Embed Size (px)

Citation preview

9. NOVEMBER 2015

WACHSTUMSMARKT APOTHEKENVERSANDHANDEL

– Eine europäische Perspektive –

AGENDA

• EINFLUSSGRÖSSEN & SCOPE

• MARKTENTWICKLUNG BIS 2018

• EINORDNUNG DER EUROPÄISCHEN MÄRKTE

- Beispiel Deutschland

- Beispiel Österreich

- Beispiel Frankreich

• FAZIT

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

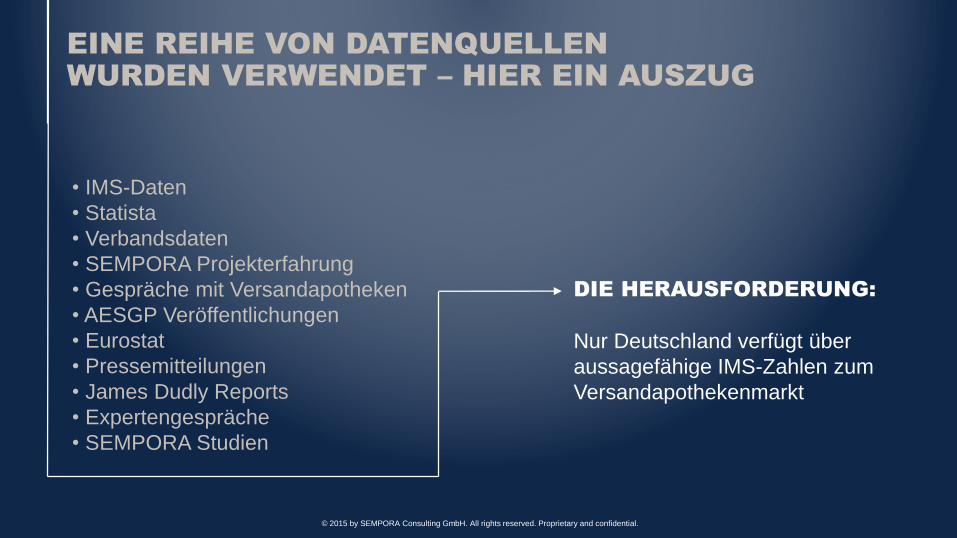

EINE REIHE VON DATENQUELLEN

WURDEN VERWENDET – HIER EIN AUSZUG

• IMS-Daten• Statista• Verbandsdaten• SEMPORA Projekterfahrung• Gespräche mit Versandapotheken• AESGP Veröffentlichungen• Eurostat• Pressemitteilungen• James Dudly Reports• Expertengespräche• SEMPORA Studien

DIE HERAUSFORDERUNG:

Nur Deutschland verfügt über aussagefähige IMS-Zahlen zum Versandapothekenmarkt

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

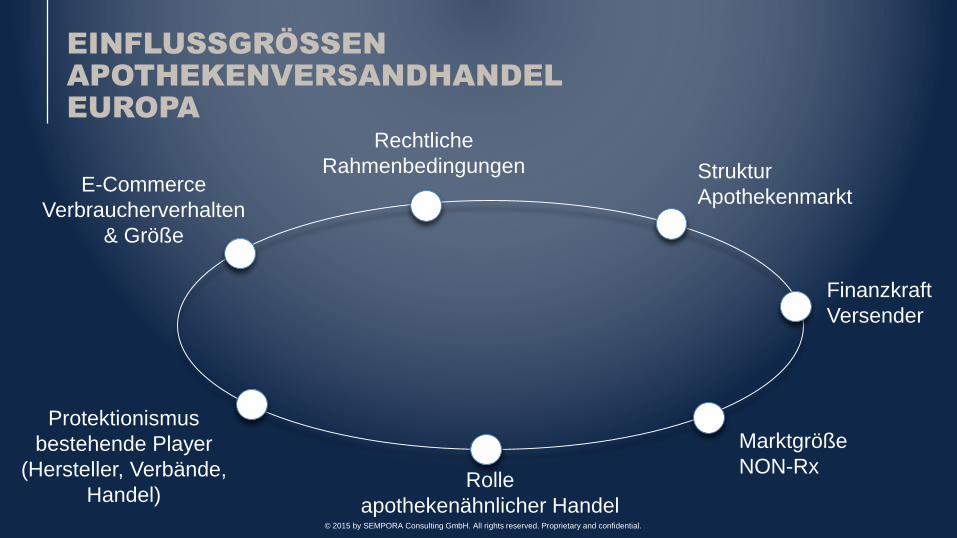

EINFLUSSGRÖSSEN

APOTHEKENVERSANDHANDEL

EUROPA

Rechtliche Rahmenbedingungen Struktur

Apothekenmarkt

Finanzkraft Versender

Marktgröße NON-Rx

Rolle apothekenähnlicher Handel

Protektionismusbestehende Player

(Hersteller, Verbände, Handel)

