Embed Size (px)

Citation preview

GESCHÄFTSBERICHT 2007ANNUAL REPORT 2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 1

WERTENTWICKLUNG 2007PERFORMANCE 2007

2

JAHRESBERICHT 2007

31.1

2.0

0

31.0

3.0

1

30.0

6.0

1

30.0

9.0

1

31.1

2.0

1

31.0

3.0

2

30.0

6.0

2

30.0

9.0

2

31.1

2.0

2

31.0

3.0

3

30.0

6.0

3

30.0

9.0

3

31.1

2.0

3

31.0

3.0

4

30.0

6.0

4

30.0

9.0

4

31.1

2.0

4

31.0

3.0

5

30.0

6.0

5

30.0

9.0

5

31.1

2.0

5

31.0

3.0

6

30.0

6.0

6

30.0

9.0

6

31.1

2.0

6

31.0

3.0

7

30.0

6.0

7

30.0

9.0

7

31.1

2.0

7

140%

130%

120%

110%

100%

90%

80%

70%

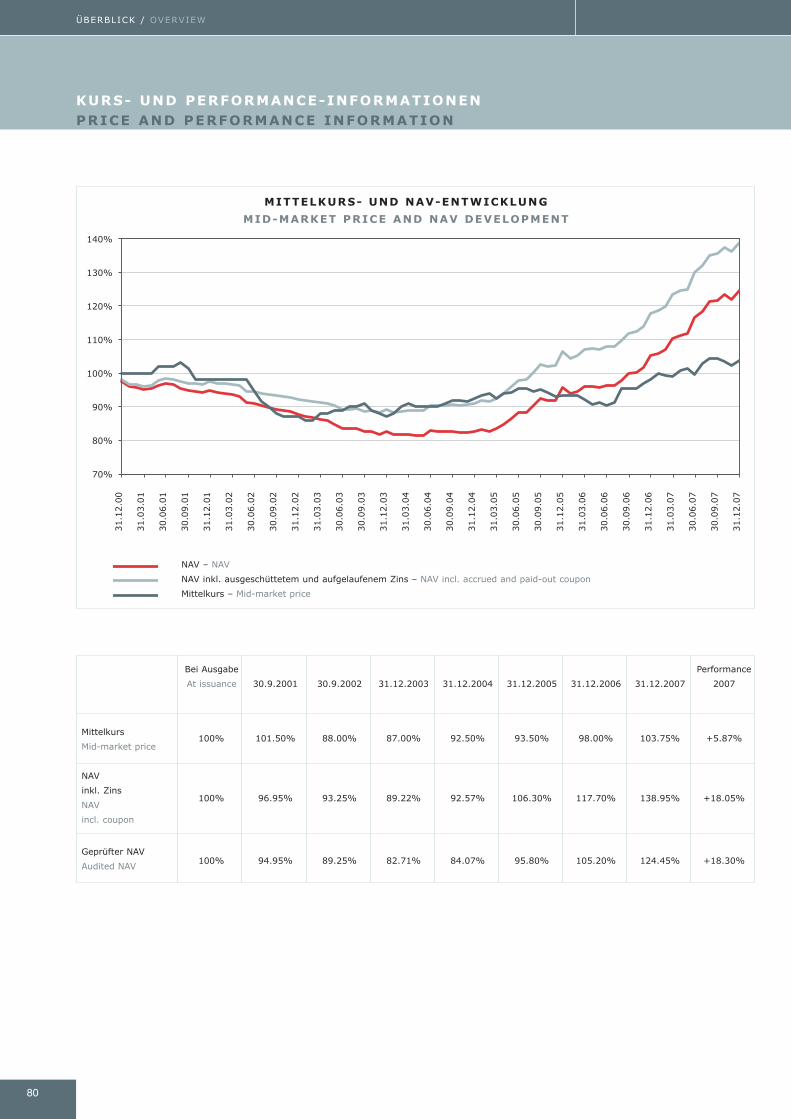

MITTELKURS- UND NAV-ENTWICKLUNG

MID-MARKET PRICE AND NAV DEVELOPMENT

NAV – NAV

NAV inkl. ausgeschüttetem und aufgelaufenem Zins – NAV incl. accrued and paid-out coupon

Mittelkurs – Mid-market price

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 2

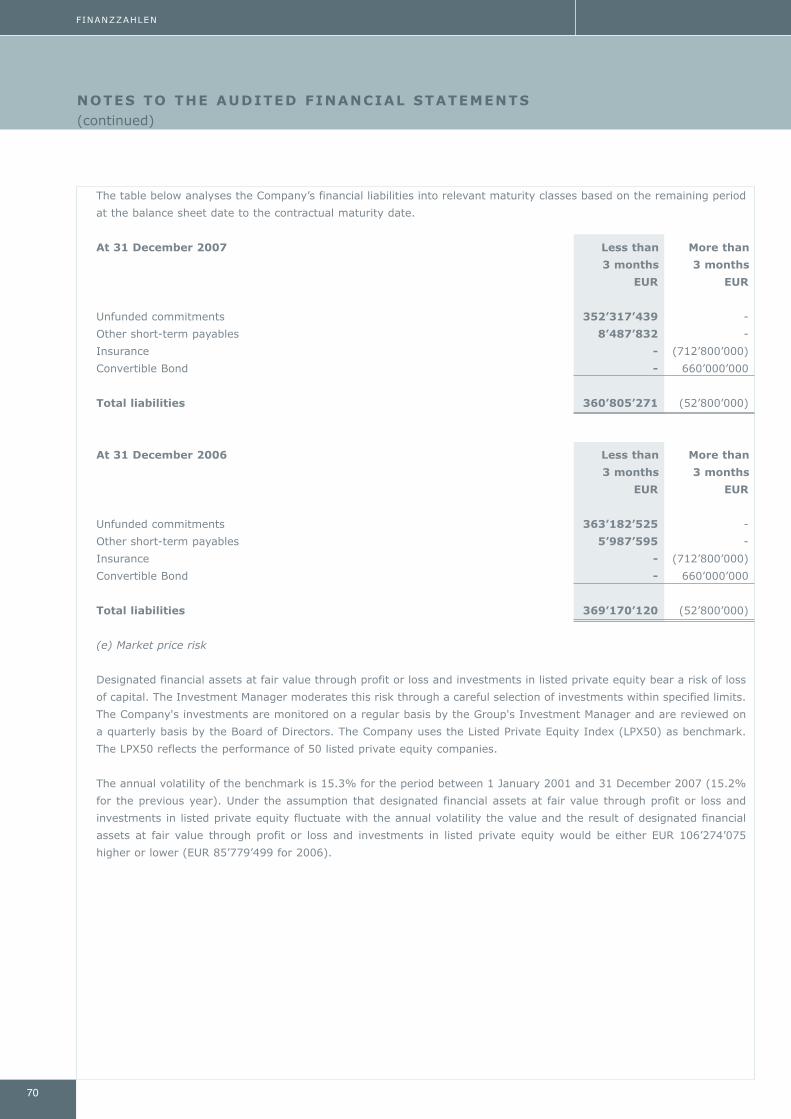

31.12.2007 31.12.2006

124.45% 105.20%

14.50% 12.50%

138.95% 117.70%

103.75% 98.00%

-16.63% -6.84%

EUR 126’809’816 EUR 129’998’324

EUR 694’601’797 EUR 564’338’811

EUR 352’317’439 EUR 363’182’525

84.56% 81.28%

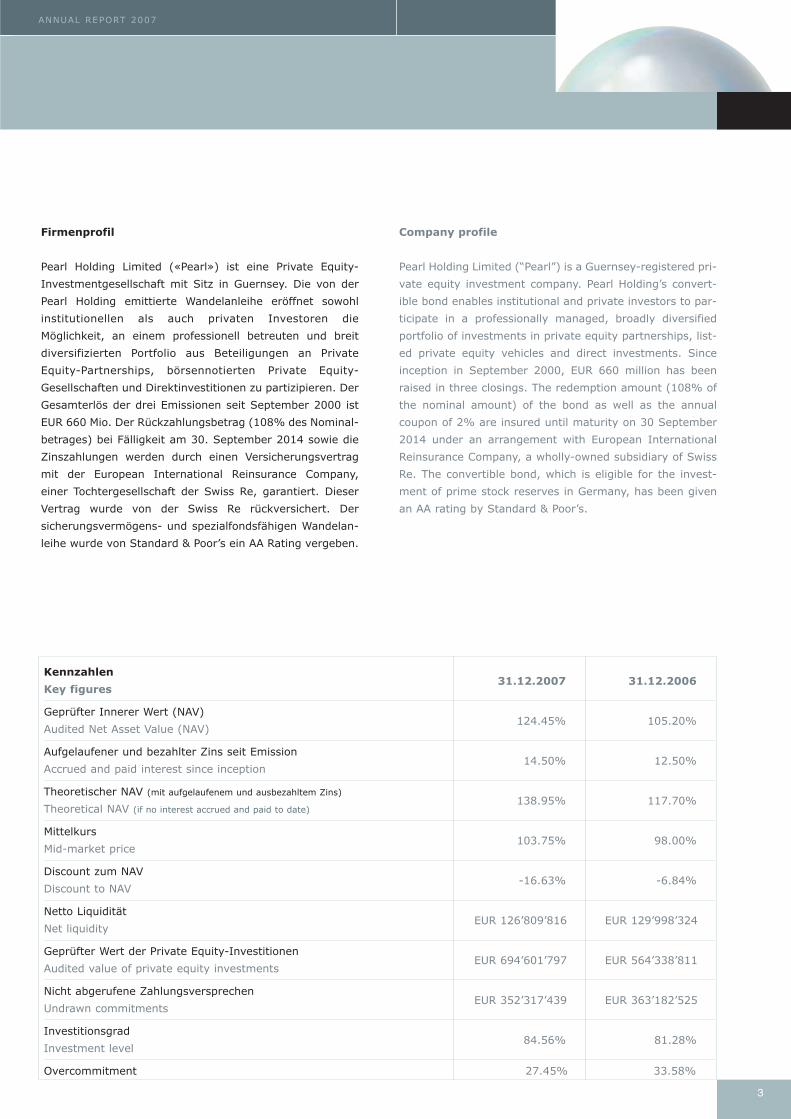

Kennzahlen

Key figures

Geprüfter Innerer Wert (NAV)

Audited Net Asset Value (NAV)

Aufgelaufener und bezahlter Zins seit Emission

Accrued and paid interest since inception

Theoretischer NAV (mit aufgelaufenem und ausbezahltem Zins)

Theoretical NAV (if no interest accrued and paid to date)

Mittelkurs

Mid-market price

Discount zum NAV

Discount to NAV

Netto Liquidität

Net liquidity

Geprüfter Wert der Private Equity-Investitionen

Audited value of private equity investments

Nicht abgerufene Zahlungsversprechen

Undrawn commitments

Investitionsgrad

Investment level

Overcommitment 27.45% 33.58%

3

ANNUAL REPORT 2007

Firmenprofil

Pearl Holding Limited («Pearl») ist eine Private Equity-

Investmentgesellschaft mit Sitz in Guernsey. Die von der

Pearl Holding emittierte Wandelanleihe eröffnet sowohl

institutionellen als auch privaten Investoren die

Möglichkeit, an einem professionell betreuten und breit

diversifizierten Portfolio aus Beteiligungen an Private

Equity-Partnerships, börsennotierten Private Equity-

Gesellschaften und Direktinvestitionen zu partizipieren. Der

Gesamterlös der drei Emissionen seit September 2000 ist

EUR 660 Mio. Der Rückzahlungsbetrag (108% des Nominal-

betrages) bei Fälligkeit am 30. September 2014 sowie die

Zinszahlungen werden durch einen Versicherungsvertrag

mit der European International Reinsurance Company,

einer Tochtergesellschaft der Swiss Re, garantiert. Dieser

Vertrag wurde von der Swiss Re rückversichert. Der

sicherungsvermögens- und spezialfondsfähigen Wandelan-

leihe wurde von Standard & Poor’s ein AA Rating vergeben.

Company profile

Pearl Holding Limited (“Pearl”) is a Guernsey-registered pri-

vate equity investment company. Pearl Holding’s convert-

ible bond enables institutional and private investors to par-

ticipate in a professionally managed, broadly diversified

portfolio of investments in private equity partnerships, list-

ed private equity vehicles and direct investments. Since

inception in September 2000, EUR 660 million has been

raised in three closings. The redemption amount (108% of

the nominal amount) of the bond as well as the annual

coupon of 2% are insured until maturity on 30 September

2014 under an arrangement with European International

Reinsurance Company, a wholly-owned subsidiary of Swiss

Re. The convertible bond, which is eligible for the invest-

ment of prime stock reserves in Germany, has been given

an AA rating by Standard & Poor’s.

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 3

INHALTSVERZEICHNISTABLE OF CONTENTS

4

JAHRESBERICHT 2007

Dieses Dokument ist nicht als Anlagewerbung oder Verkaufsprospekt gedacht und stellt weder eine Offerte noch den

Versuch der Aufforderung zur Offertenstellung für das hier beschriebene Produkt dar. Dieser Bericht wurde unter

Verwendung von Finanzdaten erstellt, die den Büchern und sonstigen Aufzeichnungen des Unternehmens per

Berichtsdatum entnommen wurden. Die im Bericht der Vermögensverwaltungsgesellschaft im Einzelnen aufgeführ-

ten Grafiken und Zahlen wurden nicht geprüft. In diesem Bericht wird die bisherige Performance beschrieben, die

nicht unbedingt ein Indikator für künftige Ergebnisse sein muss. Die Haftung des Unternehmens für Handlungen,

die auf der Grundlage der zur Verfügung gestellten Informationen vorgenommen werden, ist ausgeschlossen.

