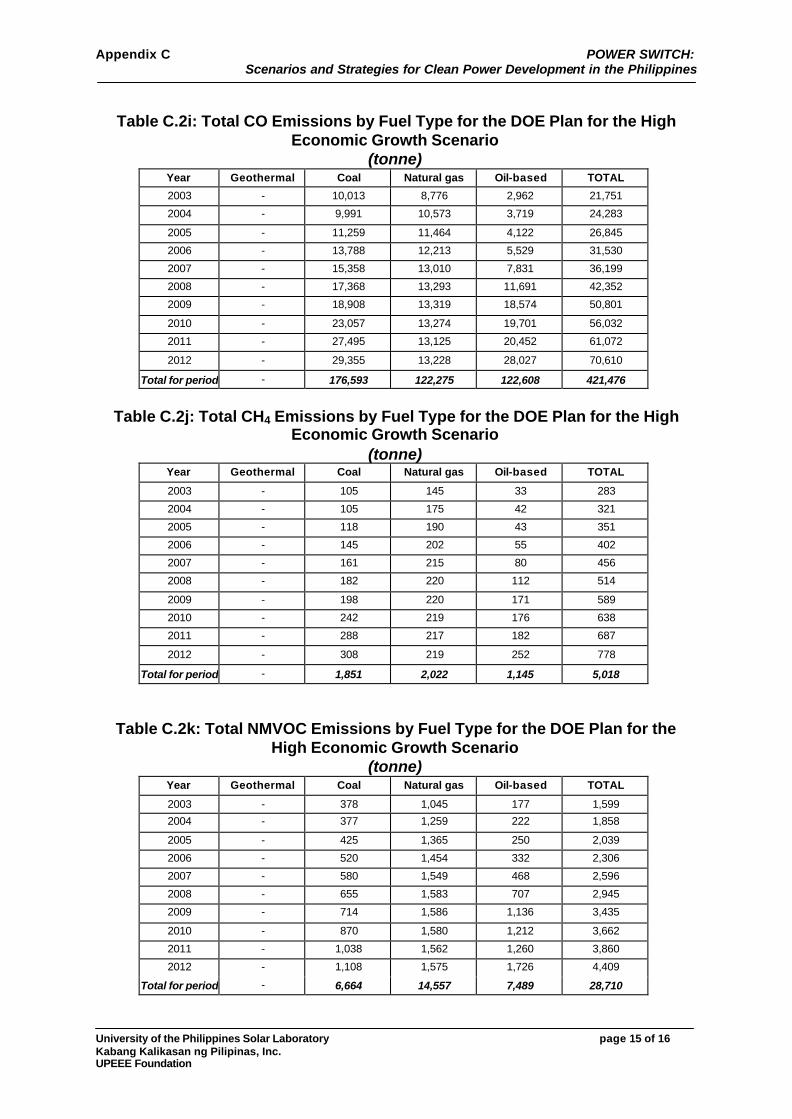

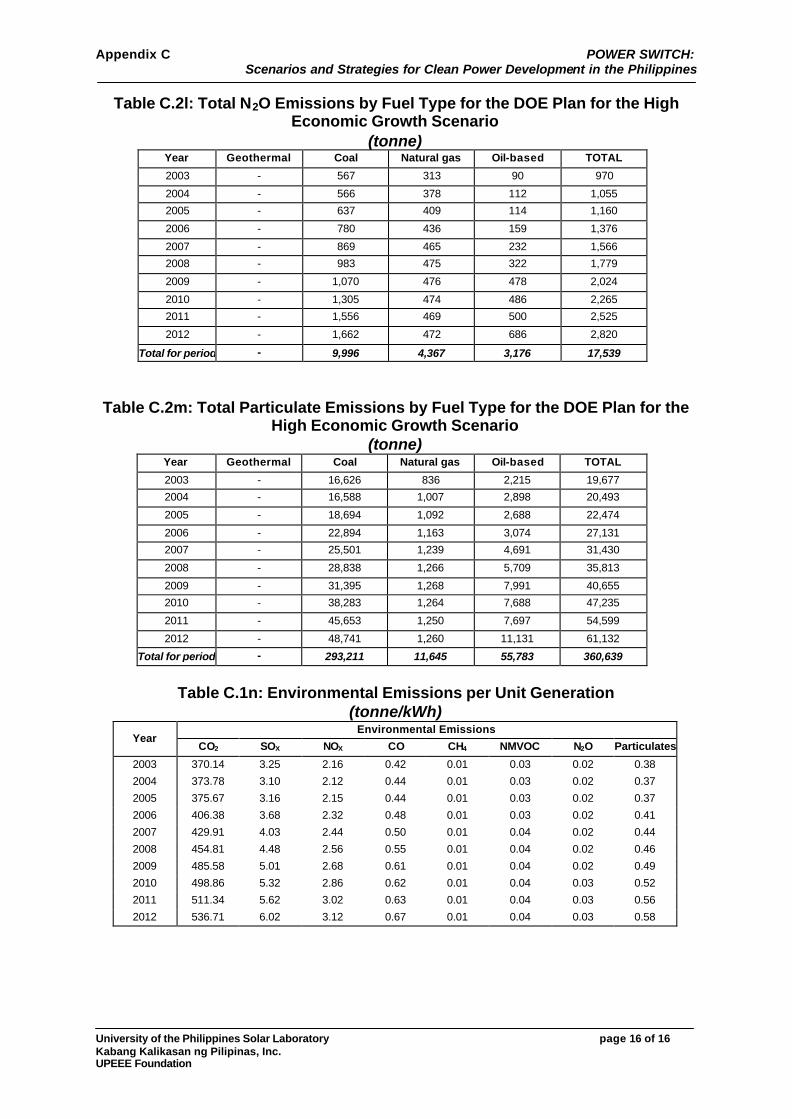

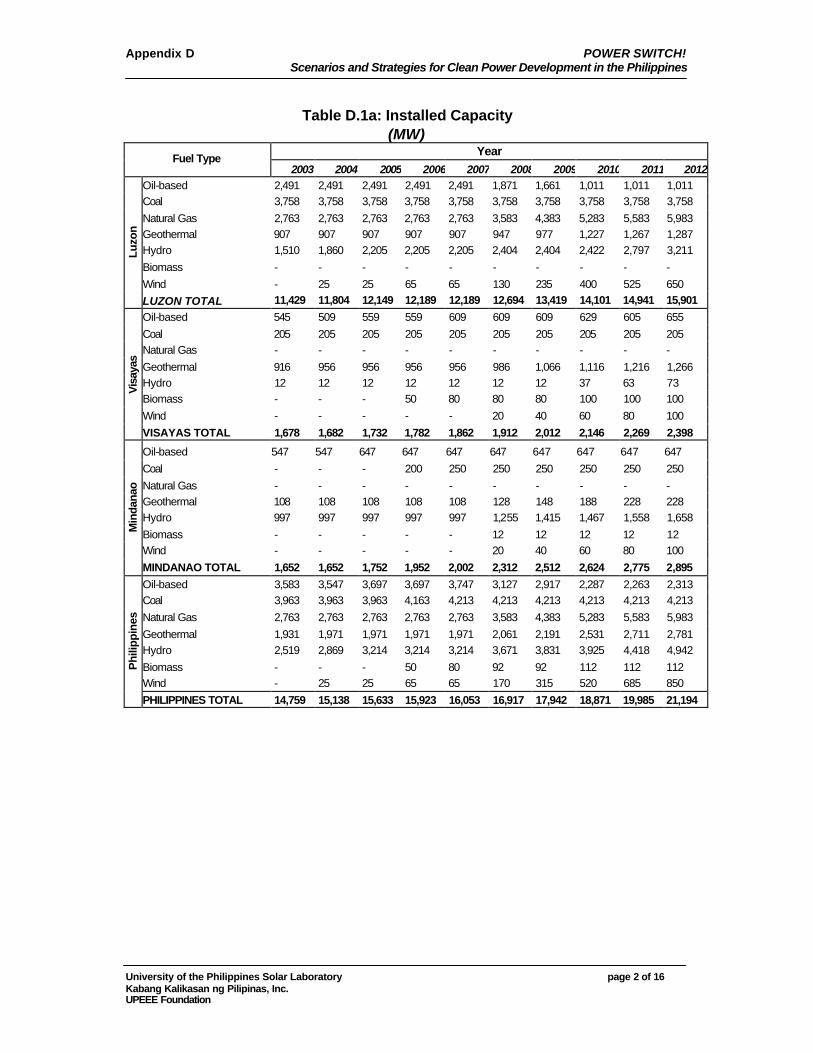

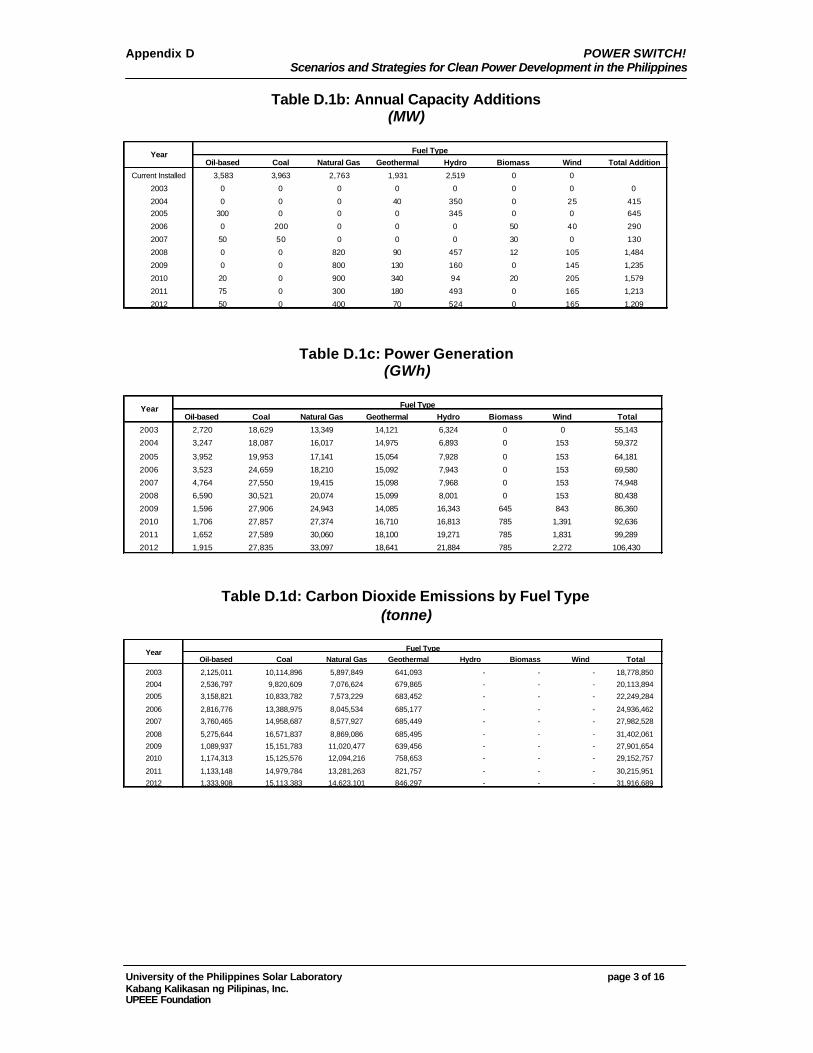

1.4 Scenarios under the Philippine Energy Plan 2003 - 2012 The prospective performance of the Philippine Power Sector was also assessed based on the Philippine Energy Plan 2003 – 2012 prepared published by the Department of Energy. Reliability, environmental emissions and costs were calculated similar to that of the historical performance assessment. PDP for the Low Economic Growth Scenario The PEP, based on the low economic growth projections of NEDA, shows that energy generation will increase by 93% (55,142 GWh in 2003 to 106,430 GWh in 2012) over the entire period at an average rate of 7.57% annually. Total installed capacity of 14,632 GW for 2003 will increase to 20,706 MW by 2012. The increase in demand will be met mostly by increases in coal power plants (3,500 MW) and oil-based plants (1,775 MW). The increase in the share of renewable energy generating capacity will come from a 795 MW large hydro, 65 MW wind and a 40 MW geothermal capacity additions. No additional capacity addition for natural gas is expected in the period. Capacity additions, operations and maintenance and fuel would require a total cost $ 23,828 million (UPSL estimate at 2002 present value). In terms of reliability, the planned capacity additions will result in high reserve margins. For example, the reserve in 2003 will be 66%. Although this is expected to decline to 22% by 2012, it is still unrealistic to expect that cost of electricity in the Philippines in the near term will decrease