Embed Size (px)

Citation preview

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.1

6. Vektorautoregressive Modelle

In bisherigen Modellen Festlegung von exogenen Variablen notwendig.

Streng genommen gibt es keine vollständig exogenen Variablen.

Beispiel: Selbst die „exogene“ Anhebung des Leit-zinssatzes war durch andere wirtschaftliche Einflussfaktoren notwendig geworden

In VARs sind alle Variablen potentiell endogen.

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.2

6.1 VAR-Modelle ohne Restriktionen

Wiederholung: Zeitreihenanalyse u. Ökonometrie I

AR(p)-Prozess:

yt = (ß +) f 1 yt-1 + f 2 yt-2 + ... +f p yt-p + ut

wobei ut ein reiner Zufallsprozess, ein white noise, ist mit

,const ,0)E( 2 == utu σ

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.3

Voraussetzung: yt (schwach) stationärer stochastischer Prozess

D.h. zeitkonstante(r) Erwartungswert und Autokovarianzfunktion ?(t ):

[ ] )()()(E

)E(

τγµµ

µ

τ =−⋅−

=

−tt

t

yy

y

Varianz ebenfalls zeitkonstant und endlich. Warum?

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.4

Nachweis durch die Charakteristische Gleichung:

01 221 =−−−− p

pz...zz ϕϕϕ

Hinreichende und notwendige Bedingung für Stationarität:

Komplexzahlige Lösungen liegen außerhalb des Einheitskreises, d.h. |z|>1.

Wenn Lösung |z|=1 ist, liegt eine Einheitswurzel (unit root) vor, der Prozess ist nichtstationär

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.5

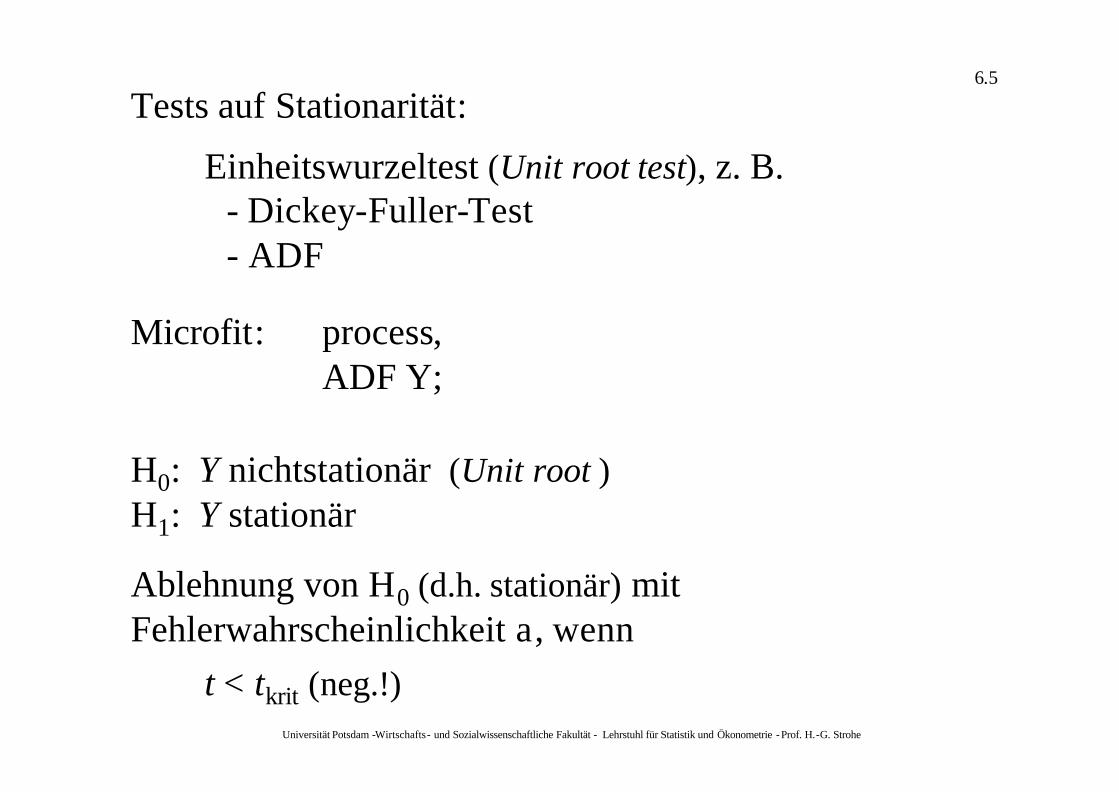

Tests auf Stationarität:

Einheitswurzeltest (Unit root test), z. B.- Dickey-Fuller-Test- ADF

Microfit: process, ADF Y;

H0: Y nichtstationär (Unit root )H1: Y stationär

Ablehnung von H0 (d.h. stationär) mit Fehlerwahrscheinlichkeit a, wenn

t < tkrit (neg.!)

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.6

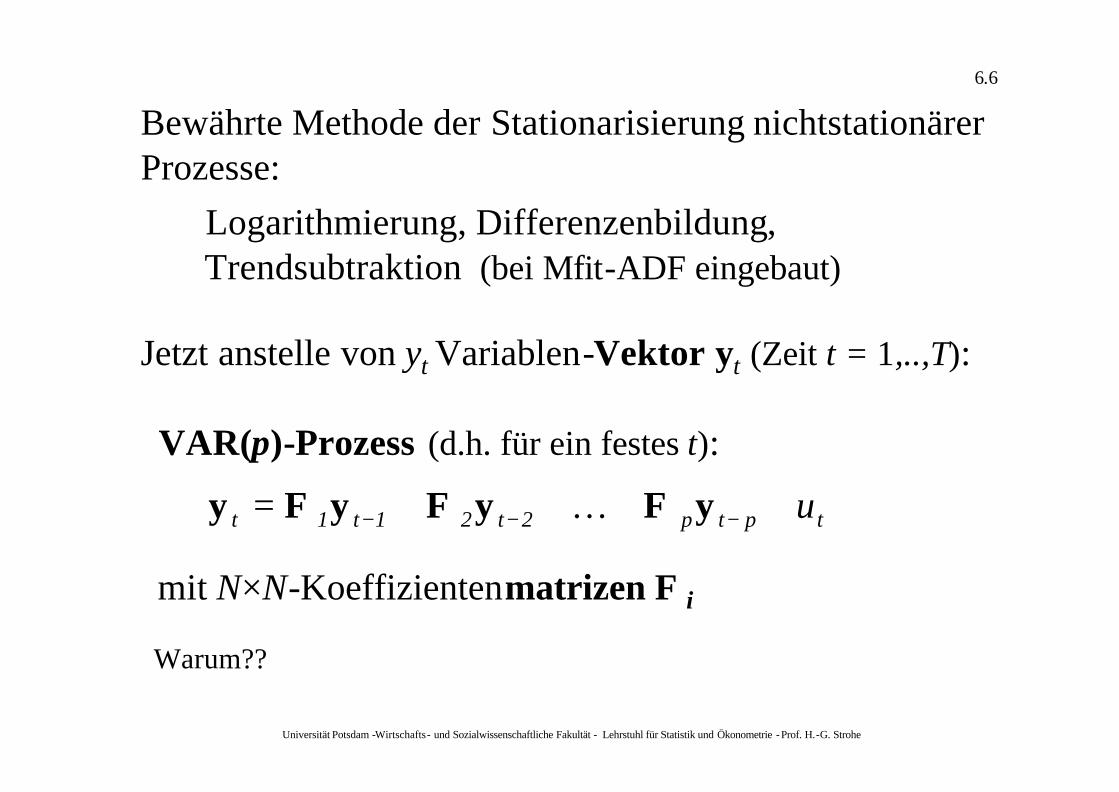

Bewährte Methode der Stationarisierung nichtstationärer Prozesse:

Logarithmierung, Differenzenbildung, Trendsubtraktion (bei Mfit-ADF eingebaut)

Jetzt anstelle von yt Variablen-Vektor yt (Zeit t = 1,..,T):

VAR(p)-Prozess (d.h. für ein festes t):

tptp2t21t1t u++++= −−− yyyy ΦΦΦ K

mit N×N-Koeffizientenmatrizen F i

Warum??