Wertentwicklung 2007 Seite 2

Daten und Fakten Seite 6

Pearl Holding Limited Seite 7

Vorwort des Verwaltungsrates Seite 8

Vereinfachte Strukturdarstellung Seite 11

Bericht des Investment Managers Seite 13

Rückblick auf die Private Equity-Industrie 2007 Seite 14

Wertentwicklung des Pearl-Portfolios Seite 23

Investitionsverlauf Seite 25

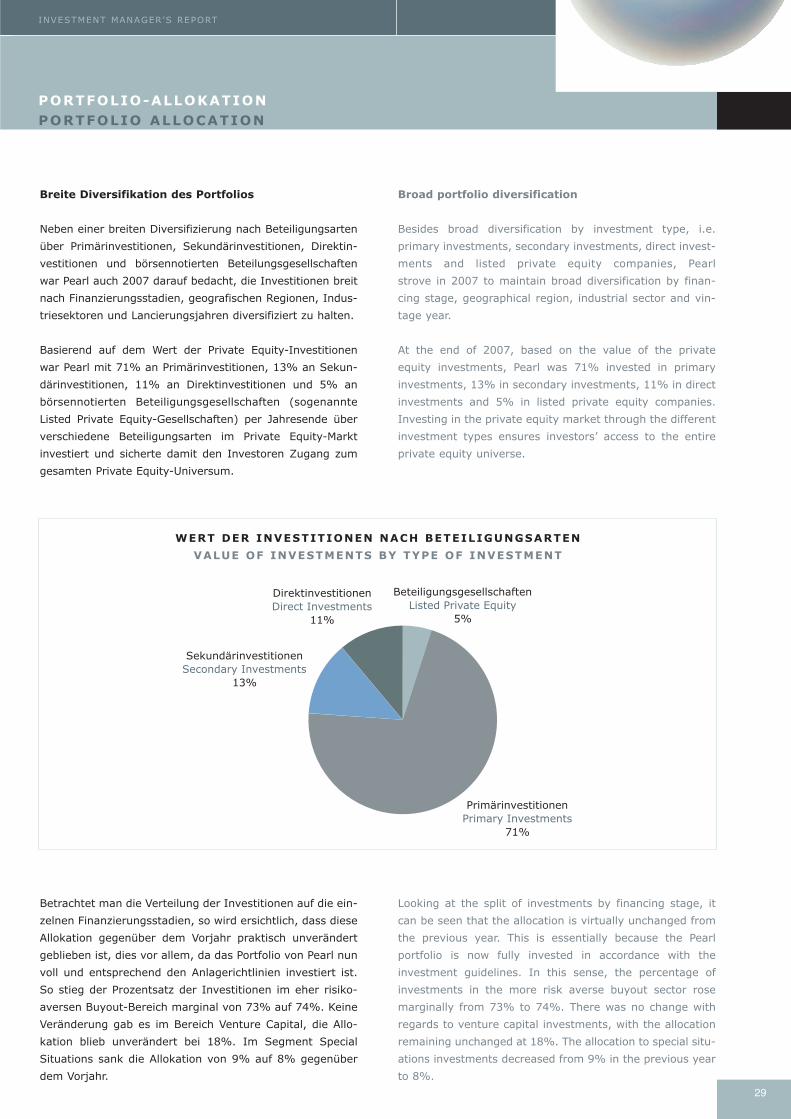

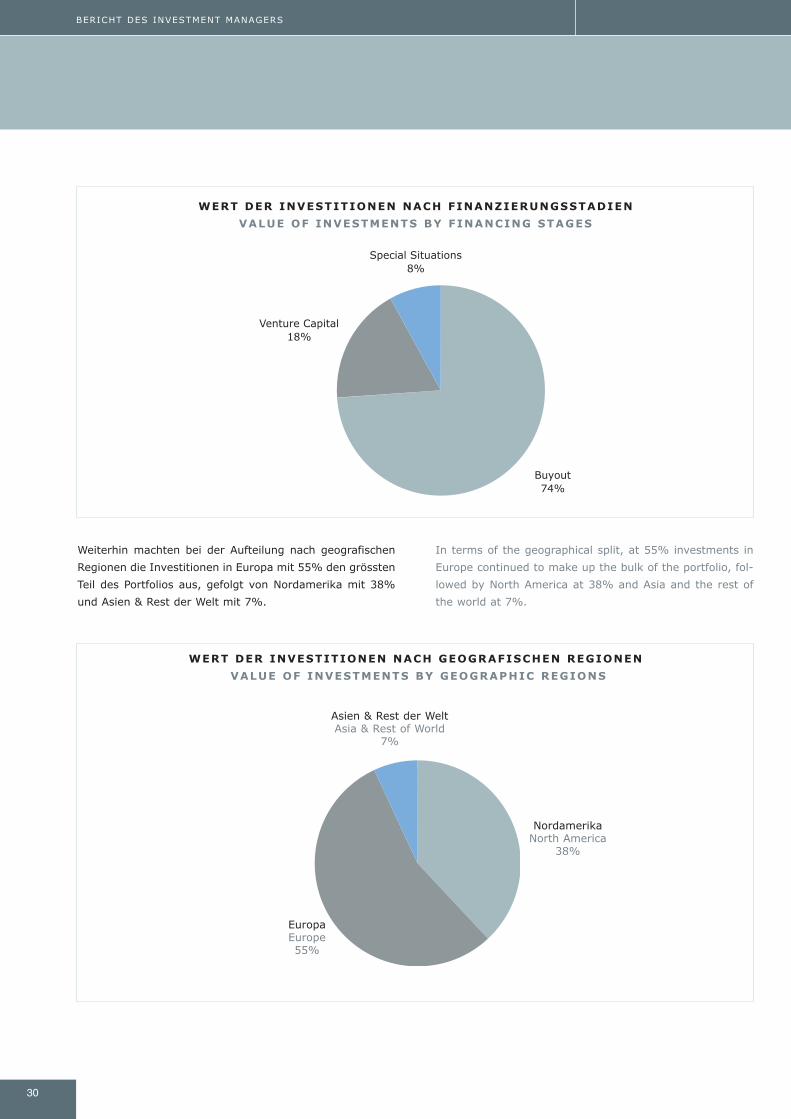

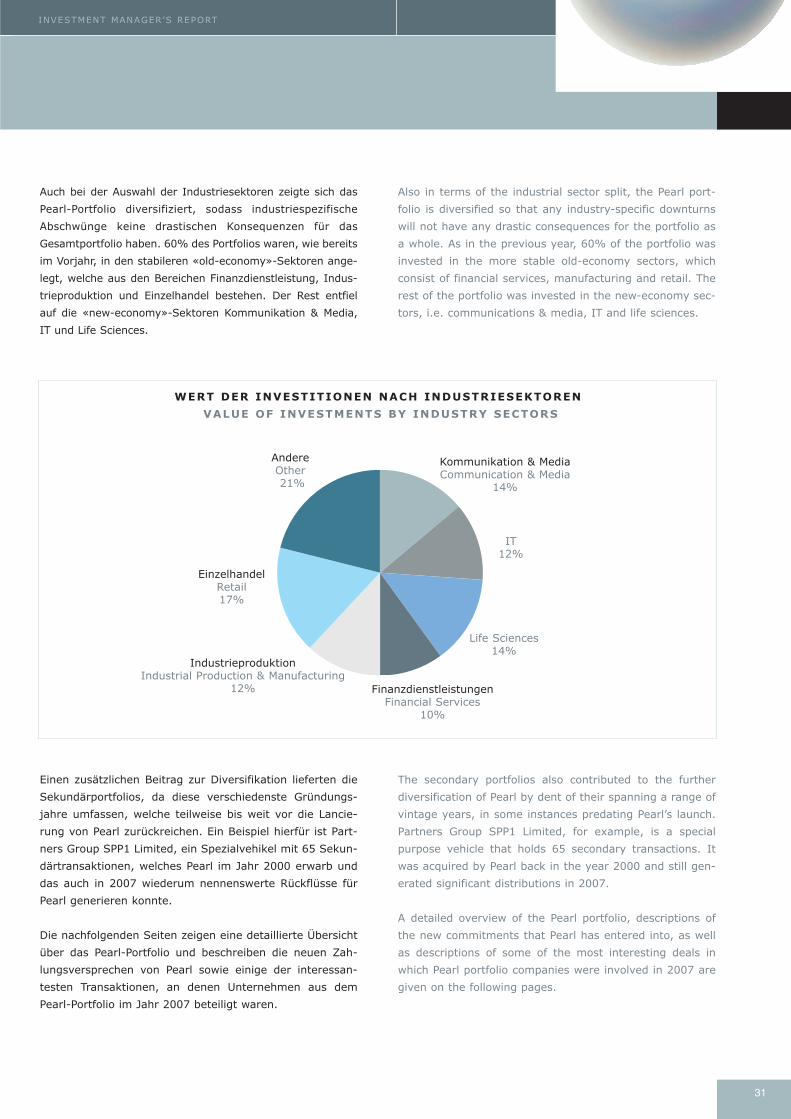

Portfolio-Allokation Seite 29

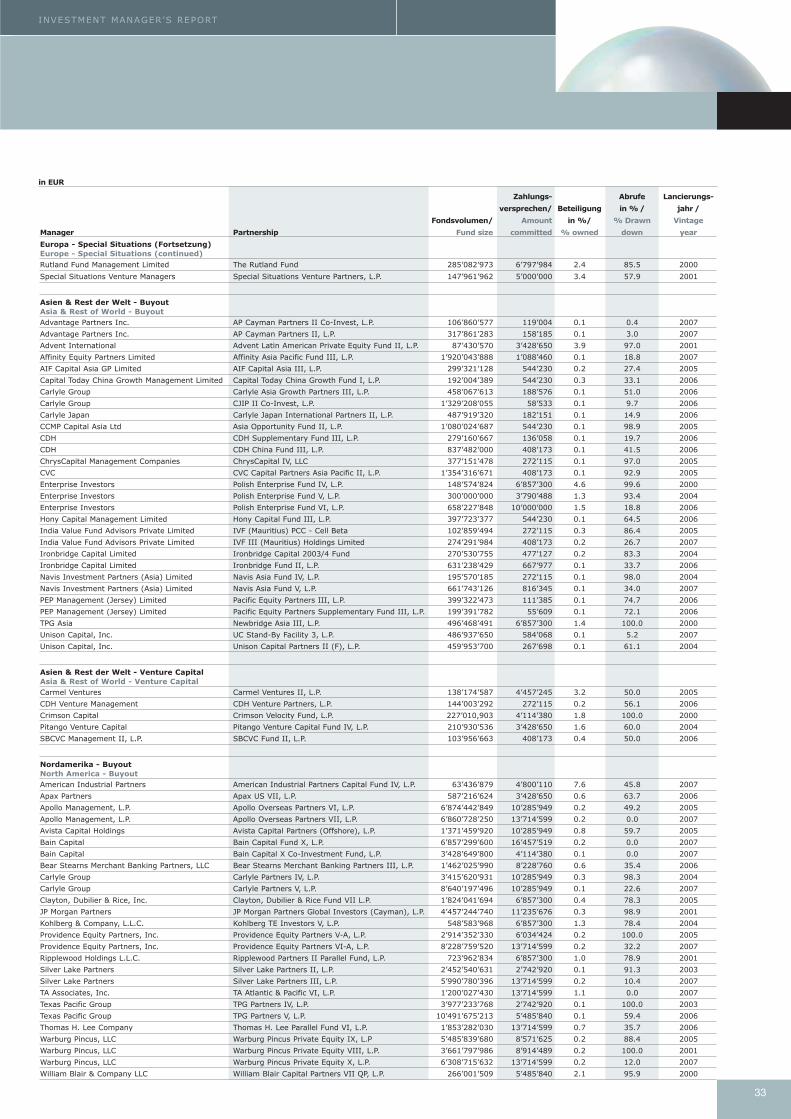

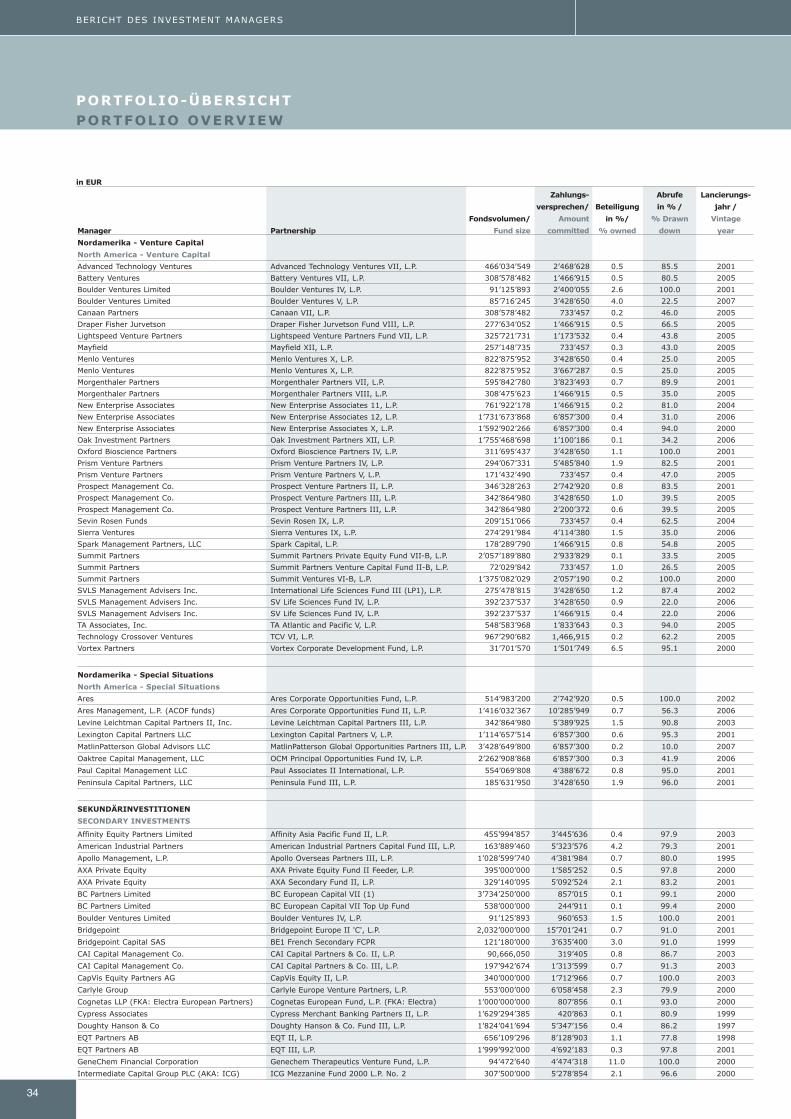

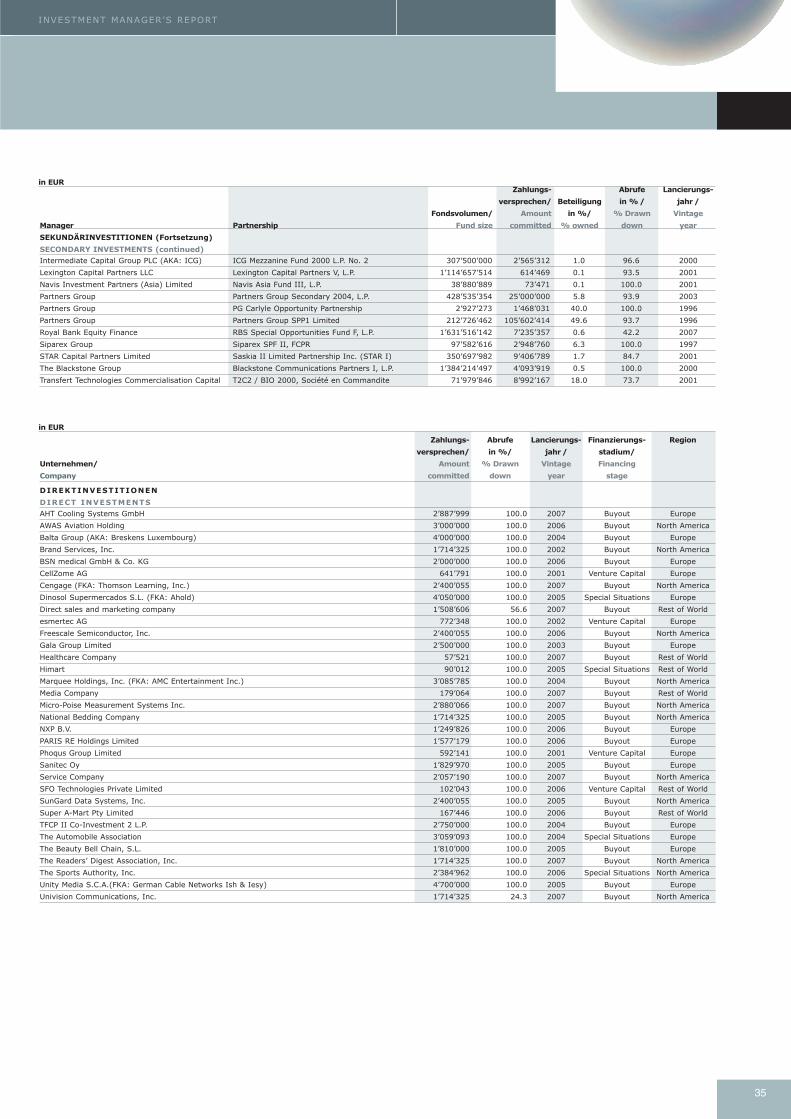

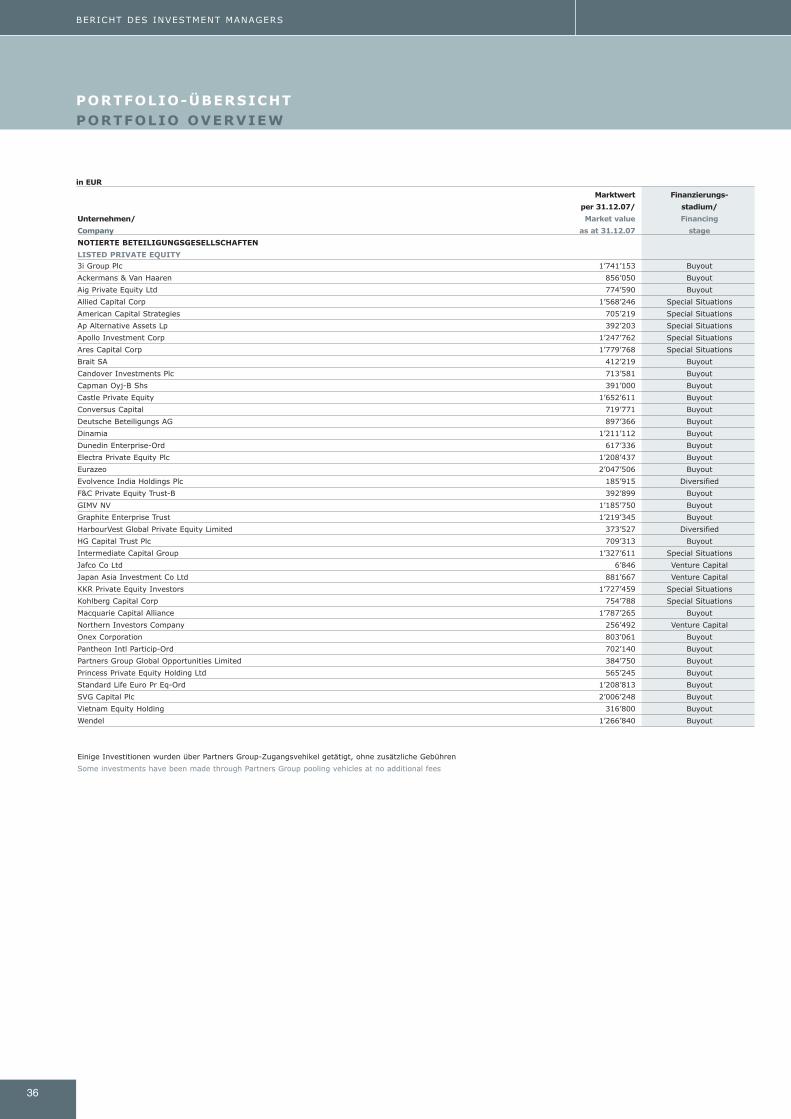

Portfolio-Übersicht Seite 32

Neue Zahlungsversprechen Seite 37

Neue Direktinvestitionen Seite 42

Ausgewählte Investitionen der Partnerships Seite 44

Ausgewählte Realisierungen Seite 47

Ausblick auf das Jahr 2008 Seite 50

Ausblick 2008 für Pearl Seite 53

Finanzzahlen Seite 55

Bericht des Wirtschaftsprüfers Seite 58

Finanzzahlen Seite 59

Kurs- und Performance-Informationen Seite 80

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 4

5

ANNUAL REPORT 2007

This document is not intended to be an investment advertisement or sales instrument; it constitutes neither an

offer nor an attempt to solicit offers for the product described herein. This report was prepared using financial

information contained in the company's books and records as of the reporting date. The charts and figures de-

tailed in the Investment Manager’s Report have not been audited. This report describes past performance, which

may not be indicative of future results. The company does not accept any liability for actions taken on the basis

of the information provided.

Performance 2007 Page 2

Facts and Figures Page 6

Pearl Holding Limited Page 7

Statement of the Board of Directors Page 8

Simplified Structural Overview Page 11

Investment Manager’s Report Page 13

Review on the Private Equity Industry in 2007 Page 14

Performance of the Pearl Portfolio Page 23

Investment Activity Page 25

Portfolio Allocation Page 29

Portfolio Overview Page 32

New Commitments to Partnerships Page 37

New Direct Investments Page 42