under this scenario. While the generation cost for this scenario is estimated at PhP 3.16/kWh, the Purchased Power Adjustment (PPA) component in the electricity bills of the end users is still expected to result in higher cost due to the high reserve margins. To meet the energy requirements, this scenario would require 124.5 million barrels fuel oil equivalent (MMBFOE) of oil, 91.9 million tonnes of coal and 1,263 billion cubic feet (BCF) of natural gas. Of these amounts, 124.5 MMBFOE of oil and 80.2 million tonnes of coal would have to be imported. The environmental emissions resulting from DOE’s generation plan for the low economic growth scenario would result in an increase in CO2, SOx and other emissions. Total CO2 emissions for the DOE plan for the low economic growth scenario is 309.3 million tonnes. The increase in the use of coal will account to contributing 55% of the total CO2 emissions for the period. Oil-based and natural gas plants will contribute 17% and 26% to the CO2 emissions, respectively. Geothermal plants will contribute only 2%. These emissions will be the direct result of the share of coal, natural gas and oil-based sources in the energy mix which is 34%, 24% and 4%, respectively for year 2003. From a share of 37% in 2003, renewable energy’s share will decrease to only 22% in 2012. The contribution of non-renewable energy sources to the energy mix, on the other hand will increase by 24%, with the continued dominance of coal plants. This scenario will require $ 29,368 million in abatement cost.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 8 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