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.7

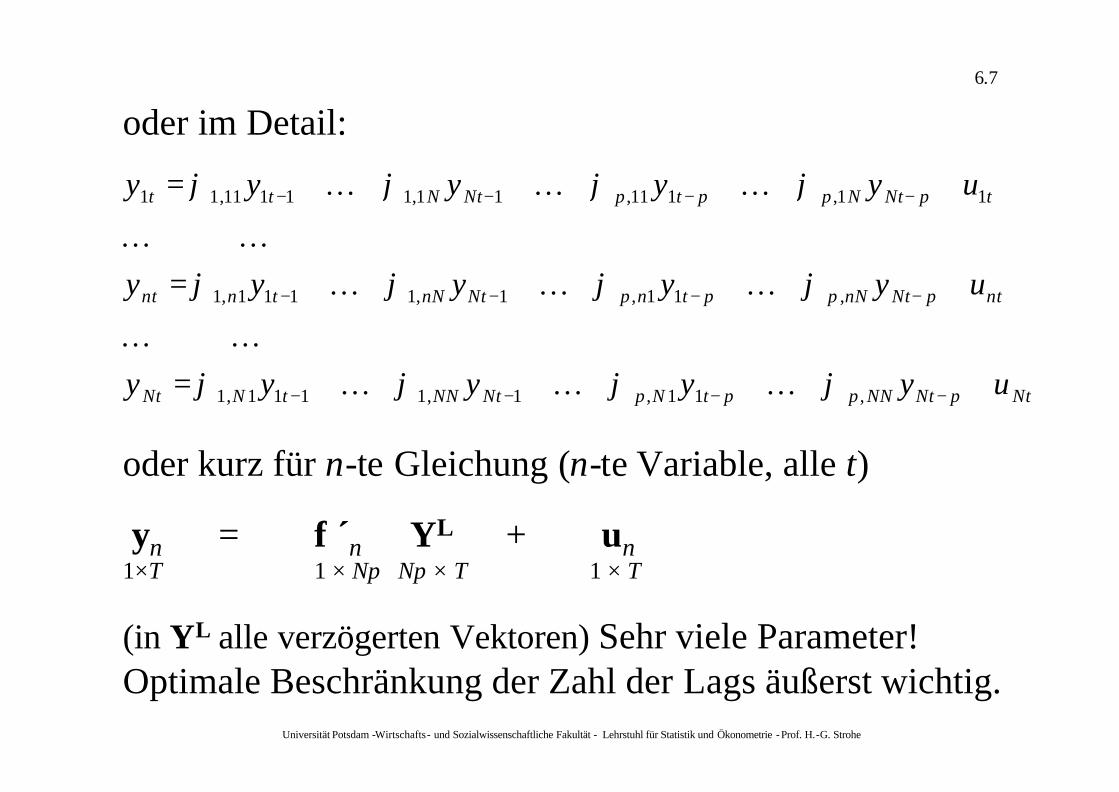

NtpNtNNpptNpNtNNtNNt

ntpNtnNpptnpNtnNtnnt

tpNtNpptpNtNtt

uyyyyy

uyyyyy

uyyyyy

+++++++=

+++++++=

+++++++=

−−−−

−−−−

−−−−

,11,1,1111,1

,11,1,1111,1

11,111,11,11111,11

ϕϕϕϕ

ϕϕϕϕ

ϕϕϕϕ

KKKKK

KKKKK

KKK

oder kurz für n-te Gleichung (n-te Variable, alle t)

yn = f ´n YL + un1×T 1 × Np Np × T 1 × T

(in YL alle verzögerten Vektoren) Sehr viele Parameter! Optimale Beschränkung der Zahl der Lags äußerst wichtig.

oder im Detail:

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.8

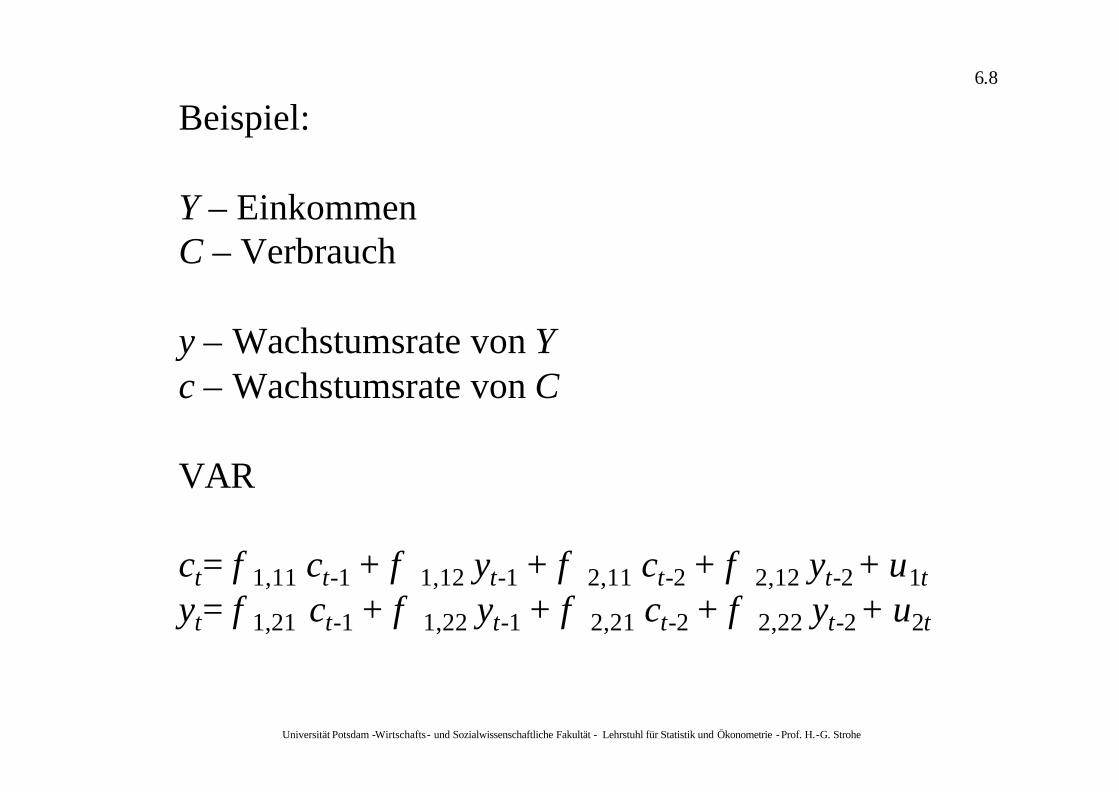

Beispiel:

Y – EinkommenC – Verbrauch

y – Wachstumsrate von Yc – Wachstumsrate von C

VAR

ct= f 1,11 ct-1 + f 1,12 yt-1 + f 2,11 ct-2 + f 2,12 yt-2 + u1tyt= f 1,21 ct-1 + f 1,22 yt-1 + f 2,21 ct-2 + f 2,22 yt-2 + u2t

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.9

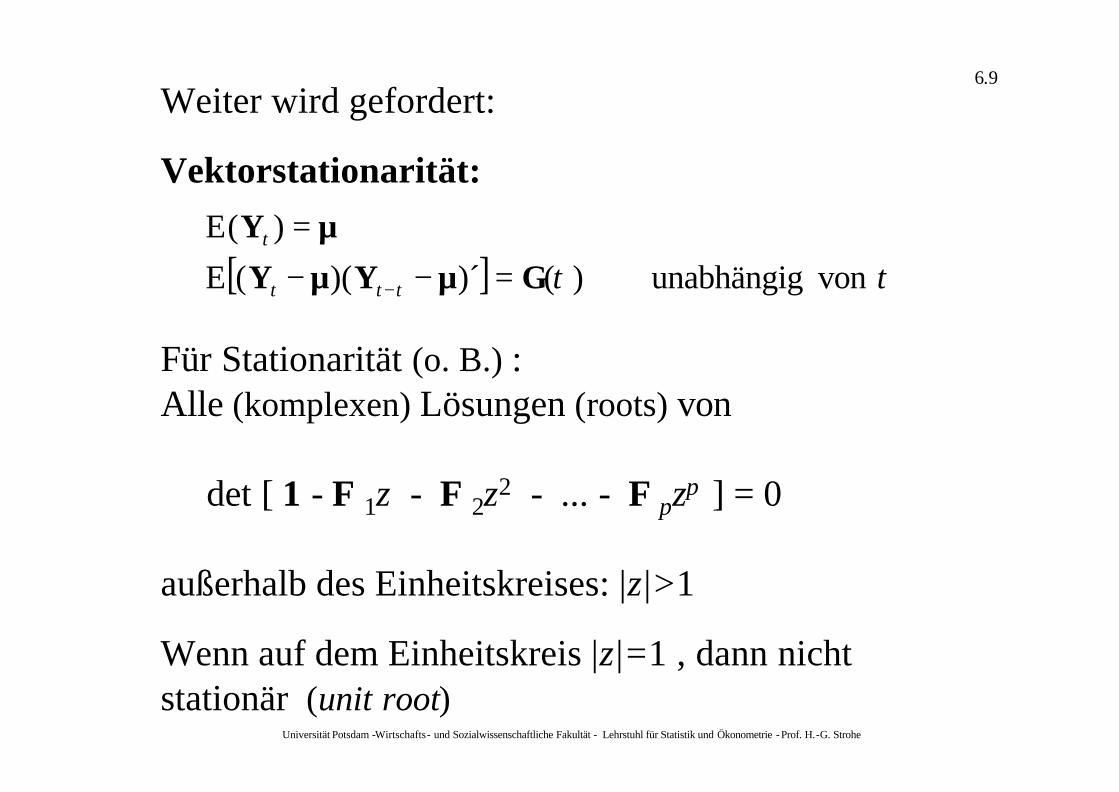

Weiter wird gefordert:

Vektorstationarität:

[ ] tttt

t

von unabhängig)()´)((E

)(E

τGµYµY

µY

=−−=

−

Für Stationarität (o. B.) :Alle (komplexen) Lösungen (roots) von

det [ 1 - F 1z - F 2z2 - ... - F pzp ] = 0

außerhalb des Einheitskreises: |z|>1

Wenn auf dem Einheitskreis |z|=1 , dann nicht stationär (unit root)

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

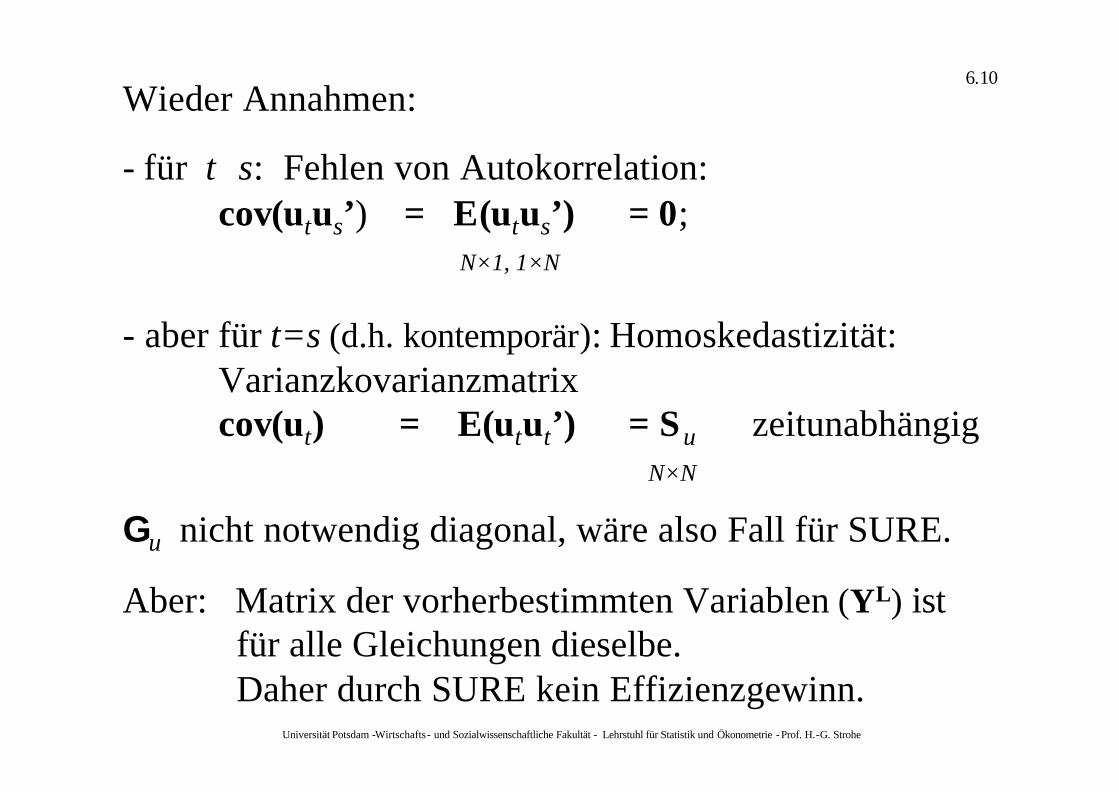

6.10Wieder Annahmen:

- für tÖs: Fehlen von Autokorrelation:cov(utus’) = E(utus’) = 0;

N×1, 1×N

- aber für t=s (d.h. kontemporär): Homoskedastizität: Varianzkovarianzmatrixcov(ut) = E(utut’) = Su zeitunabhängig

N×N

Gu nicht notwendig diagonal, wäre also Fall für SURE.

Aber: Matrix der vorherbestimmten Variablen (YL) ist für alle Gleichungen dieselbe. Daher durch SURE kein Effizienzgewinn.

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.11

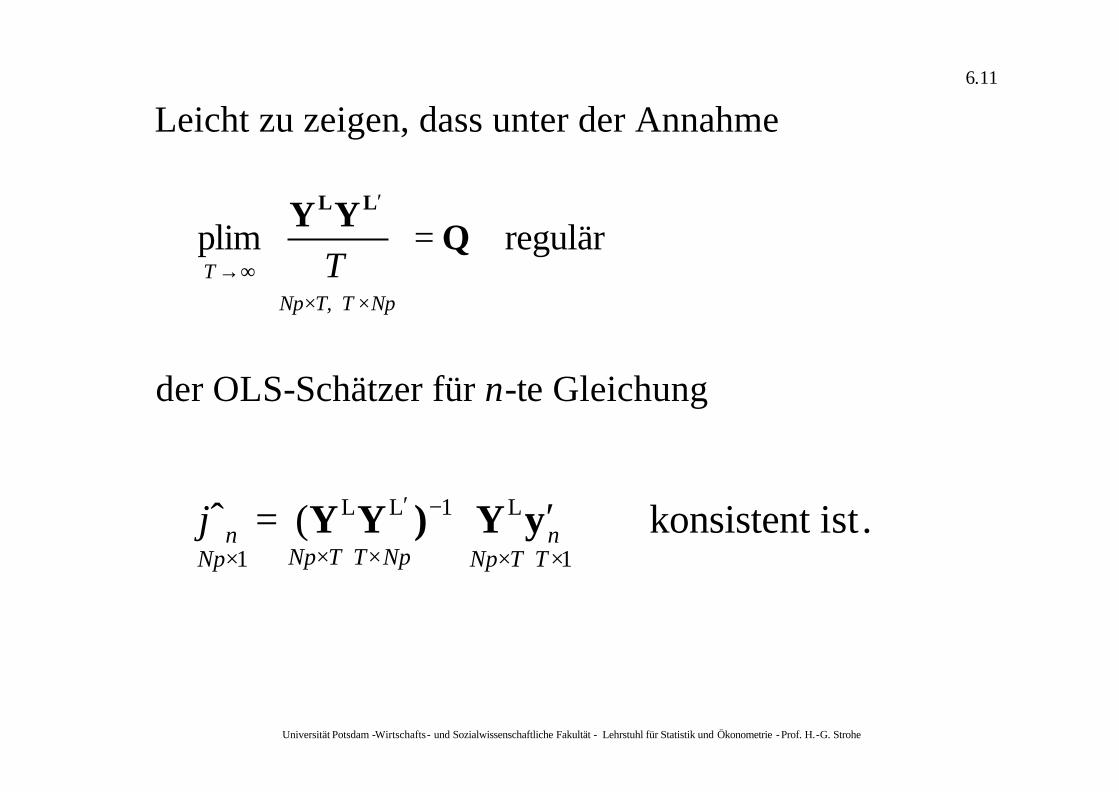

Leicht zu zeigen, dass unter der Annahme

regulärplim QYY LL

=

××

′

∞→NpT, TNp

T T

der OLS-Schätzer für n-te Gleichung

.ist konsistent(ˆ1

L

1LL

1 ××××

−′

×′=

T TNpn

NpT TNpNpn yY)YYϕ

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.12

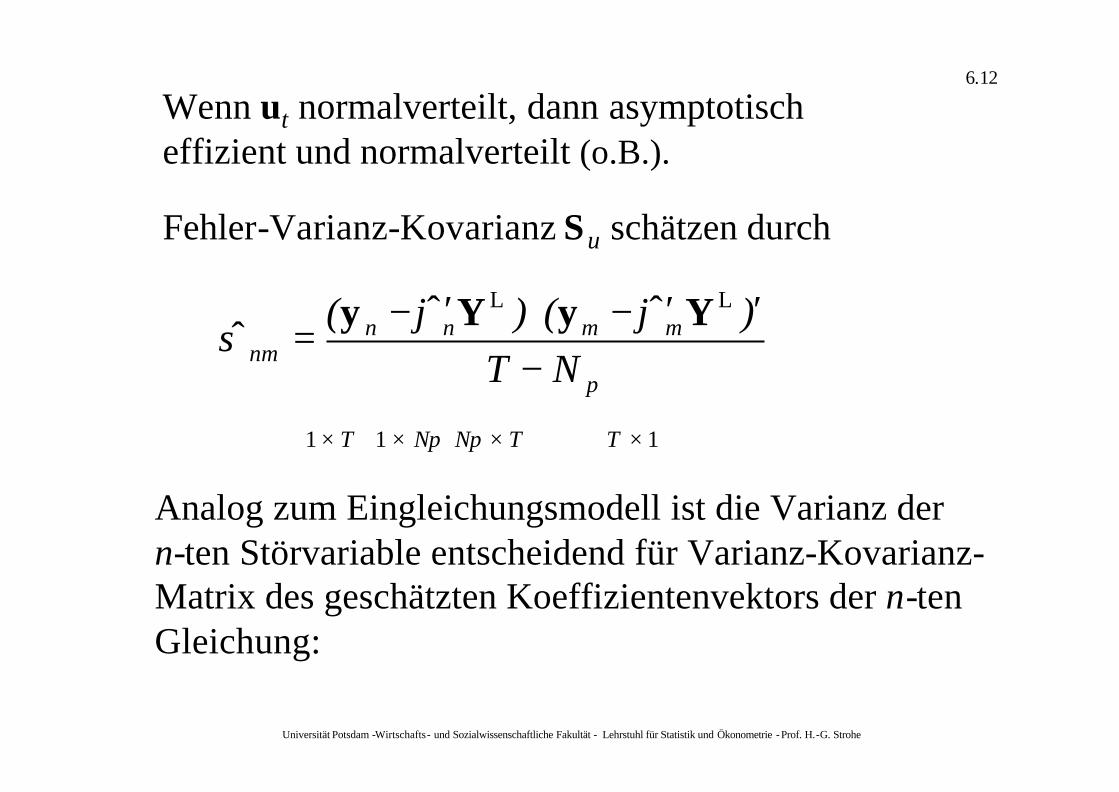

Wenn ut normalverteilt, dann asymptotisch effizient und normalverteilt (o.B.).

Fehler-Varianz-Kovarianz Su schätzen durch

1 1 1

LL

ˆˆˆ

××××

−′′−⋅′−

=

TT NpNpT

p

mmnnnm NT

)()( YyYy ϕϕσ

Analog zum Eingleichungsmodell ist die Varianz der n-ten Störvariable entscheidend für Varianz-Kovarianz-Matrix des geschätzten Koeffizientenvektors der n-ten Gleichung:

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

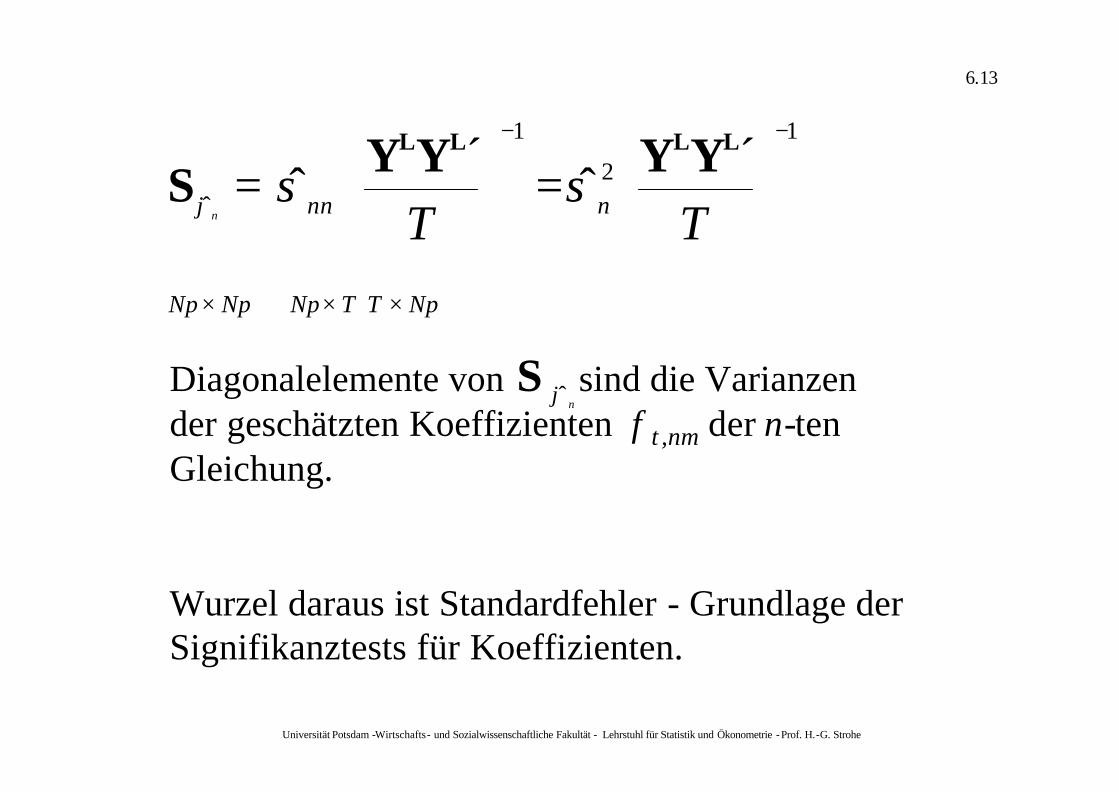

6.13

NpTT NpNp Np

nnn TTn

×××

−−

=

=

1

2

1

ˆ

´ˆ

´ˆ

LLLL YYYYS σσϕ

Diagonalelemente von sind die Varianzender geschätzten Koeffizienten f t ,nm der n-ten Gleichung.