E-Commerce Verbraucherverhalten

& Größe

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

107 MRD €

Pro Kopf 1671 €

STATUS E-COMMERCE: ITALIEN WENIGER LUKRATIV

63,4 MRD €

Pro Kopf 786 €

51,1 MRD €

Pro Kopf 775 €

7,6 MRD €

Pro Kopf 1.490 €

11 MRD €

Pro Kopf 1.258 €

11,2 MRD €

Pro Kopf 186 €

Quelle: ecommerce-europe.eu

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

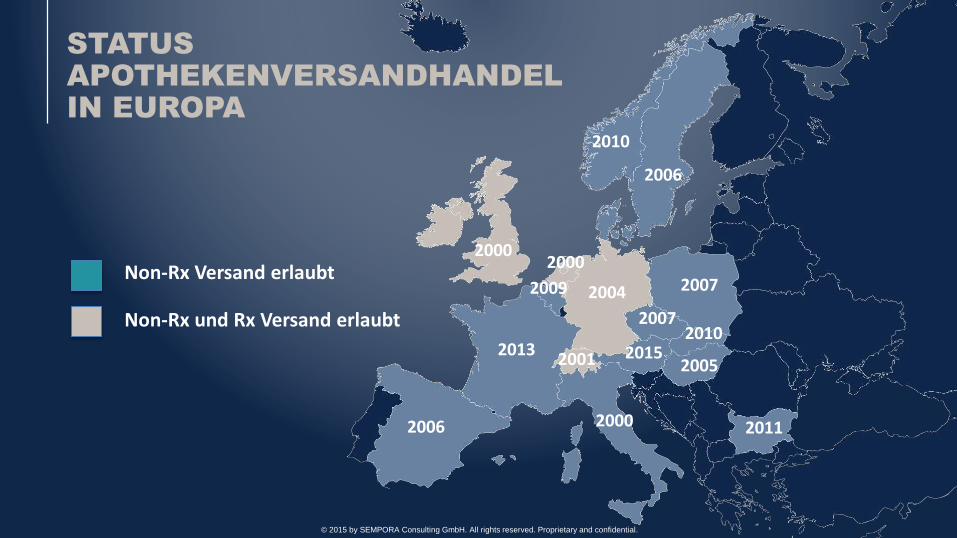

NON-RX

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

Non-Rx Versand erlaubt

Non-Rx und Rx Versand erlaubt

2010

2006

20002000

20042009

2013

2006 2000

2001 2015

2007

2007

2005

2011

2010

STATUS

APOTHEKENVERSANDHANDEL

IN EUROPA

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

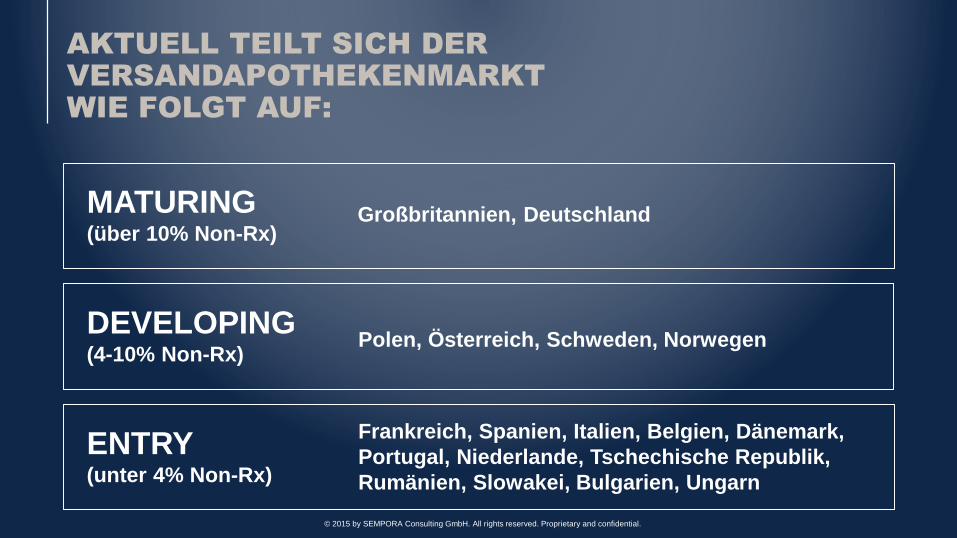

AKTUELL TEILT SICH DER

VERSANDAPOTHEKENMARKT

WIE FOLGT AUF:

Frankreich, Spanien, Italien, Belgien, Dänemark, Portugal, Niederlande, Tschechische Republik, Rumänien, Slowakei, Bulgarien, Ungarn

ENTRY(unter 4% Non-Rx)

Polen, Österreich, Schweden, NorwegenDEVELOPING(4-10% Non-Rx)

Großbritannien, DeutschlandMATURING(über 10% Non-Rx)