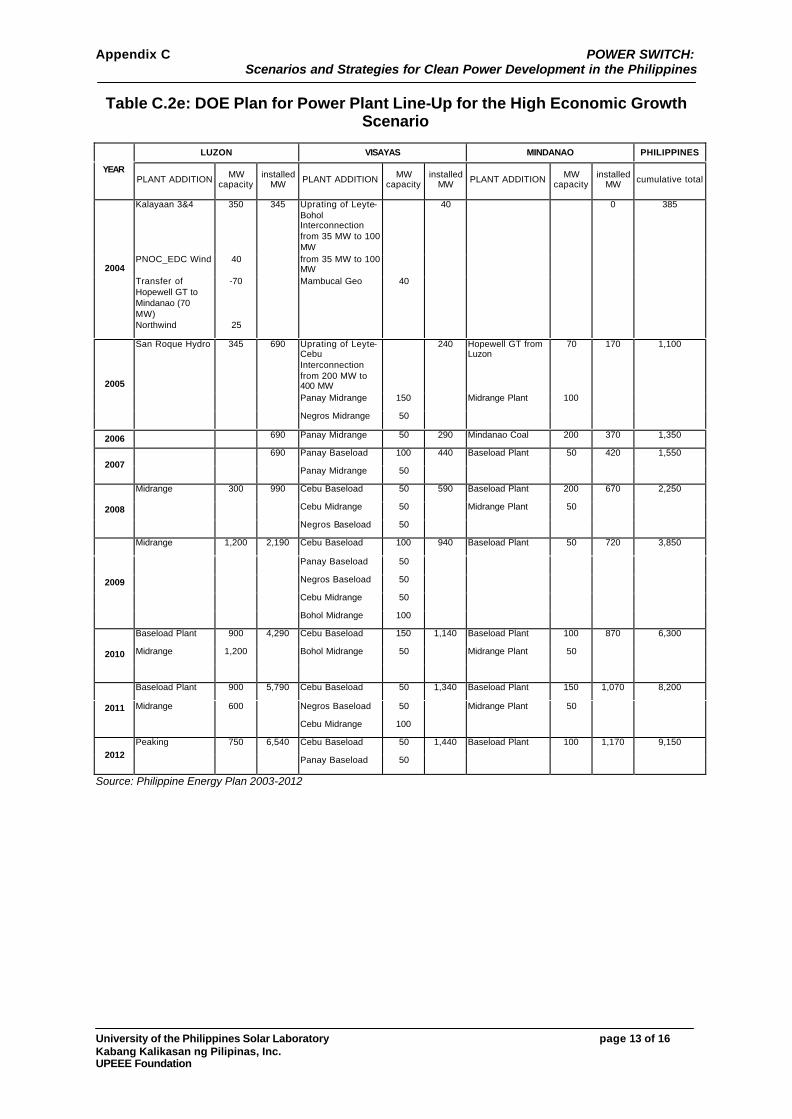

The PEP under the Low GDP Scenario reflects the continued preference on the use coal. Notably, this plan can be judged as a business-as-usual plan that will only replicate (or be even worse than) the historical performance of the Philippine power sector from the point of view of sustainable development. PDP for the High Economic Growth Scenario The DOE also prepared a power development plan based on high economic growth projections of NEDA. Analysis of the PEP under this scenario indicates that the plan is also a business-as-usual plan that will perform no better than the historical performance of the Philippine power sector, nor the scenario for the low economic growth. The following performance indicators can be expected if this scenario push through:

a) Installed capacity: 14,632 MW in 2003 to 22,756 MW in 2012

(56% increase for the 10-year period)

b) Energy generation: 55,556 GWh in 2003 to 118,470 GWh in 2012

(213% increase for the 10-year period)

c) Reserve Margin: 25% (minimum) to 65% (maximum)

d) Energy Mix: Coal - 16% in 2003 increase to 47% in 2012

Oil - 5% in 2003 increase to 16% in 2012

Natural gas - 24% in 2003 decrease to 17% in 2012

R.E. - 37% in 2003 decrease to 20% in 2012

With the continuous decline in the share of renewable energy, within the planning period, greenhouse emissions is expected to further soar, increasing by 195% from 2003 to 2012, and will require $ 32,995 million in abatement cost. 1.5 Clean Power Development Options for the Philippines Using the clean energy technologies and resources, two (2) alternative power development plans (or strategies) that will meet the demand of the Low Economic Growth Scenario and the High Economic Growth Scenario of the PEP were prepared by UPSL. These strategies are the following:

• Moderate Clean Power Development (CCPD) Plan

In this plan, capacity addition and utilization of renewable energy (geothermal, biomass, wind and hydro power) and natural gas plants are given priority over that of non-renewable plants for power generation. Total installed capacity of wind power plants is allowed to reach a maximum of 5% of the peak demand.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 9 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

• Aggressive Clean Power Development (ACDP) Plan

For this plan, the strategy is to utilize all the practical renewable energy resources where possible without caps. Cost penalties for intermittent power plant capacity beyond 5% (based on peak demand) was also imposed to account for the additional ancillary services.

It was assumed in these plans that the local natural gas industry will be able to supply fuel for up to 3,800MW natural gas power plants (maximum generation of 23,000 GWh annually) for the next twenty years. The additional natural gas requirement will be supplemented by imports from the neighboring Asian countries and other natural gas producers until new local resources are developed. For all the plans, the 2003 to 2007 capacity additions were based solely on the PEP list of committed projects. The percentage installed reserve margin for the years 2008 onwards is kept as close as possible to the corresponding PEP reserve margins for comparison. Note, however, that these reserve margins do not take into account the ancillary diesel engines, which serve as frequency regulating plants for the wind power plants. Assuming a five-year lead-time for the planning to commissioning of the additional power plants, the capacity additions starts only in 2008. In this summary, only the power development plan to meet the Low Economic Growth Scenario of the PEP 2003 – 2012 is presented. The plans that correspond to the High Economic Growth Scenario are detailed in Chapter 5. Moderate Clean Power Development (MCPD) Plan To meet the demand of the Low Economic Growth Scenario, this plan will increase the renewable energy plant installed capacity by 95% (from 4,450 MW in 2003 to 8,685 MW in 2012) and the natural gas plant capacity by 117% (from 2,763 MW in 2003 to 5,983 MW in 2012). This translates to a 69% total installed capacity for the combined natural gas and renewable energy plants. The share of renewable energy in the energy mix will increase from 37% to 41%, from the period 2003 to 2012. The natural gas contribution will also increase from 24% to 31%. This will translate to a 72% total share of clean energy in the energy mix by 2012. The share of coal and oil in the mix will be reduced by about 11% at the end of the period. This plan will reduce the GHG emissions and abatement costs for the Low GDP Scenario by 14% and 21%, respectively, as compared with the PEP. Total CO2