Wurzel daraus ist Standardfehler - Grundlage der Signifikanztests für Koeffizienten.

nϕ̂S

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.14

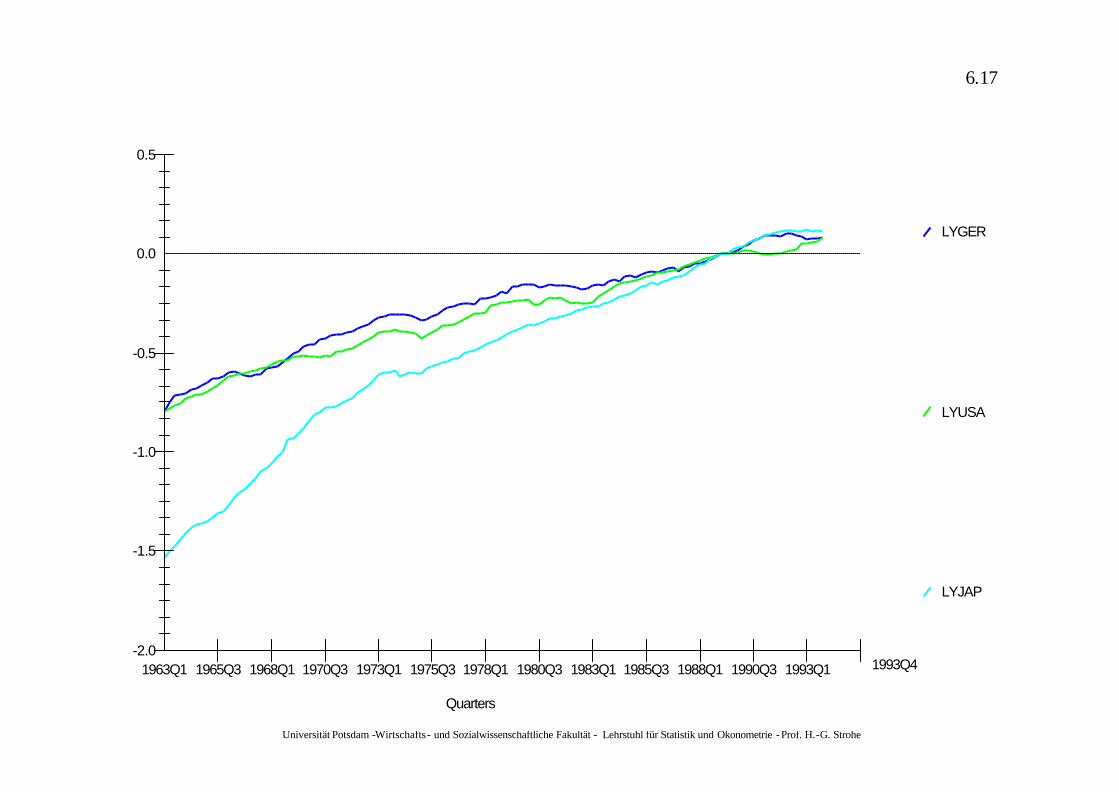

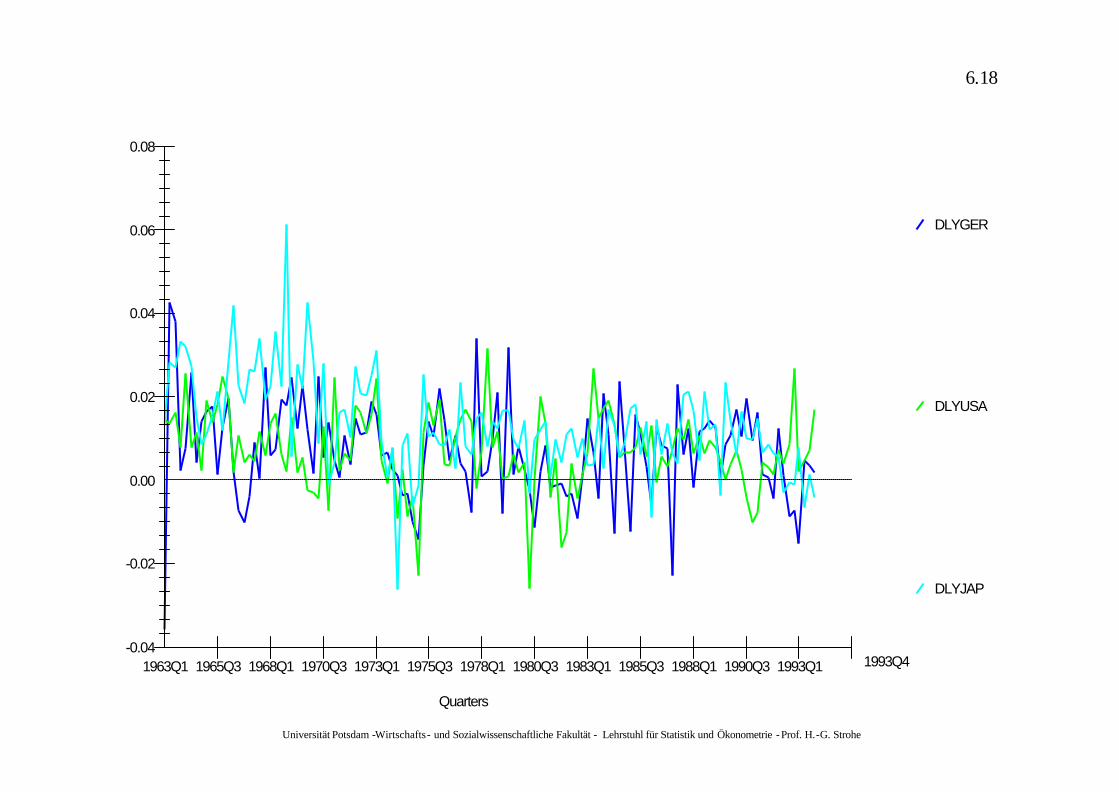

Beispiel:Wachstumsraten des Bruttoinlandsprodukts Deutschlands, der USA und Japans mit Verzögerung.Sei y nichtstationär. Dann ist ln y vielleicht schon stationär (Reduktion großer Varianzen), aber ? ln y mit großer Aussicht stationär (Trendelimination).

Interpretation von ? ln y:

1

1

11 lnlnlnln

−

−

−−

−≈

=−=∆

t

tt

t

tttt

yyy

yy

yyy

Wachstumsrate für relativ kleine ? y

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.15

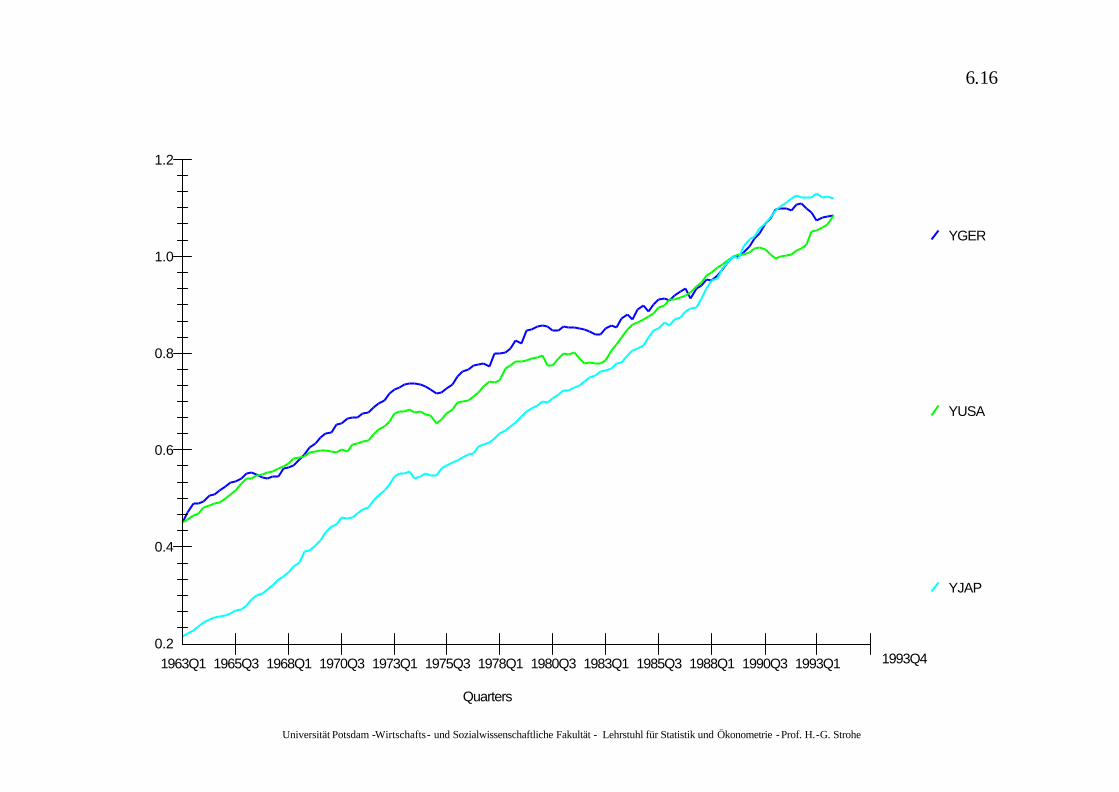

Daher als Wachstumsraten der BIPs jetzt als stationär angenommene Reihen ? ln Yt.