Selected Investments by Partnerships Page 44

Selected Portfolio Realizations Page 47

Outlook for 2008 Page 50

Outlook for 2008 for Pearl Page 53

Financial Figures Page 55

Auditor’s Statement Page 58

Financial Figures Page 59

Price and Performance Information Page 80

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 5

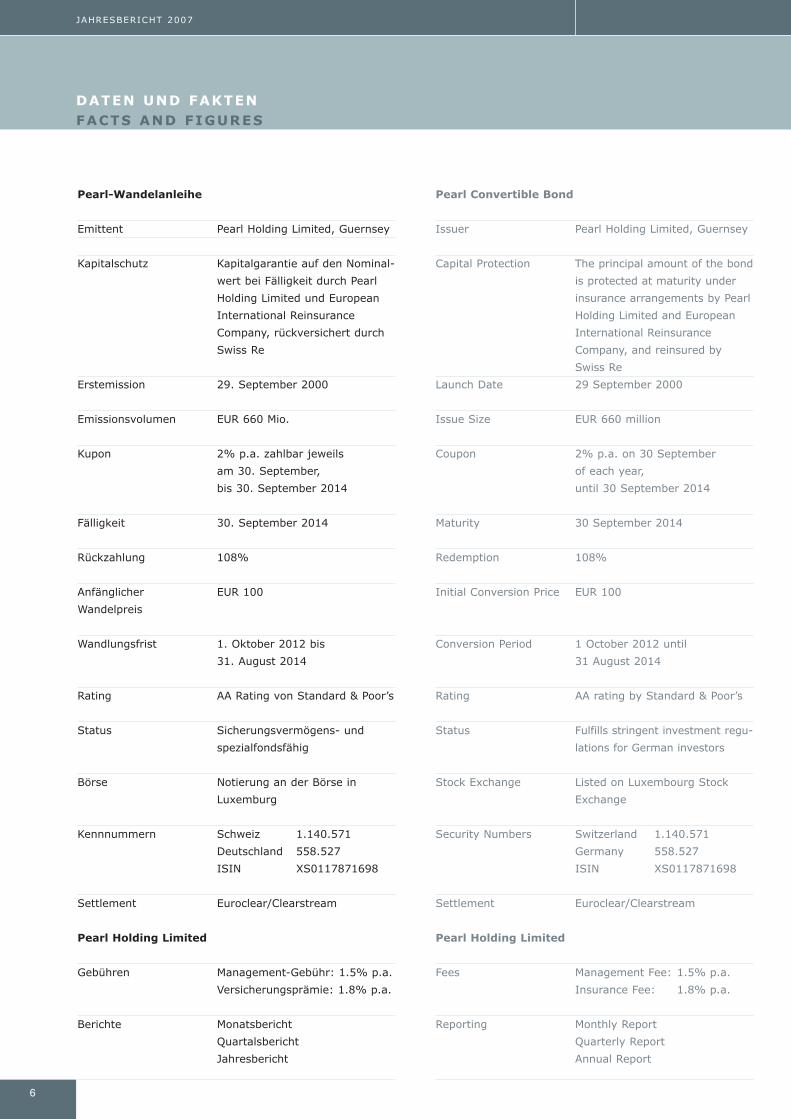

DATEN UND FAKTENFACTS AND FIGURES

6

Pearl Convertible Bond

Issuer Pearl Holding Limited, Guernsey

Capital Protection The principal amount of the bond

is protected at maturity under

insurance arrangements by Pearl

Holding Limited and European

International Reinsurance

Company, and reinsured by

Swiss Re

Launch Date 29 September 2000

Issue Size EUR 660 million

Coupon 2% p.a. on 30 September

of each year,

until 30 September 2014

Maturity 30 September 2014

Redemption 108%

Initial Conversion Price EUR 100

Conversion Period 1 October 2012 until

31 August 2014

Rating AA rating by Standard & Poor’s

Status Fulfills stringent investment regu-

lations for German investors

Stock Exchange Listed on Luxembourg Stock

Exchange

Security Numbers Switzerland 1.140.571

Germany 558.527

ISIN XS0117871698

Settlement Euroclear/Clearstream

Pearl Holding Limited

Fees Management Fee: 1.5% p.a.

Insurance Fee: 1.8% p.a.

Reporting Monthly Report

Quarterly Report

Annual Report

Pearl-Wandelanleihe

Emittent Pearl Holding Limited, Guernsey

Kapitalschutz Kapitalgarantie auf den Nominal-

wert bei Fälligkeit durch Pearl

Holding Limited und European

International Reinsurance

Company, rückversichert durch

Swiss Re

Erstemission 29. September 2000

Emissionsvolumen EUR 660 Mio.

Kupon 2% p.a. zahlbar jeweils

am 30. September,

bis 30. September 2014

Fälligkeit 30. September 2014

Rückzahlung 108%

Anfänglicher EUR 100

Wandelpreis

Wandlungsfrist 1. Oktober 2012 bis

31. August 2014

Rating AA Rating von Standard & Poor’s

Status Sicherungsvermögens- und

spezialfondsfähig

Börse Notierung an der Börse in

Luxemburg

Kennnummern Schweiz 1.140.571

Deutschland 558.527

ISIN XS0117871698

Settlement Euroclear/Clearstream

Pearl Holding Limited

Gebühren Management-Gebühr: 1.5% p.a.

Versicherungsprämie: 1.8% p.a.

