Embed Size (px)

Citation preview

UNIVERSITAT LINZJOHANNES KEPLER JKU

Technisch-NaturwissenschaftlicheFakultat

Symbolic Regression for Knowledge Discovery –Bloat, Overfitting, and Variable Interaction

Networks

DISSERTATION

zur Erlangung des akademischen Grades

Doktor

im Doktoratsstudium der

Technischen Wissenschaften

Eingereicht von:

Dipl.-Ing. Gabriel Kronberger

Angefertigt am:

Institut fur formale Modelle und Verifikation

Beurteilung:

Priv.-Doz. Dipl.-Ing. Dr. Michael Affenzeller (Betreuung)Assoc.-Prof. Dipl.-Ing. Dr. Ulrich Bodenhofer

Linz, 12, 2010

For Gabi

Acknowledgments

This thesis would not have been possible without the support of a number of people.

First and foremost I want to thank my adviser Dr. Michael Affenzeller, who has notonly become my mentor but also a close friend in the years since I first started my foraysinto the area of evolutionary computation.

Furthermore, I would like to express my gratitude to my second adviser Dr. UlrichBodenhofer for introducing me to the statistical elements of machine learning and en-couraging me to critically scrutinize modeling results.

I am also thankful to Prof. Dr. Witold Jacak, dean of the School of Informatics,Communications and Media in Hagenberg of the Upper Austria University of AppliedSciences, for giving me the opportunity to work at the research center Hagenberg andallowing me to work on this thesis.

I thank all members of the research group for heuristic and evolutionary algorithms(HEAL). Andreas Beham, for implementing standard variants of heuristic algorithmsin HeuristicLab. Michael Kommenda, for discussing extensions and improvements ofsymbolic regression for practical applications, some of which are described in this thesis.Dr. Stefan Wagner, for tirelessly improving HeuristicLab, which has been used as thesoftware environment for all experiments presented in this thesis. Dr. Stephan Winkler,for introducing me to genetic programming and system identification and for proofread-ing a first draft of this thesis to improve its linguistic quality. Ciprian Zavoianu, for theinteresting discussions about aspects of genetic programming.

I also wish to extend my thanks to my colleagues who invested a part of their valuabletime to improve application-specific sections of this thesis. Christoph Feilmayr, foradvice regarding data-based modeling of the blast furnace process and for proofreadingand improving a draft of Chapter 8. Leonhard Schickmair, for his input on variablerelevance metrics and for proofreading and improving a draft of Chapter 8. Dr. StefanFink, for preparing a dataset for economic modeling and for the discussion of economicmodels produced by genetic programming.

Finally, I thank my parents and my family who supported me and my interests incomputer science. I thank all my friends for encouraging me to finish this thesis. Thiswork is dedicated to Gabi for her love and support.

This thesis mainly reflects research work done within the Josef Ressel-center for heuris-tic optimization “Heureka!” at the Upper Austria University of Applied Sciences, Cam-pus Hagenberg. The center “Heureka!” is supported within the program “Josef Ressel-Centers” by the Austrian Research Promotion Agency (FFG) on behalf of the AustrianFederal Ministry of Economy, Family and Youth (BMWFJ).

i

Zusammenfassung

Mit der wachsenden Datenmenge, die in unterschiedlichsten Anwendungsbereichen ge-sammelt und aufgezeichnet wird, wachst auch das Bedurfnis, diese Daten sinnvoll zunutzen. In der Wissenschaft haben Daten schon seit jeher einen hohen Stellenwert. Inden jungeren Jahren gewinnt aber auch das wirtschaftliche Potential von Daten zu-nehmend an Bedeutung. In Kombination mit Verfahren zur Datenanalyse kann diesesPotential ausgeschopft werden, sei es im kommerziellen Bereich zur Optimierung vonAngeboten, oder im industriellen Bereich zur Optimierung von Ressourceneinsatz oderProduktqualitat basierend auf Prozessdaten.

In dieser Arbeit wird ein neuer Ansatz fur die Analyse von Daten vorgestellt, der aufsymbolischer Regression mit genetischer Programmierung basiert und das Ziel verfolgt,einen Gesamtuberblick uber das Zusammenspiel von einzelnen Faktoren eines Systemszu ermoglichen. Dabei sollen moglichst alle potentiell interessanten Zusammenhange,welche in einem Datensatz erkennbar sind, in Form von kompakten und verstandlichenModellen identifiziert werden.

Im ersten Teil der vorliegenden Arbeit wird dieser Ansatz der umfassenden symbo-lischen Regression im Detail beschrieben. Wesentliche Themen, die dabei eine Rollespielen, sind die Vermeidung von Bloat und Uberanpassung, die Vereinfachung von Mo-dellen und die Identifikation von relevanten Einflussgroßen. In diesem Zusammenhangwerden unterschiedliche Verfahren zur Vermeidung von Bloat vorgestellt und verglichen.Insbesondere wird der Einfluss von Nachkommenselektion auf Bloat analysiert. Daruberhinaus wird eine neue Moglichkeit zur Erkennung von Uberanpassung vorgestellt. Im Zu-ge dessen werden darauf basierende Erweiterungen zur Reduktion von Uberanpassungvorgestellt und verglichen. Eine wichtige Rolle spielt dabei das Pruning von Modellen,einerseits um Uberanpassung zu verhindern und andererseits um komplexe Modelle zuvereinfachen.

