Embed Size (px)

Citation preview

Der Weltwirtschaft zu stärkerem Wachstum verhelfen – Die Rolle

des Euro-Raums und Deutschlands

Christian Kastrop Direktor, Economics Department

24th November 2014 OECD Berlin Centre

OECD Economic Outlook

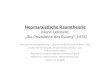

Das Wachstum der Weltwirtschaft bleibt verhalten

2

World GDP growth

Per cent, seasonally adjusted annualised rate

Source: November 2014 Economic Outlook database.

-8

-6

-4

-2

0

2

4

6

8

-8

-6

-4

-2

0

2

4

6

8

Average (1995-2007)

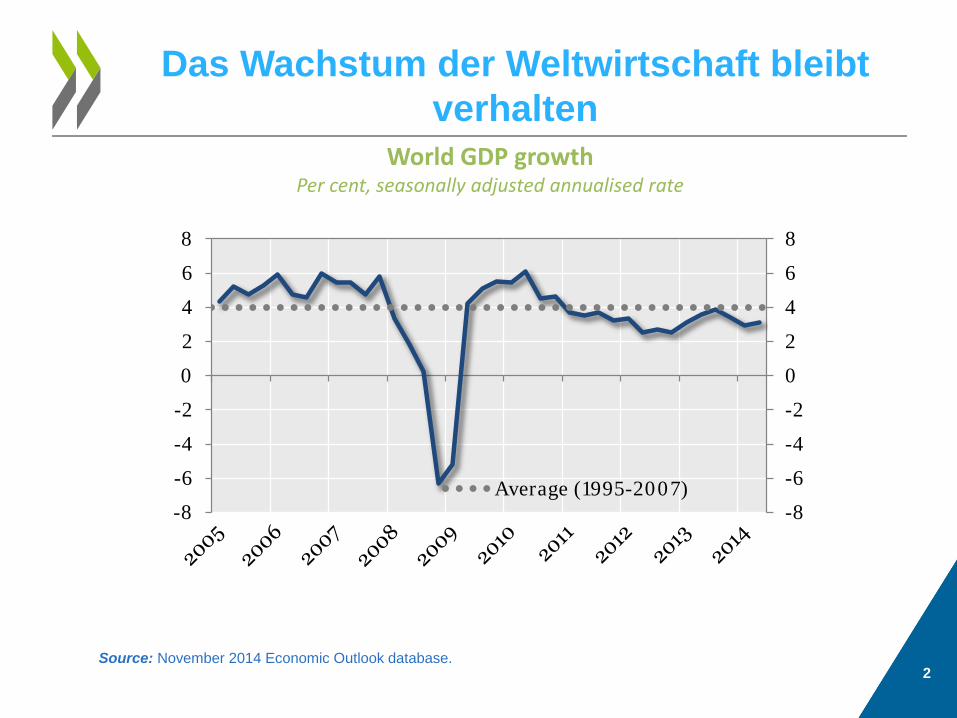

Der Außenhandel ist fast überall wenig gewachsen

3

Trade intensity1

Index, 1990=100

50

100

150

200

250

300

350United States

Trend (1990-2007)

