Embed Size (px)

Citation preview

1

Biorenewables beyond bioenergy -

- creating sustainable value

RWTH Aachen | 18 june 2014

Luuk van der Wielen and Jan van Breugel

Biomass production - for what reason ?

• food & feed

• pulp & paper

• classical construction materials: wood etc

• power & heat

• liquid transport fuels (ethanol, advanced fuels)

• chemicals & polymers

• novel (in)organic) (construction) materials: biofoam,

biocement, biogrout, bioasphalt, others …

Or a mix / portfolio – target :

all biomass-to-value !

Biomass production - for what market ?A. drop-in (fuels, syngas, H2, biogas, bioethene, biosuccinate, bioPET, …)

blend with existing economy (existing industry, infrastructure, capital,

products, buyers, … so ‘hail shale gas’ ?), or

B. substitute (PLA, PEF, biojet fuel…) replace existing products by

biorenewables (similar functionalities, reduced emission - cost, …), or

C. drop-out: (bioconcrete, biosolar, …) “New Bioeconomy” (novel products-

industries, away from vested interests, full benefit of sustainable*

development, rural development-jobs-income, distributed manufacturing,

… but Bio-Bubble – remember “New Economy-2001” ?)

• Can A, B, C can all be realities ?

• What does it require ?

* climate, economic, social

contents

1. Why ? global & regional drivers

2. How ? BBE technology portfolio

3. What ? feedstocks, products, yields – role of

scale and logistics

4. How – again ?

5. Why – again ?

Global drivers for a BBE ?

• more people with more wealth

• less nett GHG emission (global warming)

and/or climate adaptation

• politics (security of oil/gas supply)

• innovation, rural income and economic development

• increasing (and decreasing) prices of resources

• in time*, limited fossil reserves

• add sustainability to food chain

• add value to food chain and prevent hunger

Pick your personal selection !

Demand : stabilisation CO2 emissions of transport

transport fuels = 2 billion ton (GT)/jr worldwide,

annual growth 1.5% or 30 MT/yr (~120 MT/yr biomass)

` investments in 2nd generation production:

→ 200 plants or $ 50 billion every year

→ every 3 years an extra Port of Rotterdam (360 MT/jr)

→ (or every 5-6 years new Port of Shanghai)

Potential: residuals & energy crops

• maximum estimate

• global total demand

• average

• double

• current50

450700 EJ/jr

300100

Scales of biorenewables (illustration)