Berichte Monatsbericht

Quartalsbericht

Jahresbericht

JAHRESBERICHT 2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 6

7

ANNUAL REPORT 2007

PEARL HOLDING LIMITED

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 7

Dear Valued Investors

After a promising start to the first half of the year - begin-

ning with the subprime crisis in the US, which evolved into

a global credit crisis - 2007 turned into one of the most

difficult years of the past decade. This was particularly

reflected in the equity markets, which sustained larger

losses at times than after the New York attacks in 2001. It

has ultimately led to fears that a material recession could

be on the cards for the US. Contrary to these fears, the

macroeconomic picture was positive in 2007 with an

economic growth rate of 5% that was primarily the result

of dynamic growth in the emerging countries and Europe.

Moreover, corporate balance sheets, with the exception of

credit institutions, were on the whole very solid, showing

that the negative effects of the events in the credit markets

had not had an impact at the corporate level.

Even though 2007 as a whole was one of the best years ever

for the private equity industry, the credit crisis was neverthe-

less felt in the buyout sector. In the first half of the year

industry headlines were dominated by multi-billion buyout

deals, but the situation changed in the second half of the year

due to the credit crisis. As a result of reduced liquidity, cheap

debt financing was no longer available for large takeovers and

deals could no longer be realized. However, increased activ ity

for small- and mid-sized deals could be observed. Both the

mezzanine and private equity secondary markets developed

contrary to the other markets and emerged as the winners of

the credit crisis. The former profited strongly from the rise in

risk premiums, which sharply raised the return expectations

for mezzanine financing, while the latter benefited from an

adjustment of prices in the secondary market.

In 2007, venture capital fundraising remained stable at the

previous year's level. Venture investing rose in the US, but

remained constant in Europe. On the exit front, the funds

profited from a rise in the volume of mergers and acquisi-

tions (M&As) as well as an increase in the number of initial

public offerings (IPOs). The listed private equity companies

could not escape from the turmoil in the stock markets

unscathed and faced a significant rise in volatility and at

times heavy share price losses.

Although market conditions were unfavorable at times, the

past financial year turned out to be a record year for Pearl.

The audited net asset value (NAV) climbed 18.30% to a

new all-time high of 124.45%, making it Pearl’s best

annual result since its inception. Inclusion of the 2%

coupon, which is paid out to the investors every Septem-

ber, yields a theoretical NAV of as much as 138.95%.

VORWORT DES VERWALTUNGSRATESSTATEMENT OF THE BOARD OF DIRECTORS

8

Sehr geehrte Investoren

Nachdem 2007 im ersten Halbjahr vielversprechend begann,

entwickelte es sich ausgehend von der Subprime-Krise in den

USA, die sich zu einer globalen Kreditkrise entfaltete, zu

einem der schwierigsten Jahre der letzten Dekade. Dies spie-

gelte sich besonders an den Aktienmärkten wider, die zeit-

weise grössere Verluste hinnehmen mussten als nach den

Anschlägen in New York in 2001. Letztendlich führte dies zu

der allgemeinen Befürchtung, die USA könne in eine nachhal-

tige Rezession verfallen. Entgegen dieser Befürchtungen prä-

sentierte sich das gesamtwirtschaftliche Bild 2007 mit einem

Wirtschaftswachstum von 5% positiv, was vor allem auf das

dynamische Wachstum in den Schwellenländern sowie in

Europa zurückzuführen ist. Da rüber hinaus erwiesen sich die

Bilanzen der Unternehmen, mit Ausnahme der Kreditinstitu-

te, im Grossen und Ganzen als sehr solide, was zeigte, dass

sich der negative Einfluss der Geschehnisse an den Kredit-

märkten nicht bis auf Unternehmensebene ausgewirkt hat.

Obwohl 2007 gesamthaft betrachtet für die Private Equity-

Industrie eines der besten Jahre war, so machte sich die

Kreditkrise im Buyout-Segment dennoch bemerkbar. Nach-

dem in der ersten Jahreshälfte zahlreiche Multi-Milliarden

Buyout-Transaktionen die Schlagzeilen der Branche prägten,

änderte sich die Lage in Folge der Kreditkrise in der zweiten

Jahreshälfte. Aufgrund der gesunkenen Liquidität stand für

grosse Übernahmen kein günstiges Fremdkapital mehr zur

Verfügung und die Deals waren nicht mehr realisierbar.

Allerdings waren nun verstärkte Aktivitäten bei kleinen und

mittelständischen Transaktionen zu beobachten. Sowohl der

Mezzanine- als auch der Private Equity-Sekundärmarkt ent-

wickelten sich konträr zu den sonstigen Märkten und gingen

als Gewinner aus der Kreditkrise hervor. Ersterer profitierte

stark vom Anstieg der Risiko prämien, welcher die Renditeer-

wartungen von Mezzanine-Finanzierungen in die Höhe trieb,

während sich für letzteren die Anpassung des Preisniveaus

auf dem Sekundärmarkt positiv auswirkte.

Der Venture Capital-Bereich hat sich bei der Mittelbeschaf-

fung im vergangenen Jahr recht stabil entwickelt und

bewegte sich auf dem Niveau des Vorjahres. Die Inves -

titionstätigkeiten verzeichneten in den USA einen Anstieg,

während sie in Europa konstant blieben. Auf der Exit-Seite

konnten die Fonds hingegen von einem Anstieg des Volu-

mens im Bereich Fusionen und Übernahmen sowie von

einer steigenden Anzahl bei den Börsengängen profitieren.

Die börsennotierten Private Equity-Unternehmen konnten

sich den Turbulenzen an den Aktienmärkten nicht entziehen

und hatten mit einem signifikanten Anstieg der Volatilität

und zeitweise starken Kursverlusten zu kämpfen.

PEARL HOLDING LIMITED

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 8

9

The highest ever recorded annual growth in the NAV was

primarily driven by revaluations of the partnerships during

the course of the year. The development of the buyout sec-

tor and the direct investments was particularly pleasing.

This positive development essentially reflects the advanced

level of maturity of the portfolio, as the underlying partner-

ships now in the post-investment period are exiting their

investments, realizing the profits and distributing the pro-

ceeds to the investors. Thanks to these revaluations, the

falls in the share prices of the listed private equity com-

panies that had been triggered by the stock market correc-

tions could be more than offset.

With 30 new investments, of which 14 were primary funds,

nine were secondary portfolios and seven were direct

investments, Pearl saw a high level of commitment activity

again in 2007. A total of EUR 121 million in new commit-

ments were made during the past financial year.

With EUR 175 million in capital calls, the level of investment

activity was higher than in the previous year, whereby most

of the funds went to the buyout sector. The picture in terms

of distributions, which at EUR 215 million clearly surpassed

the figure for 2006, was also very pleasing for the investors.

Thus, last year, the distributions exceeded the capital calls

for new investments from the underlying portfolio partner-

ships. The investment level of Pearl nevertheless increased

by over 4% year on year to 84.56% due to the valuation

adjustments in the private equity portfolio. The objective of

maintaining a full investment level was thus achieved.

The level of diversification of the portfolio was high at year-

end 2007 not only by the type of investment, i.e. primary,

secondary and direct investments as well as listed private

equity companies, but also by financing stage, geographic-

al region, industry sector and vintage year.

The Board of Directors believe that the advanced level of

maturity of the portfolio as well as its broad diversification

are the decisive factors why Pearl is likely to continue to

perform positively, if not quite as strongly due to macroecon-

omic conditions, in the coming year.

We would like to take this opportunity to thank you, the

investors, for the confidence you have shown in Pearl and

to assure you that we will do our utmost again in the

coming year to meet your high expectations.

The Board of Directors

Guernsey, March 2008

Für Pearl war das abgelaufene Geschäftsjahr, ungeachtet des

zeitweise recht unfreundlichen Marktumfeldes, ein Rekord-

jahr. Der geprüfte Innere Wert (NAV) verzeichnete einen

Anstieg von 18.30% auf das Allzeithoch von 124.45%, was

für Pearl das beste Jahresergebnis seit Auflegung bedeutet.

Unter Berücksichtigung des 2%igen Zinskupons, der jeweils

im September an die Investoren ausbezahlt wird, ergibt sich

sogar ein theoretischer Innerer Wert von 138.95%.

Hauptgrund für den höchsten jemals verzeichneten Jahres-

zuwachs des Inneren Wertes sind die Neubewertungen der

Partnerships, welche im Laufe des Jahres vorgenommen

werden konnten. Besonders erfreulich entwickelten sich der

Buyout-Bereich sowie die Direktinvestitionen. Dabei ist

hauptsächlich der fortgeschrittene Reifegrad des Portfolios

für die positive Entwicklung verantwortlich, da die unterlie-

genden Partnerships nach Zeiten der Investition nun durch

die Veräusserung ihrer Beteiligungen vermehrt Gewinne

realisieren und diese als Ausschüttungen an die Investoren

weitergeben können. Dank der vorgenommenen Aufwer-

tungen konnten die durch die Aktienmarktkorrekturen aus-

gelösten Einbrüche bei den börsennotierten Beteiligungsge-

sellschaften mehr als ausgeglichen werden.

Mit 30 neuen Beteiligungen, davon 14 Primärfonds, neun

Sekundärportfolios und sieben Direktinvestitionen, bewegten

sich die Commitmentaktivitäten von Pearl 2007 erneut auf

hohem Niveau. Insgesamt beliefen sich die neuen Zahlungs-

zusagen im abgelaufenen Geschäftsjahr auf EUR 121 Mio.

Die Investitionstätigkeiten konnten mit Kapitalabrufen in

Höhe von EUR 175 Mio. das Vorjahresergebnis übertreffen,

wobei die meisten Gelder an das Buyout-Segment flossen.

Sehr erfreulich für die Investoren gestaltete sich das Bild

auch bei den Rückflüssen, welche mit EUR 215 Mio. das

Ergebnis von 2006 deutlich übertreffen konnten. Die

Rückflüsse waren damit im vergangenen Jahr höher als

die Abrufe der dem Portofolio zugrunde liegenden Partner -

ships für neue Investitionen. Der Investitionsgrad von Pearl

steigerte sich dennoch aufgrund der Bewertungs-

anpas sungen im Private Equity-Portfolio gegenüber dem

Vorjahr um mehr als 4% auf 84.56%. Das Ziel, den vollen

Investitionsgrad beizubehalten, konnte somit eingehalten

werden.

Das Portfolio weist per Jahresende einen breiten Diversifi-

kationsgrad auf, sowohl was die Beteiligungsarten, also

Primär-, Sekundär- sowie Direktinvestitionen und börsen-

notierte Beteiligungsgesellschaften angeht, als auch im

Hinblick auf Finanzierungsstadien, geografische Regionen,

Industriesektoren und Gründungsjahre.

PEARL HOLDING LIMITED

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 9

10

Der fortgeschrittene Reifegrad des Portfolios sowie die brei-

te Diversifikation sind nach Meinung des Verwaltungsrates

die entscheidenden Faktoren, weshalb Pearl auch im kom-

menden Jahr weiterhin, wenn auch aufgrund des gesamt-

wirtschaftlichen Umfeldes etwas weniger stark, wachsen

dürfte.

An dieser Stelle möchten wir uns bei Ihnen, den Investo-

ren, für das entgegengebrachte Vertrauen bedanken und

Ihnen versichern, dass wir auch im kommenden Jahr alles

daran setzen werden, Ihre hohen Erwartungen zu erfüllen.

Der Verwaltungsrat

Guernsey, im März 2008

PEARL HOLDING LIMITED

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 10

11

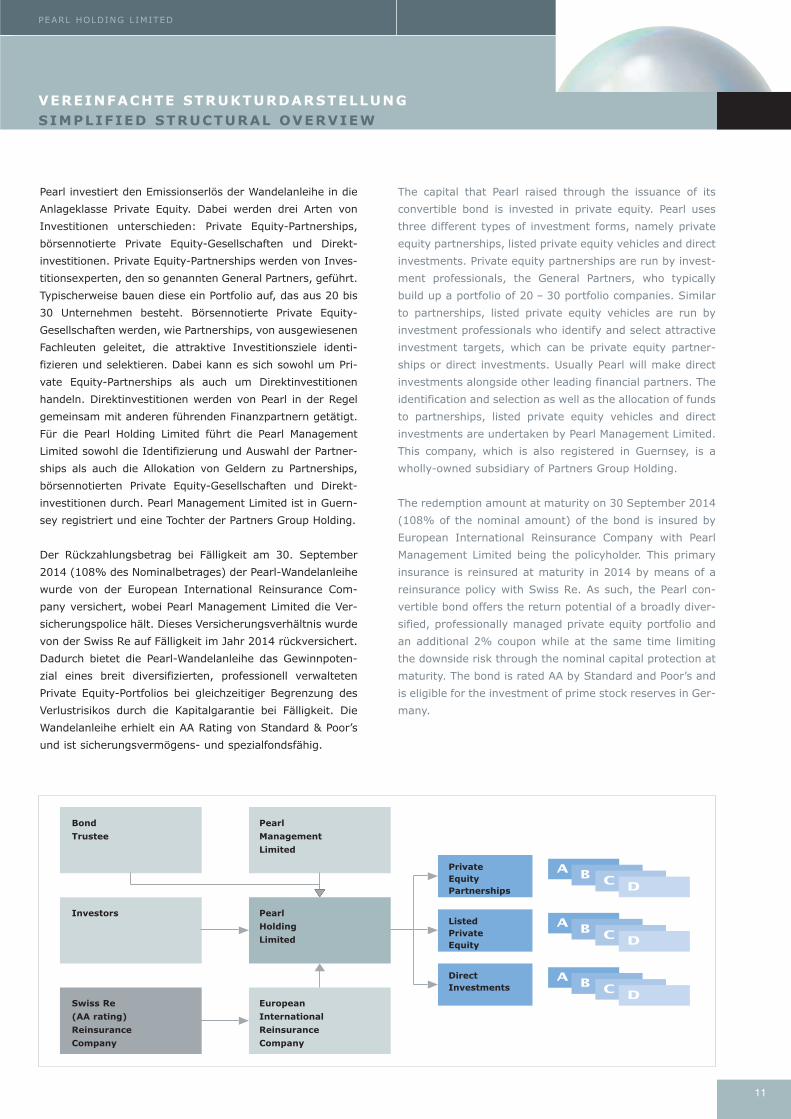

The capital that Pearl raised through the issuance of its

convertible bond is invested in private equity. Pearl uses

three different types of investment forms, namely private

equity partnerships, listed private equity vehicles and direct

investments. Private equity partnerships are run by invest-

ment professionals, the General Partners, who typically

build up a portfolio of 20 – 30 portfolio companies. Similar

to partnerships, listed private equity vehicles are run by

investment professionals who identify and select attractive

investment targets, which can be private equity partner-

ships or direct investments. Usually Pearl will make direct

investments alongside other leading financial partners. The

identification and selection as well as the allocation of funds

to partnerships, listed private equity vehicles and direct

investments are undertaken by Pearl Management Limited.

