Embed Size (px)

Citation preview

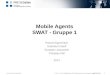

SHG MeMberS aS bank aGentS

a replication Guide for StakeHolderS

germancooperationDEUTSCHE ZUSAMMENARBEIT

Published bydeutsche Gesellschaft für internationale Zusammenarbeit (GiZ) Gmbh

Rural Financial institutions Programme

ContaCtdr. detlev holloh, GiZ Programme director

a 2/18, safdarjung enclave new delhi 110 029 / indiaPhone: +91-11-4949 5353telefax: +91-11-4949 5393email: [email protected] homepage: www.giz.de

ResPonsibleJonna bickel, amit arora

authoRswati Mehta, abhishek lahiri

editoRnitin Jindal

aRt diReCtoRanshul sharma/artworkstudios.in

new delhi, oCtobeR 2015

germancooperationDEUTSCHE ZUSAMMENARBEIT

SHG MeMberS aS bank aGentS

a replication Guide for StakeHolderS

List of Abbreviations .................................................................................................................................................... 3

Preface .............................................................................................................................................................................. 5

Introduction .................................................................................................................................................................... 6

Piloting SHG Members as Bank Agents in Uttar Pradesh and Madhya Pradesh ....................................................................................................................... 7

Deciding on the Partnership Model ....................................................................................................................... 9

Choosing Front-End Technology ............................................................................................................................. 16

Setting up the Bank Sakhi Network ........................................................................................................................ 22

Ensuring that there is a Business Case ................................................................................................................... 33

Conclusion ....................................................................................................................................................................... 41

contents

4 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

ATM Automated Teller Machines

BC Business Correspondent

BCA Business Correspondent Agent

BF Business Facilitator

BLA Block-Level Association

BSBDA Basic Savings Bank Deposit Account

CBS Core Banking System

CF Community Facilitator

CGAP Consultative Group to Assist the Poor

CSC Common Service Centre

CSP Customer Service Point

FD Fixed Deposit

FI Financial Inclusion

FLCC Financial Literacy and Credit Counselling Centre

GBA Gramin Bank of Aryavart

G2P Government to People

GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit

GPRS General Packet radio Service

HR Human resource

ICT Information and Communications Technology

liSt of abbreviationS

RuRal Financial institutions PRogRamme 5

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

IT Information Technology

KYC know Your Customer

MIS Management Information System

MOU Memorandum of Understanding

NABARD National Bank for Agriculture and rural Development

NJGB Narmada Jhabua Gramin Bank

NPA Non-Performing Assets

NPCI National Payments Corporation of India

OD over Draft

PIN Personal Identification Number

POS Point of Sale

RBI reserve Bank of India

RD recurring Deposit

RFIP rural Financial Institutions Programme

RRB regional rural Bank

SHG Self-Help Group

SHG-BLP Self-Help Group Bank Linkage Programme

SHPI Self-Help Group Promoting Institution

TSP Technology Service Provider

VO Village organisation

6 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

preface

As of March 2015, 398 million basic savings depos-it accounts (BSBDAs) have been opened through 553,713 rural banking outlets. However, dormant agents and inactive accounts pose critical challeng-es. replicable and sustainable business models of BCs are yet to evolve. Started in the early 1990s, the National Bank for Ag-riculture and rural Development’s (NABArD’s) Self-

Theintroduction of the Business Correspondent (BC) model in 2006 is considered an important

milestone in India’s financial inclusion strategy. Since then, significant progress has been made in terms of increasing penetration in rural areas and improving access for the unbanked and under-banked households across the country.

RuRal Financial institutions PRogRamme 7

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Help Group Bank Linkage Programme (SHG BLP) reached out to more than 74 lakh Self-Help Groups (SHGs) and about 89 million households across the country. The programme has tried to develop the capacity of group members and member-based in-stitutions to manage money and financial services, and to connect the community to formal financial institutions. However, the movement is facing chal-lenges, such as large non-performing assets, low take-up of voluntary savings, slow digitisation of SHG data, and the absence of records about individ-ual members. All of these limit the graduation from being a bank client through a group approach into an individual banking client.In 2012, the rural Financial Institutions Programme (rFIP), a bilateral cooperation programme, jointly implemented by NABArD and GIZ, decided to con-nect these two approaches with an objective to im-prove the integration of bank agents into the com-munity by appointing SHG members as agents or Customer Service Points (CSPs). The underlying as-sumption was that by having agents who are part of and selected by the community, the uptake and usage of financial services by other community members would increase. These agents would not discontinue serving the accounts opened by them, and SHGs and their members would become part of the financial inclusion drive.The approach has been tested with two pilot pro-jects conducted in geographically diverse locations

of Uttar Pradesh and Madhya Pradesh. The experi-ence from the twin pilot projects has demonstrat-ed better performance for Bank Sakhis vis-à-vis the conventional agents in terms of lower dor-mancy, fewer inactive accounts, and lower agent attrition level combined with high customer satis-faction. on the basis of this positive development, the rFIP has shared this approach with a range of stakeholders and received positive feedback and interest to replicate the model in other areas across the country. This replication Guide has been developed as a reference for stakeholders who are interested in adopting this model as part of their financial in-clusion strategy. It is based on the experiences from the twin pilot projects and is meant to help with the decision-making process on the critical aspects of replication of this model. This guide can be used by banks, SHG federations and pro-moting institutions, corporate BCs, donors, and any other institution which is involved in devel-oping a financial inclusion strategy under the BC ecosystem. We take this opportunity to acknowledge the support received from our partner banks and in-stitutions in the two pilot projects. Their contribu-tion towards the implementation of the projects which form the basis of this guide is immensely valued.

About RFIP

The rural Financial Institutions Programme (rFIP) is a bilateral cooperation programme, jointly implemented by the Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) on behalf of the Government of the Federal republic of Germany, and the National Bank for Agriculture and rural Development (NABArD) on behalf of the Government of India. It aims at improving access to sustainable and demand-oriented financial services through the institutions of the rural cooperative credit system, microfinance organisations, and banks and their Business Correspondents (BCs). The German Government and NABArD have supported the Self-Help Group (SHG) model and especially the Bank Linkage Programme (BLP) since its inception. over the last few years, the financial inclusion (FI) drive of the Government of India, with its focus on individual banking opportunities for rural and low-income households through banks and their agent network, has led to a change in the environment of the SHGs. With the purpose of establishing SHG members as bank agents, the rFIP aims at two things:

1. Integrating the SHG movement into the FI drive and utilising the existing infrastructure of groups, federations, and supporting agencies, which have been developed in the last two decades

2. Improving the quality of FI efforts by establishing sustainable business models for agents

1 introduction

About this guide for replication

The ensuing sections describe the different stages that stakeholders will go through along the process of implementing the programme. With each attempt at replication, decisions about partnership arrangements, technology options, the operational process as well as which services to offer including their pricing will need to be made at a local level between all stakeholders involved in the implementation. The local context and existing infrastructure need to be taken into consideration. This guide can only offer and present different options and possibilities based on our experiences, but the final decisions need to be made by the implementing partners. The key steps in the implementation are as follows:

• Step 1: Deciding on the partnership model

• Step 2: Choosing the front-end technology

• Step 3: Setting up the Bank Sakhi network

• Step 4: Ensuring that there is a business case

RuRal Financial institutions PRogRamme 9

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

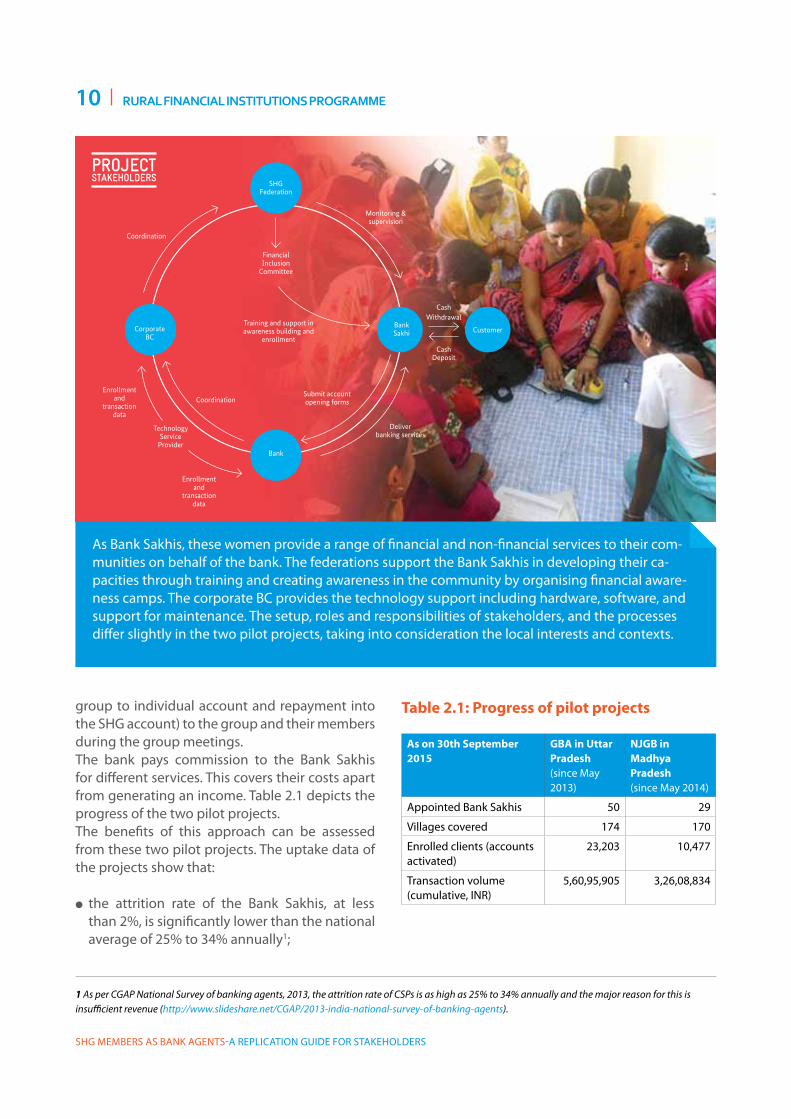

2 piloting SHG members as bank agents in uttar pradesh and Madhya pradesh

The rFIP supported two pilot projects to test the potential of establishing SHG members as bank agents. In

May 2013, the first pilot project was launched in collaboration with the Gramin Bank of Aryavart (GBA) in the Unnao District of Uttar Pradesh. The second pilot project was started with Narmada Jhabua Gramin Bank (NJGB) in May 2014, under NABArD’s guidance, in the Indore District of Madhya Pradesh, and later extended to Dewas District. The objective of these pilots was to test the uptake and challenges of this model in different parts of the country with the adoption of different partners, business models, and technologies.In both the projects, the banks partnered with a local federation, corporate BC, and technology service provider. The SHG members of the federation were appointed as bank agents through the corporate BC and were called “Bank Sakhis”. A Bank Sakhi is someone who has been a member of a SHG and has been involved in conducting banking and bookkeeping activities of the group.The Bank Sakhis offer BC and Business Facilitator (BF) services to the community members. The services include opening of savings account, recurring deposits and fixed deposits; making deposits and withdrawals; transferring money; delivering notices to loan defaulters; and recovering loans. Depending on the agreement between the bank and the corporate BC as well as between the corporate BC

and the Bank Sakhis, the agents also offer other services such as linking the Aadhaar number with bank accounts, insurance policies, and vehicle or solar home lighting system loans. Bank Sakhis are equipped with micro automated teller machines (ATMs) or laptops and can offer these services on real-time basis through the FI server of the corporate BC and/or the Core Banking System (CBS) of the bank.The Bank Sakhis in the Madhya Pradesh project also offer non-financial services through the Common Service Centre (CSC) portal. Apart from providing utility services that include mobile phone recharge, television recharge, bill and insurance premium payment, they also give e-governance services such as PAN card enrolment and Aadhaar card printing. on behalf of the federation, the Bank Sakhis also function as SHG managers and conduct SHG meetings and update their books. They can also conduct SHG transactions (savings and loan repayments) through their kiosk during the meetings. In Uttar Pradesh, the GBA has gone one step further and enabled the Bank Sakhis to debit money from the group account through the BC system. For this at least two office bearers from the SHG are required to verify the transaction through card and biometric authentication process at the BC level. Bank Sakhis can provide all kinds of banking services (such as disbursement from

10 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

group to individual account and repayment into the SHG account) to the group and their members during the group meetings.The bank pays commission to the Bank Sakhis for different services. This covers their costs apart from generating an income. Table 2.1 depicts the progress of the two pilot projects.The benefits of this approach can be assessed from these two pilot projects. The uptake data of the projects show that:

l the attrition rate of the Bank Sakhis, at less than 2%, is significantly lower than the national average of 25% to 34% annually1;

Financial Inclusion

Committee

Training and support in awareness building and

enrollment

Submit account opening formsCoordination

Coordination

Bank

Technology Service

Provider

SHG Federation

Monitoring & supervision

Bank Sakhi

Deliver banking services

Cash Deposit

Cash Withdrawal

CustomerCorporate BC

Enrollment and

transaction data

Enrollment and

transaction data

ProjectStakeholderS

As on 30th September 2015

GBA in Uttar Pradesh (since May 2013)

NJGB in Madhya Pradesh(since May 2014)

Appointed Bank Sakhis 50 29

Villages covered 174 170

Enrolled clients (accounts activated)

23,203 10,477

Transaction volume (cumulative, INr)

5,60,95,905 3,26,08,834

Table 2.1: Progress of pilot projects

1 As per CGAP National Survey of banking agents, 2013, the attrition rate of CSPs is as high as 25% to 34% annually and the major reason for this is insufficient revenue (http://www.slideshare.net/CGAP/2013-india-national-survey-of-banking-agents).

As Bank Sakhis, these women provide a range of financial and non-financial services to their com-munities on behalf of the bank. The federations support the Bank Sakhis in developing their ca-pacities through training and creating awareness in the community by organising financial aware-ness camps. The corporate BC provides the technology support including hardware, software, and support for maintenance. The setup, roles and responsibilities of stakeholders, and the processes differ slightly in the two pilot projects, taking into consideration the local interests and contexts.

