Embed Size (px)

Citation preview

1

GeschGeschääftsentwicklungftsentwicklungTechnische KunststoffeTechnische Kunststoffe

StrategiegesprStrategiegespräächch TecPartTecPartLudwigshafen, 17. November 2010Ludwigshafen, 17. November 2010Willy BertWilly Bert HovenHoven--NievelsteinNievelstein, Engineering Plastics Europe, Engineering Plastics Europe

2

BASF at a glance

BASF –The Chemical Company

Chemistry is about every aspect of life.

We are connected to deliverintelligent and sustainable solutions.

Sales 2009: €50,693 mill.

EBIT 2009: €3,677 mill.

Employees (December 31, 2009):104,779

About 1,300 new patents filed

6 Verbund sites and about 380production sites

3

BASF SegmentsC

hem

icals

Pla

sti

cs

PerformancePolymers

Polyurethanes

Crop Protection Oil & Gas

Perf

orm

an

ce

Pro

du

cts

Paper Chemicals

Dispersions& Pigments

Care Chemicals

PerformanceChemicals

Inorganics

Petrochemicals

IntermediatesF

un

cti

on

al

So

luti

on

s

ConstructionChemicals

Coatings

Catalysts

Ag

ricu

ltu

ral

So

luti

on

s

Oil

&G

as

Styrolution(01.01.2011)

4

BASF Group:Sales by segment 2009

BASFGroup

Million € (change compared with previous year)

Chemicals

7,515 (-32.7%)

Plastics

7,128 (-21.8%)

Performance Products

9,356 (+15.2%)

Oil & Gas

11,356 (-21.4%)

Agricultural Solutions

3,646 (+7.0%)

Functional Solutions

7,115 (-24.2%)

Other

4,577 (-31.2%)

22.4%

7.2%

14%

9%

18.5%

14.1%

14.8%

50,693

5

BASF Group: Sales by region 2009by location of customer

BASFGroup

Million € (Change compared with previous year)

North America

9,423 (-21%)

South America,

Africa, Middle East

4,032 (-8%)

Europe

28,532 (-22%)

Asia Pacific

8,706 (-7%)

56.3%

17.2%8%

18.6% 50,693

6

BASF sales by customer industry*

* Distribution by direct customers of BASF

Percentage of sales in 2009

> 15%

10-15%

< 5%

5-10%

10-15%

Chemicals

Automotive /

Construction / Utilities

Agriculture /

Plastics industry / Oil industry

Electrical/Electronics /

Furniture / Paper

Other industries

7

BASF how we achieve value-addinggrowth

We earn a premium onour cost of capital

We help our customersto be more successful

We ensuresustainable development

We form the bestteam in industry

+

8

BASF Group:Sales and Earnings

15

20

25

30

35

40

45

50

55

60

65

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Sales

Income from

operations (EBIT)

50.7

3.7

1

2

3

4

5

6

7

8

9

10

11

Billion €

9

RBU Engineering PlasticsNAFTA

Wyandotte, USAGVP: Larry Berkowski

Division Head: Wolfgang Hapke, Ludwigshafen

GBU Polyamide & Intermediates, Ludwigshafen, GermanyGVP: Udo Bergmann

GBU Foams, Ludwigshafen, GermanyGVP: Giorgio Greening

GBU Specialty Plastics, Ludwigshafen, GermanyDirector: Robert Heger

RBU Engineering PlasticsEurope

Ludwigshafen, GermanyGVP: Willy Hoven-Nievelstein

RBU Engineering PlasticsAsia Pacific

Singapore, SingaporeGVP: Hermann Althoff

Performance Polymers – OrganizationThree global and three regional business units

10

BASF Verbund SegmentsBASF Performance Polymers

Electrical &Electronics

Automotive

Universal

Polyamide 6.6

Caprolactam

Adipic acid

Polyamide 6

Trioxan POM

PBT

PES/PSU

CP: Cyclohexane

HMD

Compounds

DHDPS

Engineering Plastics KTEValue Chains KT

Compounds

Compounds

Engineering Plastics (KTE)

CZ: Butanediol .