This company, which is also registered in Guernsey, is a

wholly-owned subsidiary of Partners Group Holding.

The redemption amount at maturity on 30 September 2014

(108% of the nominal amount) of the bond is insured by

European International Reinsurance Company with Pearl

Management Limited being the policyholder. This primary

insurance is reinsured at maturity in 2014 by means of a

reinsurance policy with Swiss Re. As such, the Pearl con-

vertible bond offers the return potential of a broadly diver-

sified, professionally managed private equity portfolio and

an additional 2% coupon while at the same time limiting

the downside risk through the nominal capital protection at

maturity. The bond is rated AA by Standard and Poor’s and

is eligible for the investment of prime stock reserves in Ger-

many.

Pearl investiert den Emissionserlös der Wandelanleihe in die

Anlageklasse Private Equity. Dabei werden drei Arten von

Investitionen unterschieden: Private Equity-Partnerships,

börsennotierte Private Equity-Gesellschaften und Direkt-

investitionen. Private Equity-Partnerships werden von Inves -

titionsexperten, den so genannten General Partners, geführt.

Typischerweise bauen diese ein Portfolio auf, das aus 20 bis

30 Unternehmen besteht. Börsennotierte Private Equity-

Gesellschaften werden, wie Partnerships, von ausgewiesenen

Fachleuten geleitet, die attraktive Investitionsziele identi -

fizieren und selektieren. Dabei kann es sich sowohl um Pri-

vate Equity-Partnerships als auch um Direktinvestitionen

handeln. Direktinvestitionen werden von Pearl in der Regel

gemeinsam mit anderen führenden Finanzpartnern getätigt.

Für die Pearl Holding Limited führt die Pearl Management

Limited sowohl die Identifizierung und Auswahl der Partner -

ships als auch die Allokation von Geldern zu Partnerships,

börsennotierten Private Equity-Gesellschaften und Direkt -

investitionen durch. Pearl Management Limited ist in Guern-

sey registriert und eine Tochter der Partners Group Holding.

Der Rückzahlungsbetrag bei Fälligkeit am 30. September

2014 (108% des Nominalbetrages) der Pearl-Wandelanleihe

wurde von der European International Reinsurance Com-

pany versichert, wobei Pearl Management Limited die Ver -

sicherungspolice hält. Dieses Versicherungsverhältnis wurde

von der Swiss Re auf Fälligkeit im Jahr 2014 rückversichert.

Dadurch bietet die Pearl-Wandelanleihe das Gewinnpoten -

zial eines breit diversifizierten, professionell verwalteten

Private Equity-Portfolios bei gleichzeitiger Begrenzung des

Verlust risikos durch die Kapitalgarantie bei Fälligkeit. Die

Wandelanleihe erhielt ein AA Rating von Standard & Poor’s

und ist sicherungsvermögens- und spezialfondsfähig.

PEARL HOLDING LIMITED

VEREINFACHTE STRUKTURDARSTELLUNG SIMPLIFIED STRUCTURAL OVERVIEW

A B C D

A B C D

A B C D

Bond

Trustee

Swiss Re

(AA rating)

Reinsurance

Company

European

International

Reinsurance

Company

Pearl

Holding

Limited

PrivateEquityPartnerships

Listed PrivateEquity

DirectInvestments

Investors

Pearl

Management

Limited

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 11

12

JAHRESBERICHT 2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 12

13

BERICHT DES INVESTMENT MANAGERSINVESTMENT MANAGER’S REPORT

ANNUAL REPORT 2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 13

14

BERICHT DES INVESTMENT MANAGERS

The Janus character of the year 2007

In Roman mythology, Janus is the god of gates and doors as

well as of beginnings and endings: he is usually depicted with

two faces looking in opposite directions. For investors, the

year 2007 had two faces as well and will be remembered as

a Janus year. The first half was characterized by euphoria

and buoyant equity markets, interrupted only briefly by tur-

bulence in late February and early March. In contrast, the

second half of 2007 proved to be one of the most difficult

periods for investors in the past decade, characterized by

financial market unrest and increasing risks to real economic

growth in the US. This episode of a global credit crisis, dried-

up liquidity and spread widening on the interbank and credit

markets originated from rising delinquency rates on principal

and interest payments in the US subprime mortgage market.

Concerns about mortgage-backed securities and structured

credit products led to a flight to safety and liquidity. Spreads

on asset-backed commercial papers widened sharply, syndi-

cation of leveraged loans froze and equities declined due to

simultaneous hedge fund action in August, the ongoing sub-

prime crisis in the US as well as the heavy write-downs in the

financial sector in November. Ongoing uncertainty about the

situation in the credit market and its potential spillover

effects on the real economy in the US led to mounting fears

that the US might enter a recession, which would have a

severe impact on global economic growth.

Overall healthy economic picture despite the credit

crisis

A look at the overall economic picture for 2007 shows that

the world economy expanded with a GDP growth of around

5% in real terms, which is in line with the previous year.

The market turbulence definitely had an impact on econ -

omic growth during the year and brought growth rates back

down to normal levels, especially in the US. Supported by

dynamic growth in the emerging markets and in Europe,

though, the world economy still reached the growth level of

the record year 2006. Moreover, by and large corporate

balance sheets were solid, with firms exhibiting low debt

and high cash levels and continued strong earnings growth.

So the negative effects of the events in the credit markets

had not had an impact at the corporate level, albeit with the

exception of the credit institutions, which were hit hard by

the crisis and leading in some cases to posting losses due

to major write-offs in the second half of the year.

Impact of the credit crisis on the LBO market

The headlines in the previous year and again in the first half

of 2007 were dominated by announcements of multi-billion

Der Janus-Charakter des Jahres 2007

Janus, der Gott der Türen und Tore sowie des Anfangs und

des Endes in der römischen Mythologie, wird üblicherweise

doppelköpfig mit zwei Gesichtern dargestellt, die in ent-

gegengesetzte Richtungen schauen. Der sogenannte

Januskopf gilt daher als Symbol der Zwiespältigkeit und als

ein zwiespältiges Jahr wird den Investoren das Jahr 2007 in

Erinnerung bleiben. Die erste Jahreshälfte zeichnete sich

bis auf die kurzfristigen Turbulenzen Ende Februar und

Anfang März durch Euphorie und steigende Aktienkurse

aus. Im Gegensatz dazu erwies sich die zweite Jahreshälf-

te als eine der schwierigsten Perioden der letzten zehn

Jahre, gekennzeichnet von turbulenten Finanzmärkten und

einem steigenden Risiko für das reale Wirtschaftswachstum

in den USA. Durch Nichtzahlungen von Schulden bei Fällig-

keit im Markt für minderklassige Hypotheken in den USA

entstand eine globale Kreditkrise mit stark sinkender Liqui-

dität und steigenden Risikoprämien im Zwischenbankenge-

schäft und auf den Kreditmärkten. Die Besorgnis über

hypothekarisch gesicherte Wertpapiere und strukturierte

Kreditprodukte führte zu einer allgemeinen Flucht Richtung

Sicherheit und Liquidität. Die Risikoprämien für durch Ver-

mögenswerte besicherte Wertpapiere stiegen dramatisch,

die Syndizierung fremdfinanzierter Kredite kam zum Erlie-

gen und Aktien verloren an Wert, zum einen durch Hedge-

fonds, welche im August gleichzeitig grössere Transaktio-

nen durchführten, zum anderen aufgrund der weiterhin

andauernden Kreditkrise in den USA sowie der signifikanten

Ab schrei bungen im Finanzsektor im Laufe des Novembers.

Die an haltende Unsicherheit über die Situation an den Kre-

dit märkten und deren mögliche Auswirkungen auf die Real-

wirtschaft in den USA führten letztlich zu einer steigenden

Befürchtung, dass die USA in eine Rezession verfallen

könnte, was wiederum drastische Auswirkungen auf das

globale Wirtschaftswachstum hätte.

Gesunde Gesamtwirtschaft trotz Krise

Ein Blick auf das gesamtwirtschaftliche Bild in 2007 zeigt ein

reales globales Wirtschaftswachstum von 5%, ähnlich wie

im Vorjahr. Die Marktturbulenzen hatten definitiv einen Ein-

fluss und haben die Wachstumsraten, besonders in den

USA, auf ein normales Niveau zurückgebracht. Unterstützt

durch das dynamische Wachstum in den Schwellenländern

und in Europa erreichte die Weltwirtschaft dennoch das

Wachstum des Rekordjahres 2006. Die Unternehmens-

bilanzen zeigten mit niedrigen Fremdkapitalquoten, viel

liquiden Mitteln und anhaltend starken Anstiegen der Erträ-

ge im Grossen und Ganzen solide Werte. Der negative Ein-

fluss der Geschehnisse an den Kreditmärkten blieb auf

Unternehmensebene somit aus; lediglich die kreditverge-

RÜCKBLICK AUF DIE PRIVATE EQUITY-INDUSTRIE 2007REVIEW ON THE PRIVATE EQUITY INDUSTRY IN 2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 14

15

INVESTMENT MANAGER’S REPORT

leveraged buyout (LBO) deals in the private equity industry.

The record-breaking RJR Nabisco LBO in the late 1980s,

which closed at USD 32 billion, suddenly appeared relative-

ly small compared to the USD 40 billion plus deals of Bell

Canada Enterprises and TXU. Obviously, the amount of debt

financing that was used for these deals was substantial.

Moreover, the debt necessary to realize investments of this

size was available at low cost in the market during the first

half of 2007 and private equity investors coped with rising

prices for transactions by making use of a sufficient amount

of debt in the LBOs. So as transaction sizes rose, leverage

in the buyout sector also increased to record levels. As the

average deal size grew, only a small number of public firms

were still considered too large to be a target for a private

equity takeover. Rising debt levels in the transactions was

not a worry as long as the cost of the debt financing remain -

ed at the low levels of the first half of the year.

But the picture changed in the second half of the year when

the liquid credit market ground to an abrupt halt in the

wake of the subprime crisis, thereby slowing down the buy-

out market. The large- and mega-large LBOs suddenly had

hardly any access to debt financing as credit spreads widen -

ed sharply and increased the cost of debt financing sig -

nificantly, which in turn made multi-billion LBOs difficult to

realize. For the same reasons, large public to private trans-

actions also experienced difficulties after several years of

continuous growth in total volume: the market turmoil sent

capital costs for buyout firms higher and reduced the strike

zone after years of steady expansion, causing a significant

downturn in large-cap public to private volume as well.

Is this a bad thing for the private equity industry? This is

definitely not a question that can be answered with a

simple yes or no. Various statistics indicate that the credit

crisis has certainly not disrupted the entire industry. On the

contrary, there was a remarkable level of activity in the

small- and mid-cap buyout universe up to an enterprise

value of USD 1 billion during the second half of 2007. The

number of mega deals in the buyout sector, though, de -

c reased, indicating a shift from large- to mid-cap LBOs. Due to

the increase in the number of smaller deals with enterprise

values of below USD 1 billion and the contribution of the

mega deals during the first half of the year, the total vol -

ume for 2007 still showed strong results.

Shift from large- to mid-cap deals

The paradigm shift from large to smaller deals during the

year is reflected in the annual figures for the different

regions as well. Buyouts valued at more than USD 1 billion

more than doubled in the US compared to 2006 to a total

benden Banken, die durch die Krise substanziell getroffen

wurden, mussten in der zweiten Jahreshälfte aufgrund von

signifikanten Abschreibungen teilweise Verluste hinnehmen.

Auswirkungen der Kreditkrise auf den LBO-Markt

Die Schlagzeilen des Vorjahres und der ersten Hälfte von

2007 waren geprägt von fremdfinanzierten Firmenübernah-

men (LBOs) in Milliardenhöhe durch Private Equity-Unter-

nehmen. Der RJR Nabisco-Rekord der 80er Jahre in Höhe von

USD 32 Mrd. sah neben den USD 40 Mrd.-Deals von Bell

Canada Enterprises und TXU nun vergleichsweise klein aus.