50

100

150

200

250

300

350Japan

50

100

150

200

250

300

350European Union

50100150200250300350

BRIICS

1. Index of sum of exports and imports as a ratio of GDP. Source: November 2014 Economic Outlook database.

4

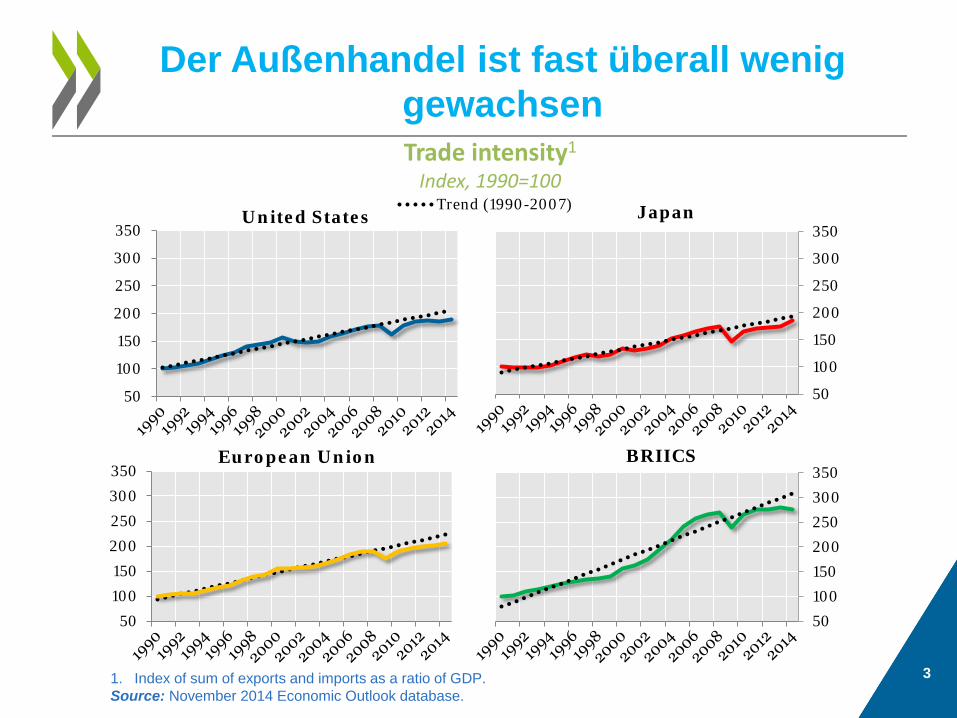

Die Nachfrage in den wichtigsten hoch entwickelten Volkswirtschaften entwickelt

sich unterschiedlich

.

Non-residential investment per capita

Index, 2005 = 100

Private consumption per capita

Index, 2005 = 100

80

90

100

110

120

80

90

100

110

120 United States Euro area Japan

85

90

95

100

105

110

115

85

90

95

100

105

110

115United States Euro area Japan

Source: OECD national accounts database; November 2014 Economic Outlook database; and OECD calculations.

5

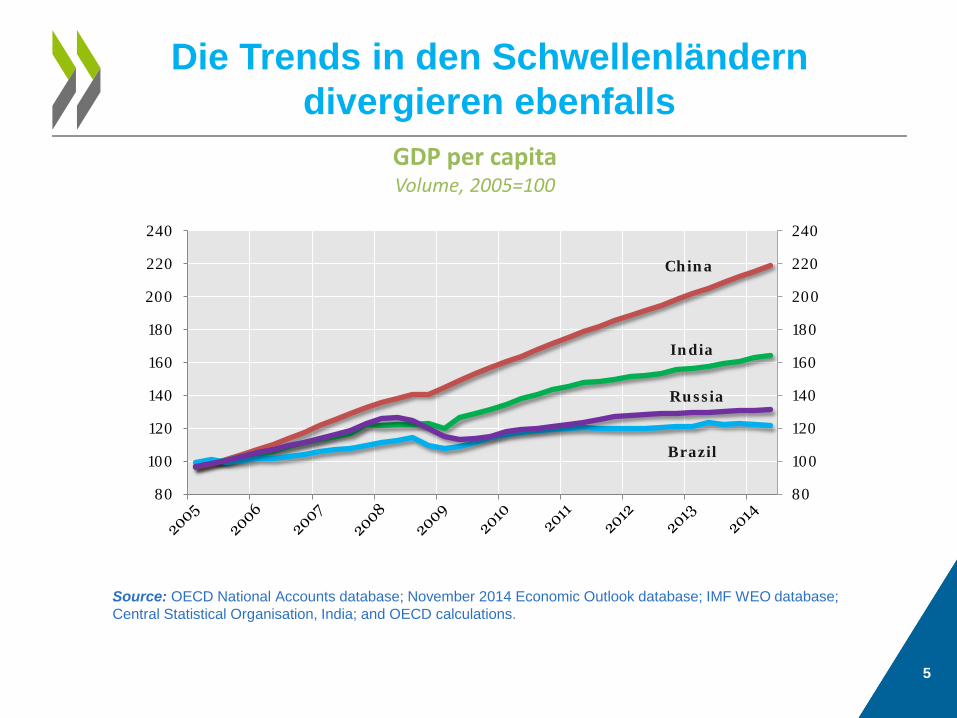

Die Trends in den Schwellenländern divergieren ebenfalls

.