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

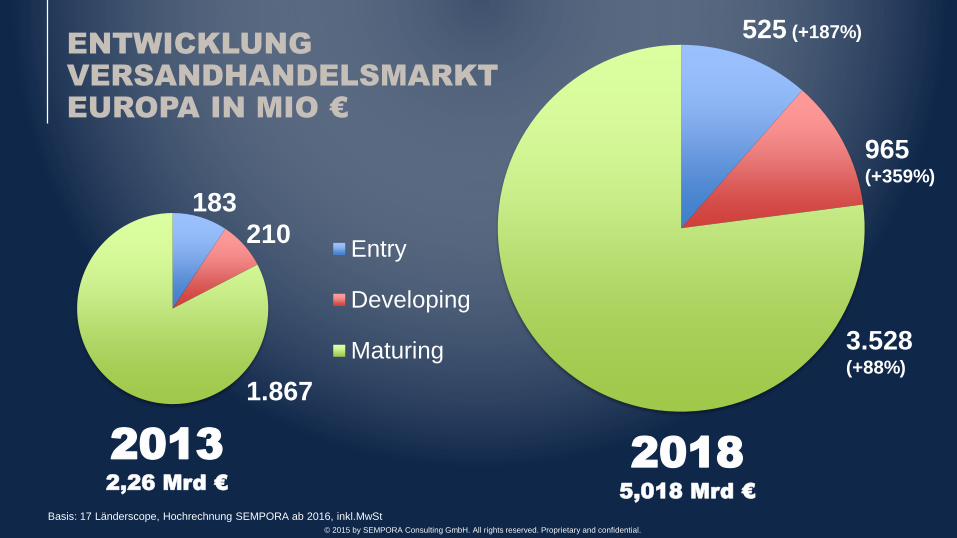

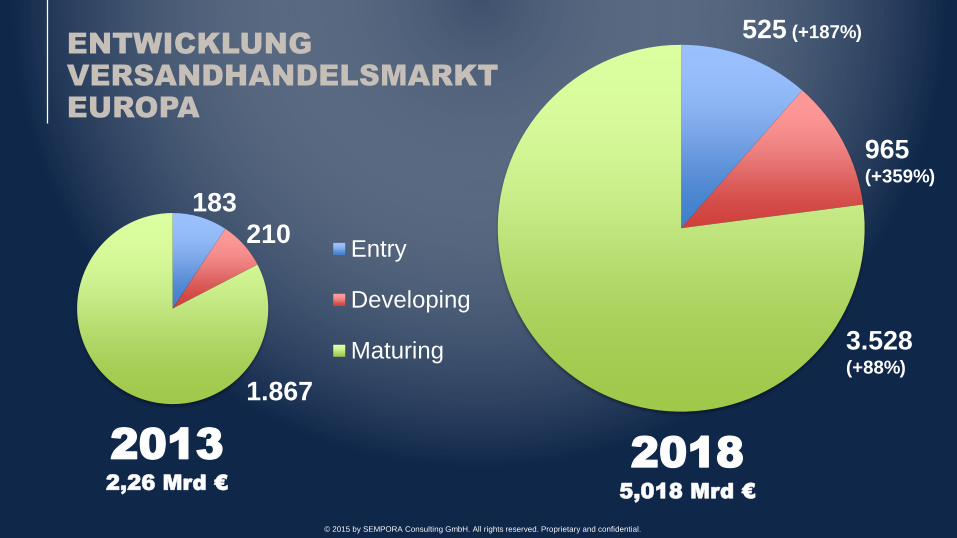

ENTWICKLUNG

VERSANDHANDELSMARKT

EUROPA IN MIO €

2013

2,26 Mrd €

2018

5,018 Mrd €

Entry

Developing

Maturing

183210

1.867

525 (+187%)

965(+359%)

3.528(+88%)

Basis: 17 Länderscope, Hochrechnung SEMPORA ab 2016, inkl.MwSt© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