DCDPS

DMT, PTA

External

Polyamide & Intermediates (G-KTI)

Compounds

Compounds

ADN CP: Butadiene .

CA: Formaldehyde

11

EngineeringPlastics

SpecialtyPlastics

FoamsPolyamide &Intermediates

PS FoamsStyropor®

Neopor®

Styrodur® CPeripor®

Specialty FoamsBasotect®

Neopolen®

BiodegradablePolymersEcoflex®

Ecovio®

Further productsPalatal®

Palusol®

Polyamide 6.6Ultramid® A

Polyamide 6Ultramid® B

Polyamide 6.66Ultramid® C

Adipic Acid

Caprolactam

Hexamethylendiamine

Performance Polymers KTProductportfolio

PA CompoundsUltramid® A, B, C, TMiramid®, Capron®

PBTUltradur®

POMUltraform®

PESU/PSU/PPSUUltrason® E, S, P

12

Performance Polymers KT

Production, Technical Centers andOffices in All Regions

Antwerp

Freeport

Kuantan

Shanghai

Wyandotte

Sparta

Altamira

LeunaSchwarzheideRudolstadt

PasirGudang

GreaterNagoya

Hong Kong

Singapore

AnsanBudd LakeFlorhamPark

Ulsan

Sao Paulo

Guaratinguetá

Santiago

Mexico City

Nanjing

Tudela

Buenos AiresConcon

Thane

Bibbiano

Production

TechnicalCenters

OfficesGeneral Lagos

LU

13

Rhodia

Ticona

Solvay

DuPont

DuPont

Sabic

DuPont

Sabic

European market position of maincompetitors in Engineering Plastics2008 (ranking)

14

Strategiegespräch TecPartAgenda

Geschäftsentwicklung

Trends

Chancen und Risiken

Materialverfügbarkeit

15

Plastics Production in the World

0

50

100

150

200

250

300

1940 1950 1960 1970 1980 1990 2000 2010 2020

Mio Tons

2009: 230

1989: 100

1976: 50

1950: 1,5

2002: 200

1985: 50

2009: 55

Europe :(WE und CE)

24,0 %

Source: PlasticsEurope Market Research Group (PEMRG)

16

Total consumption ~ 4 Mio. Tons in 2007 (pre crisis year)

Regional Market DistributionEngineering Plastics* (PA, PBT, POM, aHTT)

* Inj. Molding

NAFTA

19%

Asia

40%

Europe

37%

ROW

4%

aHTT

1%

PA

65%POM

17%

PBT

17%

aHTT

3%

PA

60%

POM

17%

PBT

20%

PBT

26%

POM

30%PA

43%

aHTT

1%

ROW4%

Asia is the largest market forEngineering plastics !

Europe remains still thelargest market for Polyamide !

17

Plastics Demand EuropeEngineering Plastics* (PA, PBT, POM, aHTT)

* Inj. molding

Demand decreased by approximately 30% iduring the crisis

~ -30%

0

500

1.000

1.500

2.000

PA

PBT

POMaHTT

Only in 2013 the pre crisis level will be reached again

Estimated point in time to beBack on pre crisis levels:

- PA: 2014- PBT: 2010- POM: 2012- aHTT: almost no decline

Source: PCI, AMI, BASF

18

Development of Regional Demand in EuropeAll Plastics (2007 – 2009)

Source: PlasticsEurope Market Research Group (PEMRG)

● 2009 ● 2008 ● 2007

WESTERS EUROPE:- All plastics:~ -15%- Eng. Plastics: ~ -30%

Eastern Europe (EU12 neu):- Almost no decline !

19

Ifo Geschäftsklima DeutschlandGewerbliche Wirtschaft

Dotcom Blaseplatzt

Pleite vonLehmannBrothers

Index “Beurteilung der Geschäftslage” folgt der Nachfrage(von 2006 bis 2008 verschlechterte sich bereits das Wirtschaftsklima spürbar !)