In Mfit: DLY mit Kennz. GER, USA, JAP (aus G7GDP.fit)

Vorgehen: Multivariate; Unrestricted VAR;

Lag-Ordnung (p) eingeben (z.B. 2); Variable eingeben.

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.16

YGER

YUSA

YJAP

Quarters

0.2

0.4

0.6

0.8

1.0

1.2

1963Q1 1965Q3 1968Q1 1970Q3 1973Q1 1975Q3 1978Q1 1980Q3 1983Q1 1985Q3 1988Q1 1990Q3 1993Q1 1993Q4

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.17

LYGER

LYUSA

LYJAP

Quarters

-0.5

-1.0

-1.5

-2.0

0.0

0.5

1963Q1 1965Q3 1968Q1 1970Q3 1973Q1 1975Q3 1978Q1 1980Q3 1983Q1 1985Q3 1988Q1 1990Q3 1993Q1 1993Q4

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.18

DLYGER

DLYUSA

DLYJAP

Quarters

-0.02

-0.04

0.00

0.02

0.04

0.06

0.08

1963Q1 1965Q3 1968Q1 1970Q3 1973Q1 1975Q3 1978Q1 1980Q3 1983Q1 1985Q3 1988Q1 1990Q3 1993Q1 1993Q4

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

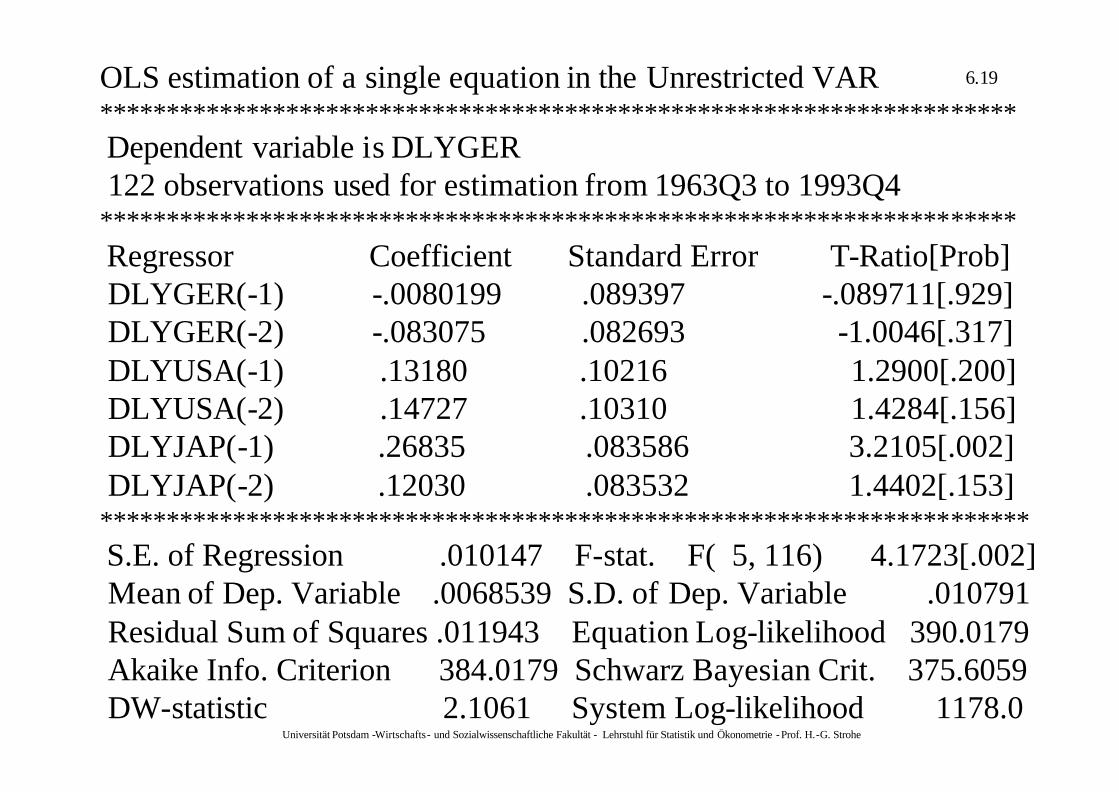

6.19OLS estimation of a single equation in the Unrestricted VAR *********************************************************************Dependent variable is DLYGER 122 observations used for estimation from 1963Q3 to 1993Q4

*********************************************************************Regressor Coefficient Standard Error T-Ratio[Prob]DLYGER(-1) -.0080199 .089397 -.089711[.929]DLYGER(-2) -.083075 .082693 -1.0046[.317]DLYUSA(-1) .13180 .10216 1.2900[.200]DLYUSA(-2) .14727 .10310 1.4284[.156]DLYJAP(-1) .26835 .083586 3.2105[.002]DLYJAP(-2) .12030 .083532 1.4402[.153]

**********************************************************************S.E. of Regression .010147 F-stat. F( 5, 116) 4.1723[.002]Mean of Dep. Variable .0068539 S.D. of Dep. Variable .010791Residual Sum of Squares .011943 Equation Log-likelihood 390.0179Akaike Info. Criterion 384.0179 Schwarz Bayesian Crit. 375.6059DW-statistic 2.1061 System Log-likelihood 1178.0

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

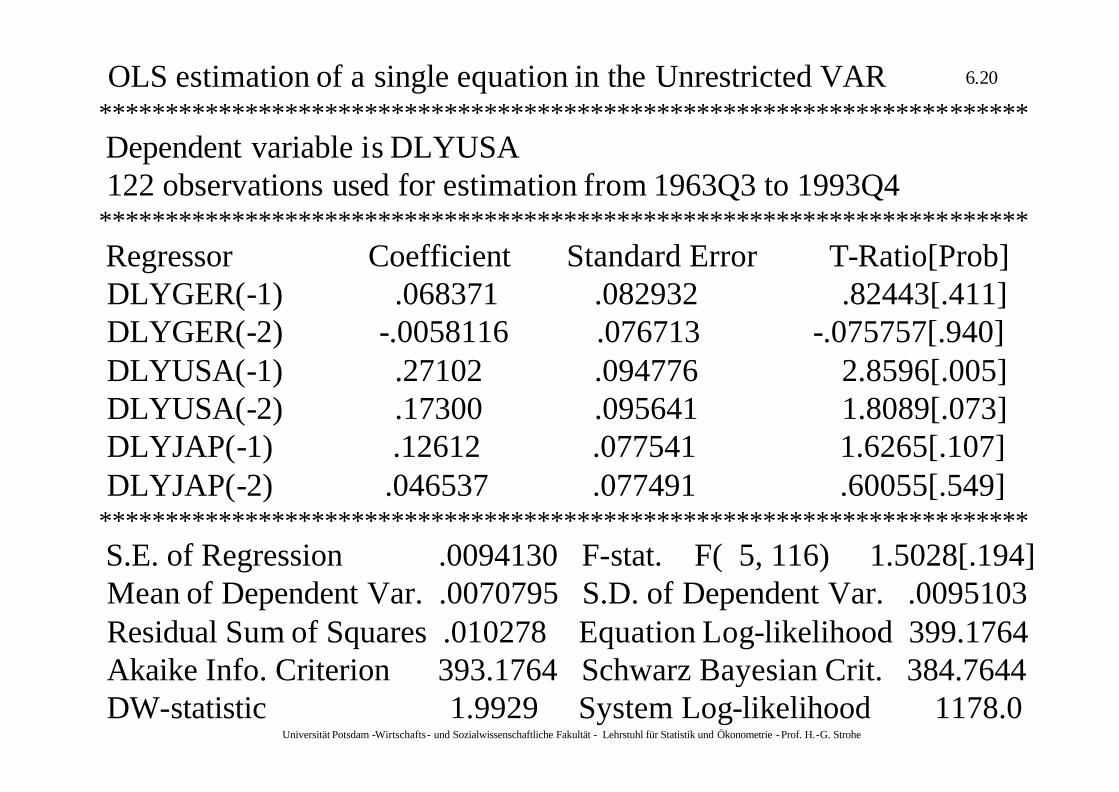

6.20OLS estimation of a single equation in the Unrestricted VAR**********************************************************************Dependent variable is DLYUSA 122 observations used for estimation from 1963Q3 to 1993Q4

**********************************************************************Regressor Coefficient Standard Error T-Ratio[Prob]DLYGER(-1) .068371 .082932 .82443[.411]DLYGER(-2) -.0058116 .076713 -.075757[.940]DLYUSA(-1) .27102 .094776 2.8596[.005]DLYUSA(-2) .17300 .095641 1.8089[.073]DLYJAP(-1) .12612 .077541 1.6265[.107]DLYJAP(-2) .046537 .077491 .60055[.549]

**********************************************************************S.E. of Regression .0094130 F-stat. F( 5, 116) 1.5028[.194]Mean of Dependent Var. .0070795 S.D. of Dependent Var. .0095103Residual Sum of Squares .010278 Equation Log-likelihood 399.1764Akaike Info. Criterion 393.1764 Schwarz Bayesian Crit. 384.7644DW-statistic 1.9929 System Log-likelihood 1178.0