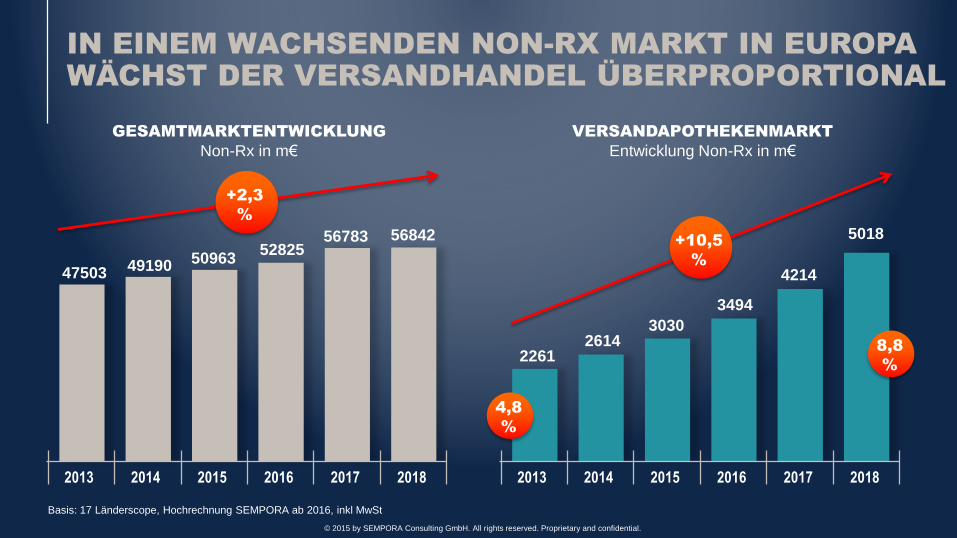

IN EINEM WACHSENDEN NON-RX MARKT IN EUROPA

WÄCHST DER VERSANDHANDEL ÜBERPROPORTIONAL

2013 2014 2015 2016 2017 2018

Basis: 17 Länderscope, Hochrechnung SEMPORA ab 2016, inkl MwSt

56842

VERSANDAPOTHEKENMARKT

Entwicklung Non-Rx in m€

GESAMTMARKTENTWICKLUNG

Non-Rx in m€

5678352825509634919047503

2013 2014 2015 2016 2017 2018

5018

4214

34943030

26142261

+2,3

%

+10,5

%

4,8

%

8,8

%

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

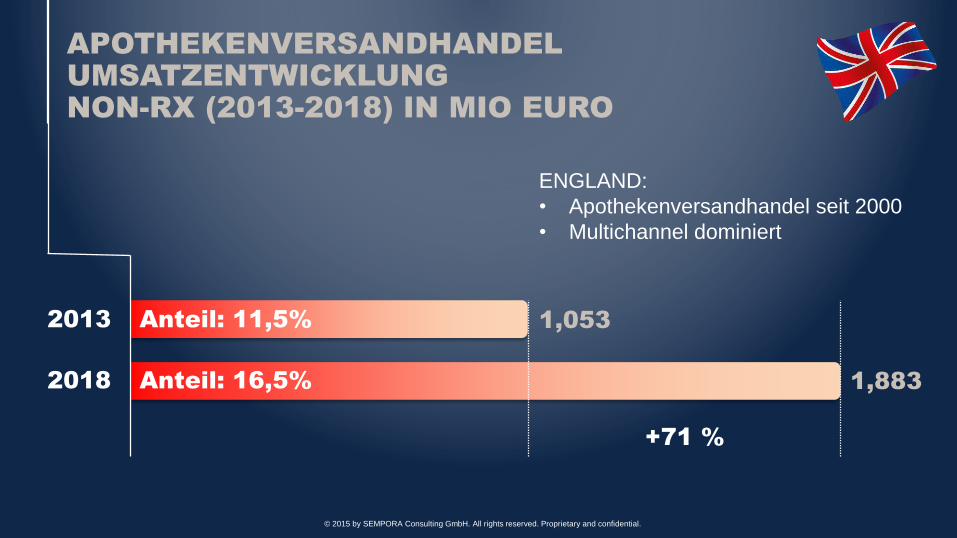

APOTHEKENVERSANDHANDEL

UMSATZENTWICKLUNG

NON-RX (2013-2018) IN MIO EURO

2018

Anteil: 11,5%

+71 %

Anteil: 16,5%

2013 1,053

1,883

ENGLAND:• Apothekenversandhandel seit 2000• Multichannel dominiert

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

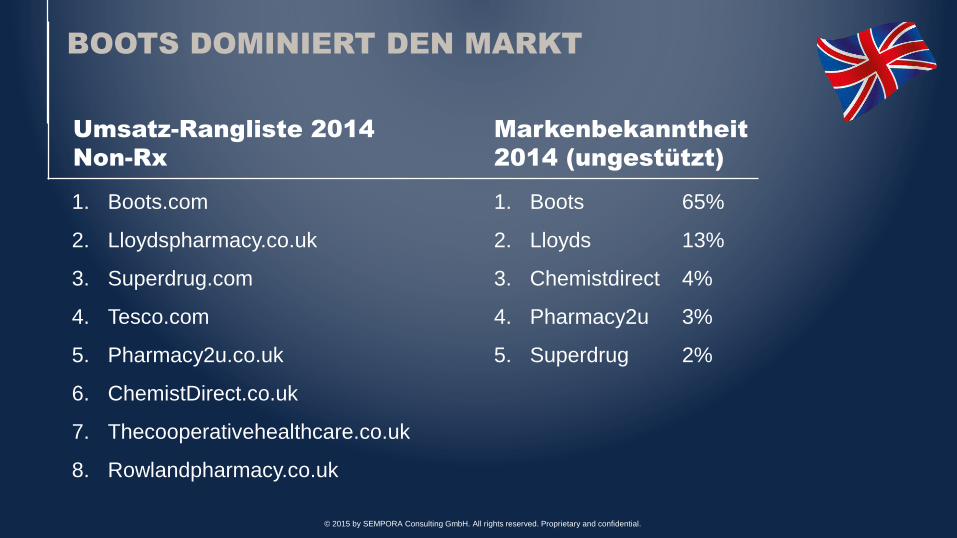

BOOTS DOMINIERT DEN MARKT

1. Boots.com

2. Lloydspharmacy.co.uk

3. Superdrug.com

4. Tesco.com

5. Pharmacy2u.co.uk

6. ChemistDirect.co.uk

7. Thecooperativehealthcare.co.uk

8. Rowlandpharmacy.co.uk

Umsatz-Rangliste 2014

Non-Rx

1. Boots 65%

2. Lloyds 13%

3. Chemistdirect 4%

4. Pharmacy2u 3%

5. Superdrug 2%

Markenbekanntheit

2014 (ungestützt)

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

BOOTS: MULTI-CHANNEL STEHT IM FOKUS

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

BOOTS: KANN

ALLES – ZUM

GUTEN PREIS

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

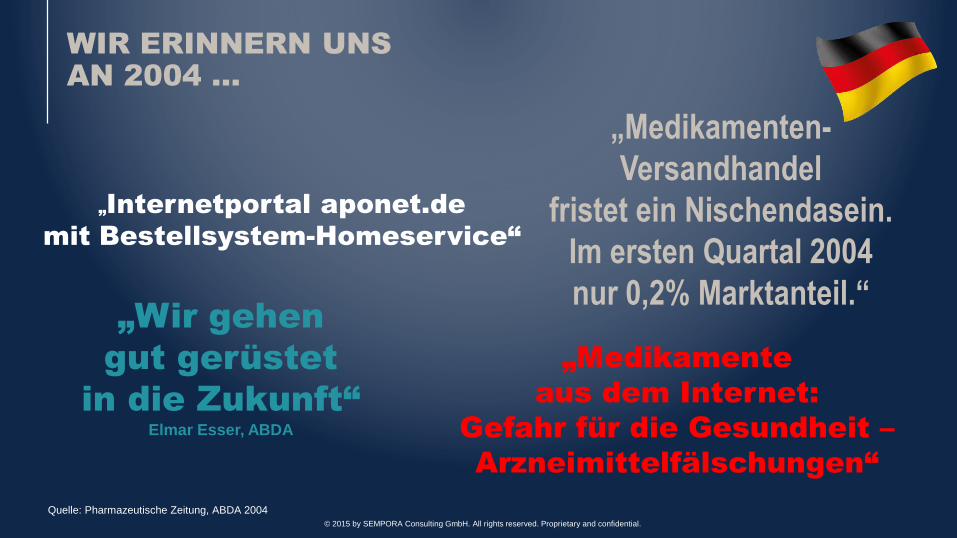

WIR ERINNERN UNS

AN 2004 ...