Verständlicherweise war der Fremdkapitalanteil in diesen

Transaktionen substanziell. Das notwendige Fremdkapital

war während der ersten Jahreshälfte im Markt jedoch sehr

günstig verfügbar und die Private Equity-Investoren konnten

daher die steigenden Preise der Transaktionen dadurch auf-

bringen, dass sie ihre Übernahmen zu einem grossen Teil mit

Fremdkapital finanzierten. Mit dem Anstieg der Transaktions-

grössen nahm also auch das benötigte Fremdkapital im Buy-

out-Segment auf ein rekordverdächtiges Niveau zu. Durch

die immer grösser werdenden Deals gab es nur noch wenige

börsennotierte Unternehmen, von denen man dachte, dass

sie aufgrund ihrer Grösse nicht Ziel einer Private Equity-

Übernahme sein könnten. Der steigende Fremdkapitalbedarf

stellte auch kein Problem dar, so lange sich die Finanzie-

rungskosten weiterhin auf so niedrigem Niveau bewegen

würden wie in der ersten Jahreshälfte.

In der zweiten Jahreshälfte änderte sich jedoch das Bild:

die liquiden Kreditmärkte kamen in Folge der Krise plötzlich

zum Erliegen und sorgten für eine Abkühlung des Buyout-

Marktes. Für grosse und Mega-Deals stand von einem auf

den anderen Tag kaum noch Fremdfinanzierung zur Verfü-

gung, da die Risikoprämien signifikant anstiegen und die

Kosten in die Höhe trieben, was wiederum dazu führte,

dass die grossen LBOs kaum noch zu realisieren waren. Aus

ähnlichen Gründen sahen sich auch die grossen Public-to-

Private-Transaktionen nach Jahren konstanten Wachstums

auf einmal mit Schwierigkeiten konfrontiert: Die Unruhen

am Markt liessen die Kapitalkosten für Buyout-Unterneh-

men in die Höhe schnellen und reduzierten die Preise, die

für Public-to-Private-Deals bezahlt wurden, nach einer ste-

tigen Expansion in den Jahren zuvor. Dies wiederum führte

dazu, dass das Volumen von grossen Public-to-Private-

Deals signifikant zurückging.

War diese Entwicklung schlecht für die Private Equity-Indu-

strie? Diese Frage kann nicht einfach mit Ja oder Nein

beantwortet werden, aber wie verschiedene Statistiken zei-

gen, hat die Krise die Industrie als Ganzes nicht beeinträch-

tigt. Im Gegenteil: Während die Anzahl der Mega-Deals

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 15

16

BERICHT DES INVESTMENT MANAGERS

of USD 451 billion, but only driven by the mega transac-

tions of the first six months. Middle-market deals valued at

between USD 100 million and USD 1 billion were up by

23%, an increase that can be attributed to the shift from

large to more medium-sized transactions in the second half

of the year, while smaller deals worth less than USD 100

million declined by 50% to USD 5 billion.

In Europe, buyouts valued at between EUR 250 million and

EUR 1 billion increased by over 38% in 2007, while deals in

the EUR 250 million to EUR 500 million range were up by

43% for the same reasons that caused the jump in the

middle market in the US. The value of EUR 1 billion plus

buyouts in 2007 fell by 14% since the majority of the mega

buyouts that boosted the numbers for this segment took

place in the US. By value, EUR 1 billion plus deals still com-

prised half of the European buyout market in 2007, but

down from 59% in 2006.

The value of Asian buyout deals decreased by 21% to USD

42 billion while the number of deals increased by 17%,

implying a larger number of deals, but with a smaller value.

There were only four buyout deals with a transaction value

of over USD 1 billion in 2007, compared to 12 deals of that

size in 2006, indicating a shift from mega deals to smaller

transactions in Asia, too.

Fundraising flattens

The overall picture on the buyout fundraising side still show -

ed high levels despite the credit crisis. However, after

seeing record fundraising levels in the first half of the year,

the credit crunch seemed to affect fundraising for buyout

funds in the second half of 2007. Out of the slightly over

USD 200 billion that were raised by buyout funds in 2007 –

just below the 2006 volume – approximately two thirds

came in during the first six months. After very strong

growth over the past 24 months, fundraising volumes

appear to be normalizing but remain at solid levels.

A healthy correction and a flight to quality

Although the correction in the debt markets was the domi-

nating negative headline during the past year, it had sev -

eral positive aspects which need to be taken into account as

well, since they should have a positive impact on the indus -

try in the long run. The ready availability of cheap debt

before the crisis not only produced an increase in the num-

ber of mega deals, but also led to high returns that were

often driven by recapitalizations. Private equity sponsors

could finance distributions to their investors via leverage, a

fact that took the focus off the core activity, namely value

zurückging, waren die Aktivitäten im klein- und mittelstän-

dischen Buyout-Segment bis zu einem Unternehmenswert

von USD 1 Mrd. in der zweiten Jahreshälfte bemerkenswert

hoch, ein Indiz für den Wechsel von grossen zu mittelgros-

sen Transaktionen. Aufgrund dieser Zunahme kleinerer

Deals und der noch in der ersten Jahreshälfte abgeschlos-

senen Mega-Deals blieb das Buyout-Investitionsvolumen

auch 2007 auf einem weiterhin hohen Niveau.

Verschiebung von grossen zu mittelgrossen Deals

Der Paradigmenwechsel von grossen zu kleineren Deals im

Laufe des Jahres spiegelt sich in allen Regionen wider.

Übernahmen über USD 1 Mrd. haben sich in den USA im

Ver gleich zu 2006 zwar auf USD 451 Mrd. mehr als verdop-

pelt, allerdings nur getrieben durch die in den ersten sechs

Monaten abgeschlossenen Mega-Transaktionen. Das mittle-

re Segment zwischen USD 100 Mio. und USD 1 Mrd. erfuhr

einen Zuwachs von 23%, was auf die Verschiebung von

grossen zu mittleren Deals in der zweiten Jahreshälfte

zurückzuführen ist, während Unter nehmens käufe unter

USD 100 Mio. um 50% auf USD 5 Mrd. zurückgingen.

In Europa stiegen Buyouts zwischen EUR 250 Mio. und EUR

1 Mrd. in 2007 um 38%, während das Segment zwischen

EUR 250 Mio. und EUR 500 Mio. sogar um 43% anwuchs,

was in beiden Fällen auf die gleichen Gründe zurückzufüh-

ren ist, die auch in den USA in diesem Bereich für die

Zunahme sorgten. Das Gesamtvolumen bei Transaktionen

über EUR 1 Mrd. ging 2007 hingegen um 14% zurück, da

die Mehrheit der Mega-Deals in den USA stattfand. Gesamt-

haft machten die Transaktionen über EUR 1 Mrd. weiterhin

rund die Hälfte des europäischen Buyout-Marktes in 2007

aus, allerdings weniger als 2006, als sie noch für 59% des

Volumens verantwortlich waren.

Asiatische Buyout-Deals gingen um 21% auf einen Gesamt-

wert von USD 42 Mrd. zurück, während die Anzahl der

Transaktionen um 17% anstieg, was eine grössere Anzahl

Deals mit geringerem Volumen impliziert. Insgesamt gab es

2007 in Asien lediglich vier Deals, deren Transaktionsvolu-

men die USD 1 Mrd.-Grenze überschritt, im Vergleich zu

zwölf im Vorjahr. Diese Abnahme zeigt auch in Asien die

Verschiebung von Mega-Deals zu kleineren Transaktionen.

Fundraising flacht ab

Das Fundraising im Buyout-Segment bleibt trotz Kreditkri-

se noch auf einem hohen Niveau. Dennoch hatte der

Zusammenbruch der Kreditmärkte auch hier einen Einfluss,

nachdem sich die Mittelbeschaffung in der ersten Jahres-

hälfte noch in rekordverdächtigen Regionen bewegt hatte.

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 16

17

INVESTMENT MANAGER’S REPORT

creation in their portfolio companies. The rising cost of

capital necessitates a shift in focus towards value creation

in the buyout segment and operational value add is gaining

in importance as the opportunities for capital arbitrage

become more limited. Private equity sponsors have to focus

on their core competencies as a result of the credit crisis,

with corporate restructuring, cost reduction and organic

and external growth turning into key factors again, leading

to a reinforcement of general partner qualities.

Record M&A volume supports private equity industry

The value of global mergers and acquisitions (M&A) hit a

new record, despite the US subprime crisis and the liquid -

ity problems in the credit markets, also driven by the mega

buyouts of TXU, First Data, Alltell and Hilton in the first half

of the year. Overall, announced takeover bids increased by

24% compared to the previous year to some EUR 4’500 bil-

lion. Transaction values decreased during the third and

fourth quarters after the record-breaking first half of 2007,

while the number of small- and mid-cap M&A transactions

increased as financing for mega deals dried up.

M&A activity involving private equity firms nevertheless

reached a record USD 791 billion, representing 18% of the

overall market. During the first half of the year, private

equity funds accounted for a large part of the M&A volume

Über USD 200 Mrd. wurden 2007 von Buyout-Fonds einge-

worben, leicht weniger als im Vorjahr. Zwei Drittel des Volu-

mens stammen aus der ersten Jahreshälfte. Nach dem

extrem starken Wachstum der letzten 24 Monate scheint

sich das Fundraising nun auf einem normalen, aber soliden

Niveau einzupendeln.

Gesunde Korrektur und die Flucht Richtung Qualität

Obwohl die Korrektur an den Fremdkapitalmärkten definitiv

die dominierende Negativ-Schlagzeile des letzten Jahres war,

so brachte sie auch einige gute Aspekte mit sich, die nicht

ausser Acht gelassen werden sollten, da sie langfristig einen

positiven Einfluss auf die Industrie haben werden. Die güns -

tige Verfügbarkeit von Fremdkapital, wie sie vor der Krise zu

beobachten war, hat nicht nur die Anzahl der Mega-Transak-

tionen erhöht, sondern zusätzlich zu hohen Renditen geführt,

die allerdings vielfach auf Rekapitalisierungen beruhten. Pri-

vate Equity-Häuser konnten Ausschüttungen über Fremdka-

pital finanzieren, was den Fokus von der eigentlichen Aufga-

be, nämlich der Schaffung von Mehrwert in den Portfolioun-

ternehmen, ablenkte. Der Anstieg der Kapitalkosten führt

nun dazu, dass es wieder mehr darum geht, Mehrwert zu

schaffen und auf operativer Ebene zu optimieren, da die

Arbitrage-Opportunitäten über Fremdkapital limitiert sind.

Private Equity-Häuser müssen sich also in Folge der Krise

wieder vermehrt auf ihre Kern aufgaben konzentrieren,

Quelle – Source: Standard & Poors LCD Computations

1’600

1’400

1’200

1’000

800

600

400

200

0

in U

SD

Mio

. –

in U

SD

mill

ion

282 296 279 319

424

528

762721

834 842

1’383

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

DURCHSCHNITTLICHE LBO-GRÖSSEN WELTWEIT

GLOBAL AVERAGE LBO SIZES

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 17

18

BERICHT DES INVESTMENT MANAGERS

due to their participation in leveraged billion dollar transac-

tions. In the wake of the credit crunch, the private equity

sponsors have almost completely withdrawn from the M&A

space and made room for the strategic investors who aim

to acquire companies in their own segment.

Mezzanine’s comeback in the aftermath of the credit

crisis

Mezzanine debt lost market share relative to senior and

second lien debt in the first half of 2007 as financial spon-

sors were, to a certain extent, able to substitute mezzani-

ne with senior debt due to the favorable credit market envir -

onment and the low level of risk aversion. This trend went

into reverse in the summer, with mezzanine again coming

to the fore: the use and the terms and conditions of mez-

zanine tranches improved significantly. Mezzanine lenders

returned to favor, supported by rising demand for loans

that have fixed interest rates and warrants tied to a com-

pany’s equity, making them less susceptible to credit mar-

ket fluctuations. Pricing started to profit from rising credit

spreads which increased the return potential for mezzanine

debt. Moreover, the credit crisis generated possibilities to

include equity kickers in mezzanine transactions again,

generating additional returns and increased investor pro-

tection. Finally, transaction risks were reduced through

Restrukturierungen, Kosten ein spa rungen sowie organisches

und externes Wachstum, was letztlich die Fähig keit der

General Partner wieder in den Vordergrund rücken lässt.

Rekord-M&A-Volumen treibt Private Equity-Industrie

Das weltweite Volumen von Fusionen und Übernahmen

(M&A) hat trotz der Subprime-Krise in den USA und den

Korrekturen an den Kreditmärkten einen neuen Höchst-

stand erreicht, unter anderem unterstützt durch die Mega-

Buyouts von TXU, First Data, Alltel und Hilton in der ersten

Jahreshälfte. Gesamthaft stiegen die ausgewiesenen Über-

nahmeangebote im Vergleich zum Vorjahr um 24% auf

etwa EUR 4’500 Mrd. Transaktionsvolumen sind allerdings

im dritten und vierten Quartal gesunken, nachdem in den

ersten sechs Monaten Rekordwerte erreicht wurden; so

wurden vermehrt kleine und mittlere M&A-Transaktionen

durchgeführt, da für die Mega-Deals kein Fremdkapital

mehr zur Verfügung stand.

Die M&A-Aktivitäten mit Private Equity-Beteiligung erreich-

ten mit einem Volumen von USD 791 Mrd. dennoch einen

neuen Rekord und machten damit 18% des gesamten

Marktvolumens aus. Während der ersten sechs Monate des

Jahres waren Private Equity-Fonds durch ihre Beteiligungen

in fremdkapitalfinanzierten Milliarden-Transaktionen gar für

Quelle – Source: Standard & Poor’s LCD European Mezzanine Review Q4, 2007

14

12

10

8

6

4

2

0

in E

UR M

rd.