GDP per capita Volume, 2005=100

80

100

120

140

160

180

200

220

240

80

100

120

140

160

180

200

220

240

China

India

Brazil

Russia

Source: OECD National Accounts database; November 2014 Economic Outlook database; IMF WEO database; Central Statistical Organisation, India; and OECD calculations.

Wachstumsprognosen für die Weltwirtschaft

GDP Volume, percentage change

6 Source: November 2014 Economic Outlook database.

Column1 2013 2014 2015 2016World 3.1 3.3 3.7 3.9

United States 2.2 2.2 3.1 3.0Euro area -0.4 0.8 1.1 1.7

Japan 1.5 0.4 0.8 1.0China 7.7 7.3 7.1 6.9India 4.7 5.4 6.4 6.6Brazil 2.5 0.3 1.5 2.0Russia 1.3 0.3 0.0 1.6

France 0.4 0.4 0.8 1.5Germany 0.2 1.5 1.1 1.8

Italy -1.9 -0.4 0.2 1.0United Kingdom 1.7 3.0 2.7 2.5

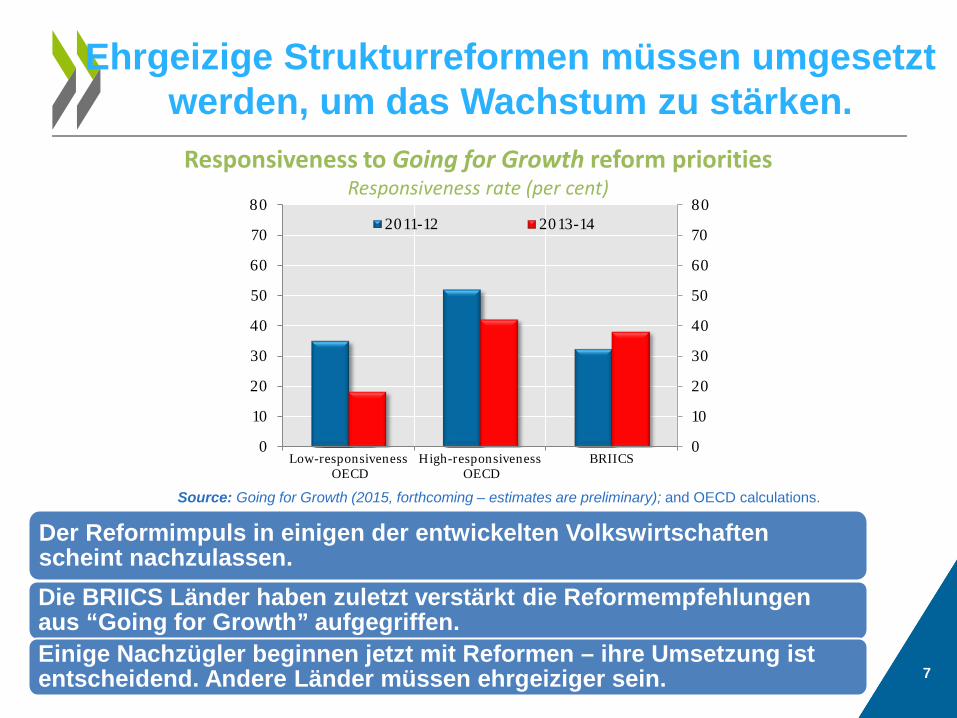

Ehrgeizige Strukturreformen müssen umgesetzt werden, um das Wachstum zu stärken.

Der Reformimpuls in einigen der entwickelten Volkswirtschaften scheint nachzulassen. Die BRIICS Länder haben zuletzt verstärkt die Reformempfehlungen aus “Going for Growth” aufgegriffen. Einige Nachzügler beginnen jetzt mit Reformen – ihre Umsetzung ist entscheidend. Andere Länder müssen ehrgeiziger sein. 7

Responsiveness to Going for Growth reform priorities Responsiveness rate (per cent)

Source: Going for Growth (2015, forthcoming – estimates are preliminary); and OECD calculations.