Quelle: Pharmazeutische Zeitung, ABDA 2004

„Medikamenten-

Versandhandel

fristet ein Nischendasein.

Im ersten Quartal 2004

nur 0,2% Marktanteil.“

„Internetportal aponet.de

mit Bestellsystem-Homeservice“

„Wir gehen

gut gerüstet

in die Zukunft“

Elmar Esser, ABDA

„Medikamente

aus dem Internet:

Gefahr für die Gesundheit –

Arzneimittelfälschungen“

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

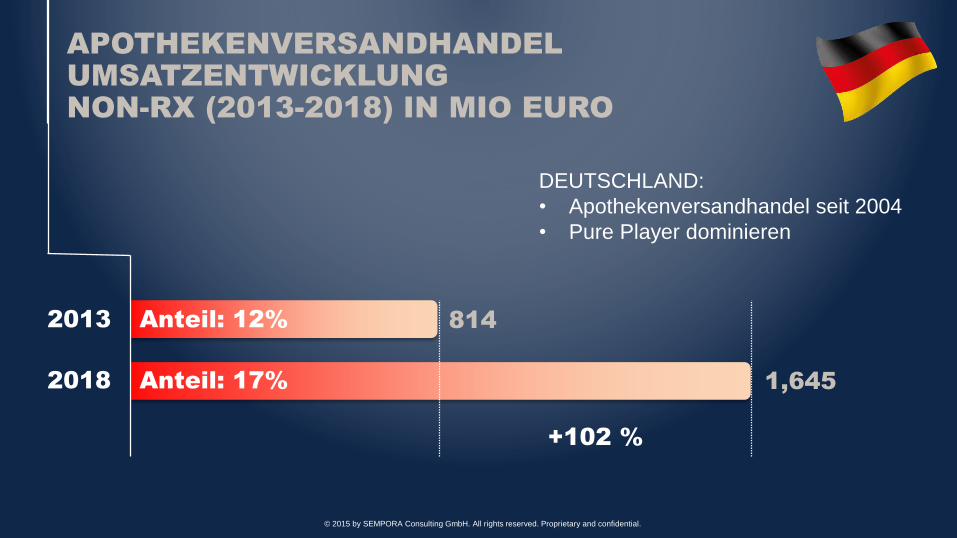

APOTHEKENVERSANDHANDEL

UMSATZENTWICKLUNG

NON-RX (2013-2018) IN MIO EURO

2018

Anteil: 12%

+102 %

Anteil: 17%

2013 814

1,645

DEUTSCHLAND:• Apothekenversandhandel seit 2004• Pure Player dominieren

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

SHOP-APOTHEKE IST MARKTFÜHRER

1. Shop-apotheke.com 138

2. Apo-rot.de 120

3. Medikamenteperklick.de 100

4. Apotal.de 80

5. Medpex.de 75

6. Sanicare.de 70

7. Docmorris.de 68

8. Apo-discounter.de 60

Umsatz-Rangliste

Non-Rx 2014/2015 (Mio €)

1. Docmorris 64%

2. Shop-apotheke 49%

3. Sanicare 42%

4. Apotal 33%

5. Apo-discounter 32%

6. Mycare 30%

7. Medpex 27%

8. Apo-neo 23%

Markenbekanntheit

2015 (gestützt)

Quelle: SEMPORA Research, Expertengespräche, SEMPORA Apothekenmarktstudie 2015© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

APOTHEKENVERSANDHANDEL

UMSATZENTWICKLUNG

NON-RX (2013-2018) IN MIO EURO

2018

Anteil: 4%

+280 %

Anteil: 8%

2013 36

101

ÖSTERREICH:• Apothekenversandhandel

seit Mitte 2015ABER: Ausländer liefern seit 2010 nach Österreich

• Pure player• Nicht jeder bietet

österreichisches Sortiment an

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

AUCH IN ÖSTERREICH IST

SHOP-APOTHEKE AUF PLATZ 1

1. Shop-apotheke.at (D) 11

2. Apo-rot.at (D) 10

3. Apotheke-Österreich.at (CZ) 8

4. ZurRose.at (D) 7

5. Vamida.at (CZ) 3-4

6. Mycare.at (D) 3

7. Apotheke.at (D) 3

8. Servusapotheke.at (CZ) 2

Umsatz-Rangliste

Non-Rx 2014/15 (Mio €)

1. Apotheke-Österreich 29%

2. Zur Rose 19%

3. EU-Versandapotheke 11%

4. Shop-apotheke 11%

5. Mycare 10%

6. Vfg 8%

7. Apo-rot 8%

8. Sanicare 7%

Markenbekanntheit

2014 (gestützt)

Quelle: SEMPORA Research, Expertengespräche, SEMPORA Studie Versandhandel Österreich 2014