– in E

UR b

illio

n

1.7 1.8

3.2 3.4

5.1

8.9

12.212.8

2000 2001 2002 2003 2004 2005 2006 2007

EUROPÄISCHES MEZZANINE-VOLUMEN 2000–2007

EUROPEAN MEZZANINE VOLUME 2000–2007

Europäisches Mezzanine-Volumen 2000–2007 – European Mezzanine Volume 2000–2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 18

19

INVESTMENT MANAGER’S REPORT

lower leverage levels. Mezzanine debt thus profited signifi-

cantly from the difficulties in the credit market. As a conse-

quence, mezzanine volume again set an annual record in

Europe with a solid increase as compared to the previous

year. In the US, where the market is based on independent

mezzanine providers, the total new-issue sponsored leverag -

ed loan volume, which includes mezzanine, indicated healthy

growth in this region as well.

Venture capital: trend to maturity

The venture segment has matured since the bursting of the

technology bubble in 2000 and the quality of the invest-

ments has improved, providing great potential for invest -

ors. In addition, a new growth segment has emerged with -

in venture which offers highly attractive opportunities.

Growth investments are typically made in fast-growing

companies that demonstrate a strong history of expansion

and are typically profitable or demonstrate a clear view to

profitability.

Global venture capital fundraising activity was relatively

stable over the past twelve months and in line with the pre-

vious year. Total US fundraising volume increased from USD

32 billion by 229 funds in 2006 to USD 35 billion by 235

funds in 2007. In Europe, 64 venture funds raised USD 5.5

billion in 2007, a slight increase on the USD 5.3 billion in

the previous year. Established venture capital and growth

funds turned their focus to investing the capital that had

been recently raised, as demonstrated by the record num-

ber of investments last year. The pace of venture investing

in the US continued to pick up throughout 2007, whereas

in Europe it remained broadly constant. Deal sizes in -

creased in Europe, though, confirming the trend towards

larger, later-stage deals.

The exit environment for venture-backed companies was

benign over the past 12 months, as can be seen by the

increase in M&A value and IPO offerings: the disclosed

value of venture-backed M&As climbed by almost 50% over

the previous year to USD 25.4 billion, while the number of

venture-backed IPOs enhanced by the same percentage to

a total of 86 in 2007. Significant growth in the IPO market

led to a situation where going public was a viable alterna-

tive to an M&A exit. As a result, companies could afford to

resist M&A offers, which often elicited even higher bids

from potential acquirers. As a consequence of the most

recent market downturn, trade sales became the flavor of

the day with significant prices being paid for established

market leaders that have developed disruptive technologies

and products. For example, the leading global entertain-

ment content company Viacom demonstrated its willing -

einen Grossteil des gesamten M&A-Volumens verantwort-

lich. Im Anschluss an die Kreditkrise haben sich die Private

Equity-Häuser dann fast komplett von Fusionen und Über-

nahmen zurückgezogen und so Platz für strategische Inves -

toren geschaffen, die zum Ziel haben, Unternehmen ihres

Segmentes zu akquirieren.

Kreditkrise bringt Mezzanine zurück

Mezzanine-Fremdkapital verlor in der ersten Jahreshälfte im

Vergleich zu vorrangigen Verbindlichkeiten Marktanteile, da

Finanzinvestoren Mezzanine aufgrund der günstigen Kredit -

märkte und der allgemein geringen Risikoaversion zu einem

gewissen Teil durch vorrangige Verbindlichkeiten ersetzten.

Diese Entwicklung erfuhr im Laufe des Sommers eine Kehrt -

wende und Mezzanine gewann wieder an Bedeutung: Bedin-

gungen und Konditionen von Mezzanine verbesserten sich

signifikant und die Präsenz nahm dadurch deutlich zu. Die

Anbieter von Mezzanine waren wieder im Geschäft, unter-

stützt durch die gestiegene Nachfrage nach Krediten mit fes -

ten Zinsen und Eigenkapitaloptionen, die dazu führen, dass

die Kredite weniger anfällig gegenüber Fluktuationen im Kre-

ditmarkt sind. Auch die Preisgestaltung profitierte vom

Anstieg der Risikoprämien, wodurch sich das Rendite -

potenzial von Mezzanine-Fremdkapital wieder erhöhte.

Ausserdem entstanden durch die Krise Möglichkeiten, Equity-

Kicker in die Mezzanine-Transaktionen einzubauen, was

zusätzliche Renditequellen schafft und für die Investoren eine

höhere Absicherung mit sich bringt. Zu guter Letzt wurde das

Transaktionsrisiko durch einen geringeren Fremdkapitalanteil

bei den Deals reduziert. Aus diesen Gründen hat Mezzanine

von den Schwierigkeiten an den Kreditmärkten stark profi-

tiert. Das Mezzanine-Volumen in Europa konnte daher wiede-

rum einen leichten Anstieg im Vergleich zum Vorjahr und

somit einen Rekord für 2007 verbuchen. In den USA, wo der

Markt im Wesentlichen von unabhängigen Mezzanine-Anbie-

tern kontrolliert wird, deutet der Anstieg des gesamten neu

aufgelegten LBO-Kreditvolumens, das Mezzanine beinhaltet,

auf ein solides Wachstum auch in dieser Region hin.

Venture Capital ist gereift

Das Venture-Segment hat sich seit dem Platzen der Technolo-

gie-Blase in 2000 stark weiterentwickelt und die Qualität der

Investitionen hat sich im Laufe der letzten Jahre deutlich ver-

bessert, was für den Investor ein enormes Potenzial bedeutet.

Zusätzlich ist das Wachstumssegment aus dem Venture-

Bereich hervorgetreten, welches äusserst interessante Mög-

lichkeiten bietet. Wachstumsinvestitionen werden üblicher-

weise in schnell wachsende Unternehmen getätigt, welche in

der Vergangenheit stark expandiert haben und bereits profita-

bel sind oder unmittelbar vor der Profitabilität stehen.

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 19

20

BERICHT DES INVESTMENT MANAGERS

ness to pay up for nextgeneration companies such as

XFire in order to be able to participate in new trends such

as social networking within the gaming space. XFire was

backed by Pearl partnership Draper Fisher Jurvetson and

New Enterprise Associates as well as Granite Global

Ventures. Growth opportunities have therefore been very

interesting and offer significant upside potential.

Another characteristic of venture capital, namely the

importance of a long-term investment horizon, is illustrated

by Swiss technology company u-blox. Since the J-curve for

venture capital investments is pronounced and requires a

strong conviction and perseverance, it is essential to have

a clear understanding of the quality and the upside poten-

tial of the investment. In the case of u-blox, an investment

period of ten years was necessary between founding the

company in 1997 and the IPO on the SWX Swiss Exchange

in October 2007.

Market turmoil supports secondary buyers

In the first half of 2007, sellers’ pricing expectations in the

secondary market were at an unreasonably high level.

However, by the end of the first half of 2007 the market

correction had caused sellers to lower their pricing expec-

tations to more realistic levels thanks to the basic function

of supply and demand. Many holders of private equity port-

folios, especially banks, entered the market to sell their

portfolios driven by an increased need for liquidity. At the

same time, the number of potential buyers in the second -

ary market remained relatively stable. Because the supply

increased but the demand remained more or less constant,

the prices for portfolios dropped to balance the disequilib -

rium – a favorable dynamic for secondary buyers. Anal -

ogous to the case of mezzanine financing, the credit crisis

can therefore be said to have had a positive impact for

secondary buyers.

Turbulent year for the listed private equity asset

class

After a solid performance in the first half of 2007, the listed

private equity stocks suffered disproportionally in the second

half amid the global financial market turmoil. Concerns about

the debt financing of private equity in general and the nega -

tive performance of the stock markets led to a significant in -

crease in volatility. In many cases, the market seemed to over-

react and ceased to differentiate between the portfolio qual -

ities of individual listed private equity companies: the funda-

mental data of the companies was no longer reflected in the

actual stock prices. Overall, as measured by the LPX50 Index,

the listed private equity asset class closed 2007 down 15%.

Die globalen Fundraising-Aktivitäten im Venture Capital-

Bereich bewegten sich im abgelaufenen Jahr auf dem

Niveau des Vorjahres. Das Gesamtvolumen in den USA

wuchs von USD 32 Mrd. aufgenommen von 229 Fonds auf

USD 35 Mrd., die von 235 Fonds eingeworben wurden. In

Europa sammelten 64 Venture-Fonds Neugelder in Höhe von

USD 5.5 Mrd. in 2007, was einem leichten Anstieg gegen -

über den USD 5.3 Mrd. des Vorjahres entspricht. Die bekann-

ten Venture Capital- und Wachstumsfonds legen ihren Fokus

derzeit darauf, das in den letzten Jahren gesammelte Kapi-

tal zu investieren, was die rekordverdächtigen Zahlen für

2007 auf der Investitionsseite belegen. So verzeichneten die

USA erneut einen Anstieg, während das Investitionsvolumen

in Europa relativ konstant blieb. Dabei ist die Grösse der

Deals in Europa angestiegen, was den Trend hin zu grö -

sseren Spätphasenfinanzierungen bestätigt.

Das Exit-Umfeld für durch Venture Capital unterstützte

Unternehmen erwies sich in den letzten zwölf Monaten als

freundlich, was im Anstieg des M&A-Volumens und der Bör-

sengänge zu erkennen ist: das Gesamtvolumen bekannt-

gegebener M&A-Transaktionen, die Venture Capital beinhal-

ten, stieg um nahezu 50% im Vergleich zum Vorjahr auf

USD 25.4 Mrd., während die Gesamtzahl der Börsen gänge

von Unternehmen, bei denen Venture Capital involviert war,

um den gleichen Prozentsatz auf 86 IPOs in 2007 stieg. Der

signifikante Anstieg stellt unter Beweis, dass der Börsen -

gang wieder eine interessante Alternative zu einem Exit

durch eine Fusion oder Übernahme ist. In Folge konnten es

sich die Unternehmen nun leisten, Übernahmeangebote

abzulehnen, was wiederum zu einer Erhöhung der Preise

führte. Im Rahmen der Marktturbulenzen haben auch Ver-

käufe an strategische Investoren wieder an Bedeutung

gewonnen: Für etablierte Marktführer, die bahnbrechende

Technologien oder Produkte entwickelt haben, zahlten stra-

tegische Investoren hohe Preise. Ein Beispiel hierfür ist das

führende global agierende Unterhaltungsunternehmen Via-

com, welches bereit war, für Firmen der nächsten Genera-

tion, wie etwa XFire, einen Aufpreis zu zahlen, um so an

neuen Trends, wie in diesem Falle dem Networking unter

Computerspielern, teilzunehmen. XFire wurde von den

Pearl-Partnerships Draper Fisher Jurvetson und New Enter-

prise Associates sowie Granite Globale Ventures unter-

stützt. Das mit Wachstumsfinanzierungen verbundene

Wertsteigerungspotenzial hat sich im abgelaufenen Jahr

erneut deutlich unter Beweis gestellt.

Ein weiteres Merkmal von Venture Capital – die Wichtigkeit

eines langfristigen Investitionshorizontes – hat weiterhin

Bestand und wird am Beispiel des Schweizer Technologie -

unternehmens u-blox deutlich. Da es bei Venture-Investi tionen

einen J-Kurven-Effekt gibt und starke Überzeugung und Aus-

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 20

21

INVESTMENT MANAGER’S REPORT

European and US private equity outperform MSCI

The 10-year performance figures for the private equity

asset class remained stable in 2007. While returns for US

private equity declined slightly to 10.9%, European private

equity returns increased from 11.3% to 12.5%. The best

performance came from US venture capital funds, which

posted an IRR of 19.1% in the ten-year period from June

1997 to June 2007. Private equity has thus again proved to

be a valuable asset class for enhancing portfolio returns. US

and European private equity funds both outperformed the

MSCI World Index, which posted a 7.5% gain over the

same 10-year period.

dauer gefragt sind, ist es von essenzieller Be deutung, ein

genaues Verständnis von der Qualität und dem Wert -

steigerungspotenzial der Investition zu besitzen. Im Fall von

u-blox war ein Investitionszeitraum von zehn Jahren zwischen

Gründung des Unternehmens und dem erfolgreichen Börsen-

gang an der SWX Swiss Exchange im Oktober 2007 notwendig.

Marktturbulenzen unterstützen den Sekundärmarkt

Während der ersten Jahreshälfte waren die Preisvorstel -

lungen der Verkäufer am Sekundärmarkt auf einem unan -

gemessen hohen Niveau. Die Marktkorrektur führte allerdings

dazu, dass die Preisvorstellungen sich nach unten orientier-

ten, was im Wesentlichen durch das Zusammenspiel von An -

gebot und Nachfrage zu erklären ist. Getrieben von Liquidi-

tätsengpässen versuchten viele Besitzer von Private Equity-

Portfolios, insbesondere Banken, ihre Anlagen am Sekundär-

markt zu veräussern. Gleichzeitig blieb die Anzahl der poten-

ziellen Käufer aber unverändert. Das Angebot stieg also, wäh-

rend die Nachfrage mehr oder weniger identisch blieb, was

dazu führte, dass die Preise der Portfolios fielen, um das

Ungleichgewicht am Markt auszugleichen – sehr zum Vorteil

Quelle – Source: Thomson Venture Economics 10Y Investment Horizon Performance per 30.06.2007, Bloomberg (GDDUWI Index Return in USD):

01.07.1997–30.06.2007 / Für Westeuropa-Mezzanine sind keine Daten verfügbar – No data available for Western Europe Mezzanine

LANGFRISTIGE PRIVATE EQUITY-PERFORMANCE

LONG-TERM PRIVATE EQUITY-PERFORMANCE

USA Westeuropa – Western Europe MSCI World

25%

20%

15%

10%

5%

0%

+10.9%

+12.5%

+8.7%

+17.4%

+19.1%

+3.0%

+5.7%

All Private Equity Buyout Venture Mezzanine

MSCI World: +7.5%

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 21

22

der Käufer von Sekundärportfolios. Ähnlich wie bei Mezzani-

ne hatte die Kreditkrise demnach auch für den Sekundär-

markt einen positiven Effekt für die Käuferseite des Seg-

ments.