20

JD PowerEstimated European Light Vehicle Assembly

Light Vehicle: passenger car plus light commercial vehicles < 6t Eastern Europe: including Russia and Turkey

In 2010 ~ 4 Mio. cars less will be built compared to pre crisis levels!

21

ACEA (European Automobile Manufacturers Association)

New Passenger Car Registration Europe

Growth in Automitive is currently heavily driven by exports to Asia andthe US

22

Business Development in the E/E-IndustryZVEI - Zentralverband Elektrotechnik- und Elektronikindustrie e.V.

23

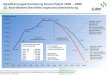

Kunststoffindustrie DeutschlandProduktionsentwicklung

Die Konjunktur in der Kunststoff-industrie in Deutschland hat sich seitFrühsommer 2009 wieder deutlich erholt.Der kräftige Aufschwung aus den Vor-monaten, hat auch im Verlauf des drittenQuartals 2010 angehalten.

Erzeuger (Kunststoffe in Primärform)Die kräftige Erholung der Produktion setztsich fort. Die mengenmäßige Produktionhat inzwischen wieder das Vorrezessions-niveau erreicht.

Verarbeitung von KunststoffenDer deutliche Aufschwung führte dazu,dass das Vorrezessionsniveau fast wiedererreicht wurde.

MaschinenbauDie konjunkturelle Erholung hat sich seitdem letzten Quartal 2009 mit deutlichenZuwächsen im Auftragseingang bemerk-bar gemacht. Auch die Produktion zogallerdings später als bei den Erzeugernund Verarbeitern wieder an. Seit Jahres-beginn 2010 geht es wieder kräftig auf-wärts. Der Rückgang im deutschenMaschinenbau war - von einem Rekord-niveau ausgehend - deutlich stärker alsbei Erzeugern und Verarbeitern, ebensoist die Erholung nun stärker ausgeprägt.

50

60

70

80

90

100

110

120

130

2005 2006 2007 2008 2009 2010

Produktionsindex(2005 = 100, Trendzyklus, monatlich)

Kunststoffe in Primärform

Verarbeitung von Kunststoffen

Kunststoffmaschinen

Quelle: Destatis / Arbeitskreis Marktforschung WVK

Aktueller Datenstand: 08/2010

24

KunststoffindustrieProduktionsentwicklung Deutschland und EU27

Die Kunststoffindustrie in Europa ist aufdem Weg der Erholung, allerdings ist dieDynamik spürbar langsamer als inDeutschland.

Die Kunststoffindustrie in Deutschlandist bei Erzeugern, Verarbeitern undMaschinenbauern zur Zeit die Lokomotivein Europa.

Der Produktionsanstieg ist bei denErzeugern stärker ausgeprägt als bei denVerarbeitern, was auch auf positivelagerzyklische Einflüsse zurückzuführenist.

Umgekehrt war in der Rezession derProduktionsrückgang bei den Erzeugernstärker als bei den Verarbeitern.

Auch der Maschinenbau zeigt einedeutliche Aufwärtsentwicklung, wobeiauch hier Deutschland als Lokomotivefungiert.

40

50

60

70

80

90

100

110

120

130

2005 2006 2007 2008 2009 2010

Produktionsindex(2005 = 100, Trendzyklus, monatlich)

Kunststoffe in Primärform (D)

Kunststoffe in Primärform (EU27)

Verarbeitung von Kunststoffen (D)

Verarbeitung von Kunststoffen (EU27)

Kunststoffmaschinen (D)

Kunststoffmaschinen (EU27)

Quelle: Destatis / Arbeitskreis Marktforschung WVK

Aktueller Datenstand: 08/2010

25

Strategiegespräch TecPartAgenda

Geschäftsentwicklung

Trends

Chancen und Risiken

Materialverfügbarkeit

26

Demand by Regions 2007 Demand by Regions 2015e

w/o Other Plastics (40 to 45 Mio t) w/o Other Plastics (~50 Mio t)

CAGR: 5.0%

215 Mio t 330 Mio t

Source: PlasticsEurope Market Research Group (PEMRG)

World Plastics Materials Demand

NAFTA

22.0%

Latin

America

5.0%

Europe

(WE + CE)

22.5%

Middle

East,

Africa

6.0%

CIS

3.0%

Japan

5.0%

China

22.0%

Rest of Asia

14.5%

.