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

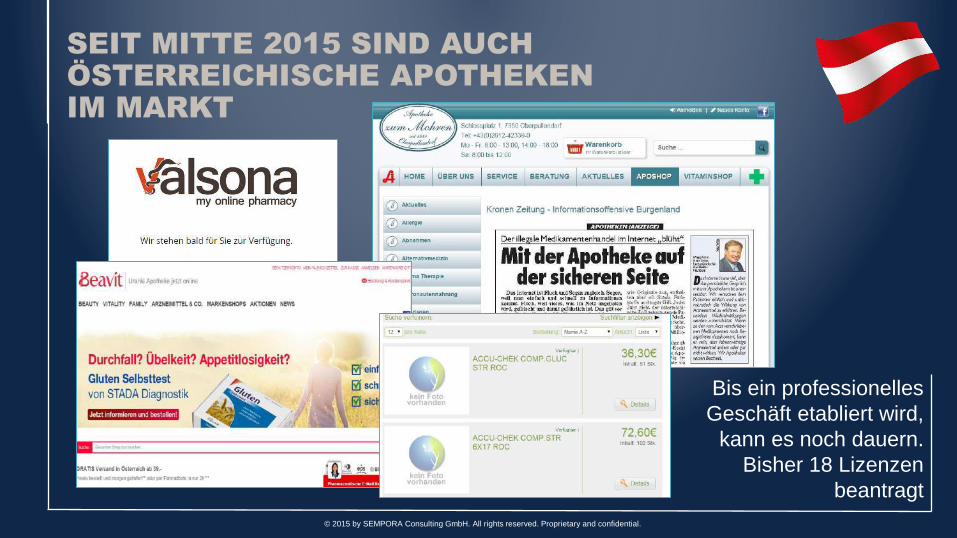

SEIT MITTE 2015 SIND AUCH

ÖSTERREICHISCHE APOTHEKEN

IM MARKT

Bis ein professionelles Geschäft etabliert wird,

kann es noch dauern.Bisher 18 Lizenzen

beantragt© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

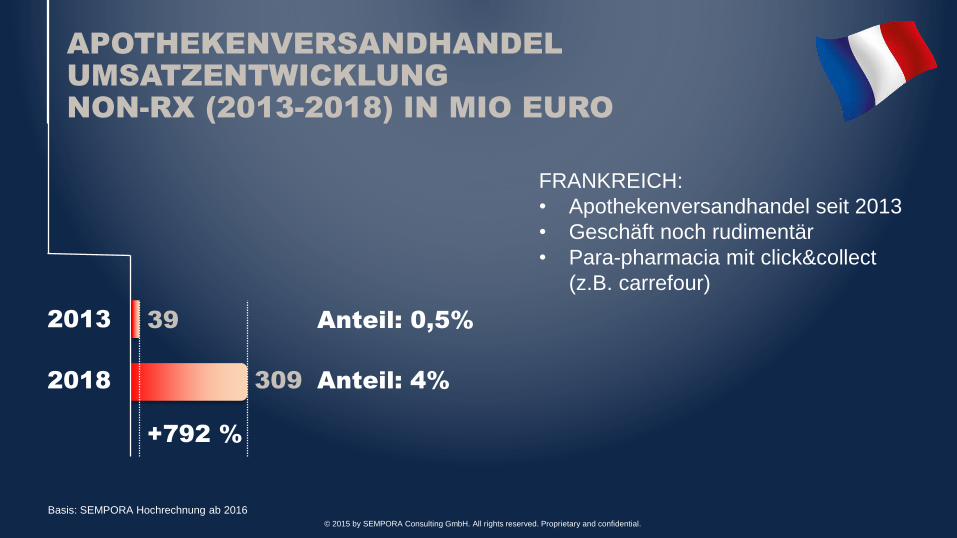

APOTHEKENVERSANDHANDEL

UMSATZENTWICKLUNG

NON-RX (2013-2018) IN MIO EURO

Anteil: 0,5%

+792 %

Anteil: 4%

2013 39

309

FRANKREICH:• Apothekenversandhandel seit 2013• Geschäft noch rudimentär• Para-pharmacia mit click&collect

(z.B. carrefour)

2018

Basis: SEMPORA Hochrechnung ab 2016© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