reduction as compared with the PEP is 44.6 million tonnes. The total cost calculated for this plan is $23,592 million and the average generation cost is PhP 3.12/kWh. This average generation cost is even cheaper than that of the PEP Low GDP scenario, which is PhP 3.16/kWh. Considering the investment, O&M and fuel costs, this plan will save $235 million in the planning period.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 10 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Aggressive Clean Power Development (ACPD) Plan To meet the demand of the Low Economic Growth Scenario, the ACPD plan will increase the renewable energy plant installed capacity by 159% (from 4,450 MW in 2003 to 11,520 MW in 2012) and the natural gas plant capacity by 95% (from 2,763 MW in 2003 to 5,383 MW in 2012). This translates to a 79% total installed capacity for the combined natural gas and renewable energy plants. The share of renewables in the energy mix will increase from 37% to 48%, from the period 2003 to 2012. The natural gas contribution will also increase from 24% to 31%. This will translate to a 79% total share of clean energy in the energy mix by 2012. The share of coal and oil in the mix will be reduced by about 20% at the end of the period. This plan will reduce the GHG emissions and abatement costs under the PEP Low GDP Scenario by 18% and 27%, respectively. The total cost calculated for this plan is $23,881 million and the average generation cost is PhP 3.17/kWh. This is comparable to the PEP Low GDP scenario, which is PhP 3.16/kWh but five centavos (PhP 0.05) per kWh more expensive than the Moderate Clean Power Development Plan due to the additional ancillary services for the intermittent wind power supply. Considering the investment, O&M and fuel costs, this plan will cost an additional $41M in the planning period compared to the PEP low GDP plan. This translates to a mitigation cost of $0.67/tonne of CO2. With the current price of CO2 at $2 - $10 per tonne, this plan will create an opportunity for the country in the carbon market. 1.6 Conclusions and Recommendations The Philippine power sector from 1991 to 2001 has not performed very well in terms of reliability and cost to end-users. While the PEP has tried to address these problems, it fails to consider the implications of the activities in this sector to the environment that could even be more important if only the externalities will be considered in the economics of energy supply. This study has assessed the technologies and resources in the Philippines that could be tapped for clean power development. To avoid significant amounts of GHG emissions in the future, the country has to resort to biomass, small hydro, wind and natural gas technologies, as was done in this study. To support power switching, new natural gas sites must be identified and developed. In addition, natural gas importation may be pursued. This study also offers two alternative paths (moderate and aggressive) through the alternative clean power development plans. These alternative plans are comparable to the PEP in terms of costs. There are even opportunities that can create additional dollar income from carbon trading and local employment. At the current CO2 prices ($5 per tonne) in the market, the Moderate Clean Power Development Plans are viable greenhouse gas mitigation option for the Philippines offering so many

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 11 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

opportunities both for the developers and the country. Switching to cleaner energy, therefore, is attractive as the price of carbon is expected to increase in the future. Pursuing Clean Power Development plans requires the development of a “clean energy” market in the country through effective policy instruments and mechanisms that will secure the investment climate while protecting public interest. A set of measures that should be made to attract more investments in renewable generation technologies in the future discussed below. Energy Planning The first step in developing the market for clean energy is to introduce reforms in the process of energy planning itself. Since power developers will only respond to the government call, it is important that the Philippine Energy Plan reflect the call for clean power development. This could be achieved through the following: • Improve the power development planning models

- Include environmental externalities in planning models to reflect the true cost to society of energy decisions;

- Consider the economics of smaller capacity, following load growth to deal with the overcapacity issue (in contrast to large capacity power plants currently used in energy planning);

- Include energy efficiency as a demand side option in energy planning models;

- Use coal-fired fluidized combustion technology as benchmark fossil-based plant instead of pulverized coal;

- Increase the number of candidate Renewable Energy-based Power Plants in the selection process. To increase the number of candidate renewable energy plants in planning, more rigorous and site-specific resource assessment must be conducted.

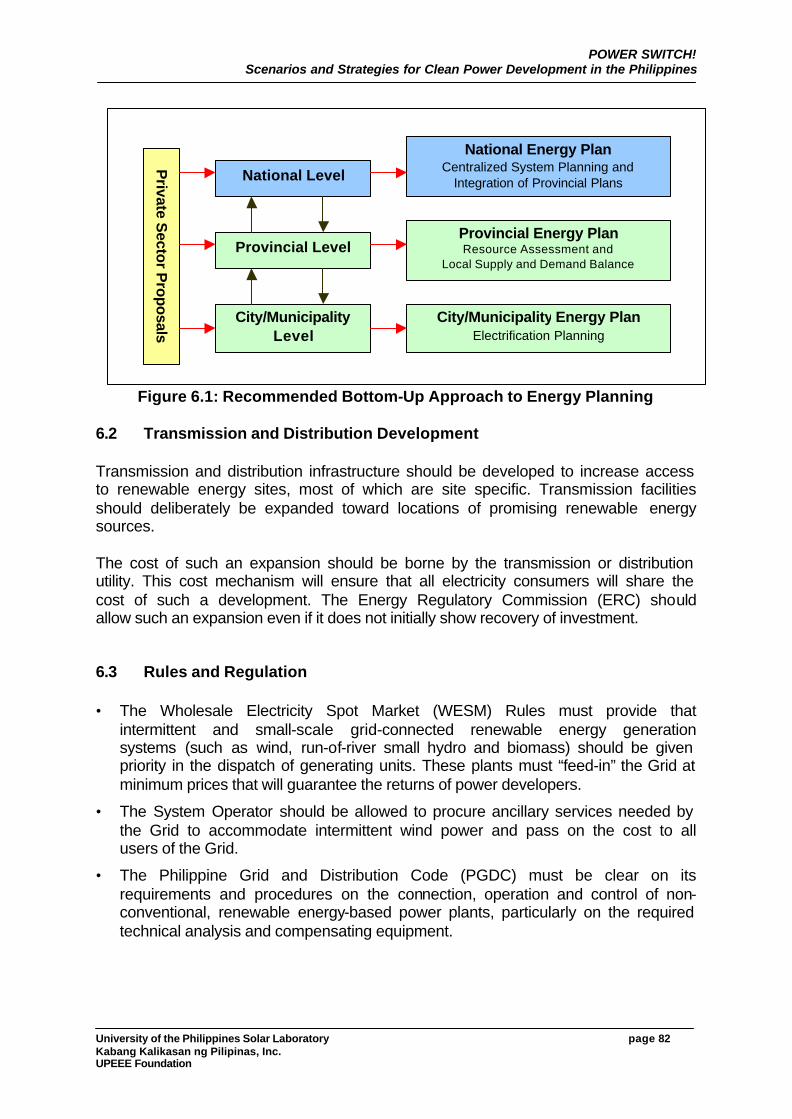

• Institutionalize a participative planning process. A decentralized planning process down to the level of the local government and participated by the stakeholders in the locality should complement the top-down planning process at the national level. Electrification planning can be done in the municipality/city levels. Resource assessment and local supply and demand balance can be done at the provincial level. This decentralized planning scheme will result in a more realistic demand forecast and will address local issues on energy, as well as issues on under- and overcapacity. While this planning process allows for a greater degree of public participation, it will also entail capacity building for local government units in the areas of planning and resource assessment.