RuRal Financial institutions PRogRamme 11

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

l The SHG members are integrated into the community (through their own group- and village-level organisations) and the other community members know and trust them. They are also more likely to stay within the community and not migrate for other job opportunities.

l The SHG members possess the fundamental financial literacy and are used to dealing with money (both their own and group members). They also have experience working with banks and other financial institutions.

l The SHG members are mostly women and are generally perceived as being more responsible and trustworthy with money. These women are also able to tap women - the part of the population which is mostly financially excluded, but provides the highest potential.

l As regional rural Banks (rrBs) are a key provider of credit under the SHG-BLP, the delivery of credit and its repayment through BC agents will not only help the banks keep track of credit flows but also migrate SHG-based transactions to the BC channel. This will ensure that post disbursement, the funds remain with the bank (in savings accounts of the group or its members) for a longer time, due to convenience of doorstep services.

l on an average, the conventional bank agents of the same bank have a higher percentage of inactive accounts. Both in Uttar Pradesh and in Madhya Pradesh, more than 40% of the accounts served by the Bank Sakhis have been active (at least one transaction in the last three months). While only 6% and 11% of the accounts served by conventional Customer Service Points (CSPs) in Uttar Pradesh and Madhya Pradesh respectively, have been transacted in the last three months; and

l the accounts opened by the Bank Sakhis have a higher savings balance and a higher proportion of deposit transactions compared to other BC agents of the same bank.

The following chapters describe the stepwise approach to replicating the approach:

• Step 1: Deciding on the partnership model• Step 2: Choosing the front-end technology• Step 3: Setting up the Bank Sakhi network• Step 4: Ensuring that there is a business case

Advantages of SHG members as Bank Sakhis

12 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Overview

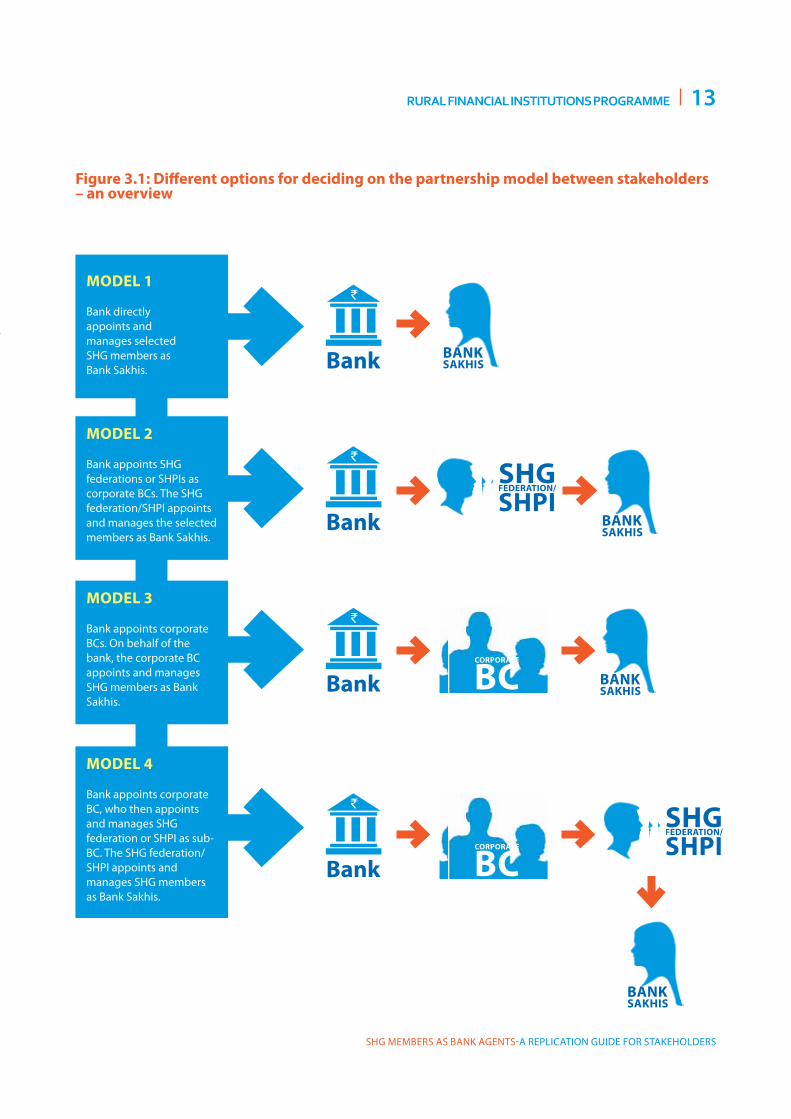

This section details the four different options (Figure 3.1)2 available to set up and implement the best partner-

ship model. In order to implement the model, a partnership between different stakeholders is required. Essential partners are the bank, who would like to engage SHG members as its agents or CSPs, and the SHG members who get appoint-ed as a CSP and are called Bank Sakhis. In many cases, the bank works with a corporate BC who acts as aggregator of CSPs and manages them. Depending upon the model selected, SHG feder-ations and/or Self-Help Group Promoting Institu-tions (SHPIs) could also support the Bank Sakhis and play a crucial role. It is up to the partners and their context to de-cide on the best partnership model. This decision will influence the respective roles and responsi-bilities of stakeholders as well as the processes to be implemented. The partners need to carefully weigh the pros and cons of the different options and select the one which is most suited for their overall strategy and the local context. In all the models, the stakeholders and the partners are closely interlinked with each other and, therefore, irrespective of the formal partnership model, all stakeholders interact with each other while per-forming their functions.This section describes these models, the roles

3 deciding on the partnership model

and responsibilities of the stakeholders under each model, and the pros and cons of each option.

Note: Another critical stakeholder is the Technology Service Provider (TSP) which is present in all the four op-tions. Its main role is to provide technology integration support to the bank. It does not directly interface with the customers and other front-end stakeholders except the bank and the corporate BC (in the case of options 3 and 4). TSP’s key responsibilities are to ensure seam-less transactions, manage FI server/gateway, generate MIS reports as per the bank’s needs, upgrade technol-ogy, and troubleshoot technology issues (hardware/software, as the case may be). In some cases, the TSP may also play the role of a corporate BC and will have to undertake roles as per options 3 and 4 described in the ensuing sections.

2 The list of these four models is not exhaustive, but these are what the RFIP has come across through its experience in this area.

RuRal Financial institutions PRogRamme 13

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Figure 3.1: Different options for deciding on the partnership model between stakeholders – an overview

MODel 1

Bank directly appoints and manages selected SHG members as Bank Sakhis.

MODel 2

Bank appoints SHG federations or SHPIs as corporate BCs. The SHG federation/SHPI appoints and manages the selected members as Bank Sakhis.

MODel 3

Bank appoints corporate BCs. on behalf of the bank, the corporate BC appoints and manages SHG members as Bank Sakhis.

Model 4

Bank appoints corporate BC, who then appoints and manages SHG federation or SHPI as sub-BC. The SHG federation/SHPI appoints and manages SHG members as Bank Sakhis.

SHG FeDeRATION/

SHPI

Bank

`

Bank

`

Bank

`

Bank

`

SHG FeDeRATION/

SHPI

BANk SAkHIS

BANk SAkHIS

BANk SAkHIS

BANk SAkHIS

CORPORATe

BC

CORPORATe

BC

14 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

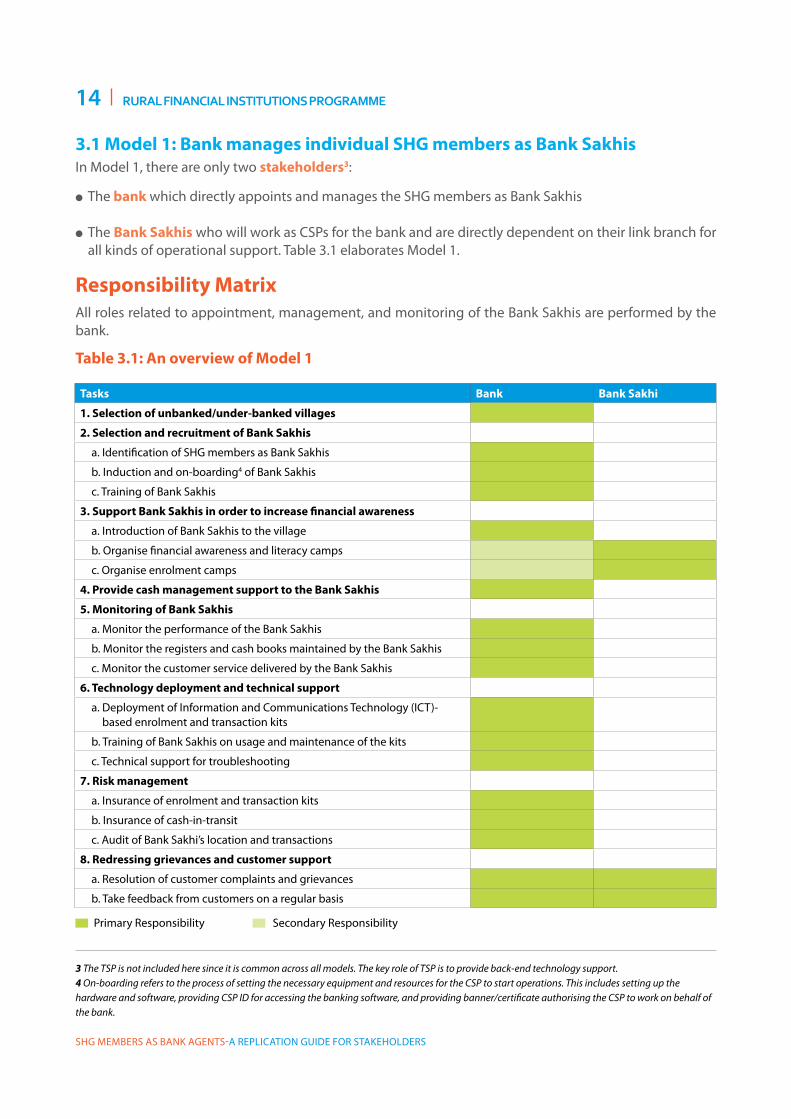

Tasks Bank Bank Sakhi

1. Selection of unbanked/under-banked villages

2. Selection and recruitment of Bank Sakhis

a. Identification of SHG members as Bank Sakhis

b. Induction and on-boarding4 of Bank Sakhis

c. Training of Bank Sakhis

3. Support Bank Sakhis in order to increase financial awareness

a. Introduction of Bank Sakhis to the village

b. organise financial awareness and literacy camps

c. organise enrolment camps

4. Provide cash management support to the Bank Sakhis

5. Monitoring of Bank Sakhis

a. Monitor the performance of the Bank Sakhis

b. Monitor the registers and cash books maintained by the Bank Sakhis

c. Monitor the customer service delivered by the Bank Sakhis

6. Technology deployment and technical support

a. Deployment of Information and Communications Technology (ICT)-based enrolment and transaction kits

b. Training of Bank Sakhis on usage and maintenance of the kits

c. Technical support for troubleshooting

7. Risk management

a. Insurance of enrolment and transaction kits

b. Insurance of cash-in-transit

c. Audit of Bank Sakhi’s location and transactions

8. Redressing grievances and customer support

a. resolution of customer complaints and grievances

b. Take feedback from customers on a regular basis

Table 3.1: An overview of Model 1

3.1 Model 1: Bank manages individual SHG members as Bank SakhisIn Model 1, there are only two stakeholders3:

l The bank which directly appoints and manages the SHG members as Bank Sakhis

l The Bank Sakhis who will work as CSPs for the bank and are directly dependent on their link branch for all kinds of operational support. Table 3.1 elaborates Model 1.

Responsibility MatrixAll roles related to appointment, management, and monitoring of the Bank Sakhis are performed by the bank.

3 The TSP is not included here since it is common across all models. The key role of TSP is to provide back-end technology support.4 On-boarding refers to the process of setting the necessary equipment and resources for the CSP to start operations. This includes setting up the hardware and software, providing CSP ID for accessing the banking software, and providing banner/certificate authorising the CSP to work on behalf of the bank.

Primary responsibility Secondary responsibility

RuRal Financial institutions PRogRamme 15

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

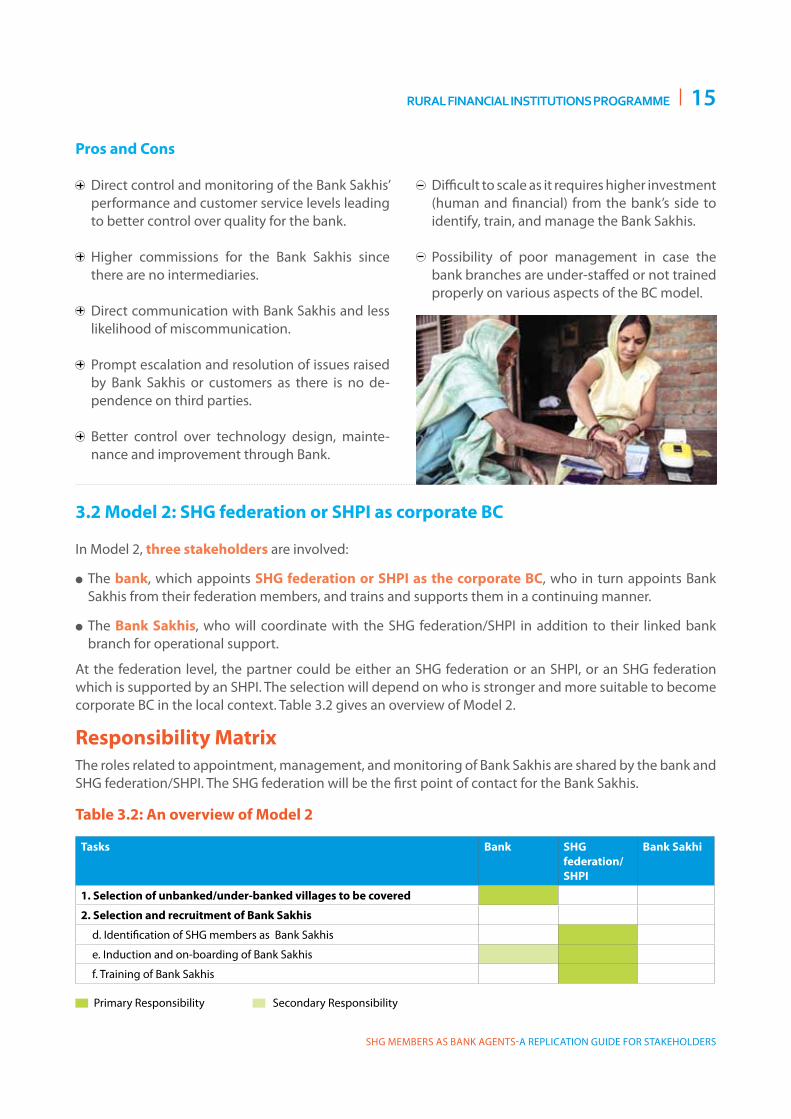

Table 3.2: An overview of Model 2

Responsibility MatrixThe roles related to appointment, management, and monitoring of Bank Sakhis are shared by the bank and SHG federation/SHPI. The SHG federation will be the first point of contact for the Bank Sakhis.