L‘ORÉAL: DIREKT AN DEN VERBRAUCHER

WWW.MY-DERMACENTER.COM/FR

Brand portfolio

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

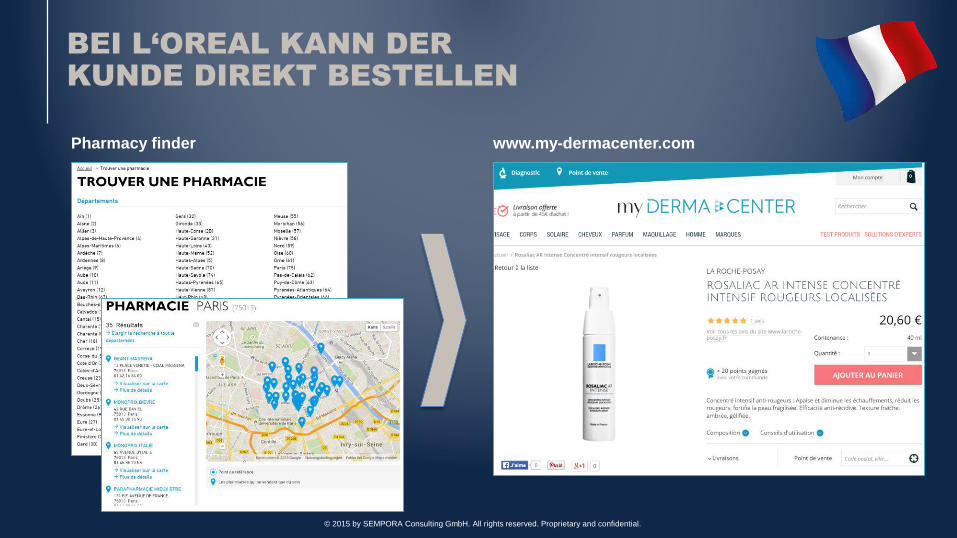

BEI L‘OREAL KANN DER

KUNDE DIREKT BESTELLEN

Pharmacy finder www.my-dermacenter.com

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

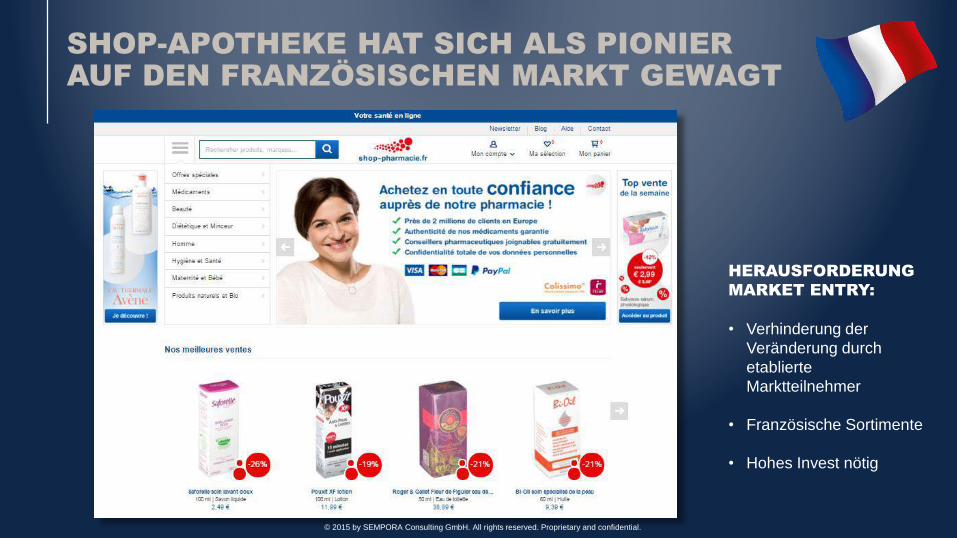

SHOP-APOTHEKE HAT SICH ALS PIONIER

AUF DEN FRANZÖSISCHEN MARKT GEWAGT

HERAUSFORDERUNG

MARKET ENTRY:

• Verhinderung der Veränderung durch etablierte Marktteilnehmer

• Französische Sortimente

• Hohes Invest nötig

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

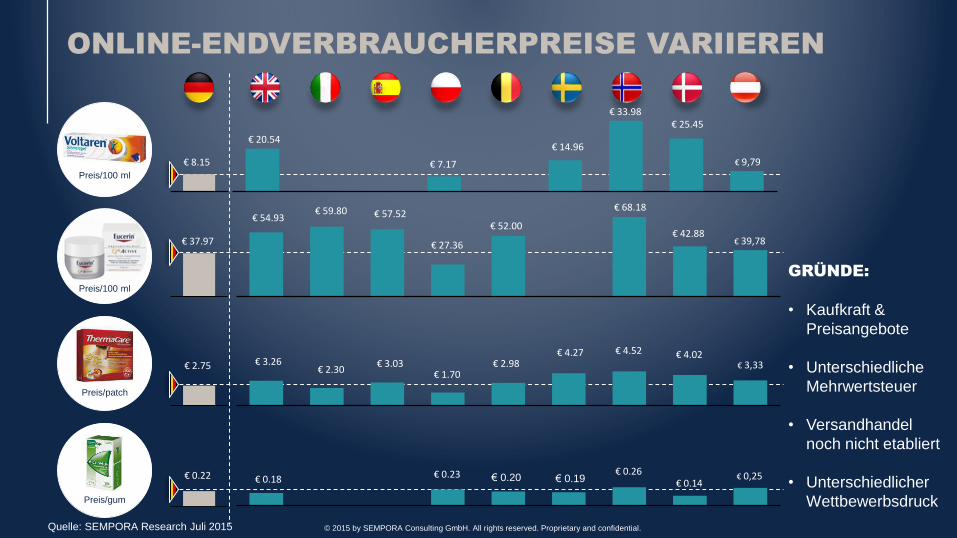

ONLINE-ENDVERBRAUCHERPREISE VARIIEREN

€ 25.45

€ 14.96

€ 7.17

€ 20.54

€ 33.98

€ 8.15

€ 42.88€ 27.36

€ 68.18€ 54.93 € 57.52

€ 52.00

€ 59.80

€ 37.97

€ 3.26€ 4.02

€ 2.98€ 4.52

€ 1.70€ 3.03

€ 4.27

€ 2.30€ 2.75

€ 0.26€ 0.20

€ 0.14€ 0.19€ 0.18 € 0.23€ 0.22

Preis/100 ml

Preis/100 ml

Preis/patch

Preis/gum

€ 9,79

€ 39,78

€ 3,33

€ 0,25

GRÜNDE:

• Kaufkraft & Preisangebote

• Unterschiedliche Mehrwertsteuer

• Versandhandel noch nicht etabliert

• Unterschiedlicher Wettbewerbsdruck

Quelle: SEMPORA Research Juli 2015 © 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

ENTWICKLUNG

VERSANDHANDELSMARKT

EUROPA

2013

2,26 Mrd €

2018

5,018 Mrd €

Entry

Developing

Maturing

183210

1.867

525 (+187%)