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

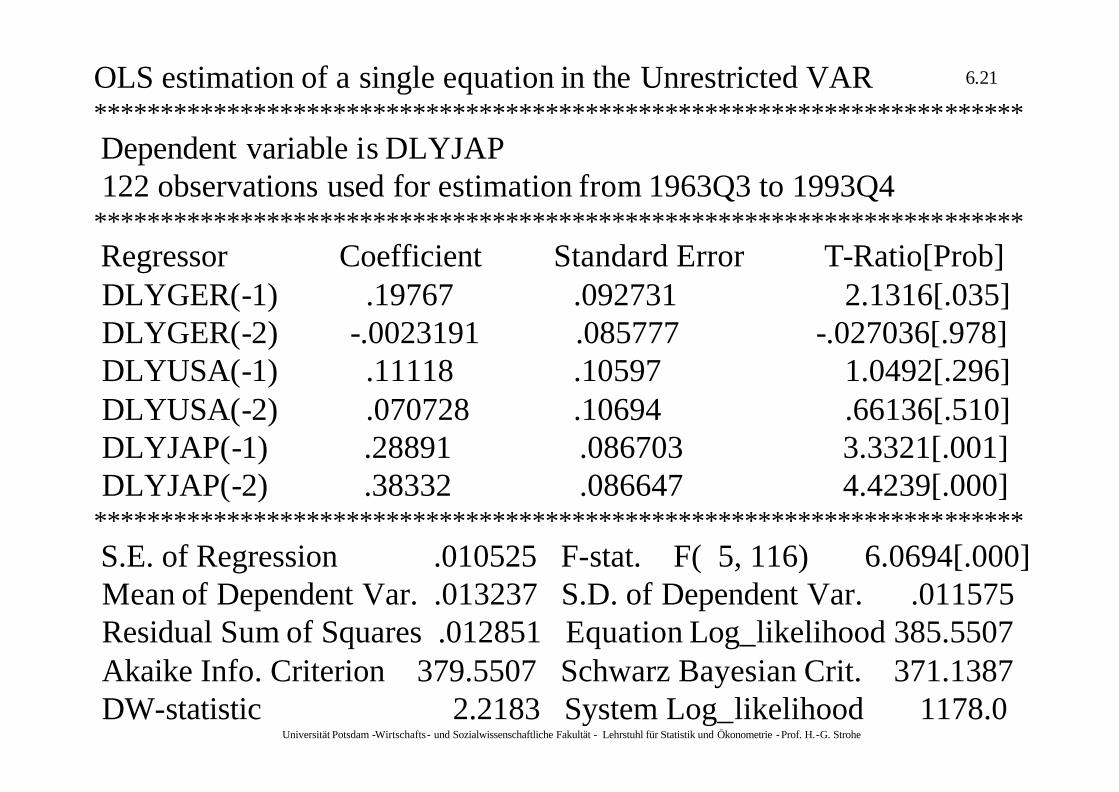

6.21OLS estimation of a single equation in the Unrestricted VAR **********************************************************************Dependent variable is DLYJAP 122 observations used for estimation from 1963Q3 to 1993Q4

**********************************************************************Regressor Coefficient Standard Error T-Ratio[Prob]DLYGER(-1) .19767 .092731 2.1316[.035]DLYGER(-2) -.0023191 .085777 -.027036[.978]DLYUSA(-1) .11118 .10597 1.0492[.296]DLYUSA(-2) .070728 .10694 .66136[.510]DLYJAP(-1) .28891 .086703 3.3321[.001]DLYJAP(-2) .38332 .086647 4.4239[.000]

**********************************************************************S.E. of Regression .010525 F-stat. F( 5, 116) 6.0694[.000]Mean of Dependent Var. .013237 S.D. of Dependent Var. .011575Residual Sum of Squares .012851 Equation Log_likelihood 385.5507Akaike Info. Criterion 379.5507 Schwarz Bayesian Crit. 371.1387DW-statistic 2.2183 System Log_likelihood 1178.0

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.22

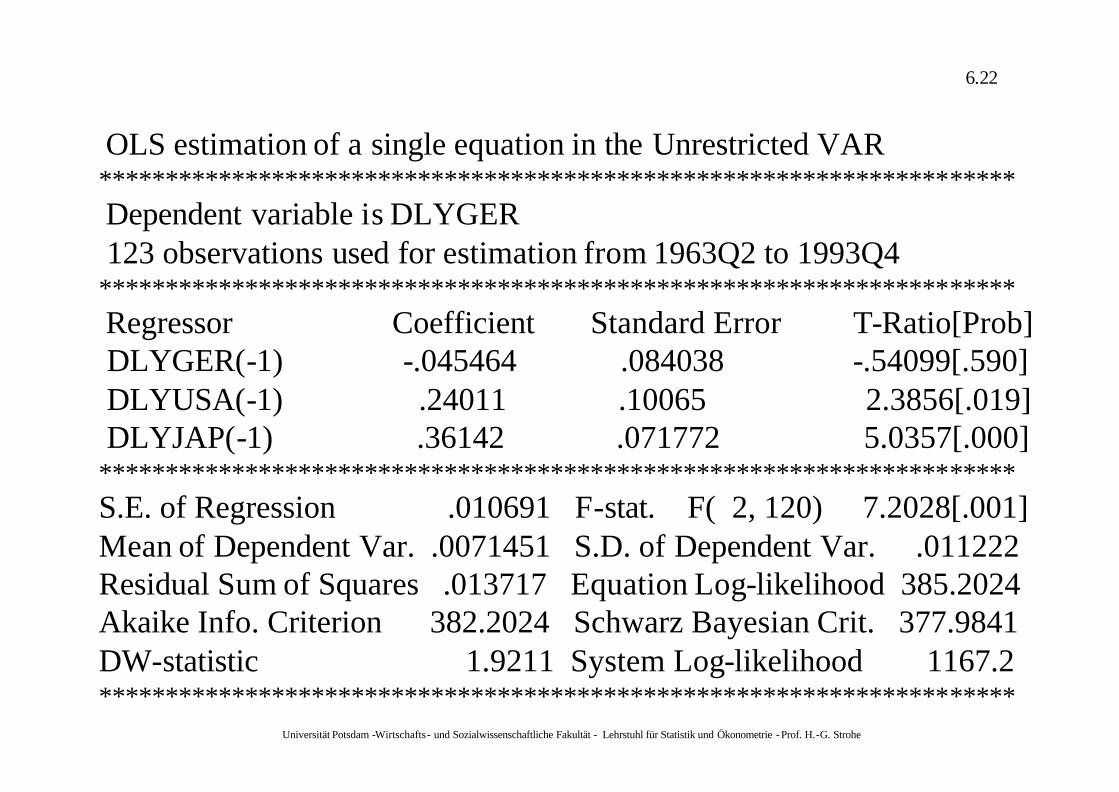

OLS estimation of a single equation in the Unrestricted VAR *********************************************************************Dependent variable is DLYGER 123 observations used for estimation from 1963Q2 to 1993Q4

*********************************************************************Regressor Coefficient Standard Error T-Ratio[Prob]DLYGER(-1) -.045464 .084038 -.54099[.590]DLYUSA(-1) .24011 .10065 2.3856[.019]DLYJAP(-1) .36142 .071772 5.0357[.000]

*********************************************************************S.E. of Regression .010691 F-stat. F( 2, 120) 7.2028[.001]Mean of Dependent Var. .0071451 S.D. of Dependent Var. .011222Residual Sum of Squares .013717 Equation Log-likelihood 385.2024Akaike Info. Criterion 382.2024 Schwarz Bayesian Crit. 377.9841DW-statistic 1.9211 System Log-likelihood 1167.2*********************************************************************

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.23

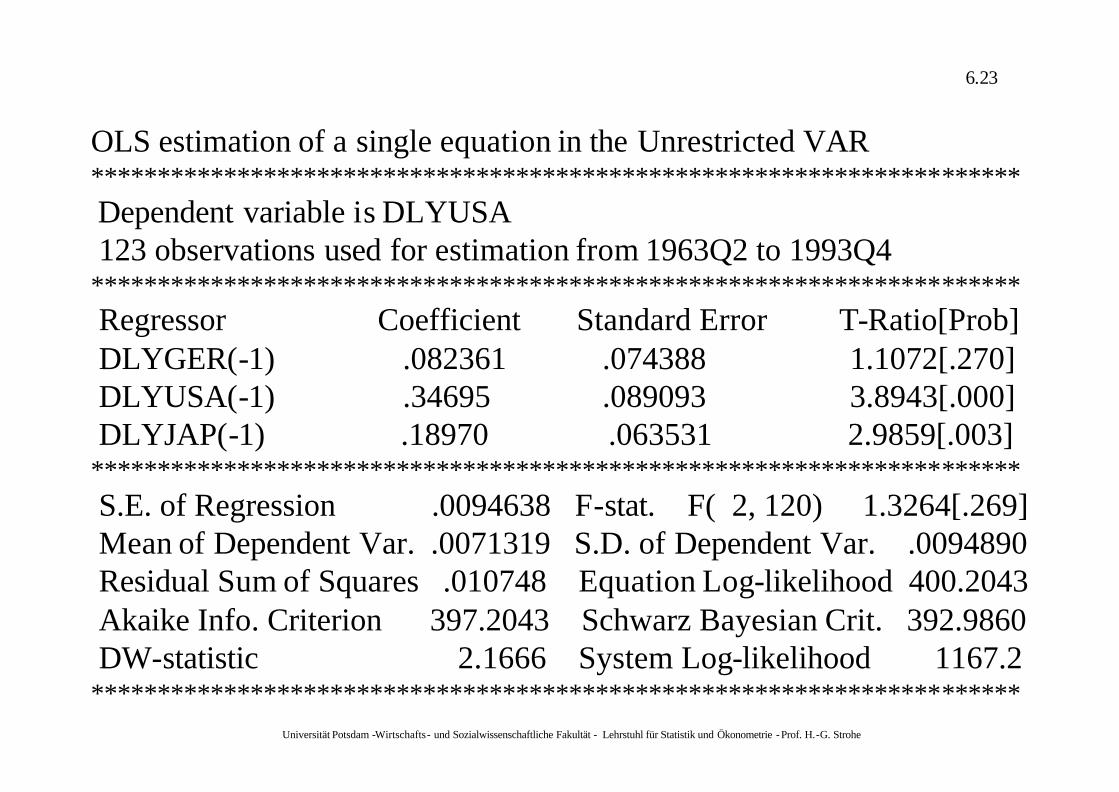

OLS estimation of a single equation in the Unrestricted VAR**********************************************************************Dependent variable is DLYUSA 123 observations used for estimation from 1963Q2 to 1993Q4