Pros and Cons

Direct control and monitoring of the Bank Sakhis’ performance and customer service levels leading to better control over quality for the bank.

Higher commissions for the Bank Sakhis since there are no intermediaries.

Direct communication with Bank Sakhis and less likelihood of miscommunication.

Prompt escalation and resolution of issues raised by Bank Sakhis or customers as there is no de-pendence on third parties.

Better control over technology design, mainte-nance and improvement through Bank.

Tasks Bank SHG federation/SHPI

Bank Sakhi

1. Selection of unbanked/under-banked villages to be covered

2. Selection and recruitment of Bank Sakhis

d. Identification of SHG members as Bank Sakhis

e. Induction and on-boarding of Bank Sakhis

f. Training of Bank Sakhis

Primary responsibility Secondary responsibility

Difficult to scale as it requires higher investment (human and financial) from the bank’s side to identify, train, and manage the Bank Sakhis.

Possibility of poor management in case the bank branches are under-staffed or not trained properly on various aspects of the BC model.

3.2 Model 2: SHG federation or SHPI as corporate BC

In Model 2, three stakeholders are involved:

l The bank, which appoints SHG federation or SHPI as the corporate BC, who in turn appoints Bank Sakhis from their federation members, and trains and supports them in a continuing manner.

l The Bank Sakhis, who will coordinate with the SHG federation/SHPI in addition to their linked bank branch for operational support.

At the federation level, the partner could be either an SHG federation or an SHPI, or an SHG federation which is supported by an SHPI. The selection will depend on who is stronger and more suitable to become corporate BC in the local context. Table 3.2 gives an overview of Model 2.

16 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

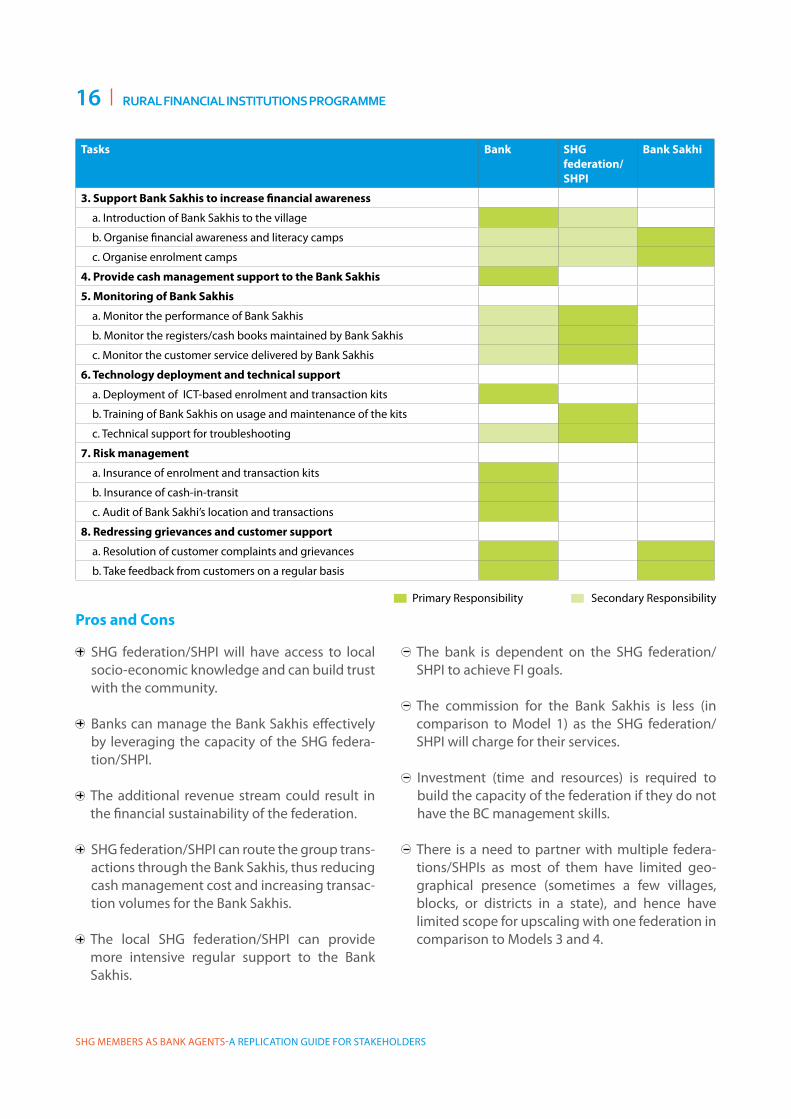

Tasks Bank SHG federation/SHPI

Bank Sakhi

3. Support Bank Sakhis to increase financial awareness

a. Introduction of Bank Sakhis to the village

b. organise financial awareness and literacy camps

c. organise enrolment camps

4. Provide cash management support to the Bank Sakhis

5. Monitoring of Bank Sakhis

a. Monitor the performance of Bank Sakhis

b. Monitor the registers/cash books maintained by Bank Sakhis

c. Monitor the customer service delivered by Bank Sakhis

6. Technology deployment and technical support

a. Deployment of ICT-based enrolment and transaction kits

b. Training of Bank Sakhis on usage and maintenance of the kits

c. Technical support for troubleshooting

7. Risk management

a. Insurance of enrolment and transaction kits

b. Insurance of cash-in-transit

c. Audit of Bank Sakhi’s location and transactions

8. Redressing grievances and customer support

a. resolution of customer complaints and grievances

b. Take feedback from customers on a regular basis

Pros and Cons

SHG federation/SHPI will have access to local socio-economic knowledge and can build trust with the community.

Banks can manage the Bank Sakhis effectively by leveraging the capacity of the SHG federa-tion/SHPI.

The additional revenue stream could result in the financial sustainability of the federation.

SHG federation/SHPI can route the group trans-actions through the Bank Sakhis, thus reducing cash management cost and increasing transac-tion volumes for the Bank Sakhis.

The local SHG federation/SHPI can provide more intensive regular support to the Bank Sakhis.

Primary responsibility Secondary responsibility

The bank is dependent on the SHG federation/SHPI to achieve FI goals.

The commission for the Bank Sakhis is less (in comparison to Model 1) as the SHG federation/SHPI will charge for their services.

Investment (time and resources) is required to build the capacity of the federation if they do not have the BC management skills.

There is a need to partner with multiple federa-tions/SHPIs as most of them have limited geo-graphical presence (sometimes a few villages, blocks, or districts in a state), and hence have limited scope for upscaling with one federation in comparison to Models 3 and 4.

RuRal Financial institutions PRogRamme 17

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

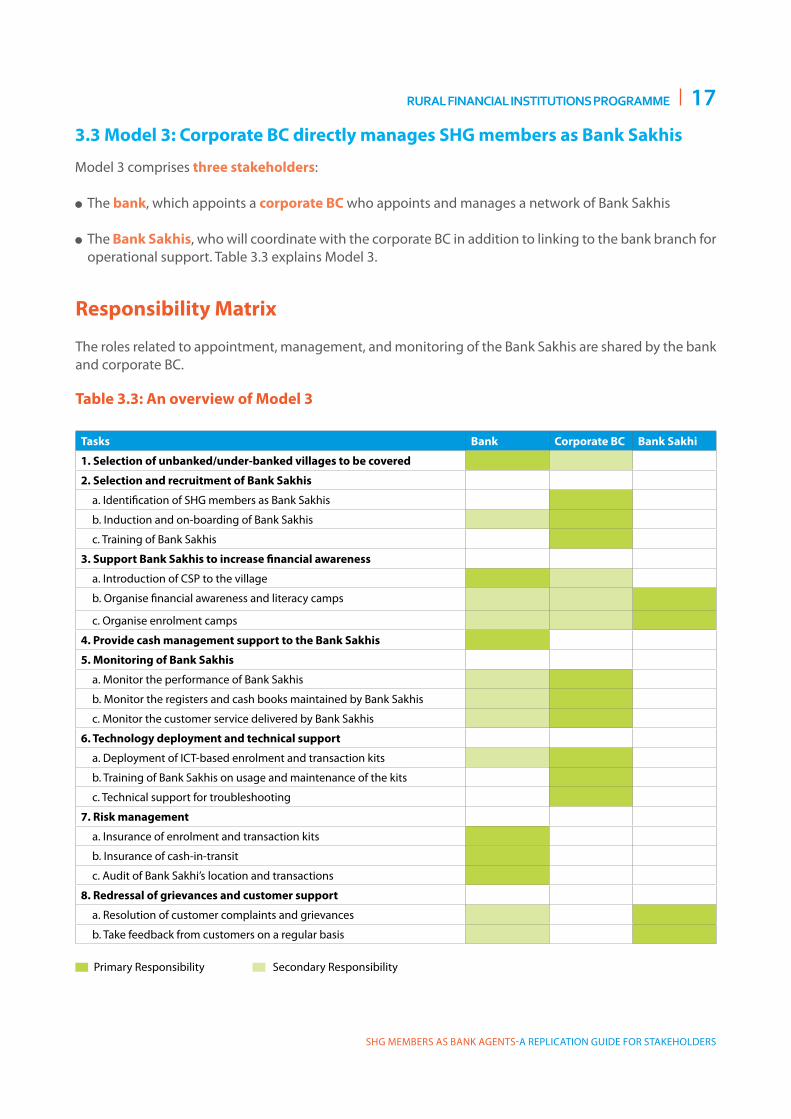

3.3 Model 3: Corporate BC directly manages SHG members as Bank Sakhis

Model 3 comprises three stakeholders:

l The bank, which appoints a corporate BC who appoints and manages a network of Bank Sakhis

l The Bank Sakhis, who will coordinate with the corporate BC in addition to linking to the bank branch for operational support. Table 3.3 explains Model 3.

Table 3.3: An overview of Model 3

Responsibility Matrix

The roles related to appointment, management, and monitoring of the Bank Sakhis are shared by the bank and corporate BC.

Tasks Bank Corporate BC Bank Sakhi

1. Selection of unbanked/under-banked villages to be covered

2. Selection and recruitment of Bank Sakhis

a. Identification of SHG members as Bank Sakhis

b. Induction and on-boarding of Bank Sakhis

c. Training of Bank Sakhis

3. Support Bank Sakhis to increase financial awareness

a. Introduction of CSP to the village

b. organise financial awareness and literacy camps

c. organise enrolment camps

4. Provide cash management support to the Bank Sakhis

5. Monitoring of Bank Sakhis

a. Monitor the performance of Bank Sakhis

b. Monitor the registers and cash books maintained by Bank Sakhis

c. Monitor the customer service delivered by Bank Sakhis

6. Technology deployment and technical support

a. Deployment of ICT-based enrolment and transaction kits

b. Training of Bank Sakhis on usage and maintenance of the kits

c. Technical support for troubleshooting

7. Risk management

a. Insurance of enrolment and transaction kits

b. Insurance of cash-in-transit

c. Audit of Bank Sakhi’s location and transactions

8. Redressal of grievances and customer support

a. resolution of customer complaints and grievances

b. Take feedback from customers on a regular basis

Primary responsibility Secondary responsibility

18 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Pros and Cons

Corporate BCs generally have a state-wide presence and can easily scale-up.

Corporate BCs work with multiple banks, and have the resources and competence for BC agent management.

Monitoring and risk management functions are stronger in the case of corporate BCs, hence the banks do not need to oversee the opera-tions directly.

Corporate BCs may not have the experience of working with SHGs.

Corporate BCs might not have detailed informa-tion about individual SHG member performance; hence the selection will be difficult.

Since the corporate BC does not have a relation-ship with the community, gaining customer trust might be difficult.

In comparison to SHG federation/SHPI, BCs, gen-erally, do not provide intensive field support to BC agents.