Turbulentes Jahr für Listed Private Equity

Nach einer äusserst soliden Entwicklung in der ersten Jah-

reshälfte erlitten die Aktien börsennotierter Private Equity-

Unternehmen im Rahmen der globalen Korrekturen über-

proportionale Verluste in der zweiten Hälfte von 2007. Die

Sorgen um die Fremdfinanzierung im Private Equity-Bereich

generell sowie die negative Entwicklung der Aktienmärkte

führten zu einem drastischen Anstieg der Volatilität. In vie-

len Fällen hatte es den Anschein, dass die Märkte überrea-

gierten und die unterschiedliche Qualität der Portfolios der

verschiedenen börsennotierten Unternehmen nicht mehr in

Betracht zogen: Die Fundamentaldaten spiegelten sich in

den Aktienkursen nicht mehr wider. Gesamthaft betrachtet

verlor die börsennotierte Private Equity-Anlageklasse im

abgelaufenen Jahr gemessen am LPX 50 etwa 15%.

Private Equity besser als Aktienmärkte

Die Gesamtperformance über die letzten zehn Jahre blieb

für die Anlageklasse Private Equity in 2007 stabil. Während

die Rendite (IRR) von Private Equity über den 10-Jahres-

Zeitraum vom Juni 1997 bis Juni 2007 in den USA mit

einem Plus 10.9% leicht rückläufig ist, stieg sie in Europa

von 11.3% auf 12.5%. Die grösste Rendite verbuchen US

Venture Capital-Fonds mit einer internen Verzinsung von

19.1%. Private Equity erweist sich somit weiterhin als wert-

volle Anlageklasse, um Portfoliorenditen zu erhöhen.

Sowohl amerikanische als auch europäische Private Equity-

Fonds rentieren langfristig besser als der MSCI World

Index, der im gleichen Zeitraum von zehn Jahren eine Ren-

dite von 7.5% aufweist.

BERICHT DES INVESTMENT MANAGERS

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 22

23

INVESTMENT MANAGER’S REPORT

2007 was the most successful financial year for Pearl

since its inception. Over the past twelve months, the

net asset value has climbed by over 18% and ended

the year at a new all-time high of 124.45%. In view of

the turmoil in the international financial markets in

the second half of the year, this is a remarkable result.

Pearl’s most successful year to date

Despite the turmoil in the international financial markets

triggered by the subprime crisis in the US, 2007 was an

extremely successful year for Pearl. With an audited net

asset value (NAV), measured at fair market value in accord -

ance with International Financial Reporting Standards

(IFRS), of 124.45% and an increase of 18.30% over the past

twelve months, it proved to be the most successful year in

Pearl’s history, despite adverse conditions at times. This

result meant that Pearl could continue the upward trend that

it has sustained since May 2004 during the past financial

year and close the year at an all-time high. Since the bond-

holders’ meeting on the amendment of the terms and condi-

tions of the bond in December 2005, the NAV has increased

by a remarkable 33.00%, a clear indication that extending

the maturity of the bond and more intensive investment activ -

ity thanks to the favorable private equity environment have

already paid off. Inclusion of the 2% coupon, which is paid

out to the investors every September, yields a theoretical

NAV of as much as 138.95%: since its inception in 2000,

Pearl has already distributed a total of around EUR 92 million

in interest payments to the bondholders.

The record growth in the NAV of Pearl is primarily due to

revaluations of the partnerships, especially those in the buy-

out sector, and the direct investments in the Pearl portfolio

that were effected during the course of the year on the back

of the positive private equity environment. This is attribu -

table, in particular, to the greater maturity of the portfolio:

now, in the post-investment period, the underlying partner -

ships are gradually realizing the investments that have per-

formed well and are distributing the proceeds to the inves-

tors. To be revalued were, among others, the secondary

portfolio Partners Group SPP1 Limited and the buyout

partnerships Global PE Fund IV, Newbridge III and EQT IV.

The turmoil in the global financial markets meant that the

year did not go so smoothly for the listed private equity

companies, which at year’s end constituted 5% of the Pearl

portfolio. Both the short-lived crisis at the end of February

and the slump in share prices during the summer months

adversely impacted their performance. The partnerships and

Das Geschäftsjahr 2007 war für Pearl das erfolg-

reichste Jahr seit Auflegung. Der Innere Wert stieg in

den vergangenen zwölf Monaten um über 18% und

beendete das Jahr auf einem neuen Höchststand von

124.45%. In Anbetracht der Turbulenzen an den

internationalen Finanzmärkten in der zweiten Hälfte

des Jahres stellt dieser Anstieg ein beeindruckendes

Ergebnis dar.

Erfolgreichstes Jahr für Pearl

Trotz der durch die Subprime-Krise in den USA ausgelös -

ten Turbulenzen an den internationalen Finanzmärkten

war 2007 für Pearl ein äusserst erfolgreiches Jahr. Mit

einem geprüften Inneren Wert (NAV) bewertet nach IFRS-

Rechnungslegungsstandard zu fairen Marktwerten von

124.45% und einem Zuwachs von 18.30% über die ver-

gangenen zwölf Monate war es trotz teilweise widriger

Bedingungen das erfolgreichste Jahr in der Geschichte

von Pearl. Mit diesem Ergebnis konnte Pearl im abgelau-

fenen Geschäftsjahr den seit Mai 2004 anhaltenden Auf-

wärtstrend weiter fortsetzen und schloss das Jahr auf

einem Allzeithoch. Seit der Obligationärsversammlung zur

Anpassung der Anleihebedingungen im Dezember 2005

stieg der NAV gar um beachtliche 33.00%, ein deutliches

Zeichen dafür, dass sich die Laufzeitverlängerung und die

durch das freundliche Private Equity-Umfeld intensivere

Investitionsaktivität bereits ausgezahlt haben. Berück-

sichtigt man zudem noch den 2%igen Zinskupon, der

jeweils im September an die Investoren ausbezahlt wird,

resultiert sogar ein theoretischer Innerer Wert von

138.95%: Seit Auflegung im Jahr 2000 hat Pearl nämlich

bereits insgesamt Zinszahlungen von rund EUR 92 Mio. an

die Anleiheninhaber ausgeschüttet.

Der Rekordzuwachs des Inneren Wertes von Pearl ist vor

allem auf Neubewertungen der Partnerships, besonders

im Buyout-Bereich, und der Direktbeteiligungen im Pearl-

Portfolio zurückzuführen, welche im Laufe des Jahres

aufgrund des positiven Private Equity-Umfeldes vor-

genommen werden konnten. Verantwortlich dafür ist

besonders der fortgeschrittene Reifegrad des Portfolios,

da die dem Portfolio zugrunde liegenden Partnerships

nach Zeiten der Investitionen nun ihre Beteiligungen,

die sich gut entwickelt haben, nach und nach veräussern

und Ausschüttungen an die Investoren vornehmen.

Aufgewertet wurden unter anderem das Sekundärport -

folio Partners Group SPP1 Limited, sowie die Buyout-

Partnerships Global PE Fund IV, Newbridge III oder EQT

IV.

WERTENTWICKLUNG DES PEARL-PORTFOLIOSPERFORMANCE OF THE PEARL PORTFOLIO

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 23

24

BERICHT DES INVESTMENT MANAGERS

the direct investments in the Pearl portfolio remained

unscathed by developments in the international equity

markets. On the contrary, thanks to revaluations the fall in

the share prices of the listed private equity companies could

be more than offset, as clearly reflected in the end-of-year

results.

Mid-market price climbs by 6%

The mid-market price of Pearl stood at 103.75% at the end

of 2007, representing a gain of 5.87% year on year and, at

the same time, a discount of 16.63% to the NAV. The bond

price continues to be well above the bond floor, underlining

the upside potential of the underlying portfolio.

Für die börsennotierten Beteiligungsgesellschaften, welche

zum Jahresende 5% des Portfolios ausmachten, verlief das

Jahr aufgrund der Turbulenzen an den globalen Finanz-

märkten weniger reibungslos. Sowohl die kurzfristige Krise

Ende Februar als auch die Kurseinbrüche während der

Sommermonate wirkten sich negativ auf deren Entwicklung

aus. Die Partnerships und Direktinvestitionen im Pearl-Port-

folio wurden von den Entwicklungen an den internationalen

Aktienmärkten nicht in Mitleidenschaft gezogen, im Gegen-

teil, sie konnten dank Aufwertungen die Einbrüche bei den

börsennotierten Beteiligungsgesellschaften mehr als aus-

gleichen, was sich im Jahresendergebnis deutlich wider-

spiegelt.

Mittelkurs steigt um 6%

Der Mittelkurs von Pearl steht per Jahresende bei 103.75%,

was einem Anstieg von 5.87% gegenüber dem Vorjahr und

gleichzeitig einem Abschlag von 16.63% auf den Inneren

Wert entspricht. Der Preis der Anleihe liegt weiterhin deut-

lich über dem Bond-Floor, was das Upside-Potenzial des

zugrundeliegenden Portfolios unterstreicht.

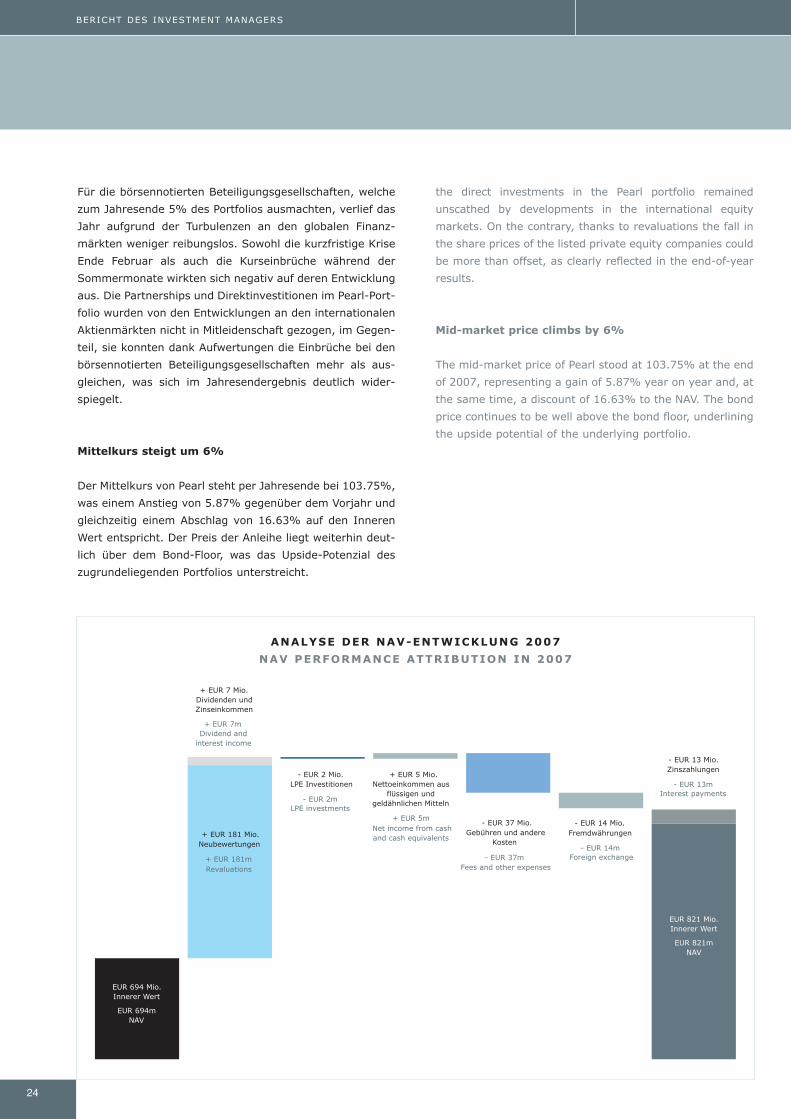

ANALYSE DER NAV-ENTWICKLUNG 2007

NAV PERFORMANCE ATTRIBUTION IN 2007

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:19 Uhr Seite 24

25

INVESTMENT MANAGER’S REPORT

30 new investments

A high level of commitment activity was again kept up in

2007 so as to maintain a full investment level. A total of 14

new capital commitments were made to primary funds,

whereby the focus was on buyout investments in North

America and Europe. Pearl, however, also made individual

commitments in the venture capital and special situations

sectors. During the course of the year, nine secondary port-

folios were also acquired and seven direct investments

were made. During the past financial year, commitments in

the order of EUR 121 million were thus spoken.

Pearl maintained an overcommitment level (undrawn commit-

ments less net liquidity divided by the NAV) of around 27% at

the end of the year. This overcommitment strategy, which

defines the size and the timing of commitments based on

modeled and actual distribution flows from the portfolio

investments, enables Pearl to maintain a full investment level.

By the end of 2007, the Pearl portfolio comprised 191 part-

nerships (thereof 160 primary investments and 31 second -

ary investments), 33 direct investments and 39 listed pri-

vate equity companies.

Continued high level of investment activity

Capital calls were slightly up from the EUR 167 million of the

previous year, but did not quite manage to match the record

level of 2005. A total of EUR 175 million was drawn down for

investments by the partnerships as well as for direct invest-

ments. At 74%, the lion’s share went once again to buyout,

followed by 18% for venture capital and 8% for special situ-

ations financings. Last year, direct investments were made in,

among others, US-headquartered Micro-Poise Measurement

Systems, a provider of measurement and inspection systems