**********************************************************************Regressor Coefficient Standard Error T-Ratio[Prob]DLYGER(-1) .082361 .074388 1.1072[.270]DLYUSA(-1) .34695 .089093 3.8943[.000]DLYJAP(-1) .18970 .063531 2.9859[.003]

**********************************************************************S.E. of Regression .0094638 F-stat. F( 2, 120) 1.3264[.269]Mean of Dependent Var. .0071319 S.D. of Dependent Var. .0094890Residual Sum of Squares .010748 Equation Log-likelihood 400.2043Akaike Info. Criterion 397.2043 Schwarz Bayesian Crit. 392.9860DW-statistic 2.1666 System Log-likelihood 1167.2

**********************************************************************

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.24

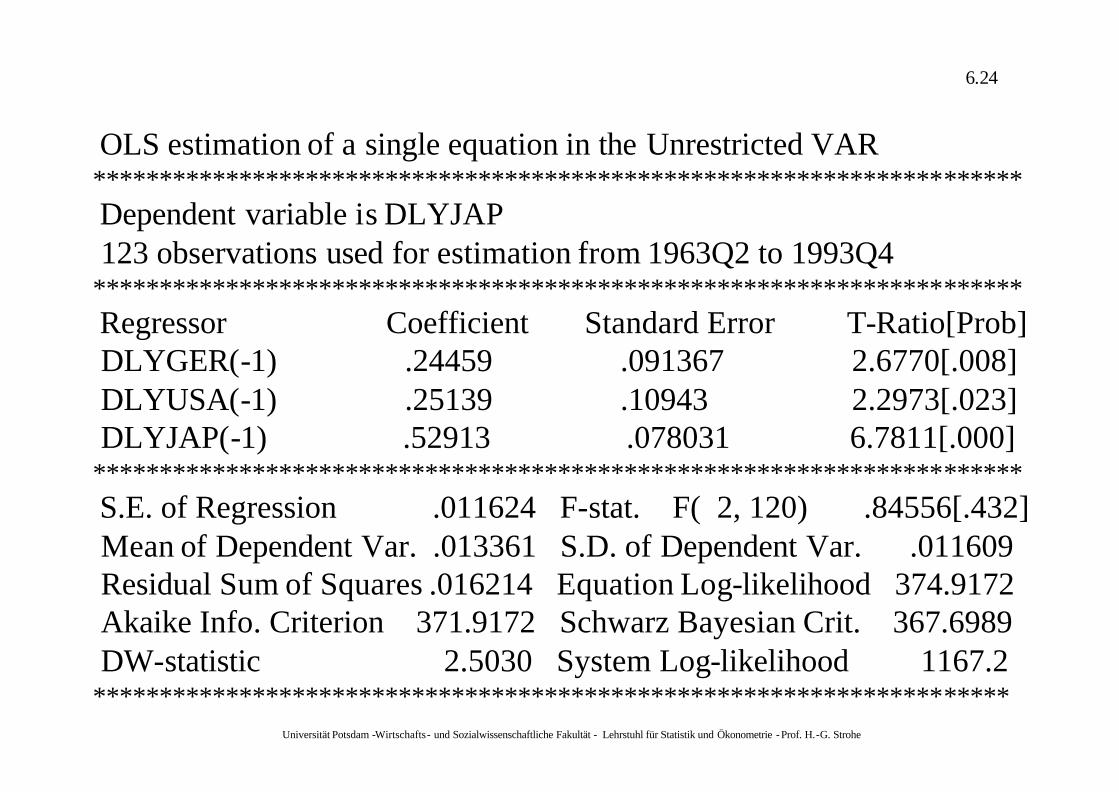

OLS estimation of a single equation in the Unrestricted VAR**********************************************************************Dependent variable is DLYJAP 123 observations used for estimation from 1963Q2 to 1993Q4

**********************************************************************Regressor Coefficient Standard Error T-Ratio[Prob]DLYGER(-1) .24459 .091367 2.6770[.008]DLYUSA(-1) .25139 .10943 2.2973[.023]DLYJAP(-1) .52913 .078031 6.7811[.000]

**********************************************************************S.E. of Regression .011624 F-stat. F( 2, 120) .84556[.432]Mean of Dependent Var. .013361 S.D. of Dependent Var. .011609Residual Sum of Squares .016214 Equation Log-likelihood 374.9172Akaike Info. Criterion 371.9172 Schwarz Bayesian Crit. 367.6989DW-statistic 2.5030 System Log-likelihood 1167.2

*********************************************************************

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

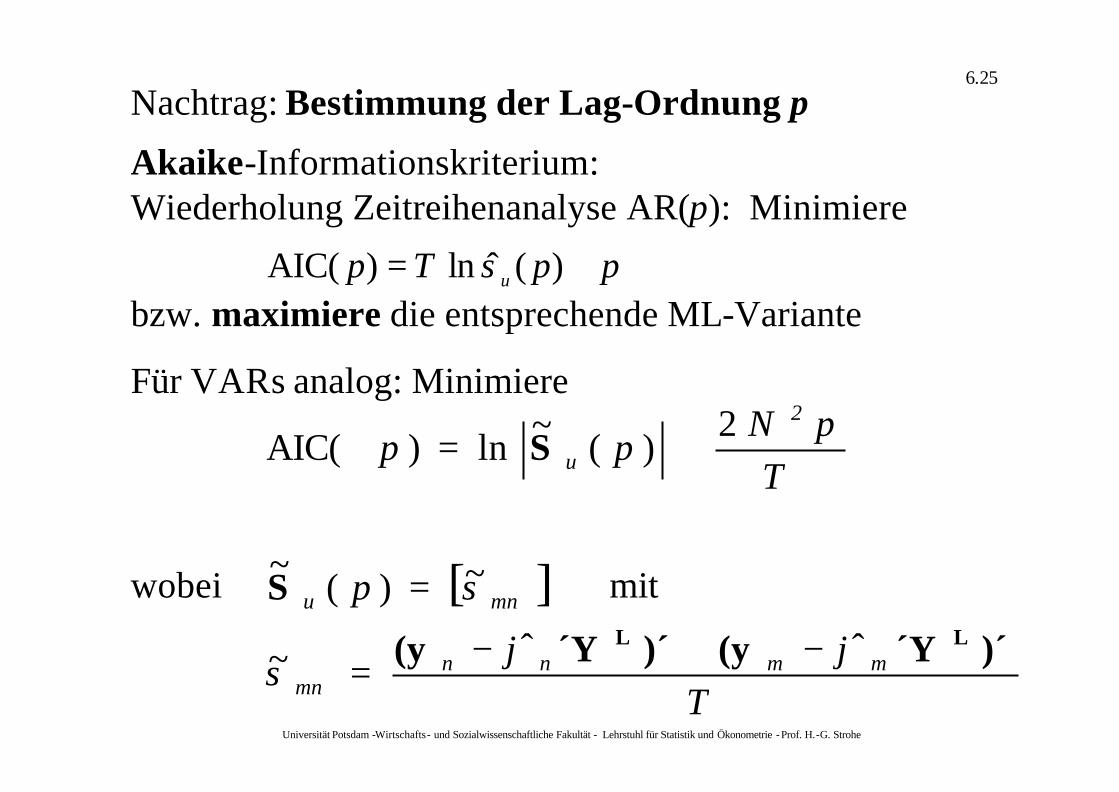

6.25

Nachtrag: Bestimmung der Lag-Ordnung p

Akaike-Informationskriterium:Wiederholung Zeitreihenanalyse AR(p): Minimiere

[ ]

Ts

sp

TpN

pp

mmnnmn

mnu

2

u

)´´Y(y )´´Y(y

S

S

LL ϕϕ ˆˆ~

~)(~

2)(

~ln)AIC(

−⋅−=

=

+=

ppsT p u += )(ˆln)AIC(

Für VARs analog: Minimiere

wobei mit

bzw. maximiere die entsprechende ML-Variante

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

6.26

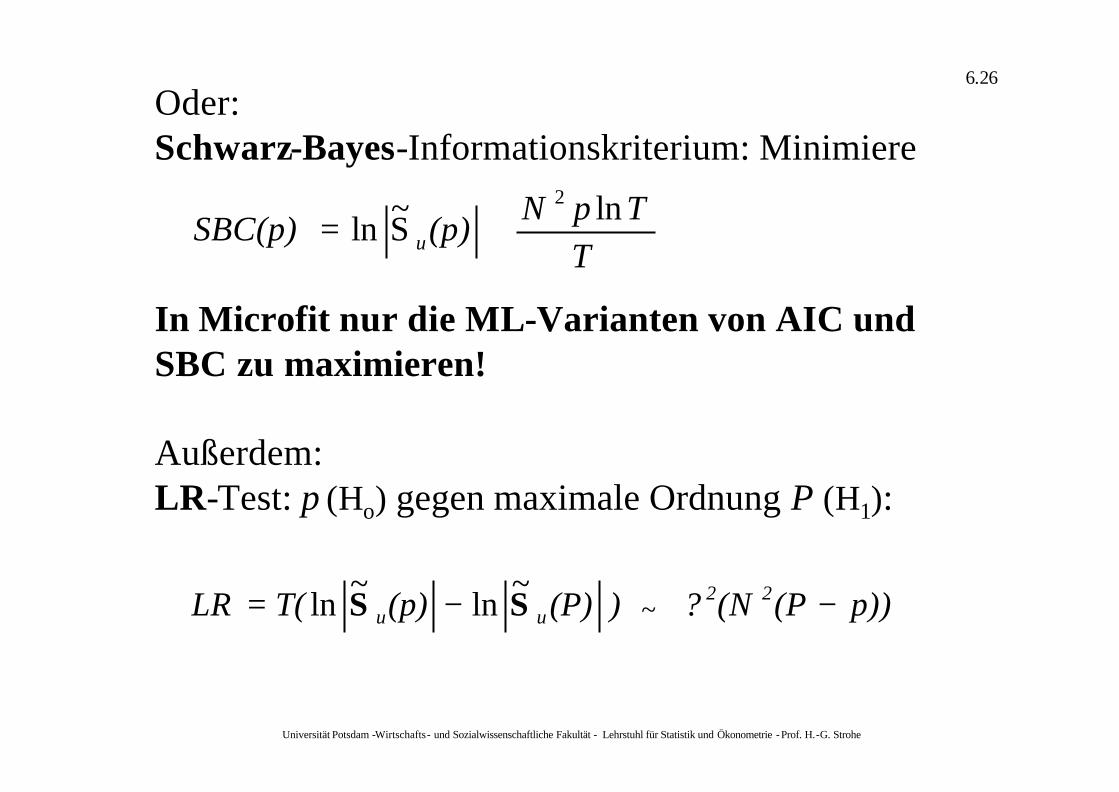

Oder:Schwarz-Bayes-Informationskriterium: Minimiere

TTpN(p)SBC(p) u

lnS~ln2

+=

In Microfit nur die ML-Varianten von AIC und SBC zu maximieren!