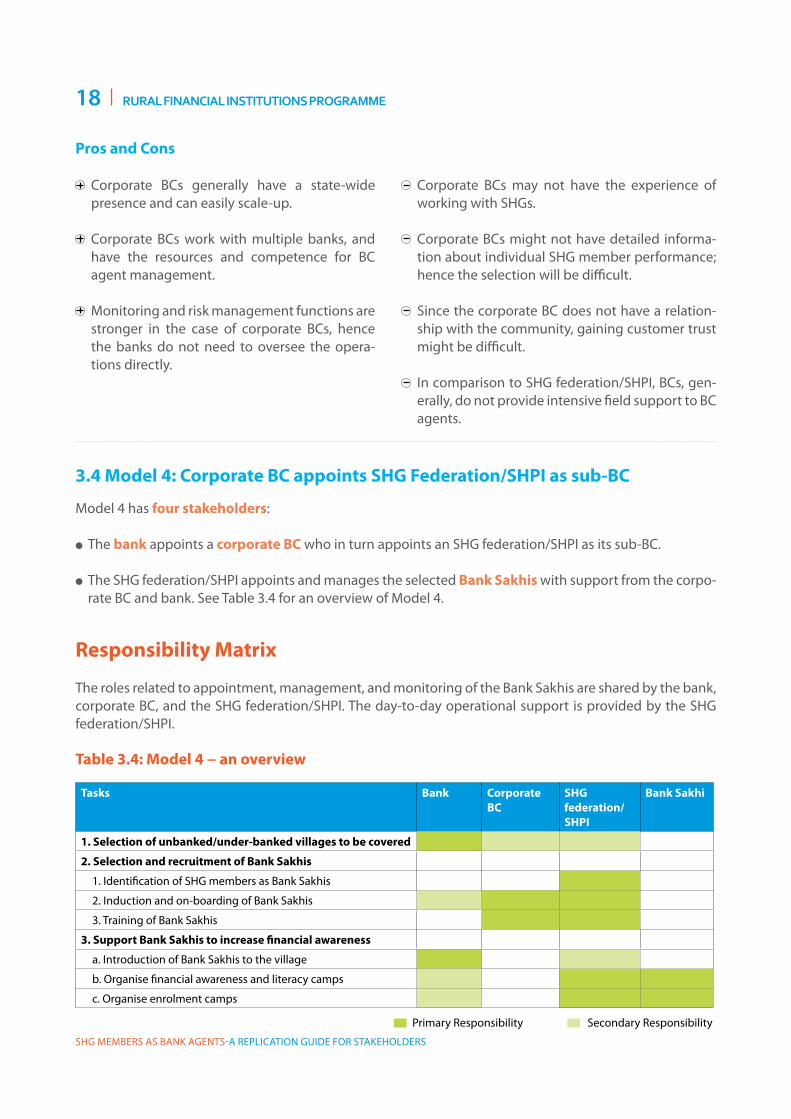

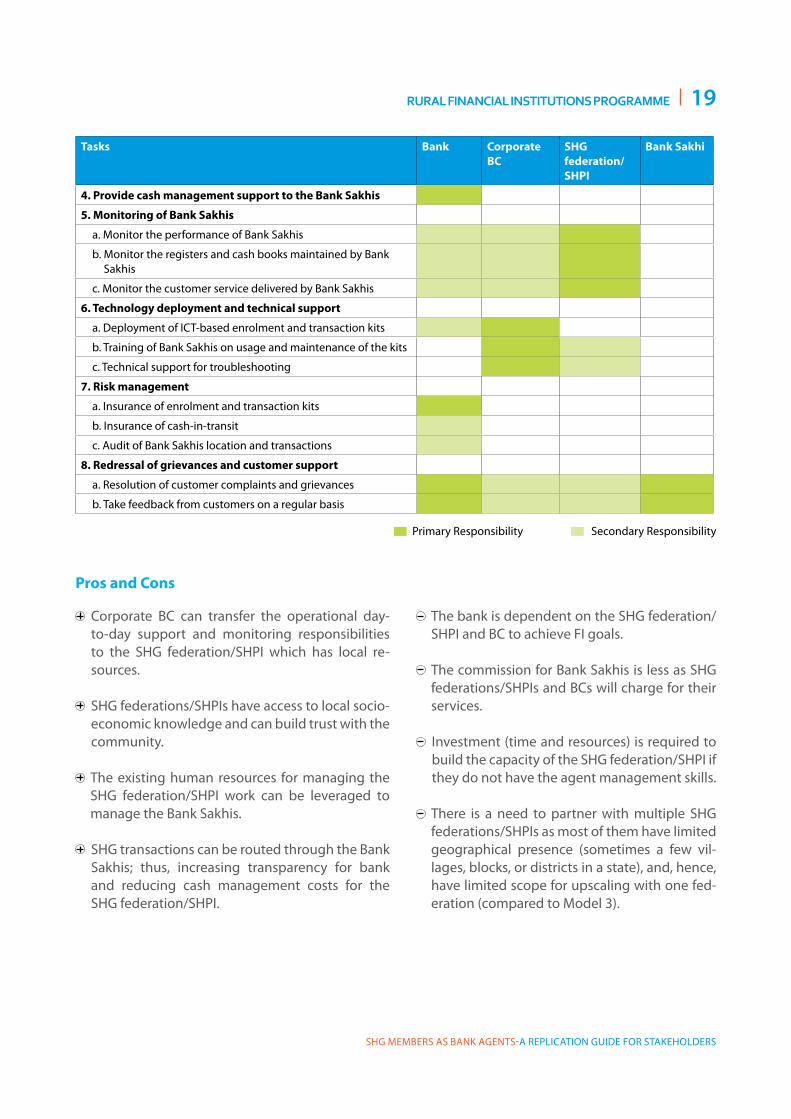

Table 3.4: Model 4 − an overview

Responsibility Matrix

The roles related to appointment, management, and monitoring of the Bank Sakhis are shared by the bank, corporate BC, and the SHG federation/SHPI. The day-to-day operational support is provided by the SHG federation/SHPI.

Tasks Bank Corporate BC

SHG federation/SHPI

Bank Sakhi

1. Selection of unbanked/under-banked villages to be covered

2. Selection and recruitment of Bank Sakhis

1. Identification of SHG members as Bank Sakhis

2. Induction and on-boarding of Bank Sakhis

3. Training of Bank Sakhis

3. Support Bank Sakhis to increase financial awareness

a. Introduction of Bank Sakhis to the village

b. organise financial awareness and literacy camps

c. organise enrolment camps

3.4 Model 4: Corporate BC appoints SHG Federation/SHPI as sub-BC

Model 4 has four stakeholders:

l The bank appoints a corporate BC who in turn appoints an SHG federation/SHPI as its sub-BC.

l The SHG federation/SHPI appoints and manages the selected Bank Sakhis with support from the corpo-rate BC and bank. See Table 3.4 for an overview of Model 4.

Primary responsibility Secondary responsibility

RuRal Financial institutions PRogRamme 19

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Tasks Bank Corporate BC

SHG federation/SHPI

Bank Sakhi

4. Provide cash management support to the Bank Sakhis

5. Monitoring of Bank Sakhis

a. Monitor the performance of Bank Sakhis

b. Monitor the registers and cash books maintained by Bank Sakhis

c. Monitor the customer service delivered by Bank Sakhis

6. Technology deployment and technical support

a. Deployment of ICT-based enrolment and transaction kits

b. Training of Bank Sakhis on usage and maintenance of the kits

c. Technical support for troubleshooting

7. Risk management

a. Insurance of enrolment and transaction kits

b. Insurance of cash-in-transit

c. Audit of Bank Sakhis location and transactions

8. Redressal of grievances and customer support

a. resolution of customer complaints and grievances

b. Take feedback from customers on a regular basis

Pros and Cons

Corporate BC can transfer the operational day-to-day support and monitoring responsibilities to the SHG federation/SHPI which has local re-sources.

SHG federations/SHPIs have access to local socio-economic knowledge and can build trust with the community.

The existing human resources for managing the SHG federation/SHPI work can be leveraged to manage the Bank Sakhis.

SHG transactions can be routed through the Bank Sakhis; thus, increasing transparency for bank and reducing cash management costs for the SHG federation/SHPI.

Primary responsibility Secondary responsibility

The bank is dependent on the SHG federation/SHPI and BC to achieve FI goals.

The commission for Bank Sakhis is less as SHG federations/SHPIs and BCs will charge for their services.

Investment (time and resources) is required to build the capacity of the SHG federation/SHPI if they do not have the agent management skills.

There is a need to partner with multiple SHG federations/SHPIs as most of them have limited geographical presence (sometimes a few vil-lages, blocks, or districts in a state), and, hence, have limited scope for upscaling with one fed-eration (compared to Model 3).

20 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

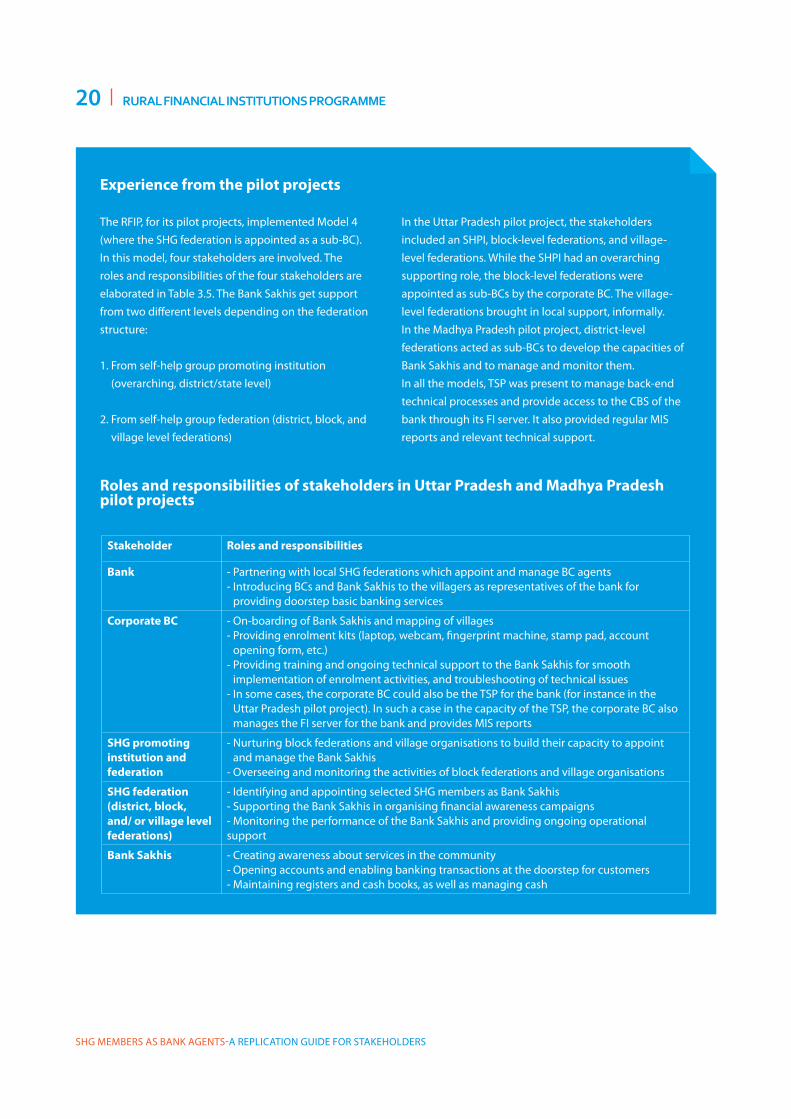

The rFIP, for its pilot projects, implemented Model 4 (where the SHG federation is appointed as a sub-BC). In this model, four stakeholders are involved. The roles and responsibilities of the four stakeholders are elaborated in Table 3.5. The Bank Sakhis get support from two different levels depending on the federation structure:

1. From self-help group promoting institution (overarching, district/state level)

2. From self-help group federation (district, block, and village level federations)

experience from the pilot projects

In the Uttar Pradesh pilot project, the stakeholders included an SHPI, block-level federations, and village-level federations. While the SHPI had an overarching supporting role, the block-level federations were appointed as sub-BCs by the corporate BC. The village-level federations brought in local support, informally. In the Madhya Pradesh pilot project, district-level federations acted as sub-BCs to develop the capacities of Bank Sakhis and to manage and monitor them.In all the models, TSP was present to manage back-end technical processes and provide access to the CBS of the bank through its FI server. It also provided regular MIS reports and relevant technical support.

Roles and responsibilities of stakeholders in Uttar Pradesh and Madhya Pradesh pilot projects

Stakeholder Roles and responsibilities

Bank - Partnering with local SHG federations which appoint and manage BC agents- Introducing BCs and Bank Sakhis to the villagers as representatives of the bank for

providing doorstep basic banking services

Corporate BC - on-boarding of Bank Sakhis and mapping of villages- Providing enrolment kits (laptop, webcam, fingerprint machine, stamp pad, account

opening form, etc.)- Providing training and ongoing technical support to the Bank Sakhis for smooth

implementation of enrolment activities, and troubleshooting of technical issues- In some cases, the corporate BC could also be the TSP for the bank (for instance in the

Uttar Pradesh pilot project). In such a case in the capacity of the TSP, the corporate BC also manages the FI server for the bank and provides MIS reports

SHG promoting institution and federation

- Nurturing block federations and village organisations to build their capacity to appoint and manage the Bank Sakhis

- overseeing and monitoring the activities of block federations and village organisations

SHG federation (district, block, and/ or village level federations)

- Identifying and appointing selected SHG members as Bank Sakhis- Supporting the Bank Sakhis in organising financial awareness campaigns- Monitoring the performance of the Bank Sakhis and providing ongoing operational support

Bank Sakhis - Creating awareness about services in the community- opening accounts and enabling banking transactions at the doorstep for customers- Maintaining registers and cash books, as well as managing cash