2

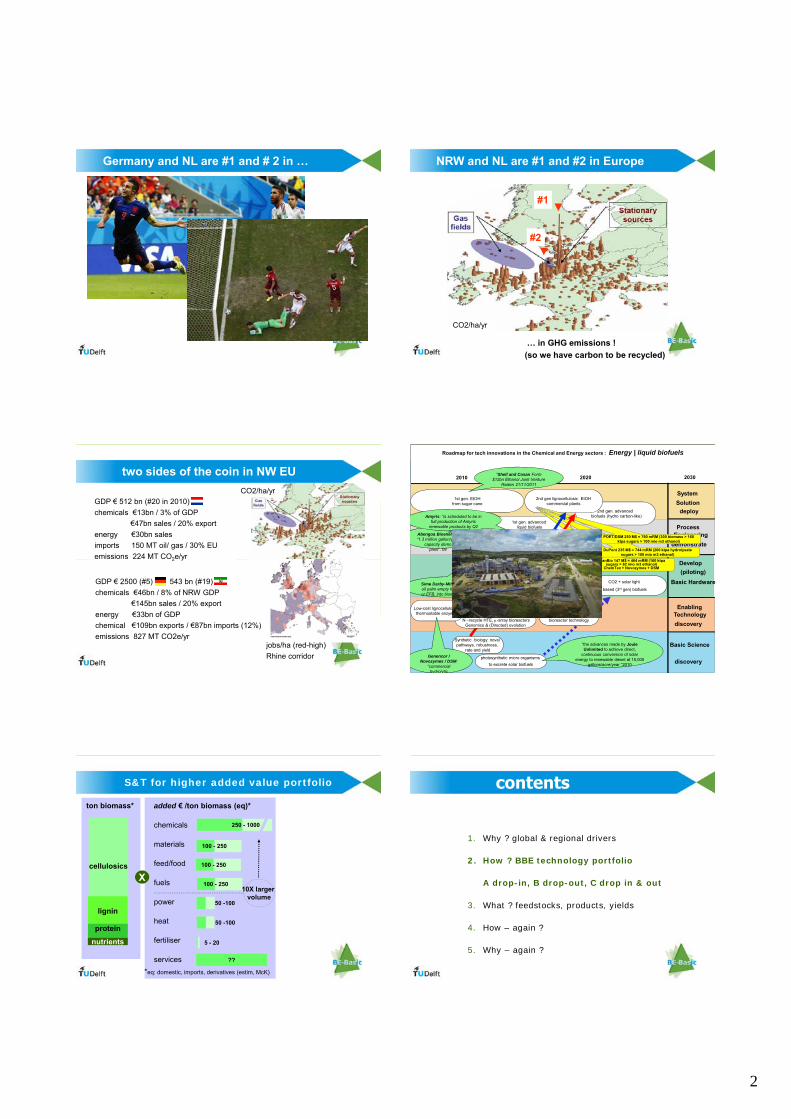

Germany and NL are #1 and # 2 in … NRW and NL are #1 and #2 in Europe

CO2/ha/yr

#1#1

#2#2

… in GHG emissions !

(so we have carbon to be recycled)