Außerdem:LR-Test: p (Ho) gegen maximale Ordnung P (H1):

~

ln~

ln p))(P(N?) (P)(p)T(LR 22uu −−= SS ~

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

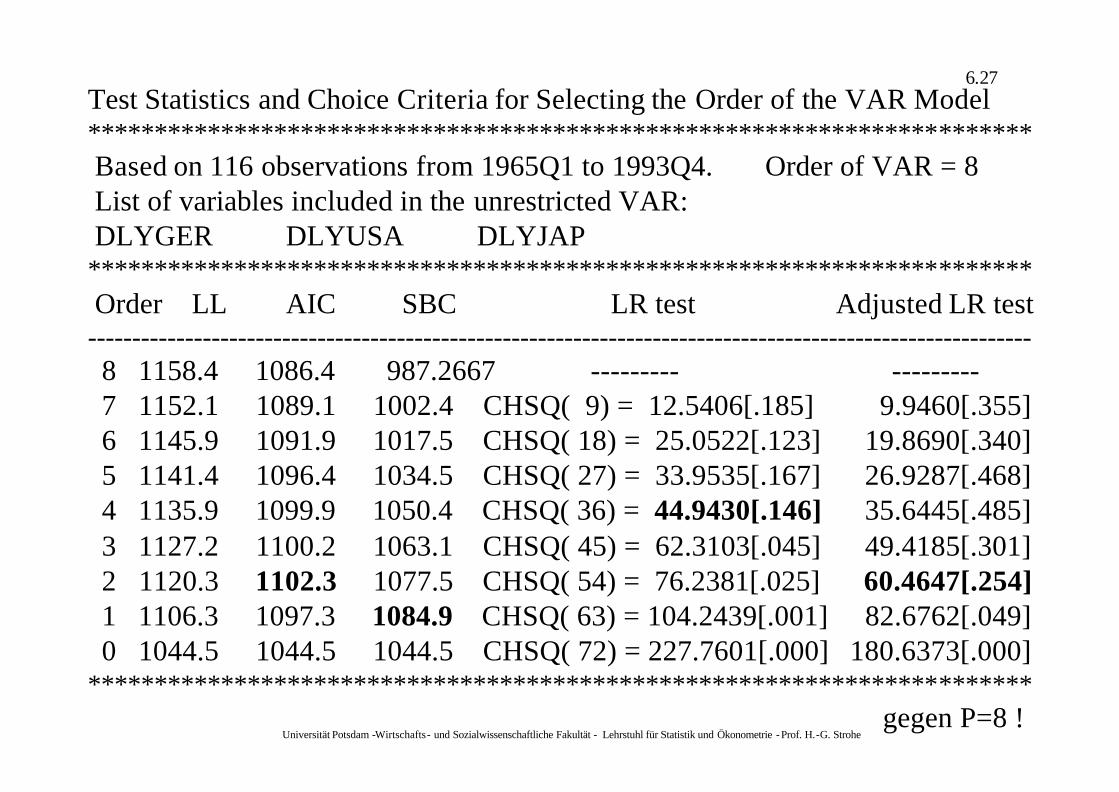

6.27Test Statistics and Choice Criteria for Selecting the Order of the VAR Model ***********************************************************************Based on 116 observations from 1965Q1 to 1993Q4. Order of VAR = 8 List of variables included in the unrestricted VAR: DLYGER DLYUSA DLYJAP

***********************************************************************Order LL AIC SBC LR test Adjusted LR test

-----------------------------------------------------------------------------------------------------------8 1158.4 1086.4 987.2667 --------- ---------7 1152.1 1089.1 1002.4 CHSQ( 9) = 12.5406[.185] 9.9460[.355]6 1145.9 1091.9 1017.5 CHSQ( 18) = 25.0522[.123] 19.8690[.340]5 1141.4 1096.4 1034.5 CHSQ( 27) = 33.9535[.167] 26.9287[.468]4 1135.9 1099.9 1050.4 CHSQ( 36) = 44.9430[.146] 35.6445[.485]3 1127.2 1100.2 1063.1 CHSQ( 45) = 62.3103[.045] 49.4185[.301]2 1120.3 1102.3 1077.5 CHSQ( 54) = 76.2381[.025] 60.4647[.254]1 1106.3 1097.3 1084.9 CHSQ( 63) = 104.2439[.001] 82.6762[.049]0 1044.5 1044.5 1044.5 CHSQ( 72) = 227.7601[.000] 180.6373[.000]

***********************************************************************gegen P=8 !

Universität Potsdam -Wirtschafts- und Sozialwissenschaftliche Fakultät - Lehrstuhl für Statistik und Ökonometrie -Prof. H.-G. Strohe

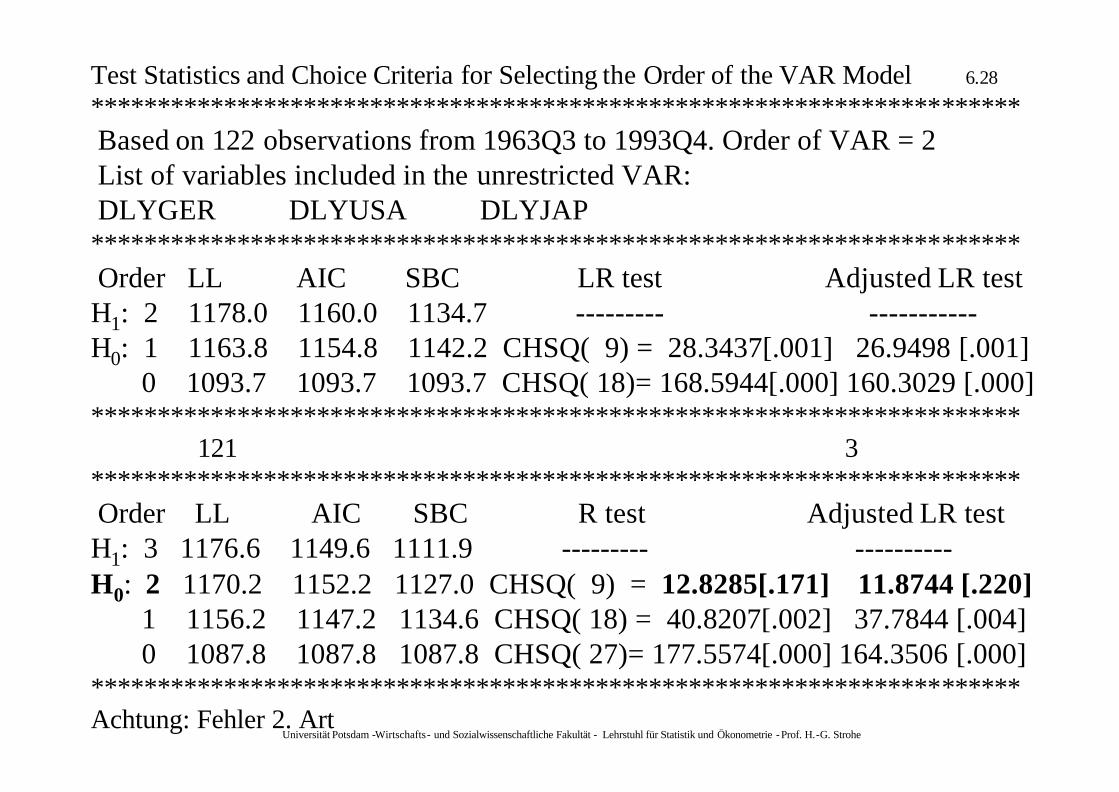

6.28Test Statistics and Choice Criteria for Selecting the Order of the VAR Model **********************************************************************Based on 122 observations from 1963Q3 to 1993Q4. Order of VAR = 2 List of variables included in the unrestricted VAR: DLYGER DLYUSA DLYJAP

**********************************************************************Order LL AIC SBC LR test Adjusted LR test H1: 2 1178.0 1160.0 1134.7 --------- -----------H0: 1 1163.8 1154.8 1142.2 CHSQ( 9) = 28.3437[.001] 26.9498 [.001]

0 1093.7 1093.7 1093.7 CHSQ( 18)= 168.5944[.000] 160.3029 [.000]**********************************************************************

121 3**********************************************************************Order LL AIC SBC R test Adjusted LR test H1: 3 1176.6 1149.6 1111.9 --------- ----------H0: 2 1170.2 1152.2 1127.0 CHSQ( 9) = 12.8285[.171] 11.8744 [.220]

1 1156.2 1147.2 1134.6 CHSQ( 18) = 40.8207[.002] 37.7844 [.004]0 1087.8 1087.8 1087.8 CHSQ( 27)= 177.5574[.000] 164.3506 [.000]

**********************************************************************Achtung: Fehler 2. Art