RuRal Financial institutions PRogRamme 21

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

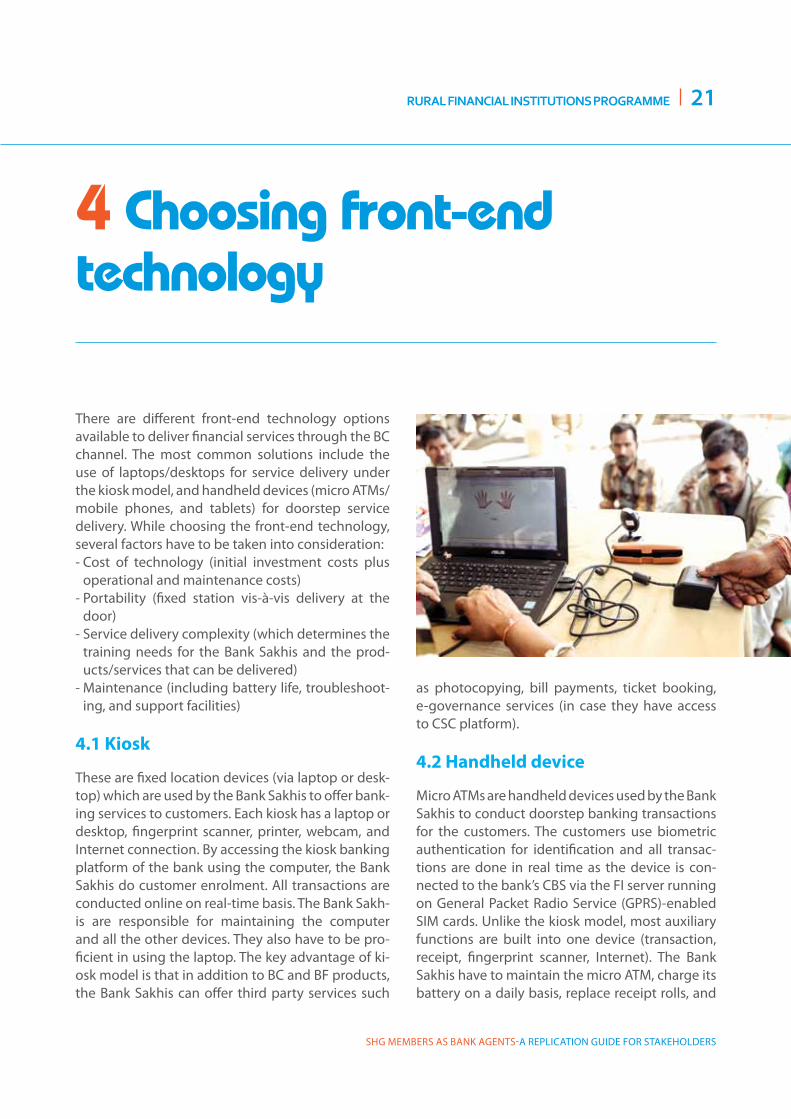

4 choosing front-end technology

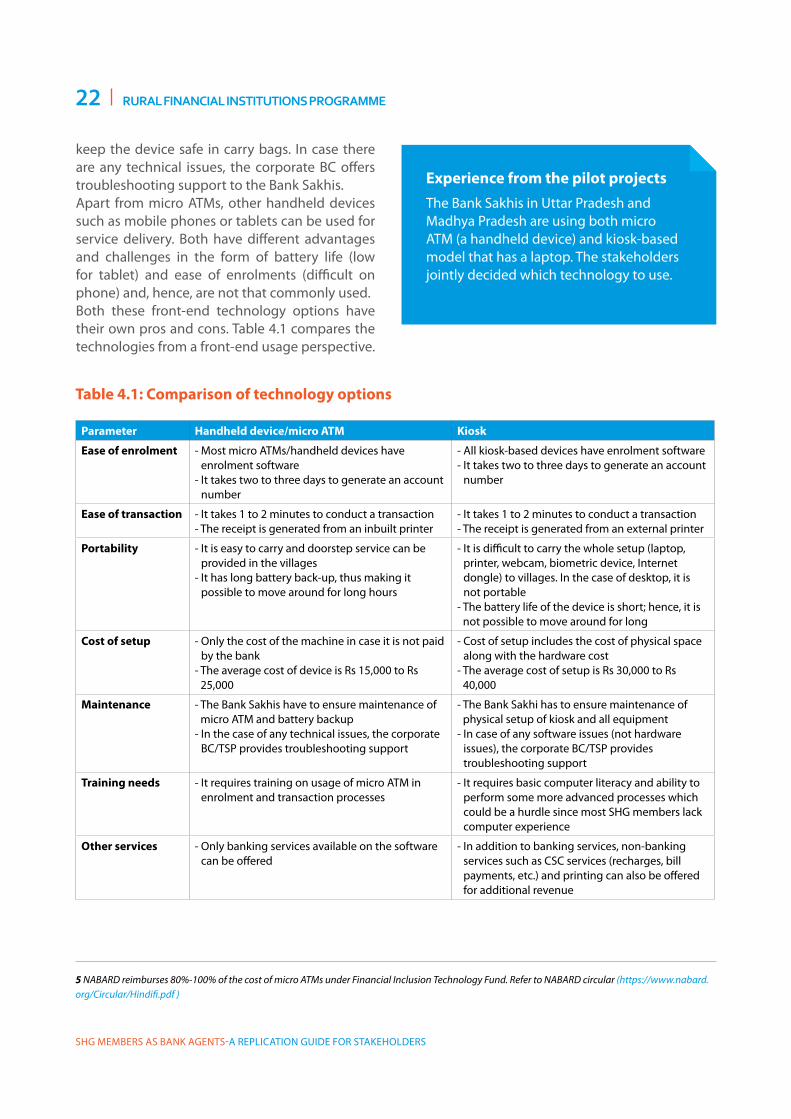

There are different front-end technology options available to deliver financial services through the BC channel. The most common solutions include the use of laptops/desktops for service delivery under the kiosk model, and handheld devices (micro ATMs/mobile phones, and tablets) for doorstep service delivery. While choosing the front-end technology, several factors have to be taken into consideration: - Cost of technology (initial investment costs plus

operational and maintenance costs)- Portability (fixed station vis-à-vis delivery at the

door)- Service delivery complexity (which determines the

training needs for the Bank Sakhis and the prod-ucts/services that can be delivered)

- Maintenance (including battery life, troubleshoot-ing, and support facilities)

4.1 Kiosk

These are fixed location devices (via laptop or desk-top) which are used by the Bank Sakhis to offer bank-ing services to customers. Each kiosk has a laptop or desktop, fingerprint scanner, printer, webcam, and Internet connection. By accessing the kiosk banking platform of the bank using the computer, the Bank Sakhis do customer enrolment. All transactions are conducted online on real-time basis. The Bank Sakh-is are responsible for maintaining the computer and all the other devices. They also have to be pro-ficient in using the laptop. The key advantage of ki-osk model is that in addition to BC and BF products, the Bank Sakhis can offer third party services such

as photocopying, bill payments, ticket booking, e-governance services (in case they have access to CSC platform).

4.2 Handheld device

Micro ATMs are handheld devices used by the Bank Sakhis to conduct doorstep banking transactions for the customers. The customers use biometric authentication for identification and all transac-tions are done in real time as the device is con-nected to the bank’s CBS via the FI server running on General Packet radio Service (GPrS)-enabled SIM cards. Unlike the kiosk model, most auxiliary functions are built into one device (transaction, receipt, fingerprint scanner, Internet). The Bank Sakhis have to maintain the micro ATM, charge its battery on a daily basis, replace receipt rolls, and

22 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

keep the device safe in carry bags. In case there are any technical issues, the corporate BC offers troubleshooting support to the Bank Sakhis.Apart from micro ATMs, other handheld devices such as mobile phones or tablets can be used for service delivery. Both have different advantages and challenges in the form of battery life (low for tablet) and ease of enrolments (difficult on phone) and, hence, are not that commonly used.Both these front-end technology options have their own pros and cons. Table 4.1 compares the technologies from a front-end usage perspective.

Table 4.1: Comparison of technology options

Parameter Handheld device/micro ATM kiosk

ease of enrolment - Most micro ATMs/handheld devices have enrolment software

- It takes two to three days to generate an account number

- All kiosk-based devices have enrolment software- It takes two to three days to generate an account

number

ease of transaction - It takes 1 to 2 minutes to conduct a transaction- The receipt is generated from an inbuilt printer

- It takes 1 to 2 minutes to conduct a transaction- The receipt is generated from an external printer

Portability - It is easy to carry and doorstep service can be provided in the villages

- It has long battery back-up, thus making it possible to move around for long hours

- It is difficult to carry the whole setup (laptop, printer, webcam, biometric device, Internet dongle) to villages. In the case of desktop, it is not portable

- The battery life of the device is short; hence, it is not possible to move around for long

Cost of setup - only the cost of the machine in case it is not paid by the bank

- The average cost of device is rs 15,000 to rs 25,000

- Cost of setup includes the cost of physical space along with the hardware cost

- The average cost of setup is rs 30,000 to rs 40,000

Maintenance - The Bank Sakhis have to ensure maintenance of micro ATM and battery backup

- In the case of any technical issues, the corporate BC/TSP provides troubleshooting support

- The Bank Sakhi has to ensure maintenance of physical setup of kiosk and all equipment

- In case of any software issues (not hardware issues), the corporate BC/TSP provides troubleshooting support

Training needs - It requires training on usage of micro ATM in enrolment and transaction processes

- It requires basic computer literacy and ability to perform some more advanced processes which could be a hurdle since most SHG members lack computer experience

Other services - only banking services available on the software can be offered

- In addition to banking services, non-banking services such as CSC services (recharges, bill payments, etc.) and printing can also be offered for additional revenue

5 NABARD reimburses 80%-100% of the cost of micro ATMs under Financial Inclusion Technology Fund. Refer to NABARD circular (https://www.nabard.org/Circular/Hindifi.pdf )

experience from the pilot projectsThe Bank Sakhis in Uttar Pradesh and Madhya Pradesh are using both micro ATM (a handheld device) and kiosk-based model that has a laptop. The stakeholders jointly decided which technology to use.

RuRal Financial institutions PRogRamme 23

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Figure 5.1: Inception and execution phases

5 Setting up the bank Sakhi network

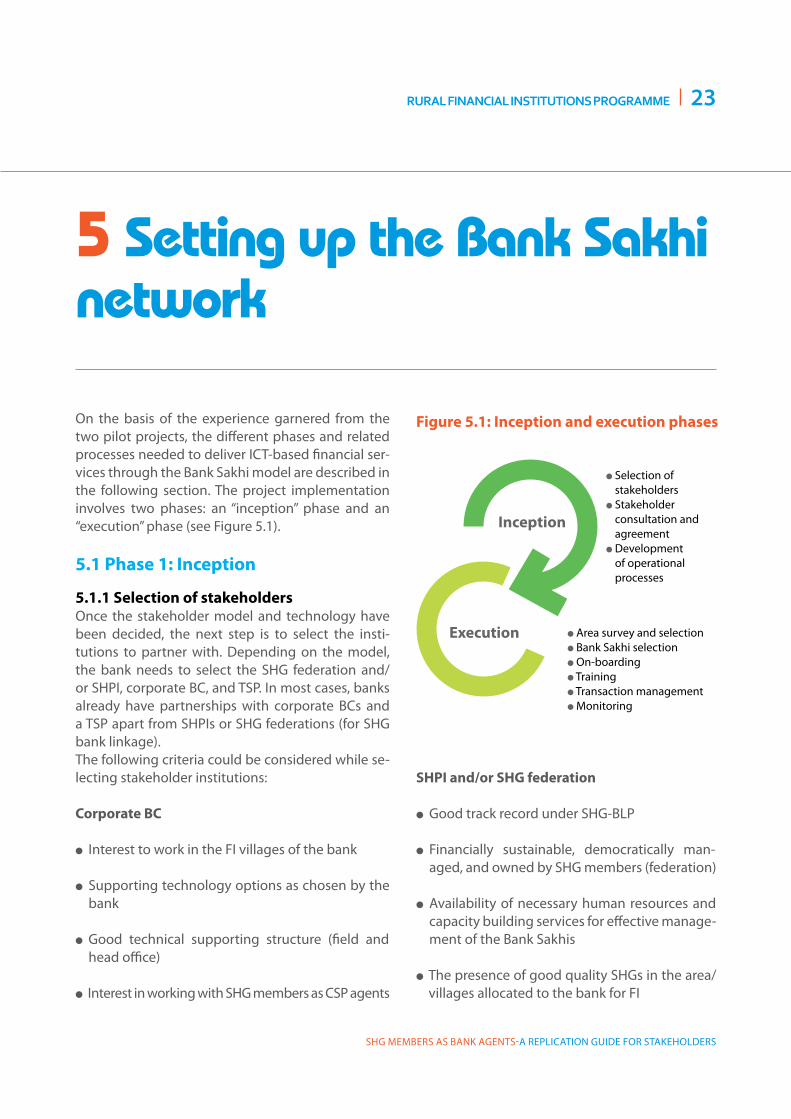

on the basis of the experience garnered from the two pilot projects, the different phases and related processes needed to deliver ICT-based financial ser-vices through the Bank Sakhi model are described in the following section. The project implementation involves two phases: an “inception” phase and an “execution” phase (see Figure 5.1).

5.1 Phase 1: Inception

5.1.1 Selection of stakeholdersonce the stakeholder model and technology have been decided, the next step is to select the insti-tutions to partner with. Depending on the model, the bank needs to select the SHG federation and/or SHPI, corporate BC, and TSP. In most cases, banks already have partnerships with corporate BCs and a TSP apart from SHPIs or SHG federations (for SHG bank linkage).The following criteria could be considered while se-lecting stakeholder institutions:

Corporate BC

l Interest to work in the FI villages of the bank

l Supporting technology options as chosen by the bank

l Good technical supporting structure (field and head office)

l Interest in working with SHG members as CSP agents

l Selection of stakeholders

l Stakeholder consultation and agreement

l Development of operational processes

Inception

execution l Area survey and selectionl Bank Sakhi selectionl on-boardingl Trainingl Transaction managementl Monitoring

SHPI and/or SHG federation

l Good track record under SHG-BLP

l Financially sustainable, democratically man-aged, and owned by SHG members (federation)

l Availability of necessary human resources and capacity building services for effective manage-ment of the Bank Sakhis

l The presence of good quality SHGs in the area/villages allocated to the bank for FI

24 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

5.1.2 Stakeholder consultation and agreementDuring the conceptualisation of the project, all stakeholders (bank, BC, sub-BC, TSP) are consult-ed about the rationale, objective, and proposed outcome under this approach. on finding synergy amongst the stakeholders, a formal joint meeting is held to decide upon the terms of agreement and roles and responsibilities.The following points need to be agreed upon with the partners:

l objectives, targets, and timelines for the project

l roles and responsibilities of each stakeholder

l Standard operating procedures

l Commercial aspects, i.e. revenue sharing be-tween the partners

l Taxes and duties to be paid as well as respective clauses for indemnity, audit, and jurisdiction for each stakeholder

In order to formally agree on all the points, a joint Memorandum of Understanding (MoU) should be signed by all the stakeholders. Depending on the stakeholder model used, banks usually have a bi-partite agreement with the corporate BC (or SHG federation), who might in turn sign bi-partite agreements with each Bank Sakhi covering the roles and responsibilities of both the parties. If a sub-BC is involved in the model, the BC and the sub-BC normally also sign a bi-partite agreement endorsed by the bank. All agreements clearly spell out the revenue sharing agreement and mecha-nism between the parties.