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

Low-responsiveness OECD

High-responsiveness OECD

BRIICS

2011-12 2013-14

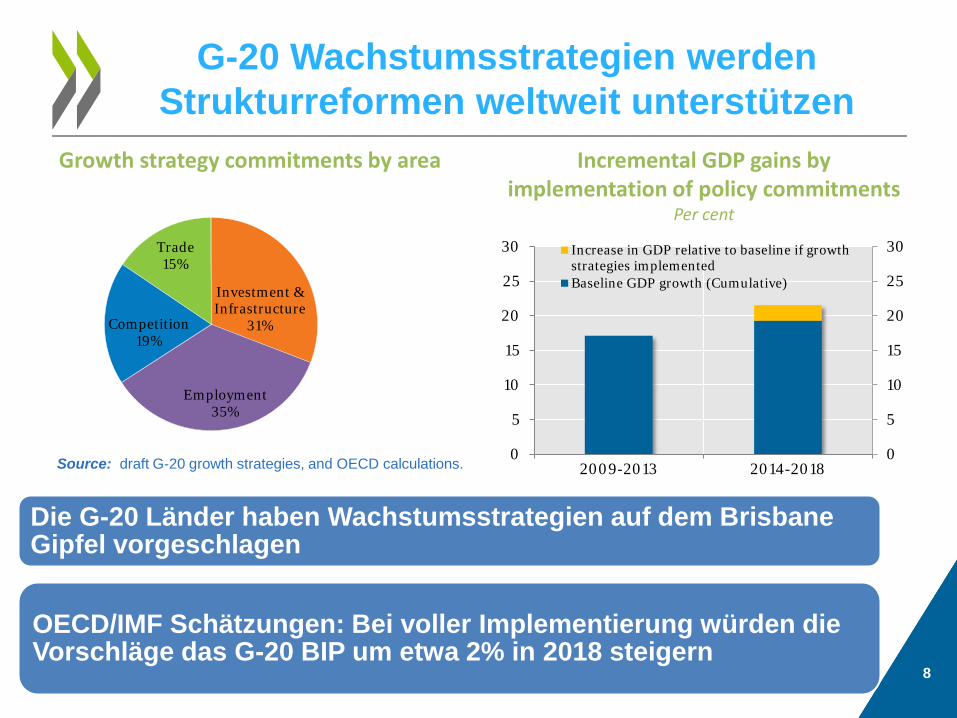

G-20 Wachstumsstrategien werden Strukturreformen weltweit unterstützen

Die G-20 Länder haben Wachstumsstrategien auf dem Brisbane Gipfel vorgeschlagen

OECD/IMF Schätzungen: Bei voller Implementierung würden die Vorschläge das G-20 BIP um etwa 2% in 2018 steigern

8

Incremental GDP gains by implementation of policy commitments

Per cent

Growth strategy commitments by area

Investment & Infrastructure

31%

Employment 35%

Competition 19%

Trade 15%

Source: draft G-20 growth strategies, and OECD calculations. 0

5

10

15

20

25

30

0

5

10

15

20

25

30

2009-2013 2014-2018

Increase in GDP relative to baseline if growthstrategies implementedBaseline GDP growth (Cumulative)