Transmission and Distribution Development Transmission and distribution infrastructure should be developed to increase access to renewable energy sites, most of which are site specific. Transmission facilities should deliberately be expanded toward locations of promising renewable energy sources.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 12 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

The cost of such an expansion should be borne by the transmission or distribution utility. This cost mechanism will ensure that all electricity consumers will share the cost of such a development. The Energy Regulatory Commission (ERC) should allow such an expansion even if it does not initially show recovery of investment. Rules and Regulation • The Wholesale Electricity Spot Market (WESM) Rules must provide that

intermittent and small-scale grid-connected renewable energy generation systems (such as wind, run-of-river small hydro and biomass) should be given priority in the dispatch of generating units. These plants must “feed-in” the Grid at minimum prices that will guarantee the returns of power developers.

• The System Operator should be allowed to procure ancillary services needed by the Grid to accommodate intermittent wind power and pass on the cost to all users of the Grid.

• The Philippine Grid and Distribution Code (PGDC) must be clear on its requirements and procedures on the connection, operation and control of non-conventional, renewable energy-based power plants, particularly on the required technical analysis and compensating equipment.

Incentive Programs • The Department of Energy must ensure that renewable energy development

should always be included in the Philippine Investment Priorities of the Board of Investment to ensure that the fiscal (e.g., tax exemptions, income tax holidays and tax credits) and non-fiscal (e.g., simplification of custom procedures and importation of consigned equipment) will be available for renewable energy developers.

• An assistance program should be created for renewable energy development. This may include subsidy for resource assessment and feasibility studies for serious developers of renewable energy.

• Dedicated Financing Windows that allow longer repayment periods for renewable energy-based development.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 13 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

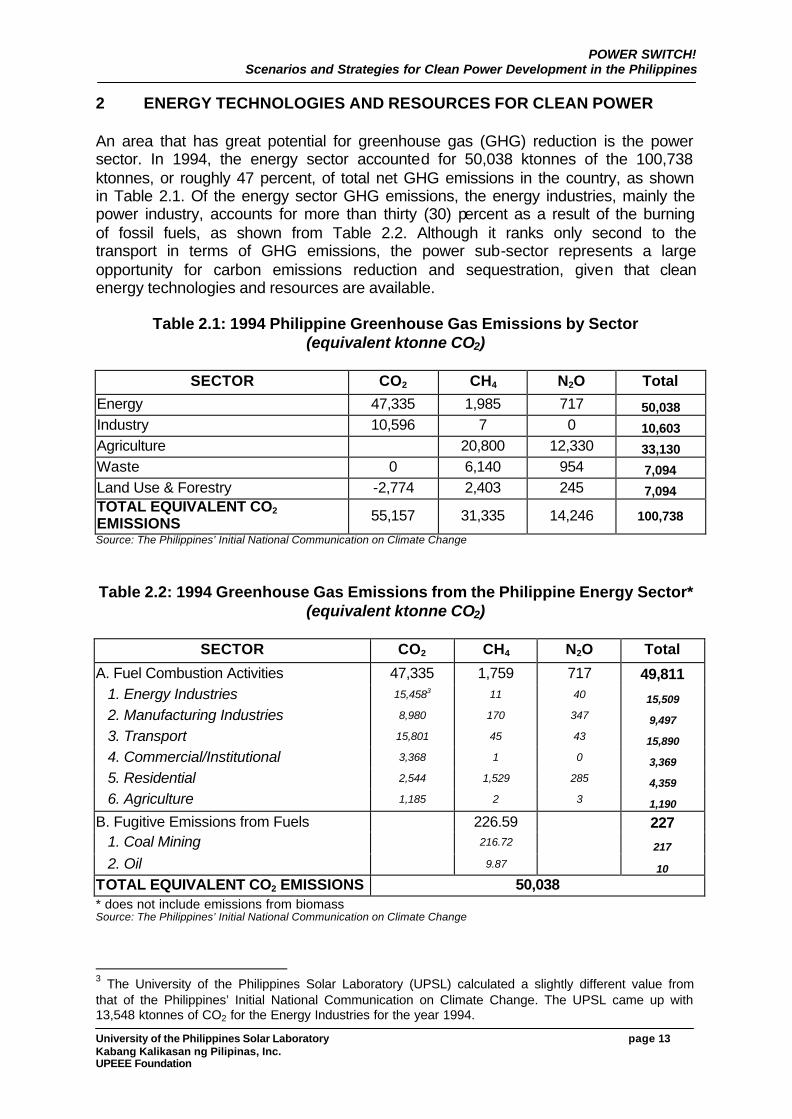

2 ENERGY TECHNOLOGIES AND RESOURCES FOR CLEAN POWER An area that has great potential for greenhouse gas (GHG) reduction is the power sector. In 1994, the energy sector accounted for 50,038 ktonnes of the 100,738 ktonnes, or roughly 47 percent, of total net GHG emissions in the country, as shown in Table 2.1. Of the energy sector GHG emissions, the energy industries, mainly the power industry, accounts for more than thirty (30) percent as a result of the burning of fossil fuels, as shown from Table 2.2. Although it ranks only second to the transport in terms of GHG emissions, the power sub-sector represents a large opportunity for carbon emissions reduction and sequestration, given that clean energy technologies and resources are available.

Table 2.1: 1994 Philippine Greenhouse Gas Emissions by Sector (equivalent ktonne CO2)

SECTOR CO2 CH4 N2O Total

Energy 47,335 1,985 717 50,038 Industry 10,596 7 0 10,603 Agriculture 20,800 12,330 33,130 Waste 0 6,140 954 7,094 Land Use & Forestry -2,774 2,403 245 7,094 TOTAL EQUIVALENT CO2 EMISSIONS 55,157 31,335 14,246 100,738

Source: The Philippines’ Initial National Communication on Climate Change

Table 2.2: 1994 Greenhouse Gas Emissions from the Philippine Energy Sector*

(equivalent ktonne CO2)

SECTOR CO2 CH4 N2O Total

A. Fuel Combustion Activities 47,335 1,759 717 49,811 1. Energy Industries 15,4583 11 40 15,509

2. Manufacturing Industries 8,980 170 347 9,497

3. Transport 15,801 45 43 15,890

4. Commercial/Institutional 3,368 1 0 3,369

5. Residential 2,544 1,529 285 4,359

6. Agriculture 1,185 2 3 1,190

B. Fugitive Emissions from Fuels 226.59 227 1. Coal Mining 216.72 217

2. Oil 9.87 10

TOTAL EQUIVALENT CO2 EMISSIONS 50,038 * does not include emissions from biomass Source: The Philippines’ Initial National Communication on Climate Change