5.1.3 Development of operational processesStakeholders draw the project implementation plan with documentation of step-by-step pro-cess for the delivery and management (front-end and back-end) of Bank Sakhi-led financial services. This will be based on the roles and re-sponsibilities identified earlier. The following processes need to be documented at this stage:

l Area survey and selectionl Bank Sakhi selectionl on-boardingl Trainingl Enrolment and transactionsl Cash managementl Monitoring and reporting

once documented, this forms the basis for devel-oping training modules for capacity building of the Bank Sakhis.

5.2 Phase 2: execution

5.2.1 Area and village selectionThe first step in the second phase is to finalise the area and villages from which the Bank Sakhis need to be selected to deliver the financial services. The steps for this are as follows:

1. The bank makes suggestions about possibly un-banked/under-banked villages where good-qual-ity SHGs are present.

2. A baseline survey is conducted by the BC or sub-BC with the help of local field staff to assess the current socio-economic conditions, financial be-haviour of the village community, status of ac-cess to the banking services in the village, and telecom connectivity.

3. Profiles are prepared of the villages selected un-der the project. These include key data such as number of households, voter population (gender wise), number of banks and other financial in-stitutions present, socio-economic status of the population, key livelihood sources, public utili-ties, and government scheme beneficiaries.

The baseline survey and village profile help to meas-ure the outcome and impact of FI efforts over short-term and long-term periods6. It also helps to identify the interventions to ensure high uptake by assess-ing the need for financial awareness, which products need to be offered, potential customer segments, and so on.

6 The “SHG Members as Bank Agents Toolkit” developed by the RFIP includes sample formats used for baseline survey and village profiling.

RuRal Financial institutions PRogRamme 25

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

7 The “SHG Members as Bank Agents Toolkit” developed by the RFIP includes sample formats which can be adjusted and used.

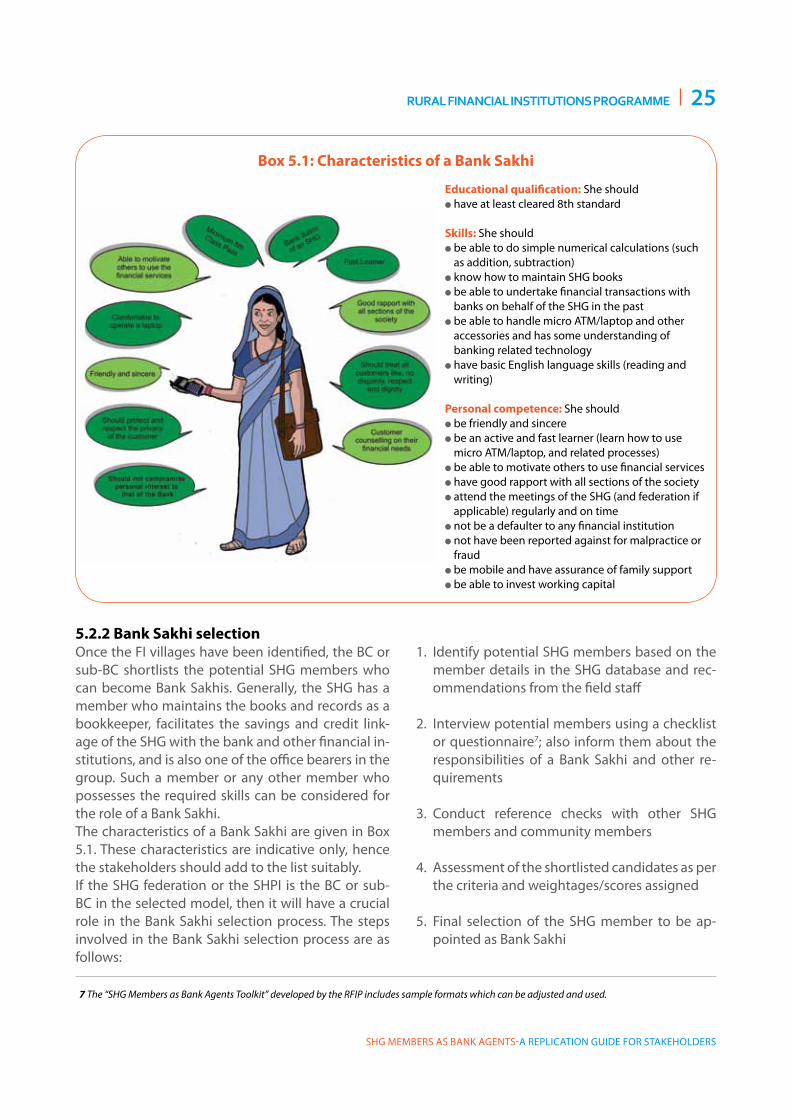

Box 5.1: Characteristics of a Bank Sakhi

educational qualification: She should l have at least cleared 8th standard

Skills: She should l be able to do simple numerical calculations (such

as addition, subtraction) l know how to maintain SHG booksl be able to undertake financial transactions with

banks on behalf of the SHG in the past l be able to handle micro ATM/laptop and other

accessories and has some understanding of banking related technology

l have basic English language skills (reading and writing)

Personal competence: She should l be friendly and sincere l be an active and fast learner (learn how to use

micro ATM/laptop, and related processes) l be able to motivate others to use financial services l have good rapport with all sections of the society l attend the meetings of the SHG (and federation if

applicable) regularly and on timel not be a defaulter to any financial institutionl not have been reported against for malpractice or

fraudl be mobile and have assurance of family support l be able to invest working capital

5.2.2 Bank Sakhi selectiononce the FI villages have been identified, the BC or sub-BC shortlists the potential SHG members who can become Bank Sakhis. Generally, the SHG has a member who maintains the books and records as a bookkeeper, facilitates the savings and credit link-age of the SHG with the bank and other financial in-stitutions, and is also one of the office bearers in the group. Such a member or any other member who possesses the required skills can be considered for the role of a Bank Sakhi. The characteristics of a Bank Sakhi are given in Box 5.1. These characteristics are indicative only, hence the stakeholders should add to the list suitably. If the SHG federation or the SHPI is the BC or sub-BC in the selected model, then it will have a crucial role in the Bank Sakhi selection process. The steps involved in the Bank Sakhi selection process are as follows:

1. Identify potential SHG members based on the member details in the SHG database and rec-ommendations from the field staff

2. Interview potential members using a checklist or questionnaire7; also inform them about the responsibilities of a Bank Sakhi and other re-quirements

3. Conduct reference checks with other SHG members and community members

4. Assessment of the shortlisted candidates as per the criteria and weightages/scores assigned

5. Final selection of the SHG member to be ap-pointed as Bank Sakhi

26 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

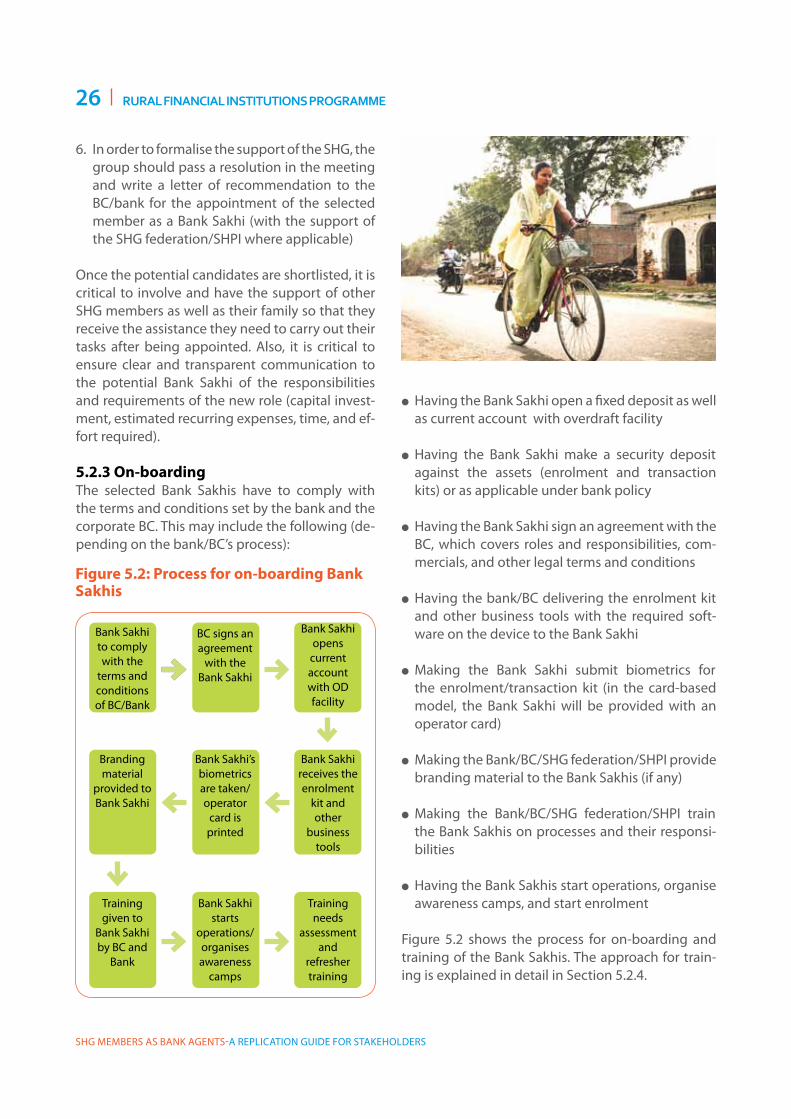

6. In order to formalise the support of the SHG, the group should pass a resolution in the meeting and write a letter of recommendation to the BC/bank for the appointment of the selected member as a Bank Sakhi (with the support of the SHG federation/SHPI where applicable)

once the potential candidates are shortlisted, it is critical to involve and have the support of other SHG members as well as their family so that they receive the assistance they need to carry out their tasks after being appointed. Also, it is critical to ensure clear and transparent communication to the potential Bank Sakhi of the responsibilities and requirements of the new role (capital invest-ment, estimated recurring expenses, time, and ef-fort required).

5.2.3 On-boardingThe selected Bank Sakhis have to comply with the terms and conditions set by the bank and the corporate BC. This may include the following (de-pending on the bank/BC’s process):

Figure 5.2: Process for on-boarding Bank Sakhis

Bank Sakhi to comply with the

terms and conditions of BC/Bank

Branding material

provided to Bank Sakhi

Training given to

Bank Sakhi by BC and

Bank

BC signs an agreement

with the Bank Sakhi

Bank Sakhi’s biometrics are taken/operator

card is printed

Bank Sakhi starts

operations/ organises awareness

camps

Bank Sakhi opens

current account with oD facility

Bank Sakhi receives the enrolment

kit and other

business tools

Training needs

assessment and

refresher training

l Having the Bank Sakhi open a fixed deposit as well as current account with overdraft facility

l Having the Bank Sakhi make a security deposit against the assets (enrolment and transaction kits) or as applicable under bank policy

l Having the Bank Sakhi sign an agreement with the BC, which covers roles and responsibilities, com-mercials, and other legal terms and conditions

l Having the bank/BC delivering the enrolment kit and other business tools with the required soft-ware on the device to the Bank Sakhi

l Making the Bank Sakhi submit biometrics for the enrolment/transaction kit (in the card-based model, the Bank Sakhi will be provided with an operator card)

l Making the Bank/BC/SHG federation/SHPI provide branding material to the Bank Sakhis (if any)

l Making the Bank/BC/SHG federation/SHPI train the Bank Sakhis on processes and their responsi-bilities

l Having the Bank Sakhis start operations, organise awareness camps, and start enrolment

Figure 5.2 shows the process for on-boarding and training of the Bank Sakhis. The approach for train-ing is explained in detail in Section 5.2.4.

RuRal Financial institutions PRogRamme 27

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

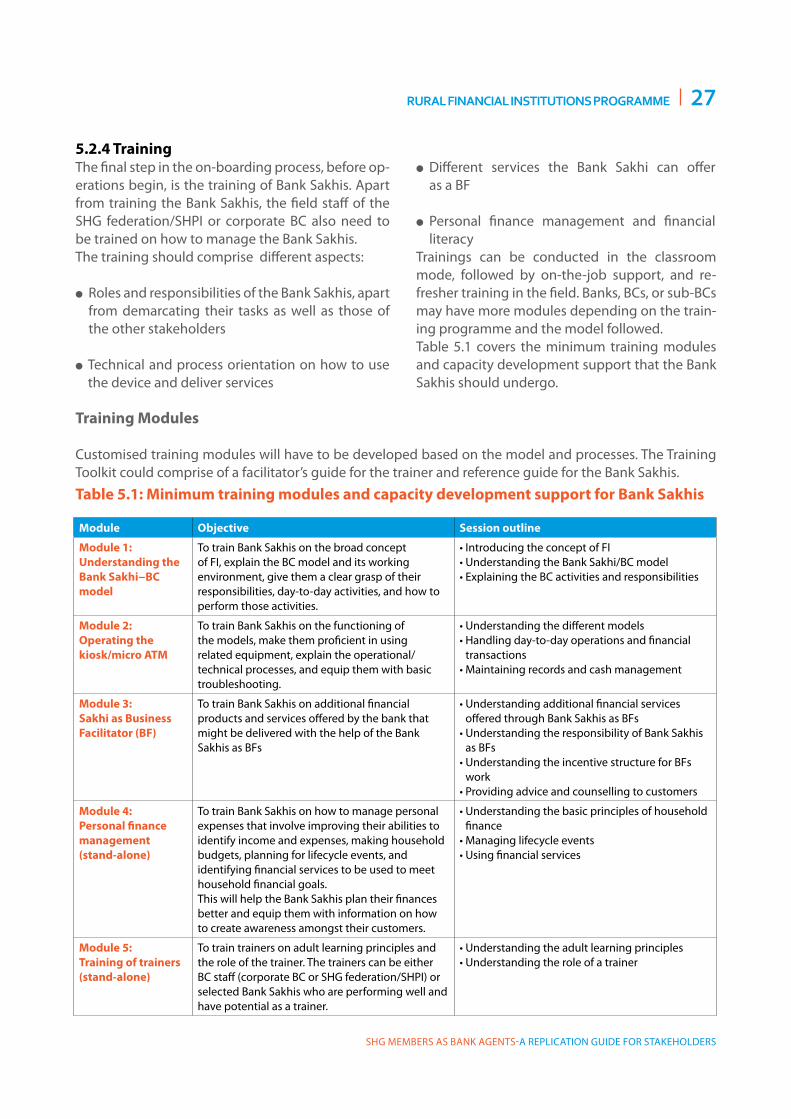

Table 5.1: Minimum training modules and capacity development support for Bank Sakhis

Training Modules

Customised training modules will have to be developed based on the model and processes. The Training Toolkit could comprise of a facilitator’s guide for the trainer and reference guide for the Bank Sakhis.