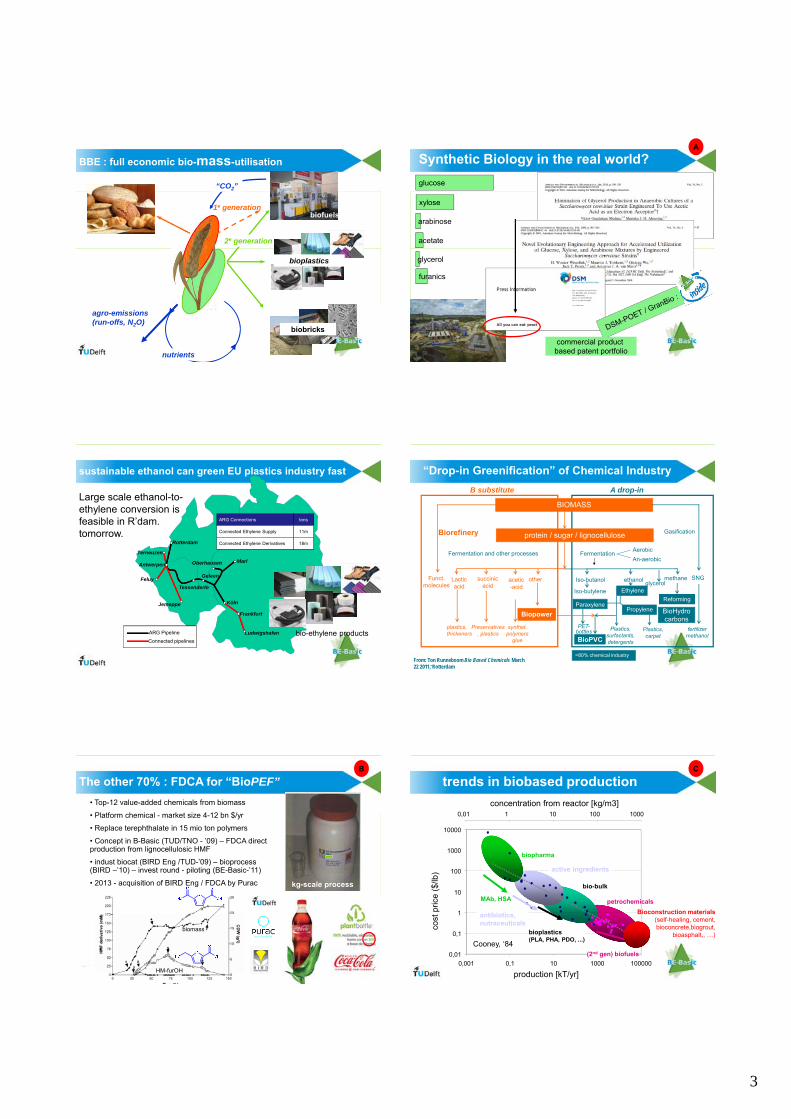

two sides of the coin in NW EU

GDP € 512 bn (#20 in 2010)

chemicals €13bn / 3% of GDP

€47bn sales / 20% export

energy €30bn sales

imports 150 MT oil/ gas / 30% EU

emissions 224 MT CO2e/yr

GDP € 2500 (#5) 543 bn (#19)

chemicals €46bn / 8% of NRW GDP

€145bn sales / 20% export

energy €33bn of GDP

chemical €109bn exports / €87bn imports (12%)

emissions 827 MT CO2e/yrjobs/ha (red-high)

Rhine corridor

CO2/ha/yr

2020 2030

2nd gen. advanced biofuels (hydro carbon-like)

Synthetic biology: novel pathways, robustness,

rate and yield

1st gen. EtOHfrom sugar cane

2010

photosynthetic micro organisms

to excrete solar biofuels

Low cost photo bioreactor technology

C5 & C6 cofermentation ; biomassN –recycle HTE, -array bioreactors

Genomics & (Directed) evolution

CO2 + solar light

based (3rd gen) biofuels

Low-cost lignocellulosic pretreatmenttechnology for efficient fail-proof intermediate:

low cost sugar (C5/6) platform

1st gen. advanced liquid biofuels

(hydro carbon-like)

2nd gen lignocellulosic EtOHpilot and demonstration plants

2nd gen lignocellulosic EtOHcommercial plants

System

Process Engineering

Develop

Basic Hardware

Enabling Technology

Basic Science

deploy

discovery

discovery

demonstrate

Solution

(piloting)

Low-cost lignocellulosic, thermostable enzymes

Abengoa Bioenergy: “1.3 million gallon/year

capacity demo plant”.’09

“the advances made by Joule Unlimited to achieve direct,

continuous conversion of solar energy to renewable diesel at 15,000

gallons/acre/year ”2010

“Shell and Cosan Form $12bn Ethanol Joint Venture

Raizen 21/11/2011

Amyris: “is scheduled to be in full production of Amyris

renewable products by Q2 2012.

DSM-TUD-B-Basic: “all you can eat

yeast”.2011

Genencor / Novozymes / DSM:

“commercial hydrolytic

Sime Darby-Mitsui: “convert oil palm empty fruit bunches, or EFB, into bioethanol”.2010

GranBio 147 M$ = 464 mRM (160 ktpasugars > 82 mio m3 ethanol)

ChemTex + Novozymes + DSM

DuPont 235 M$ = 744 mRM (200 ktpa hydrolysate sugars > 100 mio m3 ethanol)

POET/DSM 250 M$ = 790 mRM (300 biomass > 160 ktpa sugars > 100 mio m3 ethanol)

Roadmap for tech innovations in the Chemical and Energy sectors : Energy | liquid biofuels

added € /ton biomass (eq)*

chemicals

materials

feed/food

fuels

power

heat

fertiliser

services

100 - 250

100 - 250

50 -100

100 - 250

250 - 1000

50 -100

5 - 20

??