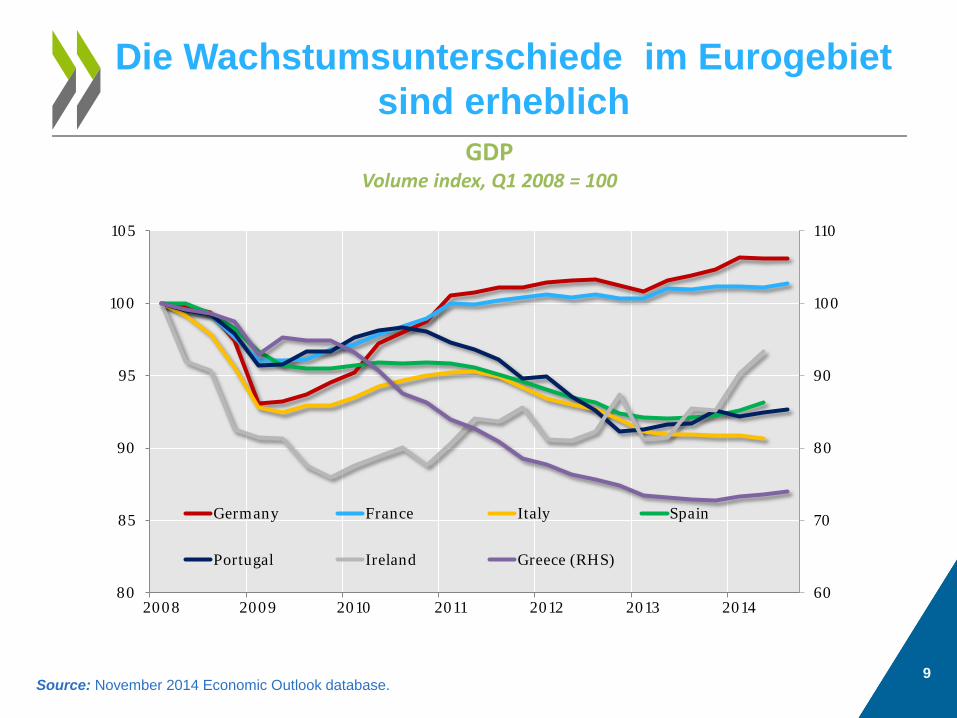

Die Wachstumsunterschiede im Eurogebiet sind erheblich

GDP Volume index, Q1 2008 = 100

Source: November 2014 Economic Outlook database. 9

60

70

80

90

100

110

80

85

90

95

100

105

2008 2009 2010 2011 2012 2013 2014

Germany France Italy Spain

Portugal Ireland Greece (RHS)

