Embed Size (px)

Citation preview

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 1/8

Results Conference Call – 1Q11

May 2, 2011

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 2/8

The information contained in this presentation may include statements which constitute

forward-looking statements, as defined by Section 27A of the U.S. Securities

Act of 1933, as amended, and Section 21E of the U.S. Securities Exchange Act of

1934, as amended. Such forward-looking statements involve a certain degree of risk

and uncertainty with respect to business, financial, trend, strategy and other forecasts,

and are based on assumptions, data or methods that, although considered reasonable

by the company at the time, may be incorrect or imprecise, or may not be

possible to realize. The company gives no assurance that expectations disclosed in

this presentation will be confirmed. Prospective investors are cautioned that any suchforward-looking statements are not guarantees of future performance and involve risks

and uncertainties, and that actual results may differ materially from those in the

forward-looking statements, due to a variety of factors, including, but not limited to, the

risks of international business and other risks referred to in the company’s filings with

the CVM and SEC. The company does not undertake, and specifically disclaims any

obligation to update any forward-looking statements, which are valid only for the date on

which they are made.

Legal Notice

2

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 3/8

Agenda

1Q11 Performance

Debt

Liability Management

Growth

4

5

6

7

3

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 4/8

1Q11 Performance

Key Indicators Pulp Sales Mix (%)

Cash Cost (R$/t) Pro Forma EBITDA (R$ million) and EBITDA Margin (%)

1Q11 4TQ0 1Q10 1Q11 vs4Q10

1Q11 vs1Q10

Pulp Production (‘000 t) 1,319 1,330 1,267 -1% 4%

Pulp Sales (‘000 t) 1,259 1,254 1,281 0% -2%

Paper Production (‘000 t) 29 26 29 9% -1%

Paper Sales (‘000 t) 36 30 28 19% 30%

Net Revenue (R$ million) 1,548 1,563 1,511 -1% 2%

Pro Forma EBITDA (R$ million) 607 606 597 0% 2%

EBITDA Margin (%) 39% 39% 39% 0 p.p. 0 p.p.

Financial Income (R$ million) 11 35 (337) -67% -

Net Income (R$ million) 389 162 9 140% -

46%

20%

25%

9%

1Q11

413425

446

1Q10 4Q10 1Q11

Cash Cost

597 606 607

1Q10 4Q10 1Q11

39% 39% 39%

4

38%

30%

23%

9%

4Q10

Europe North America Asia Brazil/Others

40%

28%

24%

8%

1Q10

Cash Cost 2010

R$452/t

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 5/8

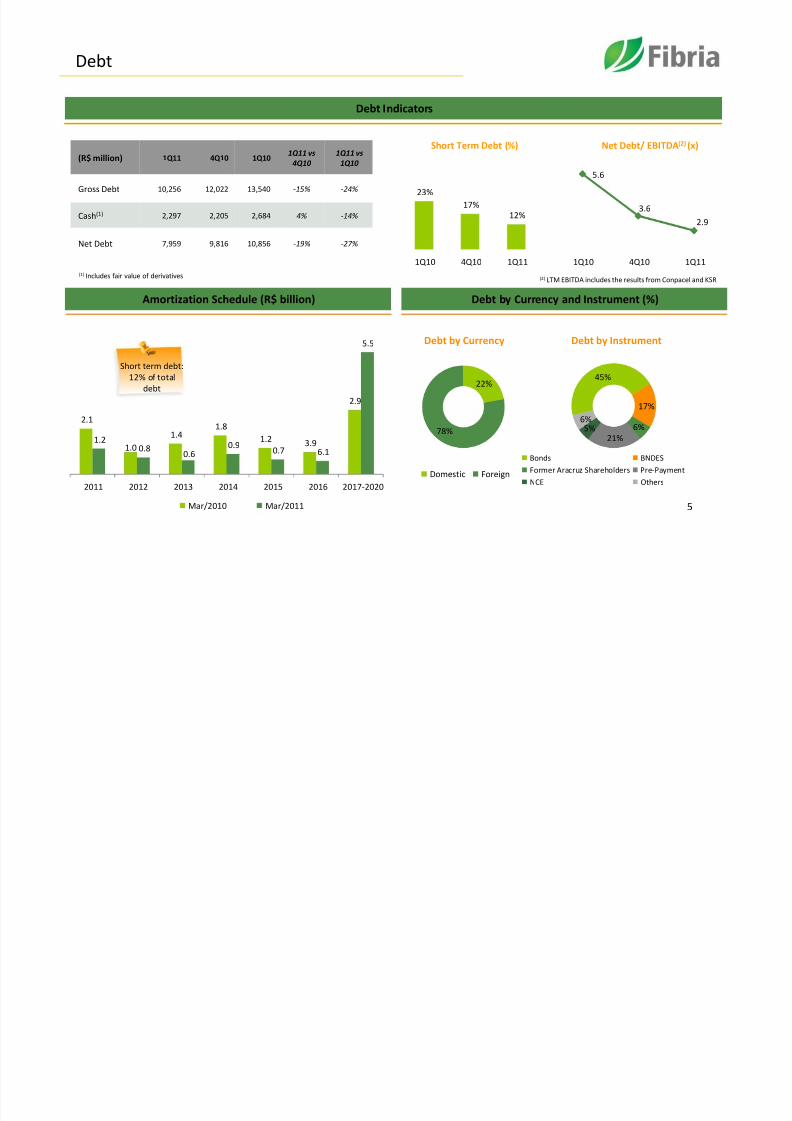

Debt

Amortization Schedule (R$ billion)