S&T for higher added value portfolio

cellulosics

lignin

protein

nutrients

X

ton biomass*

*eq: domestic, imports, derivatives (estim, McK)

10X larger volume

contents

1. Why ? global & regional drivers

2. How ? BBE technology portfolio

A drop-in, B drop-out, C drop in & out

3. What ? feedstocks, products, yields

4. How – again ?

5. Why – again ?

3

nutrients

2e generation

agro-emissions(run-offs, N2O)

biobricks

bioplastics

1e generationbiofuels

“CO2”

BBE : full economic bio-mass-utilisation Synthetic Biology in the real world?

glucose

xylose

arabinose

acetate

glycerol

furanics

commercial product based patent portfolio

A

Oberhausen

Köln

Rotterdam

Terneuzen

Geleen

Marl

Ludwigshafen

Feluy

Jemeppe

Frankfurt

Antwerpen

Tessenderlo

ARG Connections tons

Connected Ethylene Supply

Connected Ethylene Derivatives

11m

18m

ARG Pipeline

Connected pipelinesbio-ethylene products

Large scale ethanol-to-ethylene conversion is feasible in R’dam.tomorrow.

sustainable ethanol can green EU plastics industry fast “Drop-in Greenification” of Chemical Industry

BIOMASS

protein / sugar / lignocellulose

Iso-butanol ethanol methane SNG

Iso-butylene Ethylene

Gasification

B substitute A drop-in

FermentationAerobic

An-aerobic

othersuccinic acid

acetic-acid

Lactic acid

Funct. molecules

Preservatives, plastics

synthet. polymers

glue

plastics, thickeners

Paraxylene

PET-bottles

Propylene

fertilizer methanol

=80% chemical industry

Plastics, surfactants, detergents

Plastics, carpet

Biorefinery

Reforming

Fermentation and other processes

glycerol

From: Ton Runneboom Bio Based Chemicals March 22 2011, Rotterdam

Biopower

BioPVC

BioHydrocarbons

The other 70% : FDCA for “BioPEF”

biomass

HM-furOH

• Top-12 value-added chemicals from biomass

• Platform chemical - market size 4-12 bn $/yr

• Replace terephthalate in 15 mio ton polymers

• Concept in B-Basic (TUD/TNO - ’09) – FDCA direct production from lignocellulosic HMF

• indust biocat (BIRD Eng /TUD-’09) – bioprocess (BIRD –’10) – invest round - piloting (BE-Basic-’11)

• 2013 - acquisition of BIRD Eng / FDCA by Purac kg-scale process

B

trends in biobased production

production [kT/yr]

concentration from reactor [kg/m3]

0,01

0,1

1

10

100

1000

10000

0,001 0,1 10 1000 100000

petrochemicals

bio-bulk

active ingredients

biopharma

Cooney, ‘84

0,01 1 10 100 1000

MAb, HSA

antibiotics, nutraceuticals

bioplastics(PLA, PHA, PDO, ...)

(2nd gen) biofuels

cost

pric

e ($

/lb)

Bioconstruction materials (self-healing, cement, bioconcrete,biogrout,

bioasphalt,, …)

C

4

In-situ concrete by carbonate fixation

Biogrout & bioconcrete: from soft soil to rock solidC

100 micrometer (10-4 m)

Van Paassen Animations ©

contents

1. Why ? global & regional drivers

2. How ? BBE technology portfolio

3. What ? feedstocks, products, yields

a. yield, b. scale, c. intermediates/structure (in practise)

4. How – again ?

5. Why – again ?

Fermentable sugars

Xylose

Plantation image from: biofuel.webgarden.com

Glucose

drop-outs ?

mass yield matters: products are sold per tonne

C H

O

substitutes

fuels (energy dense) &polymers (PE,PP, PS, PVC)

natural gas

crude oil

biomass CH2O0.5

ethanol

sugars, lactic

CO2

drop-ins

mass composition biobased and fossil feedstocks and products

energy density increases

global production (MT/year) fuels 2000 (jet 300)cement 3000 (600 MT CO2)food 4000 (50% waste)glass 120plastics 280 (big 5: 200) steel 120 (200 MT CO2)