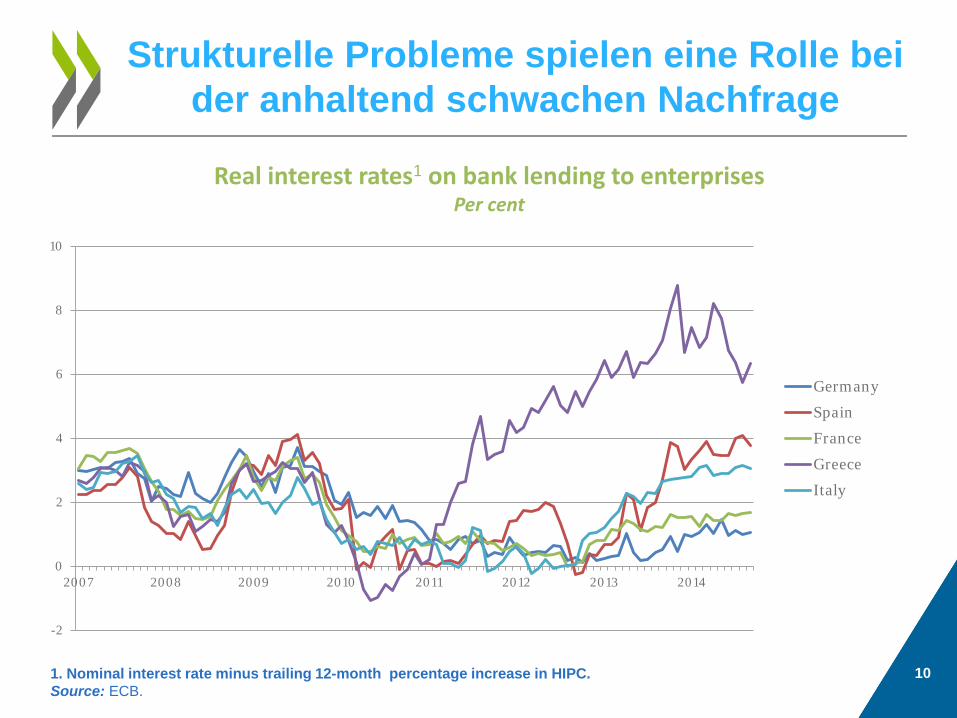

Strukturelle Probleme spielen eine Rolle bei der anhaltend schwachen Nachfrage

1. Nominal interest rate minus trailing 12-month percentage increase in HIPC. Source: ECB.

Real interest rates1 on bank lending to enterprises Per cent

10

-2

0

2

4

6

8

10

2007 2008 2009 2010 2011 2012 2013 2014

Germany

Spain

France

Greece

Italy

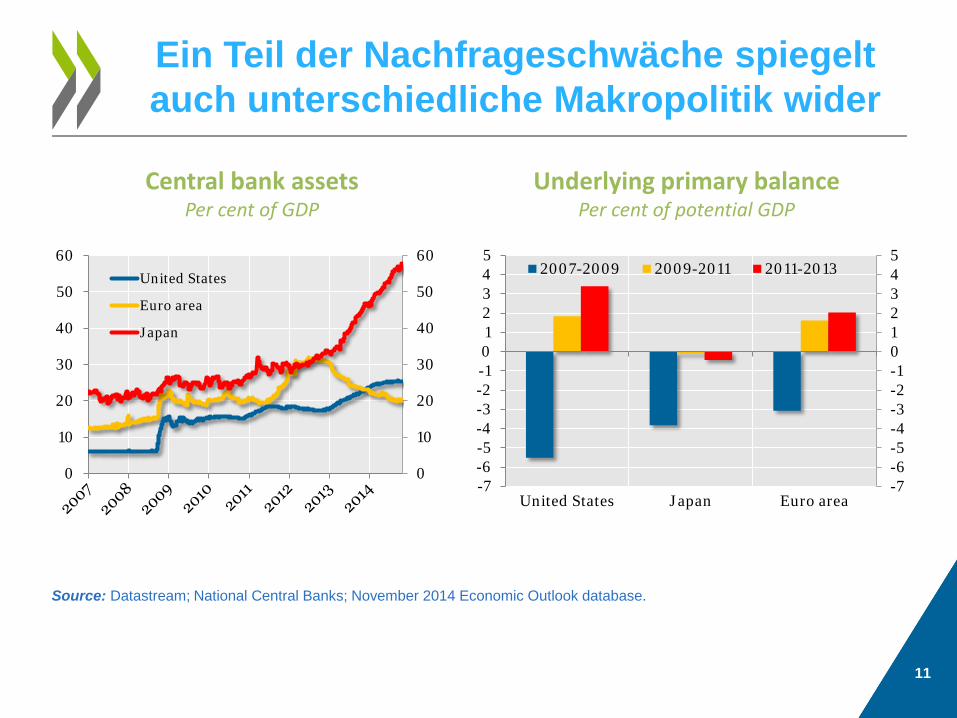

Ein Teil der Nachfrageschwäche spiegelt auch unterschiedliche Makropolitik wider

0

10

20

30

40

50

60

0

10

20

30

40

50

60United States

Euro area

Japan

Central bank assets Per cent of GDP

Source: Datastream; National Central Banks; November 2014 Economic Outlook database.

Underlying primary balance Per cent of potential GDP

11

-7-6-5-4-3-2-1012345

-7-6-5-4-3-2-1012345

United States Japan Euro area

2007-2009 2009-2011 2011-2013

Die Makropolitik unterstützt aber zunehmend die Nachfrage

ECB assets

Trillions of euros

Source: Datastream; November 2014 Economic Outlook database.