965(+359%)

3.528(+88%)

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

2018 WERDEN INTERESSANTE MARKTGRÖSSEN IN

NEUEN MÄRKTEN ERREICHT

NON-RX VERSANDAPOTHEKENMARKT 2018 IN MIO €

Groß-

britanien

Deutschland Frankreich Polen Italien Spanien Österreich Belgien Schweden Norwegen Niederlande Rumänien Tschechien Dänemark Slowakei Bulgarien Ungarn Portugal

16,5 17,0 3,6 9,7 3,0 4,0 8,0 4,0 10,0 10,0 3,0 1,0 4,0 5,0 4,0 2,0 1,0 1,0

Anteil an Non-Rx (in Prozent):

1.8831.645

309

245

196 181

101 91 91 88

37 31 28 25 25 23 11 8

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

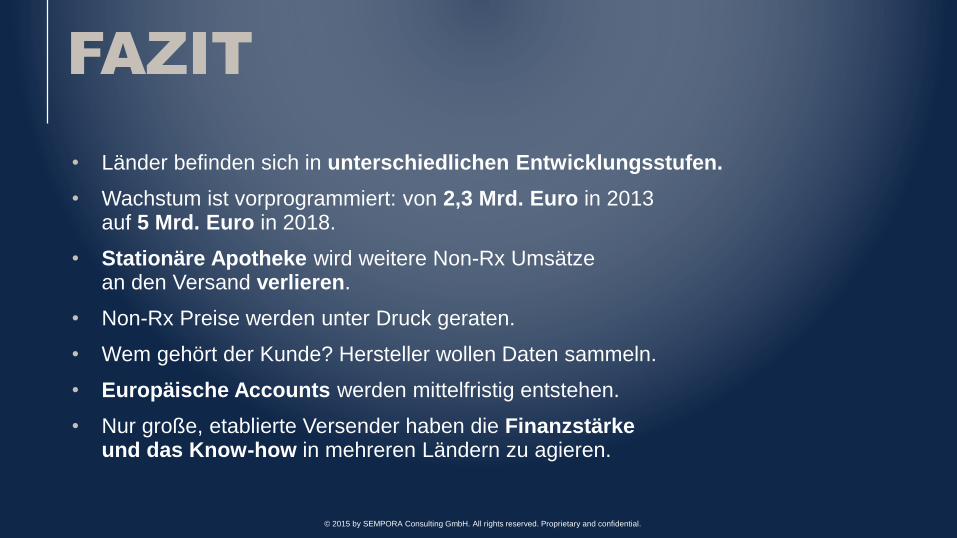

FAZIT

• Länder befinden sich in unterschiedlichen Entwicklungsstufen.

• Wachstum ist vorprogrammiert: von 2,3 Mrd. Euro in 2013 auf 5 Mrd. Euro in 2018.

• Stationäre Apotheke wird weitere Non-Rx Umsätze an den Versand verlieren.

• Non-Rx Preise werden unter Druck geraten.

• Wem gehört der Kunde? Hersteller wollen Daten sammeln.

• Europäische Accounts werden mittelfristig entstehen.

• Nur große, etablierte Versender haben die Finanzstärke und das Know-how in mehreren Ländern zu agieren.

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

QUELLEN

• ABDA Germany

• AESGP

• Agencia Española de Medicamentos y ProductosSanitarios

• Algemene PharmaceutischeBond

• AOK Bundesverband (2015)

• Apotekforeningen 2015

• BPI: Erstattungszentren in Europa und den USA (2010)

• Catena Farmaceutica

• CEF Farmaciainsieme

• CIA World Factbook

• CNGPO

• commonwealthfund.org

• Croatian Medical Journal (2012)

• Eminet www.ec.europa.eu

• EUAV (Les Echos Etudes)

• European Observatory on Health Systems and Policies

• European Pharmacists Forum

• Eurostat

• Farma Campania

• Farmatua

• FECOFAR

• Federazione Nazionale UnitariaTitolari di Farmacia

• FederFARMA.CO S.p.A

• Föderaler Öffentlicher Dienst Belgien (2015)

• GIRP

• Google Our Mobile Planet

• HSCIC

• Hungarian Central Statistical Office (2015)

• IMS Health Data

• IMS Health Retail & Hospital Audits Synopsis 2012

• IMS Pharmaceutical Pricing & Reimbursement Concise Guide

• IMS Report

• INFARMED

• Institut nationale de la statistique et des étudeséconomiques

• ISPOR

• James Dudley – Entering thedigital battleground (2015)

• James Dudley – Management Pharmacy Survey (2014)

• Ministére des Affaires Socialesde la Santé et des Droites des Femmes

• Ministry of Foreign Affairs ofDenmark

• National Institute for Quality-and OrganizationalDevelopment in Healthcare andMedicine (2015)

• Norwegian Medicines Agency

• OECD

• Ordem dos farmacêuticos

• PPRI

• Sector Report 2013 –Pharmaceutical and HealthcareSector Bulgaria

• SEMPORA Marktreport Französischer Apothekenmarkt

• SEMPORA Study: The UK Pharmacy Market 2014

• SIMV – French association ofhealth animal industry

• Sinfarma Soc. Coop

• Statista

• The World Bank

• WHO

© 2015 by SEMPORA Consulting GmbH. All rights reserved. Proprietary and confidential.

Ansprechpartner für weitere Details der Studie:Tobias BrodtkorbManaging Partner

[email protected] 45349-30