Biorefinery structure - biomass to integral value

• tune portfolio value renewable energy/fuels/chemicals

• counter-acting scale effects of logistics (5-10% for bagasse,

30% for palm oil biomass) and conversion costs

• energy/heat, water, and nutrient integration

• need for cross-industry sector collab’s (JVs, trade, co-op’s,…)

conversion to fuels fuel

conversion to chemicals

conversion to power/heat

pretreatment / hydrolysis

harvest / logistics

chemicals/materials

renewablepower/heat

nutrients/water

‘switch’

food/feed

5

(I) Bioenergy Only: sugars to ethanol (100%) , power (heat)

(II) Chem’s : sugars to organic acids (25%) + ethanol (75%), lignin to power (+ less excess heat), CO2

(III) Chem’s & Materials : sugars to organic acids (25%) + ethanol (75%), lignin to power (+ less excess heat), CO2 to bioconstruction

150

900 910

1743

3 tons of raw biomass at gate(2/3 cellulosics + 1/3 lignin)

biomass biorefined to sugars and lignin

revenue in US$

CO2

heat

1743CO2 in mat’s

(II) (III)(I)

power

ethanolsugars

chem’s

biorenewables’ scenarios

pos. and neg. economic value

lignin

26

palmitic acid

glycerolsugars

methane

butanol

propionic acid

ethanol

succinic acid

citric acid

lactic acid

p-xylenecrude oil

syngas

0.25

adipic/acrylic

ethylene

propylene

jetfuel/diesel

1,4 BDO

0.5

1.0

0.3

1.1

0.4

0.3

CO2

biomass

ligninemethanol

Hcomb

105 J/kg

600

0

biomass yield

Cost contribution of feedstocks

$400/ton

$50..130*/ton

$660/ton

$6/ton

$1600/ton

$1200/ton

$400/ton

$800/ton

$402/ton

feedstocks products

Only established market: APEX ENDEX Woodpellets ~ $130*/ton

27

palmitic acid

glycerolsugars

methane

butanol

propionic acid

ethanol

succinic acid

citric acid

lactic acid

p-xylenecrude oil

syngas

0.25

adipic/acrylic

ethylene

propylene

jetfuel/diesel

1,4 BDO

0.5

1.0

0.3

1.1

0.4

0.3

CO2

biomass

ligninemethanol

feedstocks

Hcomb

105 J/kg

600

0

biomass yield

Combined (drop-in/substitute/-out) scenarios ?products

$400/ton

$50..130/ton

$660/ton

$6/ton biocon-struction

advanced fuels

connect 2 sectors w mega-volumes

Winning Team

2013 LST MSc

Design Competition

woodpellets + … power/heat + ethanol + biochemical + €€ (instead of –SDE)

Hcomb

105 J/kg

platforms

Which platforms (redox/mass balance) ?

feedstocks products

29

ethanol

butanol

lignine

succinic(p)ethylcarb.

ureawoodpellets

formic

crude oils

hydrogen, electricity

ammonia

ethanol

butanol

lignine

sugarssyngas

CO2

jet fuelaromatics

CO2/biochem

1,2

4,5

1,2,3 4,5

(4)

3

Result: 5 fairly different designs

6

BIRD Chains (BIoRenewable jet & Diesel supply Chains) is series of PDEng feasibility projects in Brazil and ASEAN with AirFrance/KLM, TUD, DAB, and regional partners in Brazil & Malaysia, prep. for HIP.