12

0

1

2

3

4ECB's target

0.0

0.5

1.0

1.5

0.0

0.5

1.0

1.5

2012 2013 2014 2015 2016

Change in the government underlying primary balance

Per cent of potential GDP

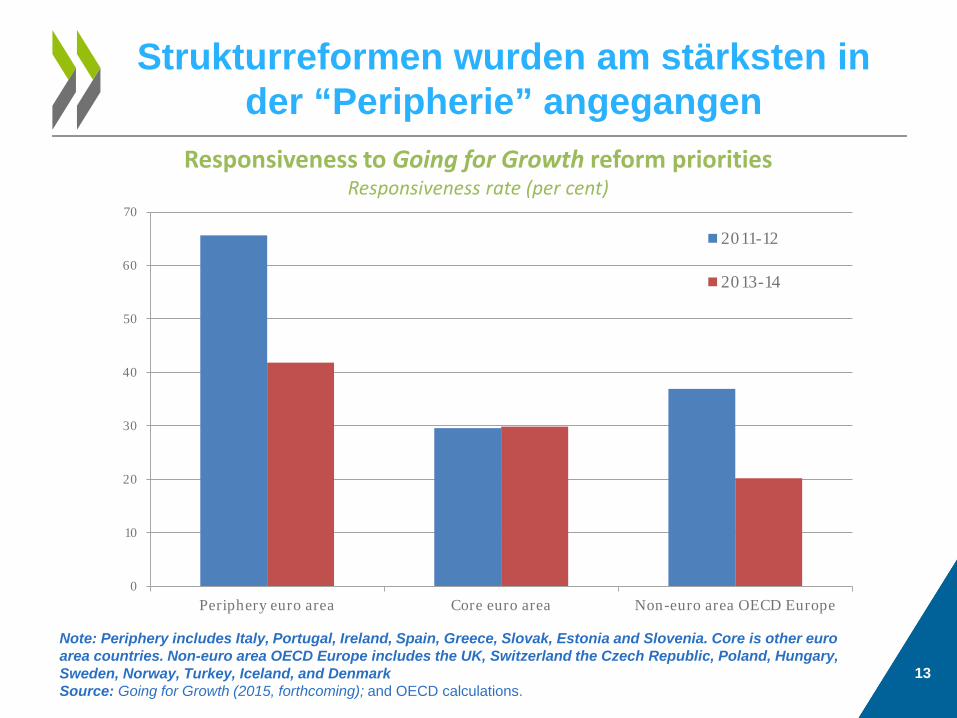

Strukturreformen wurden am stärksten in der “Peripherie” angegangen

0

10

20

30

40

50

60

70

Periphery euro area Core euro area Non-euro area OECD Europe

2011-12

2013-14

Note: Periphery includes Italy, Portugal, Ireland, Spain, Greece, Slovak, Estonia and Slovenia. Core is other euro area countries. Non-euro area OECD Europe includes the UK, Switzerland the Czech Republic, Poland, Hungary, Sweden, Norway, Turkey, Iceland, and Denmark Source: Going for Growth (2015, forthcoming); and OECD calculations.

Responsiveness to Going for Growth reform priorities Responsiveness rate (per cent)