NAFTA

19.0%Latin

America

5.0%

Europe

(WE + CE)

21.0%Middle

East,

Africa

6.0%

CIS

4.0%

Japan

4.0%

China

25.0%

Rest of Asia

16.0%

27

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Growth above BIPEngineering Plastics* (PA, PBT, POM, aHTT)

* Inj. Molding

2010 2020

Source: BASF

2005 2007

BIP (EU27) TK (EU27)

3.8% p.a.

2.0% p.a.

28

ProfitabilityContinued pressure on margins

The business with Engineering plastics was heavily hit by the crisis(> -40%). Polyamide was hit the most

DEngineering Plastics producers were already impacted before thecirisis because margins were already eaten up by increased rawmaterial cost. Additional capacities were delayed respectively notbuilt at all.

Raw materials price (PA/PBT/POM precursor) most probably willfurther increase in 2011, which will lead to additional marginpressure.

29

Focus on InnovationProduct Developments

~ 1980s high performance polymers „will rule the world“

~ 1990s “blends are the solution”

~ 2000s “New Polymere” (Questra® ,Carylon®)

~ 2010s smart building blocks, smart blends, functional & nanoadditives and specialties

Fazit:

New polymere will only be successful in niche areas

Existing polymers will be modified to fulfill market requirements

(including polymere on renewable resources).

Producers will differentiate increasingly through spezialities

30

€New Application

(metal replacement,new markets like solar energy …)

New / improved Products(e.g. High Speed, FR, UV resistent,

High Strength, High Heat …)

New Production process(e.g. Pulltrusion for LGF ...)

Engineering Plastics KTE

Key elements to create value for thecustomer and BASF

New Processing Technology(Dolphin, direct metallization,Selective Laser Sintering ...)New Simulation and

testing methods(UltrasimTM, topological optimization ...)

31

Strategic Business Development alongMegatrends

MEGATRENDS

Globalization &Developing Markets

UrbanizationGrowing & agingPopulation

Energy Demand& Climate Protection

Individualisation

Health &Nutrítion

Living &Construction

Energy &Resources

Mobility &Communication

Mobility &Lifestyle

Influence on our business ? Find the most promising opportunities !

32

Energy DemandResources& ClimateProtection

GrowingRaw Material

Demand

Description

Demandfor Water

Increase ofEnergy demandand efficiency

CleanEnvironment

ResponsibleCare

Challenge

New EnergiesEnergy Storage& Distribution

Public & RuralWater Supply

Affordable,efficient useof material

Eco-efficientProducts

Bio PolymersHeat storage …

Business Development

BatteriesEnergy

Distribution NetGreen Powertrain

Solar energy

Water treatmentWater

InfrastructureDesalination

MiningOil- and Gas-Exploration

Sea-Application

Megatrends Drive Innovations

33

Bio-Based PolyamidesÖko-Efficiency-Portfolio

Base Case:

Production, Useand Disposal of atypical air intakemanifold (AIM)for a passengercar over adistance of200.000 km

From an ecological point of view PA6.6 and PA5.10represent the lower performing alternatives.

34

Performance Polymers KT

From Commodities to Specialties

High

Low

Productioncosts

Productcharacteristics

PC

Polyamide

PPO

PMMA

PS

PP

EPS construction

ABS

POM

PBT

PUR specialties

ASA

PUR basic products

EPSpackaging

PEPVC

Circle size = consumption

KT products

Price mainlydetermined by ...