3 The University of the Philippines Solar Laboratory (UPSL) calculated a slightly different value from that of the Philippines’ Initial National Communication on Climate Change. The UPSL came up with 13,548 ktonnes of CO2 for the Energy Industries for the year 1994.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 14 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

This study focuses on the reliability, cost and environmental performance (particularly on GHG emissions) of the power sector. In particular, it looks into scenarios that would entail switching to clean energy technologies from conventional fossil fuel-based technologies for grid-connected power generation. In the sections that follow, technologies and resources that could be used to reduce GHGs from the power sector shall be discussed and evaluated to determine what could be used in the Philippine power sector. 2.1 Clean Energy Technologies Clean energy technologies are those that result in relatively fewer GHG emissions per unit of energy service delivered as compared to conventional technologies. These technologies may be classified as4:

• measures that reduce the energy intensity of the economy (e.g., energy conservation, improvement of power plant heat rates);

• measures that reduce the carbon intensity of energy (e.g., renewable energy technologies); and

• measures that integrate carbon sequestration into the energy production and delivery system.

These technologies may be an attractive alternative to conventional fossil fuel-based generation technologies in terms of its environmental benefits. However, they must compete with the same technologies in terms of other criteria such as cost, resource availability and technology maturity before application on a significant scale could be expected. In the following sections, a number of clean energy technologies shall be discussed. These technologies will then be evaluated to determine their viability for the Philippine power sector. Measures that Reduce Energy Intensity One way of reducing the energy intensity of the economy is by minimizing energy losses in the system. In power generation, improvements could be made to improve the efficiency of existing power plants by decreasing their heat rates, i.e., the heat energy in Btu required by the power plants to produce a kilowatt-hour of electric energy. This is done by looking at ways to improve the performance of existing power plant components like boilers, turbines and generators. This measure is a cost-effective method of achieving CO2 reductions in that it would not entail large costs for equipment although it would require capability-building activities. The Philippines Department of Energy (DOE) has already started a Heat Rate Improvement Program, which is expected to achieve a substantial amount of energy savings.

4 Marilyn A. Brown, Mark D. Levine and Walter D. Short, Scenarios for a Clean Energy Future, (U.S.: Interlaboratory Working Group on Energy-Efficient and Clean Energy Technologies), p. 1.2

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 15 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Another measure is the use of efficient end-use devices. Improved technologies for electricity-consuming end-use devices are available in the market like more efficient motors, lighting technologies, refrigerators and air conditioners. In a study made by Leverage International (Consultants) Inc. on the characterization of new commercial buildings in the Philippines, it was mentioned that energy savings amounting to 39%, 32% and 10% could be realized from more efficient air conditioning, lighting and other office equipment, respectively5. In the industrial sector, potential energy savings could be realized in the use of high efficiency motors. A study conducted in 1994 estimated energy savings amounting to 423 GWh and about 74 MW of capacity could have been realized by the year 2010 in the Manila Electric Company (MERALCO) franchise area6 alone had a high efficiency motors program been implemented in 19977. The DOE has for some time been implementing an efficiency and energy-labeling and standard program to help consumers select electric appliances and equipment. The program includes the Efficiency Standard and Labeling for Room Air Conditioners, the Energy Labeling Program for Refrigerators and Freezers, the Fluorescent Lamp Ballast Energy Efficiency Standard and the Performance Certification of Fans and Blowers. The program is expected to achieve a potential energy savings amounting to 9.7 MMBFOE from 2002 to 20118. Despite the high potential of technology measures that reduce energy intensity, which could be treated as a resource in energy planning, it is not used in this study because data available in the Philippines is insufficient to do so. Measures that Reduce the Carbon Intensity of Energy For the electricity generation sector, technologies that reduce carbon intensity of energy can be classified in a number of categories. These categories are not absolute in that they sometimes overlap and some particular technology types fall under two or more categories. They are as follows: • Renewable energy technologies

These are technologies that harness the energy from renewable energy sources for power generation. Renewable energies include solar, wind, hydro, biomass and geothermal energies. Aside from it’s being clean, renewable energy sources, because of its “inexhaustibility” addresses other challenges of the energy sector such as sustainability and energy security.

5 Philippine New Commercial Building Market Characterization, (Philippines: Department of Energy, 1998), p. 9. 6 MERALCO is the distribution utility that services Metro Manila, Bulacan, Rizal, Cavite and parts of the provinces of Laguna, Quezon, Batangas and Pampanga. 7 The study referred to is the Asian Development Bank-funded Long Term Power Planning Study conducted by SRC in 1994, mentioned in the material for the March 12, 1998 meeting for the Motor Energy Efficiency Enhancement Program. 8 Philippine Energy Plan 2002-2011, (Philippines: Department of Energy), p. 59.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 16 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

1. Wind Energy. The kinetic energy of the wind can be converted to mechanical energy by means of a wind turbine. This mechanical energy can then be used to run electric generators to produce electricity. Wind energy conversion technology (WEC) is a mature technology, with worldwide installed capacity totaling to 24,000 MW by the end of 2001.

Intermittent power would affect power system operability and stability and therefore poses limitations on levels of penetration of wind power. Various modeling studies show that wind generation capacities could amount from a low value of 4% to a high value of 50% of system load9, depending on system conditions. Utilities’ operational experience, particularly in the United States, has been limited to low wind power penetration levels so far. Also, intermittent generation will require additional ancillary services to be provided in the grid, and therefore translates to higher electricity costs. For the Philippines, initial estimates for wind penetration levels are between 5% and 20%. The University of the Philippines Solar Laboratory (UPSL) is currently doing studies to determine acceptable wind penetration levels considering economics and the stability of the transmission system.

2. Hydro Power. Hydro power refers to the use of falling or flowing water for

power. It is a renewable form of energy because the energy of flowing water ultimately comes from the sun. Water evaporation from the oceans and other parts of the earth’s surface consumes about one fourth of the total solar incidence on the planet. This water will return to the earth’s surface as precipitation (e.g., through rain or snow) and part of it will eventually contribute to the flow of streams, rives and falls.

Hydro power resources come in various sizes. The Philippines Department of Energy (DOE) classifies hydro resources based on its potential capacity, as follows: micro-hydro for hydro resources with capacities ranging from 1 to 100 kW; mini-hydro for those with capacities from 101 kW to 10 MW, and; large hydro as those with capacities greater than 10 MW10. Hydro power is considered a clean technology because it is renewable and does not emit air pollutants. In some cases, it generates some amount of GHG gases as a result of the rotting of organic matter that get submerged in reservoirs, but the amount of emissions is small as compared to fossil fuel-based electricity generation. The Canadian Hydropower association estimates that GHG emissions from hydro facilities is 60 times less than that of coal power plants and 18 times less than that of natural gas power plants11.