Debt Indicators

Debt by Currency and Instrument (%)

(R$ million) 1Q11 4Q10 1Q101Q11 vs

4Q10

1Q11 vs

1Q10

Gross Debt 10,256 12,022 13,540 -15% -24%

Cash(1) 2,297 2,205 2,684 4% -14%

Net Debt 7,959 9,816 10,856 -19% -27%

23%17%

12%

1Q10 4Q10 1Q11

Short Term Debt (%) Net Debt/ EBITDA(2) (x)

5.6

3.6

2.9

1Q10 4Q10 1Q11

(2) LTM EBITDA includes the results from Conpacel and KSR

2.1

1.0

1.41.8

1.2 3.9

2.9

1.20.8

0.60.9

0.7 6.1

5.5

2011 2012 2013 2014 2015 2016 2017-2020

Mar/2010 Mar/2011

22%

78%

Debt by Currency

Domestic Foreign

45%

17%

6%

21%5%

6%

Debt by Instrument

Bonds BNDES

Former Aracruz Shareholders Pre-Payment

NCE Others

5

(1) Includes fair value of derivatives

Short term debt:

12% of total

debt

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 6/8

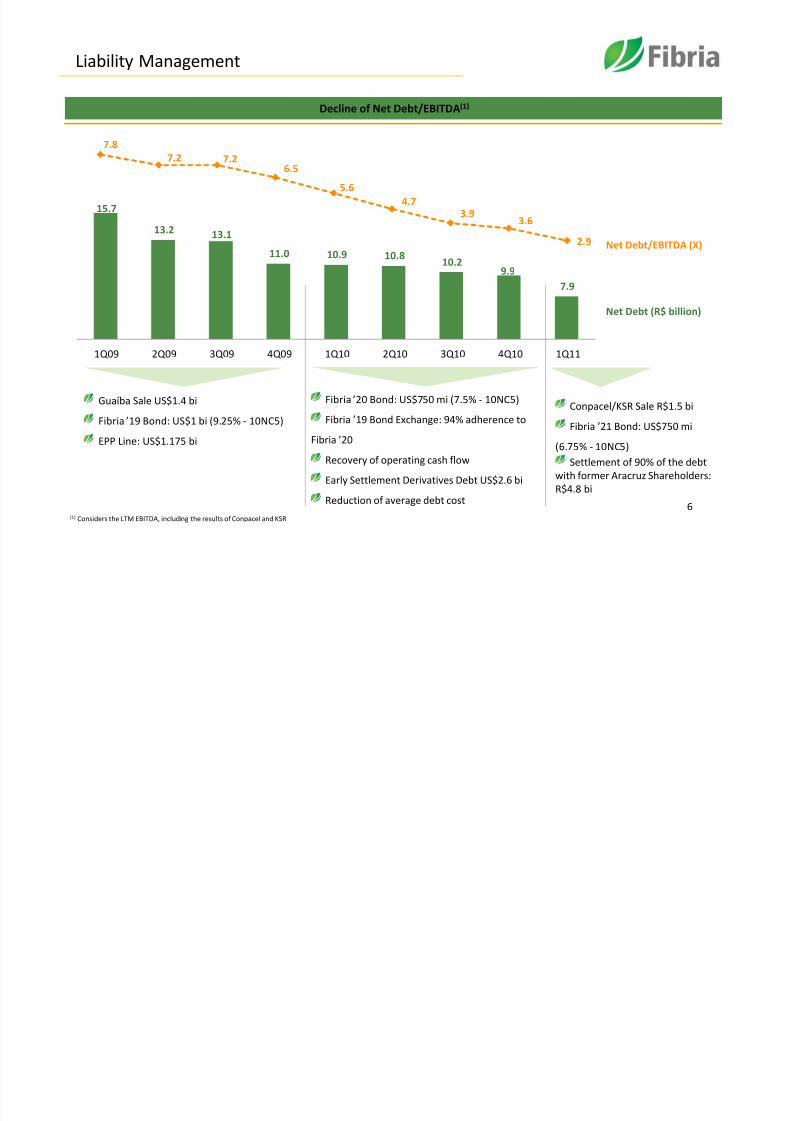

7.8

7.2 7.26.5

5.6

4.73.9

3.6

2.9

Liability Management

6

15.7

13.2 13.1

11.0 10.9 10.810.2

9.9

7.9

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11

Net Debt/EBITDA (X)

Fibria ’20 Bond: US$750 mi (7.5% - 10NC5)