Module Objective Session outline

Module 1: Understanding the Bank Sakhi−BC model

To train Bank Sakhis on the broad concept of FI, explain the BC model and its working environment, give them a clear grasp of their responsibilities, day-to-day activities, and how to perform those activities.

• Introducing the concept of FI• Understanding the Bank Sakhi/BC model• Explaining the BC activities and responsibilities

Module 2: Operating the kiosk/micro ATM

To train Bank Sakhis on the functioning of the models, make them proficient in using related equipment, explain the operational/technical processes, and equip them with basic troubleshooting.

• Understanding the different models• Handling day-to-day operations and financial

transactions• Maintaining records and cash management

Module 3: Sakhi as Business Facilitator (BF)

To train Bank Sakhis on additional financial products and services offered by the bank that might be delivered with the help of the Bank Sakhis as BFs

• Understanding additional financial services offered through Bank Sakhis as BFs

• Understanding the responsibility of Bank Sakhis as BFs

• Understanding the incentive structure for BFs work

• Providing advice and counselling to customers

Module 4: Personal finance management (stand-alone)

To train Bank Sakhis on how to manage personal expenses that involve improving their abilities to identify income and expenses, making household budgets, planning for lifecycle events, and identifying financial services to be used to meet household financial goals. This will help the Bank Sakhis plan their finances better and equip them with information on how to create awareness amongst their customers.

• Understanding the basic principles of household finance

• Managing lifecycle events• Using financial services

Module 5: Training of trainers (stand-alone)

To train trainers on adult learning principles and the role of the trainer. The trainers can be either BC staff (corporate BC or SHG federation/SHPI) or selected Bank Sakhis who are performing well and have potential as a trainer.

• Understanding the adult learning principles• Understanding the role of a trainer

5.2.4 TrainingThe final step in the on-boarding process, before op-erations begin, is the training of Bank Sakhis. Apart from training the Bank Sakhis, the field staff of the SHG federation/SHPI or corporate BC also need to be trained on how to manage the Bank Sakhis. The training should comprise different aspects:

l roles and responsibilities of the Bank Sakhis, apart from demarcating their tasks as well as those of the other stakeholders

l Technical and process orientation on how to use the device and deliver services

l Different services the Bank Sakhi can offer as a BF

l Personal finance management and financial literacy

Trainings can be conducted in the classroom mode, followed by on-the-job support, and re-fresher training in the field. Banks, BCs, or sub-BCs may have more modules depending on the train-ing programme and the model followed. Table 5.1 covers the minimum training modules and capacity development support that the Bank Sakhis should undergo.

28 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

For more details refer to the SHG Members as Business Correspondent Training Module de-veloped by GIZ−NABArD rural Financial Institu-tions Programme.

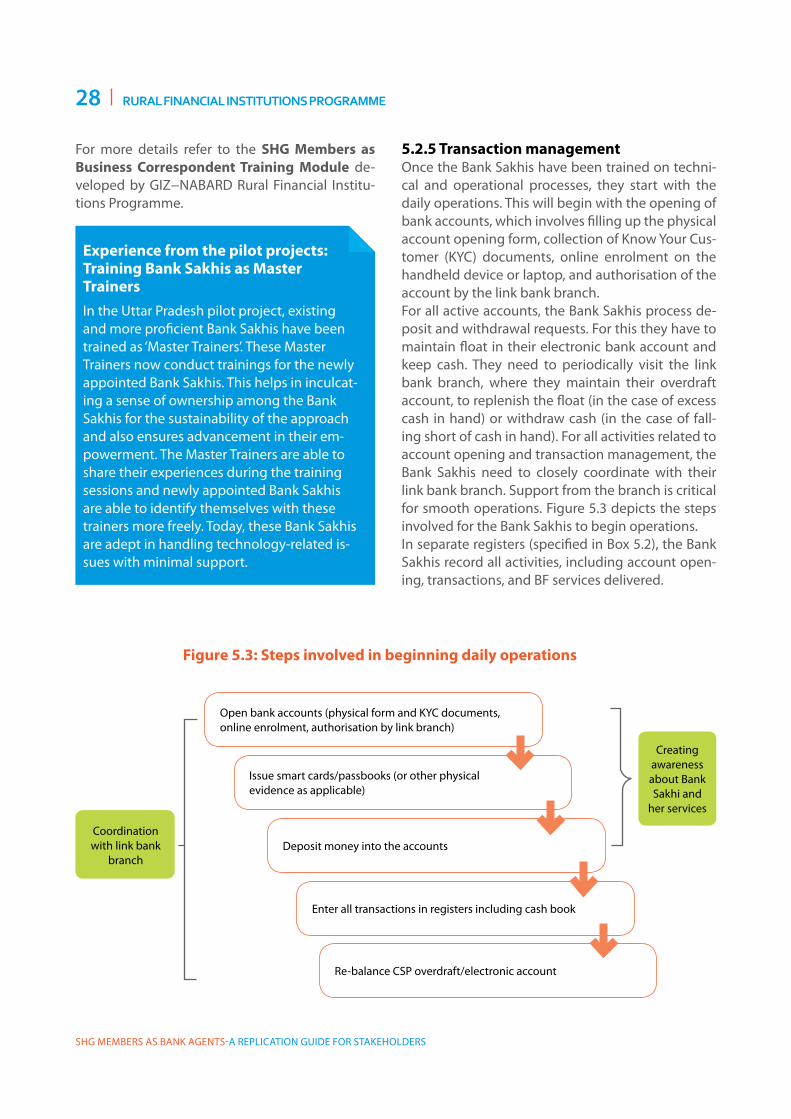

open bank accounts (physical form and kYC documents, online enrolment, authorisation by link branch)

Deposit money into the accounts

Issue smart cards/passbooks (or other physical evidence as applicable)

Enter all transactions in registers including cash book

Figure 5.3: Steps involved in beginning daily operations

Coordination with link bank

branch

Creating awareness about Bank Sakhi and

her services

re-balance CSP overdraft/electronic account

5.2.5 Transaction managementonce the Bank Sakhis have been trained on techni-cal and operational processes, they start with the daily operations. This will begin with the opening of bank accounts, which involves filling up the physical account opening form, collection of know Your Cus-tomer (kYC) documents, online enrolment on the handheld device or laptop, and authorisation of the account by the link bank branch. For all active accounts, the Bank Sakhis process de-posit and withdrawal requests. For this they have to maintain float in their electronic bank account and keep cash. They need to periodically visit the link bank branch, where they maintain their overdraft account, to replenish the float (in the case of excess cash in hand) or withdraw cash (in the case of fall-ing short of cash in hand). For all activities related to account opening and transaction management, the Bank Sakhis need to closely coordinate with their link bank branch. Support from the branch is critical for smooth operations. Figure 5.3 depicts the steps involved for the Bank Sakhis to begin operations.In separate registers (specified in Box 5.2), the Bank Sakhis record all activities, including account open-ing, transactions, and BF services delivered.

experience from the pilot projects: Training Bank Sakhis as Master TrainersIn the Uttar Pradesh pilot project, existing and more proficient Bank Sakhis have been trained as ‘Master Trainers’. These Master Trainers now conduct trainings for the newly appointed Bank Sakhis. This helps in inculcat-ing a sense of ownership among the Bank Sakhis for the sustainability of the approach and also ensures advancement in their em-powerment. The Master Trainers are able to share their experiences during the training sessions and newly appointed Bank Sakhis are able to identify themselves with these trainers more freely. Today, these Bank Sakhis are adept in handling technology-related is-sues with minimal support.

RuRal Financial institutions PRogRamme 29

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

5.2.6 MonitoringAs the Bank Sakhis serve the customers and handle cash on behalf of the bank and/or the corporate BC, it is very important that their transaction behaviour is monitored on a regular basis. Even though SHG members, being part of the local community, may be considered better in terms of integrity and con-duct with the customers, yet well-defined moni-toring indicators need to be established for better accountability, operational transparency, process compliance, and fraud prevention. Monitoring should also be used to observe the performance of the Bank Sakhis and identify interventions to strengthen their skills and competence. Monitoring can be an effective tool to gather feedback from the Bank Sakhis and customers, and can also help to im-prove processes and customer service.The following questions need to be answered while developing the monitoring processes and protocols:

l What to monitor? The decision on what to monitor will depend on the maturity of the implementation process. For instance, during the initial stages, the awareness building and enrolment activities need to be moni-

tored more frequently. As the Bank Sakhis start performing better, the focus will shift to liquid-ity management, transaction behaviour, and cus-tomer service. The list of monitoring areas can be as follows:

o Performance – Enrolment, transactions, other services

o Processes – Turn-around time for various pro-cesses, compliance to processes

o Customer service – Customer feedback and satisfaction, customer complaints

o Outreach – Coverage of the allocated villages, awareness building

o Record keeping – registers should be regularly updated, duly completed, and signed

o Branding – Banners, posters, certificate, etc. provided by the bank/corporate BC

o liquidity/cash management – Cash and over-draft balance (electronic balance) maintained

l Who will monitor? Stakeholders need to decide on the monitor-ing roles and responsibilities. each stakeholder needs to take up some responsibility for moni-

30 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

toring. It is generally recommended to task the stakeholder who is closest to the Bank Sakhis with the day-to-day monitoring. In case the SHG federa-tion or the SHPI is part of the model, they can moni-tor the functioning of the Bank Sakhis with the least incremental effort and cost since they already have field resources working with the Bank Sakhis and the SHGs.

l When to monitor and at what frequency?The frequency should be decided on the basis of the resources available and the geographical location (proximity and ease of travel) of the operations. Dur-ing the initial stages and during scale up, more fre-quent monitoring will be required (on a daily basis).

l How to monitor?The method of monitoring will depend on the moni-toring areas. Some of the key methods of monitor-ing are as follows:o Field visits – regular visits by the SHG federation/

SHPI, BC, and bank staff are required to monitor performance, maintenance of the record and cash management, and also gather feedback from the Bank Sakhis and customers.

o Management Information System – The MIS will provide the performance data as well as data on key indicators which need to be tracked to achieve

Registers to be maintained at the Bank Sakhi level:l Account opening and passbook/card distribution

with the date of enrolment, name, village, account number, passbook/card distributed with date, signatures, etc.

l Cash book, with cash-in-hand and account balance details

l Customer complaint register with customer complaints, action taken, and dates of resolution

l Visitor’s register with the name of the officer, date and purpose of visit, and observations

Registers to be maintained at the Federation/BC level:l FI activity register (with monthly summary of

all enrolment and transaction activities, camps conducted)

l Bank Sakhi complaint register (with Bank Sakhi complaints, action taken, and date of resolution)

l Monitoring register (with checklist of monitoring questions and observations on the same)

Box 5.2: Registers for monitoring activity at Bank Sakhi and Federation level 8

8 The “SHG Members as Bank Agents Toolkit” developed by the RFIP includes samples for Registers and Reporting Formats.

RuRal Financial institutions PRogRamme 31

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

experience from the pilot projects

Some of the key lessons learnt from the pilots projects with regard to implementation are as follows:

l Selection of stakeholderso The presence of pro-active, decisive, and robust

institutional stakeholders is of critical importance in the smooth launch and progress of the projects. It is important to select stakeholders who are financially sustainable and have the required human resources.

o regular and clear communication between all the stakeholders is critical to ensure that issues are identified and resolved in time. Monthly or quarterly meetings to review progress and proactively resolving the issues will ensure smooth implementation.

l Selection of Bank Sakhiso The SHG federation/SHPI is best placed to select the

Bank Sakhis since they know the SHG members, their savings/credit history, and personal background. The Bank Sakhis recommended by them are seen as reliable and trustworthy bank agents.

o once the potential Bank Sakhis have been shortlisted, it is very important to seek agreement with their family and their SHG so that they get support in their future endeavours.

l leveraging the SHG federation/SHPI staffo Since the SHG federation’s staff is already available in

the field, they are best placed to provide inexpensive operational support to the Bank Sakhis.

o It is important to understand the existing organogram of the SHG federation/SHPI (especially of the operational staff), and assign responsibilities accordingly.

o Since the SHG federation/SHPI staff is locally available, they could assist the Bank Sakhis in the case of any technical issues, and support them to conduct camps and so on.

l Training and capacity buildingo regular refresher trainings for the Bank Sakhis

are extremely important to ensure that they understand products and processes and are updated about any changes. Monthly meetings could be conducted wherein reviews of performance, planning for the month, and refresher trainings are done.

o The Bank Sakhis, after a few months experience, become adept in conducting training programmes for newly inducted Bank Sakhis. They can be groomed as master trainers for induction training or to conduct refresher trainings.

o In addition to Bank Sakhis, building the capacity of the SHG federation/SHPI staff is also critical. They need to be offered trainer skills so that they are able to conduct future trainings.

l Project monitoringo Monitoring should be conducted by all the

stakeholders. Monitoring by the link bank branch of the Bank Sakhis is very effective as this makes the branch accountable and helps in overall achievement of project goals.

o Maintaining and publishing a comprehensive MIS (preferably on a daily basis) is very important for monitoring and ensuring all stakeholders are updated.

project objectives (e.g. percentage of women cli-ents, average quarterly balance in the accounts). The reconciliation should be made at regular in-tervals between data generated by the MIS and data updated in the registers maintained by the Bank Sakhis.

o Call centre – In case the bank and/or corporate BC

has a call centre, then the same can be used to monitor complaints received, time taken to re-solve the issues, and customers as well as Bank Sakhi feedback.

o Internal audit – The bank and corporate BC must conduct regular internal audits based on a pre-decided checklist.