13

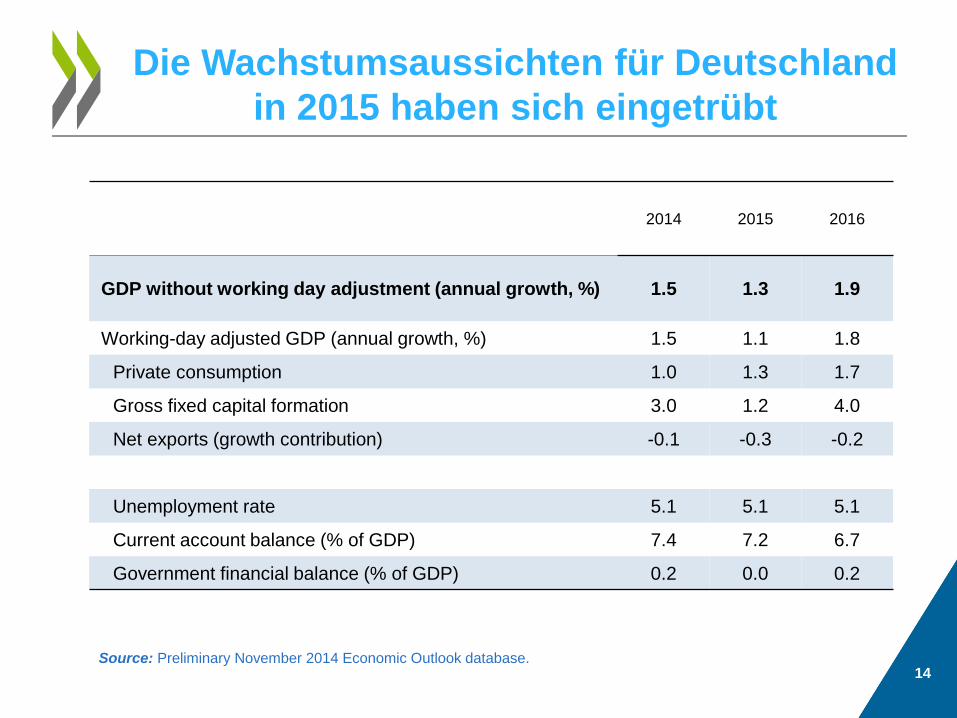

Die Wachstumsaussichten für Deutschland in 2015 haben sich eingetrübt

14 Source: Preliminary November 2014 Economic Outlook database.

2014 2015 2016

GDP without working day adjustment (annual growth, %) 1.5 1.3 1.9

Working-day adjusted GDP (annual growth, %) 1.5 1.1 1.8

Private consumption 1.0 1.3 1.7

Gross fixed capital formation 3.0 1.2 4.0

Net exports (growth contribution) -0.1 -0.3 -0.2

Unemployment rate 5.1 5.1 5.1

Current account balance (% of GDP) 7.4 7.2 6.7

Government financial balance (% of GDP) 0.2 0.0 0.2

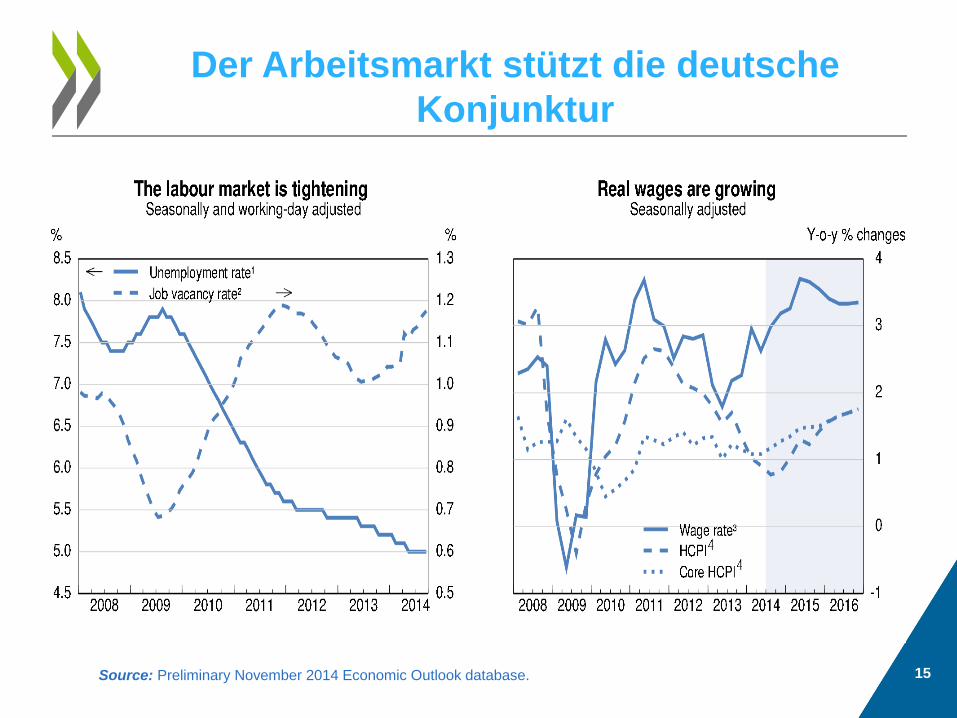

Der Arbeitsmarkt stützt die deutsche Konjunktur

15 Source: Preliminary November 2014 Economic Outlook database.

Wie sollte die deutsche Wirtschaftspolitik handeln?

16

Höhere Ausgaben für Kinderbetreuung und Verkehrsinfrastrukur sind nötig. Sie würden das Wachstumspotenzial in Deutschland erhöhen und die Konjunktur im Euroraum stützen.

Regulatorischer Hemmnisse im Dienstleistungssektor müssen reduziert werden. Das würde Investitionen stärken und das Wachstum in Deutschland auf eine breitere Basis stellen.

Wichtige Punkte

17

Staatseinnahmen und Ausgaben können wachstumsfreundlicher gemacht werden

Reduzierung der Besteuerung von Arbeit kann die Arbeitsnachfrage der Unternehmen erhöhen

Bankbilanzen sollten gestärkt werden

Die Makropolitik wird mehr unterstützend für die Nachfrage, aber wegen der Nachfrageschwäche sollte mehr getan werden

Strukturelle Faktoren für niedriges Potentialwachstum fallen zusammen mit Nachfrageschwäche, was das Risiko andauernder Stagnation erhöht

Geldpolitik, Fiskalpolitik und Strukturreformen sind komplementär zur Unterstützung des Aufschwungs

18

For further information

data visualization tool

OECD Economic Outlook, November 2014

• Website with additional information

• Read this publication online

• Compare your country with OECD data

www.oecd.org/eco/economicoutlook.htm

OECD OECD Economics

Disclaimers: The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.