Supply chain projects

sugars

lignocellulose bioplastic

biofuelbiorefinery

sugars

lignocellulose biofuel

bioplasticbiorefinery

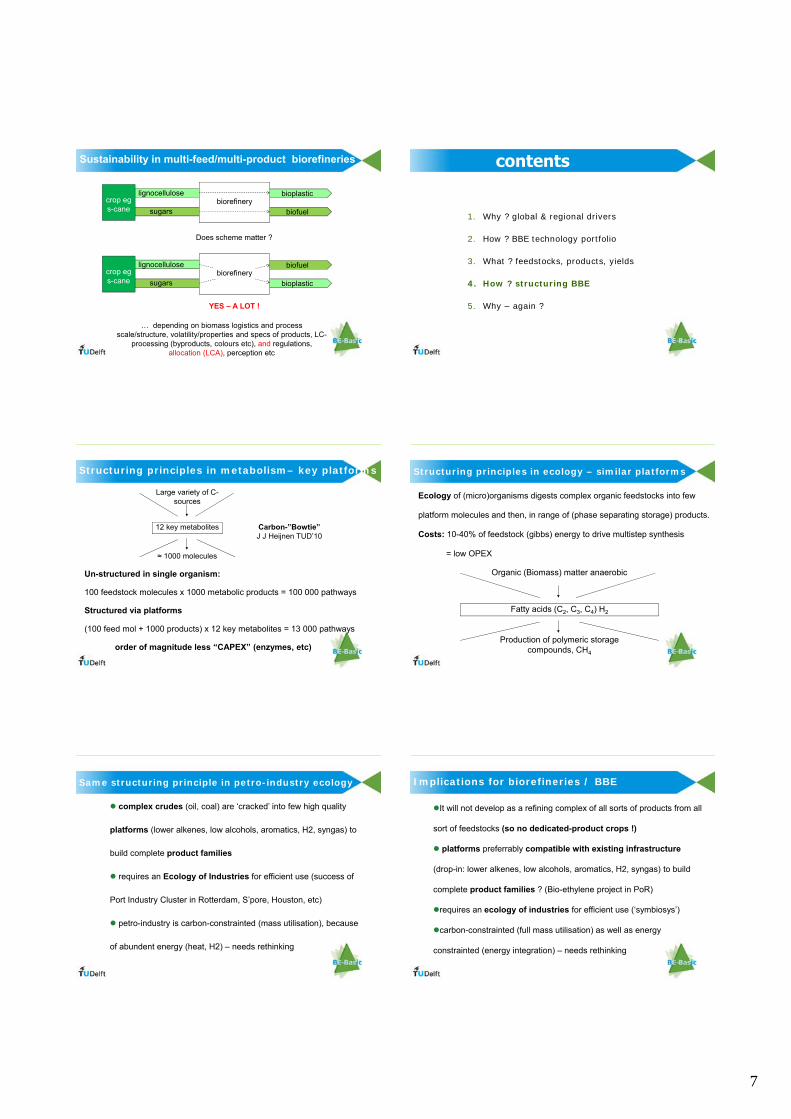

Sustainability in multi-feed/multi-product biorefineries

Does scheme matter ?

YES – A LOT !

… depending on biomass logistics and process scale/structure, volatility/properties and specs of products, LC-

processing (byproducts, colours etc), and regulations, allocation (LCA), perception etc

crop egs-cane

crop egs-cane

ASEAN - Scenarios mill-integrated biomass processing

mill basedplantation +

mill based

1 central biomass

processing plant

A1

(n=1)

A2

A5

n regular mills

per

B1

B2

B5

(n=5)

$ 400/ton

0

200

400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Number of mills per conversion plant

USD

/tonne Ferm

entatble sugar

General Expenses

Overhead

Capital charge

Labour and other DPC

Logistics

Raw materials

Mill-integrated lignocellulosics ?

BRAZILIAN 1465 (U$ 460)

NY #11 1685 (U$ 530) LTC M’sia 1770 (U$ 557)

margin (excluding energy credits)

$ 400/ton

LTC US$ 557

NY No. 12 US$ 530

Brazilian US$ 460

Distributed biomass processes are often favorable

Example: conversion of lignocellulosic palm biomass to sugarsM del Mar Palmeros et al (2013)

full plant designs

approximate method

include (process) learning effects:

logistical costs dominate

NPV / DCCF / PBT for 3* and 10 PO mill clusters

* productivity of 3 mill cluster is scaled (x 3.3) to that of 10 mill clusterM del Mar Palmeros et al (2013); final report of MICCI project

3 mills cluster has

higher CAPEX

3 mills cluster has lower

OPEX yet the effect is

discounted by time

* with learning effects like in SC

EtOH (Goldemberg), single-PO-

mill-integration appears feasible:

every mill produces PO & sugars

7

sugars

lignocellulose bioplastic

biofuelbiorefinery

sugars

lignocellulose biofuel

bioplasticbiorefinery

Sustainability in multi-feed/multi-product biorefineries

Does scheme matter ?