32 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

To achieve the objective of ensuring greater FI out-reach of the banking sector, the BC model is being promoted by the government and the regulator. In order to make this model viable in the long run, it is very important that the model is financially sustainable. To achieve this, it is crucial to ensure that all the stakeholders in the ecosystem make enough money to sustain their operations.The following sections (and Figure 6.1) discuss two critical aspects of the business case for stake-holders, especially the Bank Sakhis and the feder-ation: (i) commission structures and (ii) products and services offered.

6.1 Commission structures

As per a CGAP study9, only about 48% CSPs (Cus-tomer Service Points of Banks/corporate BCs) are paid their commission on time. Also, the an-

6 ensuring that there is a business case

Figure 6.1: Two critical aspects of the business case for stakeholders

nual high attrition rate of 25%−34% is expected to increase if the income expectations are not met. In order to keep the CSPs interested in the model, it is necessary that they are paid an adequate and timely commission. The same applies in the case of the Bank Sakhis too. To maintain transparency and trust, the commission structure should be fixed and shared with them. Depending on the partners involved in the imple-mentation (e.g. the corporate BC, sub-BC/SHG fed-eration/SHPI), the commission will be shared as per their roles and responsibilities. To avoid any future conflict, the same should also be mentioned in the MoUs between the bank and Bank Sakhi/SHPI/SHG federation. The following key questions need to be answered when deciding on the commission structures:

• For which activities will the commission be paid (see Table 6.1)?o Account opening: Commission is paid only once

account has been activated. Some banks also di-vide the commission and pay a part of it once a transfer has been made into the account.

o Transactions: Commission is paid on deposits, withdrawals, and fund transfers.

o Account balance: Commission can be paid on the basis of the balance maintained in the ac-counts opened by the Bank Sakhis.

o BF activities: Commission is paid on all services delivered by the Bank Sakhis as BFs including term deposits, loan applications, Non-Perform-ing Assets (NPA) recoveries, etc.

9 http://www.slideshare.net/CGAP/2013-india-national-survey-of-banking-agents

2. Products

and services offered

1. Commission

structures

RuRal Financial institutions PRogRamme 33

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Table 6.1: Ongoing practices for commission calculation basis

• How much to pay and on what basis?The bank can pay either fixed monthly commissions or variable commissions based on the business gen-erated by the Bank Sakhis. Normally, a fixed monthly commission is provided in the initial phase and then a variable commission is applied. The calculation of commission can also differ based on the activity and stage of the operations. For instance, initially the compensation for account opening could be higher, and once the Bank Sakhis start performing better, the commissions for transactions can be increased.In the long run, it is suggested that transactions should be the major revenue driver and need to be compensated adequately. Servicing transactions also has costs associated with it in terms of cost of maintaining float as for working capital needs, and the cost of re-balancing (visiting bank to balance cash in hand and overdraft account). Hence, the commission paid on transactions needs to be ad-equate to cover these costs.

the CsP is the last mile delivery stakeholder in the model and

ensuring adequate financial rewards to it is critical.

Activity Basis

Account opening • Flat amount per account opened

Transactions • Flat percentage of the value of transaction• Flat percentage of the value of transaction with minimum and maximum

commission caps• Flat commission per transaction• Staged commission structure with different rates for different slabs of amount

Account balance • Flat percentage of the average account balance

BF services • Flat commission on term deposits opened• Flat percentage on value of term deposits opened• Flat percentage on the amount of NPA recovered• Flat percentage on the amount of loan sourced

• How to decide on the commission share for the sub-BC (SHG federation/SHPI)?

In the cases where a sub-BC (SHG federation/SHPI) is assigned to the model, a cost-benefit analysis needs to be done in order to ensure that the mod-el is financially viable for them. In the cases where the sub-BC will receive a commission share from the Bank Sakhis, the mechanism for payment of the commissions to the sub-BC needs to be de-cided from the beginning. The payment can be made either by the Bank Sakhis as fixed percent-age of the commissions earned by them, or the bank/corporate BC can pay directly a pre-decided percentage.

• When to pay?Most banks pay the commission on a monthly basis. However, some service providers/BCs pay transaction commissions on real-time basis and account opening commissions on a monthly ba-sis. Irrespective of the frequency, it is important to avoid any delay in payment, as it will result in in-ordinate delays which should be avoided as they may de-motivate the agents.

• How to pay?In order to ensure transparency and efficiency of the payout, the Bank Sakhis and SHG federation/SHPI (if present) should be paid electronically by the bank. Delays might take place if commissions are first paid by the bank to the corporate BC and

34 RuRal Financial institutions PRogRamme

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

then the corporate BC pays the other stakehold-ers. In such cases, the bank could take a debit authority from the corporate BC to debit their account and credit the Bank Sakhis’ accounts for commissions. This way the commission payment could be done on the same day.

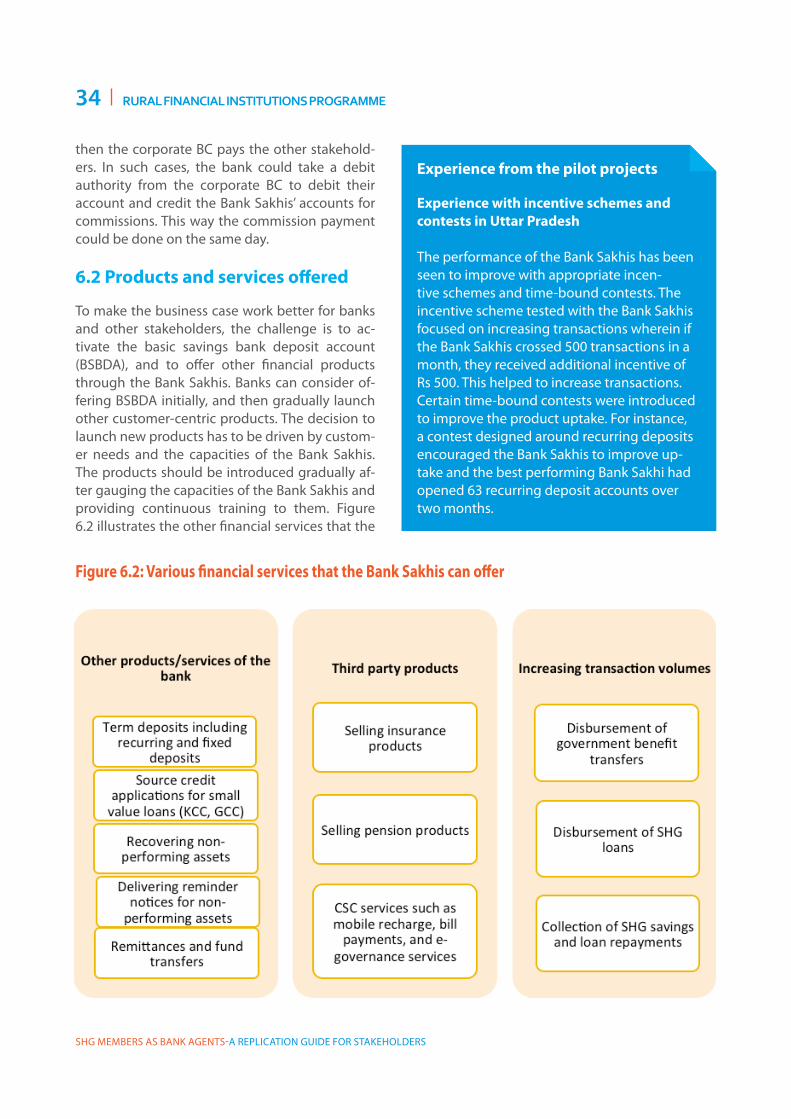

6.2 Products and services offered

To make the business case work better for banks and other stakeholders, the challenge is to ac-tivate the basic savings bank deposit account (BSBDA), and to offer other financial products through the Bank Sakhis. Banks can consider of-fering BSBDA initially, and then gradually launch other customer-centric products. The decision to launch new products has to be driven by custom-er needs and the capacities of the Bank Sakhis. The products should be introduced gradually af-ter gauging the capacities of the Bank Sakhis and providing continuous training to them. Figure 6.2 illustrates the other financial services that the

Figure 6.2: Various financial services that the Bank Sakhis can offer

experience from the pilot projects

experience with incentive schemes and contests in Uttar Pradesh

The performance of the Bank Sakhis has been seen to improve with appropriate incen-tive schemes and time-bound contests. The incentive scheme tested with the Bank Sakhis focused on increasing transactions wherein if the Bank Sakhis crossed 500 transactions in a month, they received additional incentive of rs 500. This helped to increase transactions. Certain time-bound contests were introduced to improve the product uptake. For instance, a contest designed around recurring deposits encouraged the Bank Sakhis to improve up-take and the best performing Bank Sakhi had opened 63 recurring deposit accounts over two months.

RuRal Financial institutions PRogRamme 35

SHG MEMBErS AS BANk AGENTS-A rEPLICATIoN GUIDE For STAkEHoLDErS

Bank Sakhis can offer in addition to BSBDA.The Bank Sakhis’ integration into and trust by the community provides them with advantages in pro-viding all these services to the customers. Further-more, it is important to ensure a diverse product suite in order to ensure enough volume of transac-tions and a business case for the introduction of the Bank Sakhis. A diverse product suite will also result in higher satisfaction for customers who can use the Bank Sakhis as “one-stop-shop”.Banks can further leverage the Government to Per-son (G2P) payment schemes and SHG transactions by routing them through the Bank Sakhis. This will bring all these transactions into the formal payment system and, thereby, increase transparency and sav-ings float for the banks.

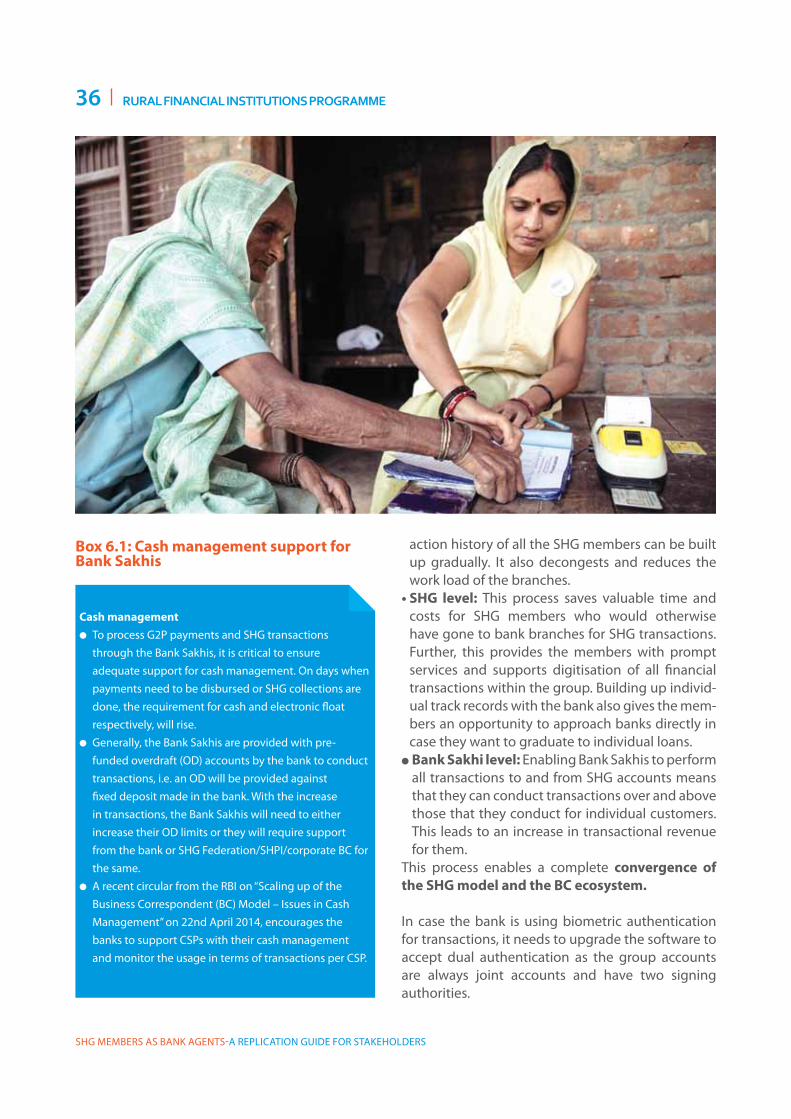

6.3 Including SHG transactions into the BC Channel

one gap in the BC model has been that only individ-ual accounts could be served at the agent (CSP) lev-el. Group accounts still needed to be served at the branch level, where multiple office bearers (at least two in the case of SHGs) are needed to authenticate themselves through signatures. only then money from a group account (Savings Bank Account/Cash Credit Limit) could be withdrawn and distributed among the individual SHG members. This required the signatories of the group to visit the branches, spending a lot of time and money, and causing in-convenience to the members and leaders of the group.A majority of the customers of the Bank Sakhis are SHG members, who use their individual accounts for individual financial services but also transact within the group, to and from the group account. With the current applications and software, the Bank Sakhis can then perform the following transactions for the SHG (given that all the members have indi-vidual accounts serviced by the Bank Sakhis):