9 p. 49, Yih-huei Wan and Brian K. Parsons, Factors Relevant to Utility Integration of Intermittent Renewable Technologies, (Colorado: National Renewable Energy Laboratory, 1993), p. 49. 10 The World Energy Commission uses a different classification from that used by the DOE, which are as follows: micro hydro resources are those with capacities less than 100 kW; mini-hydro resources are those with capacities ranging from 100 kW to 1 MW, and; small hydro resources are those with capacities from 1 to 10 MW. Large hydro resources are those with capacities greater than 10 MW. Thus, the Philippine definition of mini-hydro encompasses the WEC mini- and small-hydro resources. 11 Quick Facts, Canadian Hydropower Association

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 17 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Hydro power facilities offer other benefits such as low generation costs, high efficiencies, little maintenance, long life and high levels of reliability. They are – large hydro in particular - however, associated with a number of negative impacts. Among them are:

Ecological Effects

a. Landscape destruction

b. Destruction of fish habitat and fisheries

c. Rearrangement of water resources

d. Increase in water pollution

e. Displacement/wiping out of plant and animal species

f. Silting Social Impacts

A major negative social impact of large hydro projects is the dislocation of population. Various hydro projects in the Philippines have dislocated thousands. In the Philippines, the Agno River Basin Development Program resulted in the loss of hectares of Ibaloy ancestral lands and the subsequent dissolution of several Ibaloy communities. The alteration of the local ecosystem also resulted in the loss of resource base, which served as livelihood of the Ibaloys.

Risk and Safety

Major disasters involving dams have occurred in the past at 6 to 10 year intervals. With about 15,000 dams all over the world, the frequency of disasters involving dams is 1 disaster for every 120,000 dam years. Speculation also arise that dams cause earthquakes in its surrounding areas.

3. Biomass Energy. Like hydro and geothermal power, biomass energy is a

renewable resource that can be used for base load electric generation. Technologies that can be used to generate power from biomass include gasification-electric generation systems and burner technologies similar to that used for coal.

4. Geothermal Energy. Geothermal energy refers to the heat stored in the

rocks within the earth. In places where the earth’s heat flow is concentrated, this energy may be harnessed in the form of steam or hot water, which can subsequently be used for power generation. Geothermal energy is not entirely GHG emissions-free, but it emits far less greenhouse gases as compared to fossil fuel-based counterparts.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 18 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

5. Solar Energy. Solar radiation may be converted to electricity by using solar thermal engines or photovoltaic cells. Solar thermal engines make use of solar concentration systems, which, as the name implies, concentrates the power of the sun, to generate high enough temperatures to heat and boil water to drive steam engines. Photovoltaics, on the other hand, convert solar energy directly to electricity in a solid-state device called the solar cell.

• Clean coal technologies

Coal in itself is considered not a clean fuel because of the relatively high levels of carbon dioxide and pollutant emissions resulting from its combustion as compared with other fuels. Despite its unfavorable environmental reputation, coal is still widely used around the world for power generation because it is abundant and cheap. Various research and development efforts in the past three decades have been successful in coming up with technologies that give better efficiencies than the conventional pulverized coal technology or that convert coal into liquid or gas fuels. Many such technologies have been demonstrated in various countries but still remain not widely used because its high investment costs are quite prohibitive. These include fluidized bed systems such as pressurized fluidized bed combustion (PFBC) and circulating fluidized bed combustion (CFBC), integrated gasification combustion cycle (IGCC) systems and coal-fueled diesel engines. Clean coal technologies are costly, sometimes requiring around $3,000 per kilowatt of installed capacity.

• Gas turbines

Current gas turbine plants have efficiencies of around thirty percent. Newer plants are actually achieving efficiencies greater than forty percent. But since this type of plant is normally used for peak load applications, this would have a relatively low impact on emissions reduction.

• Fuel cells

Fuel cells are devices that convert fuel and oxygen to electricity and heat by means of an electrochemical reaction. For most fuel cells, hydrocarbon fuels need to undergo a process of reforming to produce hydrogen, which is the form of fuel required for the electrochemical reaction to take place. Fuel cells have efficiencies ranging from 40 to 60 percent and could achieve very negligible carbon and air pollutant emissions when paired with carbon separation technologies. Costs are prohibitive, however, ranging from $2,000 to $4,000 per installed kilowatt.

• Distributed energy technologies

Unlike centralized generating units, distributed energy technologies are small and modular, with sizes ranging from a few kilowatts to a few megawatts. Distributed energy technologies can be located on the site where the resource is available or near the place where the energy is to be used. Greater local control of the system and waste heat utilization lead to higher energy efficiencies, and thus, less GHG and air pollutant emissions.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 19 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Distributed power units could be connected directly to consumers or to the transmission or distribution grid. These could provide standby generation and base load generation, peak shave, and provide waste heat (cogeneration). And because they are located near the load, transmission and distribution costs can be reduced. Technologies used for such applications include internal combustion engine-generators, fuel cells, turbine generators and renewable technologies like solar photovoltaics, wind turbines and microturbines. Through a process called gasification, biomass fuels could also be used for distributed generation to produce a gaseous fuel that can be burned in diesel- or gas motors or in gas turbines.

• Improved fossil fuel-based technologies

Aside from clean coal technologies, newer and more efficient versions of conventional fossil fuel-based technologies have been and are being developed and designed.

• Natural gas technologies

Natural gas is a fossil fuel that has clean burning properties and lower CO2 emissions as compared to other fuels. Natural gas could be used to fuel a number of power generating technologies, including combined cycle gas turbines and fuel cells. Some of these technologies, particularly combined cycle gas turbines, have investment costs that are competitive with other conventional power generation technologies.

Measures that Integrate Carbon Sequestration Carbon sequestration involves the capturing of carbon dioxide in the atmosphere or keeping it from reaching the atmosphere. For the power sector, devices for carbon sequestration use the process of adsorption of carbon dioxide on materials like activated carbon, zeolites or inorganic membranes. Employing such devices in power generation facilities would require significant capital cost and may thus increase the cost of electricity.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 20 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

2.2 Resource Assessment The technologies described above would be rendered useless without the energy resource required to run them. The following sections will quantify the amount of clean energy resources in the Philippines, which will then be subsequently used for the generation of power switching scenarios. Wind Power The wind resource analysis and mapping study for the Philippine archipelago conducted by the National Renewable Energy Laboratory (NREL) shows that the country has plentiful wind electric potential. The NREL study identified around 10,000 sites in the country, occupying a total area of 11,055 km2 or roughly 3.34% of total Philippine land area, with good to excellent resource levels - equivalent to an annual average wind power of 300 W/m2 or greater12 (wind speeds of 6.4 m/s or greater). According to the study13, these sites could support at least 76,600 MW of installed capacity and generate 195,200 GWh/yr. Including sites with moderate wind resource levels, amounting to 97,000 installed capacity, would more than double total installed capacity to 173,600 MW bringing the total estimated power generation from wind to 361,000 GWh/yr. The study, however, was not able to include factors such as transmission and grid accessibility constraints in the assessment. The NREL study identified six regions in the country where the best wind resource in the country are located. These are:

1. the Batanes and Babuyan islands of north Luzon;

2. the northwest tip of Luzon (Ilocos Norte);

3. the higher interior terrain of Luzon, Mindoro, Samar, Leyte, Panay, Negros, Cebu, Palawan, eastern Mindanao, and adjacent islands;

4. well-exposed east-facing coastal locations from northern Luzon southward to Samar;

5. the wind corridors between Luzon and Mindoro (including Lubang Island);

6. between Mindoro and Panay (including the Semirara Islands and extending to the Cuyo Islands).