YES – A LOT !

… depending on biomass logistics and process scale/structure, volatility/properties and specs of products, LC-

processing (byproducts, colours etc), and regulations, allocation (LCA), perception etc

crop egs-cane

crop egs-cane

contents

1. Why ? global & regional drivers

2. How ? BBE technology portfolio

3. What ? feedstocks, products, yields

4. How ? structuring BBE

5. Why – again ?

Structuring principles in metabolism– key platforms

Large variety of C-sources

12 key metabolites Carbon-”Bowtie”J J Heijnen TUD’10

≈ 1000 molecules

Un-structured in single organism:

100 feedstock molecules x 1000 metabolic products = 100 000 pathways

Structured via platforms

(100 feed mol + 1000 products) x 12 key metabolites = 13 000 pathways

order of magnitude less “CAPEX” (enzymes, etc)

Organic (Biomass) matter anaerobic

Fatty acids (C2, C3, C4) H2

Production of polymeric storage compounds, CH4

Structuring principles in ecology – similar platforms

Ecology of (micro)organisms digests complex organic feedstocks into few

platform molecules and then, in range of (phase separating storage) products.

Costs: 10-40% of feedstock (gibbs) energy to drive multistep synthesis

= low OPEX

Same structuring principle in petro-industry ecology

complex crudes (oil, coal) are ‘cracked’ into few high quality

platforms (lower alkenes, low alcohols, aromatics, H2, syngas) to

build complete product families

requires an Ecology of Industries for efficient use (success of

Port Industry Cluster in Rotterdam, S’pore, Houston, etc)

petro-industry is carbon-constrainted (mass utilisation), because

of abundent energy (heat, H2) – needs rethinking

Implications for biorefineries / BBE

It will not develop as a refining complex of all sorts of products from all

sort of feedstocks (so no dedicated-product crops !)

platforms preferrably compatible with existing infrastructure

(drop-in: lower alkenes, low alcohols, aromatics, H2, syngas) to build

complete product families ? (Bio-ethylene project in PoR)

requires an ecology of industries for efficient use (‘symbiosys’)

carbon-constrainted (full mass utilisation) as well as energy

constrainted (energy integration) – needs rethinking

8

contents

1. Why ? global & regional drivers

2. How ? BBE technology portfolio

3. What ? feedstocks, products, yields

4. How ? structuring BBE

5. Why – again ?

Global drivers for a BBE ?

• more people with more wealth

• less nett GHG emission (global warming)

and/or climate adaptation

• politics (security of oil/gas supply)

• innovation, rural income and economic development

• increasing (and decreasing) prices of resources

• in time*, limited fossil reserves

• add sustainability to food chain

• add value to food chain and prevent hunger

Pick your personal selection !

Chemical clusters – drop-in ?

S’pore

Shanghai

R’dam

Ruhr

Houston

Paulinia

Rest of the World – substitute or drop-out scenario’s ?

Max the BBE opportunities !• (A) drop-in, (B) substitute and (C) drop-out can all be

realities and require:

• further integration of industrial sectors – fuel & construction,

fuel & agro, waste & feed, … to enable full (bio)mass utilisation

(mass, energy, economy, climate)

• regional diversification to benefit fully from brown field (EU,

USA) and green field (LA, Africa, Asia) situations

• rethink scale & regulations – hi-tech distributed

manufacturing, process technology, infrastructure, agri-models,

finance models, regulations (especially around recycling), ...

B(E)-Basic Foundation

T +31 15 – 2782363

W www.be-basic.org

or

Contact us

Back-up slides

• BE-Basic – what’s that ?