Fibria ’19 Bond Exchange: 94% adherence to

Fibria ’20

Recovery of operating cash flow

Early Settlement Derivatives Debt US$2.6 bi

Reduction of average debt cost

Net Debt (R$ billion)

Conpacel/KSR Sale R$1.5 bi

Fibria ’21 Bond: US$750 mi

(6.75% - 10NC5)

Settlement of 90% of the debt

with former Aracruz Shareholders:

R$4.8 bi

Guaíba Sale US$1.4 bi

Fibria ’19 Bond: US$1 bi (9.25% - 10NC5)

EPP Line: US$1.175 bi

Decline of Net Debt/EBITDA(1)

(1) Considers the LTM EBITDA, including the results of Conpacel and KSR

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 7/8

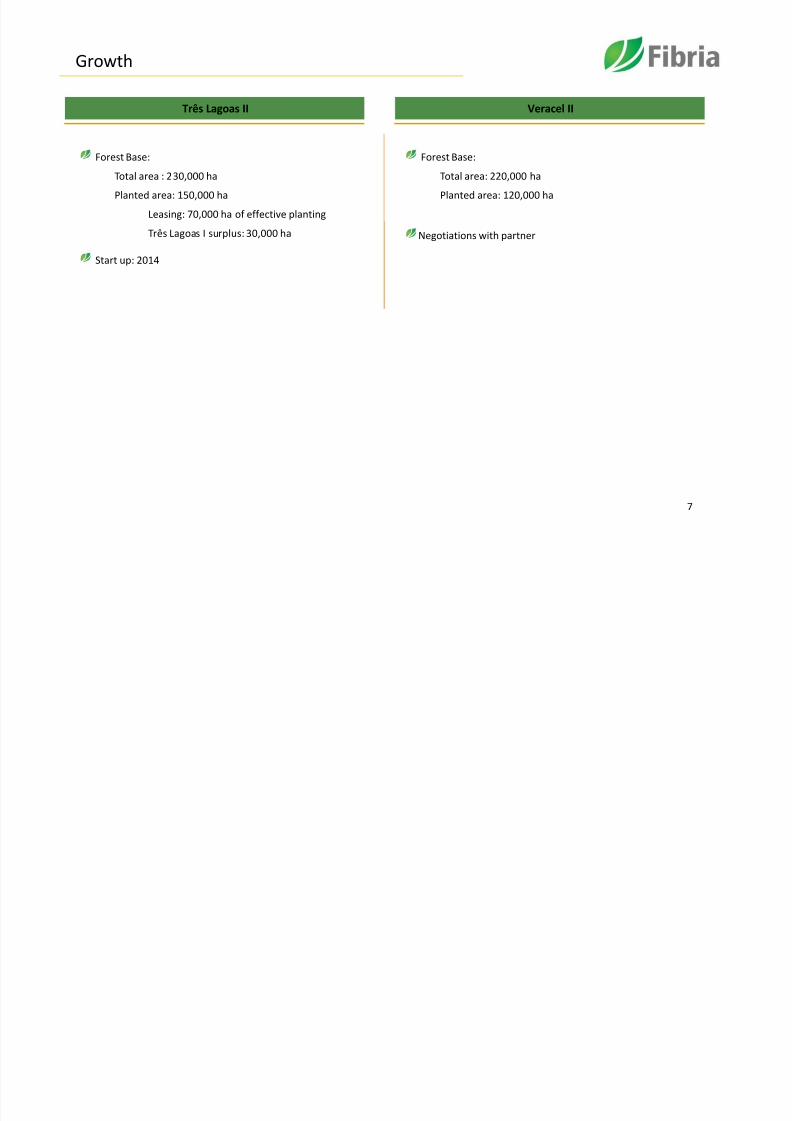

Growth

Três Lagoas II

7

Veracel II

Forest Base:

Total area : 230,000 ha

Planted area: 150,000 ha

Leasing: 70,000 ha of effective planting

Três Lagoas I surplus: 30,000 ha

Start up: 2014

Forest Base:

Total area: 220,000 ha

Planted area: 120,000 ha

Negotiations with partner

8/3/2019 call 1T11 ENG FINAL

http://slidepdf.com/reader/full/call-1t11-eng-final 8/8

Investor Relations Team:

Website: www.fibria.com.br/ri

E-mail: [email protected]

Tel.: +55 (11) 2138-4565

8

![nagano-traveler-call-leaflet · 2017. 7. 19. · Call Center for Traveler Support Multilingual NAGANO Azusa River, Kamikouchi NAGANO PEOPLE CALL CENTER YOU [TRAVELER] CALL CALL 3-way](https://img.pdfslide.org/doc/110x75/5ff778a5bf22974fca7e22d1/nagano-traveler-call-leaflet-2017-7-19-call-center-for-traveler-support-multilingual.jpg)

![Call Center[1]](https://img.pdfslide.org/doc/110x75/577c7c1b1a28abe054994e3b/call-center1.jpg)

![Programme [eng]](https://img.pdfslide.org/doc/110x75/568c52e41a28ab4916b88c02/programme-eng-56fc6d05dac74.jpg)