Differen-tiationpotentialin themarket

Standardproducts

Specialties

PET(bulk)

SAN

SBC

aHTTP*

*e.g. PSU; PES

35

Trends Engineering PlasticsProduction

Compounds

Compounding where the customers are – issue countrieswith yet small markets

Balance between large scale compounders and flexiblemarket reaction

Polymers

Balance between large scale production of polymers andflexible prodcution units

Regional complexity – access to raw materials and energyvs. access to markets

36

Trends in the Engineering PlasticsIndustry - Summary

Engineering Plastics will continue to grow above GDPs

Additional growth will be generated through the contribution ofEP to solutions for climate change and resource issues

A further shift „East“ will happen

Standardization of plastics will increase, but valuedifferentiation will become more important at the same time(Innovations)

Large Companies will further globalize

The need for cost leadership will reduce the number ofsuppliers

New polymers will only be successful in niche areas

Mobility, E/E and packaging will drive further growth

37

Strategiegespräch TecPartAgenda

Geschäftsentwicklung

Trends

Chancen und Risiken

Materialverfügbarkeit

38

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

1990

1995

2000

2005

2010

2015

2020

PA

66

Dem

and

inM

ioto

/a

Kapazitäten in der PolyamidWertschöpfungskette sind genügendvorhanden

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

1990

1995

2000

2005

2010

2015

2020

PA

6D

em

and

inM

ioto

/a

Film

EP

Staple

Carpet

Industrial

Textile

Film

EP

Staple

Carpet

Industrial

Textile

Source: PCI

39

Engineering Plastics KTE

Future Challenges

Margin development

Portfolio shifts / regional transfers

Return on investment (assets)

Retun on projects (new application developments)

Technology develpment („Plastics“ / „Parts“)

Business modells

People

Government regulations

Public opinion

40

Strategiegespräch TecPartAgenda

Geschäftsentwicklung

Trends

Chancen und Risiken

Materialverfügbarkeit

41

Supply situation 2010 for manyproducts worldwide

Supply situationSupply situation

Delivery

Plant availability

Inventory

Demand vs. planning

42

Inventory LevelsThe Plastics industry was hit very hard in 2008 by theeconomic crisis

Strong business decline from January to December 2008 (e.g. for Eng.Plastics in BASF – 67%)

Order entry almost stalled in Q4

Return of business in Q1 – Q2 2009 to a level of ~ 75 %

Reduction of production volumesReduction of inventory levels down to safety stocks only

In 2009 the economic outlook remained weak

Production priority: Products made to order !

43

Cautious ForecastThe economic recovery was better than expected

The growth forecast of our customers for 2010 was in therange of +10 % (compared to a minus 25% level in H2/20009 vs. H1/2008)

Continued low production volumesContinued low inventory levelsLow forecast for precursors (raw materials, additives, glass fibers, etc.)

In Q1/2010 demand increased by around 35%

Safety stocks were quickly depletedZero inventory levelsBased on low forecasts shortage of precursors(raw materials, additives, glass fibers, etc.)

44

Plant availabilityExample: BASF Engineering Plastics in Europe in 2009

Capacity utilization in compounding down to 25%

Polymerization running at 40 % utilization rate

Risk analysis to run polymerization at low utilization rates

Production conditions in 2009:

Start-up conditions in 2009/10:

Shifts in operational working points led to malfunctions(mass balances, volume flows, pressures, temperatures)

Production change over increases to serve customerdemands = capacity loss

Unforeseen technical problems

45

Supply situation 2010 for many productsworldwide

Supply situationSupply situation

Delivery

Plant availability

Inventory

Demand vs. planning

~ 0

46

Compounds - different additives,pigments, glass fibers

Polyamide 66 - polymer precursors

PBT - butanediol

POM - polymer

Polyamide 6 - caprolactam

Product availability issues inEngineering Plastics

47

Materialknappheit und ihreEntwicklung

Start up issues (HMD-production are resolved)

Supply contracts optimized (utilization of two C4-based-suppliers)

Polymer demand covered via 2nd source (C3) (~ 10%)

Polymer availability will remain tight in the market

Polyamide 66

Impact modifier(wax – additives)

Production issues resolved/production structuresoptimized

Force Majeure expected to be lifted in Q4

Product development initiated to provide technicalalternatives

Other additives(e.g. glass, pigments, )

Raw material availability will remain tight in the industrydue to increased production changes but also due todemand beyond previous years (halogene-free flame retardants)

Overall product availability will improve in Q4 2010

48