In contrast to the optimistic estimate of the NREL, an earlier study by the United Nations Industrial Development Organization (UNIDO) in 1994 puts the wind electric power potential for the entire Philippines at a very conservative value of 250 MW14.

12 In one of the NREL scenarios, areas with annual wind power densities of 300 W/m2 or greater were assumed to have sufficient potential for the economic development of utility-scale wind energy. 13 Assumptions used by NREL to come up with estimates are: 500 kW turbine size, hub height = 40 m, rotor diameter = 38 m, turbine spacing = 10D by 5D, capacity/km2 = 6.9 MW. 14 UNIDO, Assessment of Technical, Financial and Economic Implications of Wind Energy Applications for Power Generation, (1994).

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 21 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

Despite the vastness of wind resources in the country, current utilization are mostly to run wind pumps and a few small-scale turbine generators. At present, there are more than 500 wind pump and 9 wind turbine installations in the country. All wind turbine installations are of the stand-alone type, among which are the following:

1. A 10-kW system in Pagudpod, Ilocos Norte in Luzon. This is a pilot project of the National Power Corporation to electrify a number of households. It was commissioned in 1996.

2. A 25-kW stand-alone system in Picnic Grove, Tagaytay, Batangas in Luzon.

3. A 3-kW system in Bantay, Ilocos Sur in Luzon. In tandem with a diesel generator, this system is used to power up a relay station of the Philippine Telegraph and Telecommunications Company (PT & T). It is in operation since 1994.

4. A 25-kW system in General Santos in Mindanao. Two committed wind projects are expected to contribute a significant amount of electricity to grid. These are the 40-MW North Luzon Wind Power Project (NLWPP) of the Philippine National Oil Company-Energy Development Corporation (PNOC-EDC) and the 25-MW wind project of Northwind, which are scheduled for commissioning in 2006 and 2004, respectively. These wind facilities will both be located in Ilocos Norte. Proponents of these projects were able to secure power purchase agreements with the local distribution utility, which they used to obtain financing. Further, project proponents were able to obtain very lenient and attractive financing schemes. The PNOC-EDC project was given a soft loan amounting to $48 million dollars by the Japan Bank for International Cooperation (JBIC) at annual interests below 1 percent (0.95 percent for goods, 0.75 percent for consulting services) and a 40-year repayment period (inclusive of a 10-year grace period). Project proponents claim that they will be able to sell electricity at prices below that of the grid. It is significant to note two issues that developers of these two wind power projects had to address. First is the absence of site-specific wind assessment data, which required the developers to collect at least two-years of wind speed measurements. Second is the connection of the wind farms to the transmission grid. Transmission facilities are quite far from the wind sites, that for the NLWPP, that the PNOC-EDC was required to put up 42 kilometers of transmission line and 130 transmission line towers/poles to connect to the nearest transmission line trunk.

POWER SWITCH! Scenarios and Strategies for Clean Power Development in the Philippines

University of the Philippines Solar Laboratory page 22 Kabang Kalikasan ng Pilipinas, Inc. UPEEE Foundation

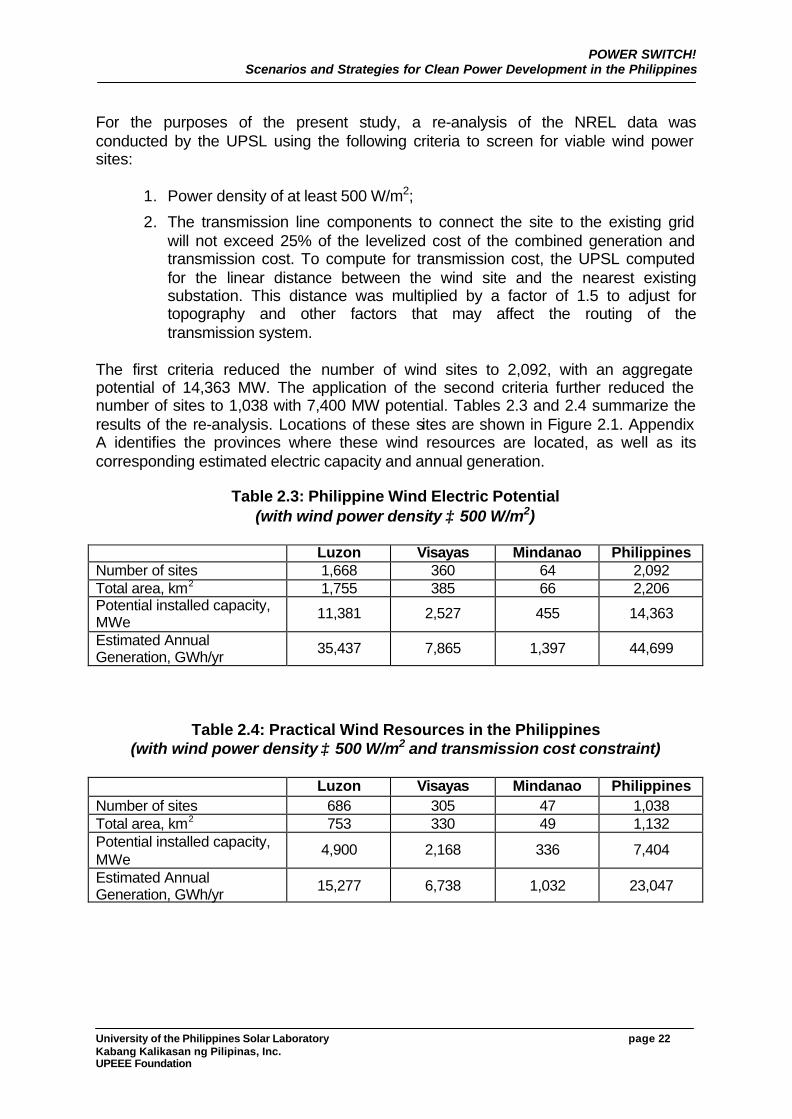

For the purposes of the present study, a re-analysis of the NREL data was conducted by the UPSL using the following criteria to screen for viable wind power sites:

1. Power density of at least 500 W/m2;