Ein weiterer wesentlicher Aspekt ist die Analyse und Darstellung der umfangreichenMenge von unterschiedlichen Modellen, die aus dem vorgestellten Ansatz resultiert. Indiesem Zusammenhang werden Moglichkeiten zur Quantifizierung von relevanten Ein-flussgroßen vorgestellt, die in weiterer Folge verwendet werden konnen, um Interaktionenvon Variablen des analysierten Systems zu identifizieren. Durch die Visualisierung die-ser Interaktionen entsteht ein Gesamtuberblick uber das betrachtete System. Dies warealleine durch die Analyse einzelner Modelle, die sich auf spezielle Aspekte konzentrie-ren, nicht moglich. Zusatzlich wird im ersten Teil auch die Prognose von multivariatenZeitserien mit genetischer Programmierung beschrieben.

Im zweiten Teil dieser Arbeit wird gezeigt, wie der vorgestellte Ansatz fur die Analysevon realen Systemen eingesetzt werden kann und dadurch neue Einblicke ermoglichtwerden konnen. Die Daten stammen von einem Hochofen fur die Produktion von Stahlund von einem industriellen chemischen Prozess. Zusatzlich wird gezeigt wie derselbeAnsatz zur Identifikation von makrookonomischen Zusammenhangen eingesetzt werdenkann.

Abstract

With the growing amount of data that are collected and recorded in various applicationareas the need to utilize these data is also growing. In science, data have always playedan important role; in recent years, however, the economic potential of data has alsobecome increasingly important. In combination with methods for data analysis, datacan be utilized to their full potential, whether in the commercial sector to optimize offers,or in the industrial sector to optimize resources and product quality based on processdata.

This work describes a new approach for the analysis of data which is based on sym-bolic regression with genetic programming and aims to generate an overall view of theinteractions of various variables of a system. By this means, all potentially interestingrelationships, which can be detected in a dataset, should be identified and representedas compact and understandable models.

In the first part of this work, this approach of comprehensive symbolic regression isdescribed in detail. Important issues that play a role in the process are the preventionof bloat and over-fitting, the simplification of models, and the identification of relevantinput variables. In this context, different methods for bloat control and prevention arepresented and compared. In particular, the influence of offspring selection on bloat isanalyzed. In addition, a new way to detect over-fitting is presented. On the basis ofthis, extensions for the reduction of over-fitting are presented and compared. Pruningof models is featured prominently, on the one hand to prevent over-fitting and on theother hand to simplify complex models.

An important aspect is the analysis of the vast amount of different models that resultsfrom the proposed approach. In this context, different methods to quantify relevantfactors are proposed. These methods can be used to identify interactions of variablesof the analyzed system. Visualizing such interactions provides a general overview ofthe system in question which would not be possible by analysis of individual modelswhich are concentrated on selected aspects of the problem. Additionally, the prognosisof multivariate time series with genetic programming is described in the first part.

The second part of this work shows how the described approach can be applied tothe analysis of real-world systems, and how the result of this data analysis process canresult in the gain of new knowledge about the investigated system. The analyzed datastem from a blast furnace for the production of steel and an industrial chemical process.In addition the same approach is also applied on a data collection storing economic datain order to identify macro-economic interactions.

Eidesstattliche Erklarung

Ich erklare an Eides statt, dass ich die vorliegende Dissertation selbststandig und ohnefremde Hilfe verfasst, andere als die angegebenen Quellen und Hilfsmittel nicht benutztbzw. die wortlich oder sinngemaß entnommenen Stellen als solche kenntlich gemachthabe.

Linz, December 15, 2010 Dipl.-Ing. Gabriel Kronberger

vii

Contents

1. Introduction 71.1. Thesis Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101.2. Research Project Background . . . . . . . . . . . . . . . . . . . . . . . . . 11

2. Machine Learning and Data Mining 132.1. Supervised Learning and Unsupervised Learning . . . . . . . . . . . . . . 132.2. Classification, Regression and Clustering . . . . . . . . . . . . . . . . . . . 142.3. Reinforcement Learning . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152.4. Time Series Forecasting . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162.5. Generalization and Overfitting . . . . . . . . . . . . . . . . . . . . . . . . 16

2.5.1. Overfitting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.5.2. Bad Generalization because of Incomplete Data . . . . . . . . . . . 182.5.3. Time Series Modeling Pitfalls . . . . . . . . . . . . . . . . . . . . . 18

3. Evolutionary Algorithms and Genetic Programming 213.1. Evolutionary Algorithms . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213.2. Genetic Programming . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

3.2.1. Genetic Programming Variants . . . . . . . . . . . . . . . . . . . . 223.3. Bloat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.3.1. Inviable Code and Unoptimized Code . . . . . . . . . . . . . . . . 253.3.2. Bloat Control in Practice . . . . . . . . . . . . . . . . . . . . . . . 253.3.3. Bloat Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263.3.4. Theoretically Motivated Bloat Control . . . . . . . . . . . . . . . . 273.3.5. Quantification of Bloat . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.4. Data-based modeling with Genetic Programming . . . . . . . . . . . . . . 293.4.1. Symbolic Regression . . . . . . . . . . . . . . . . . . . . . . . . . . 293.4.2. Overfitting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

3.5. Offspring Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 313.6. Genetic Programming with HeuristicLab . . . . . . . . . . . . . . . . . . . 32

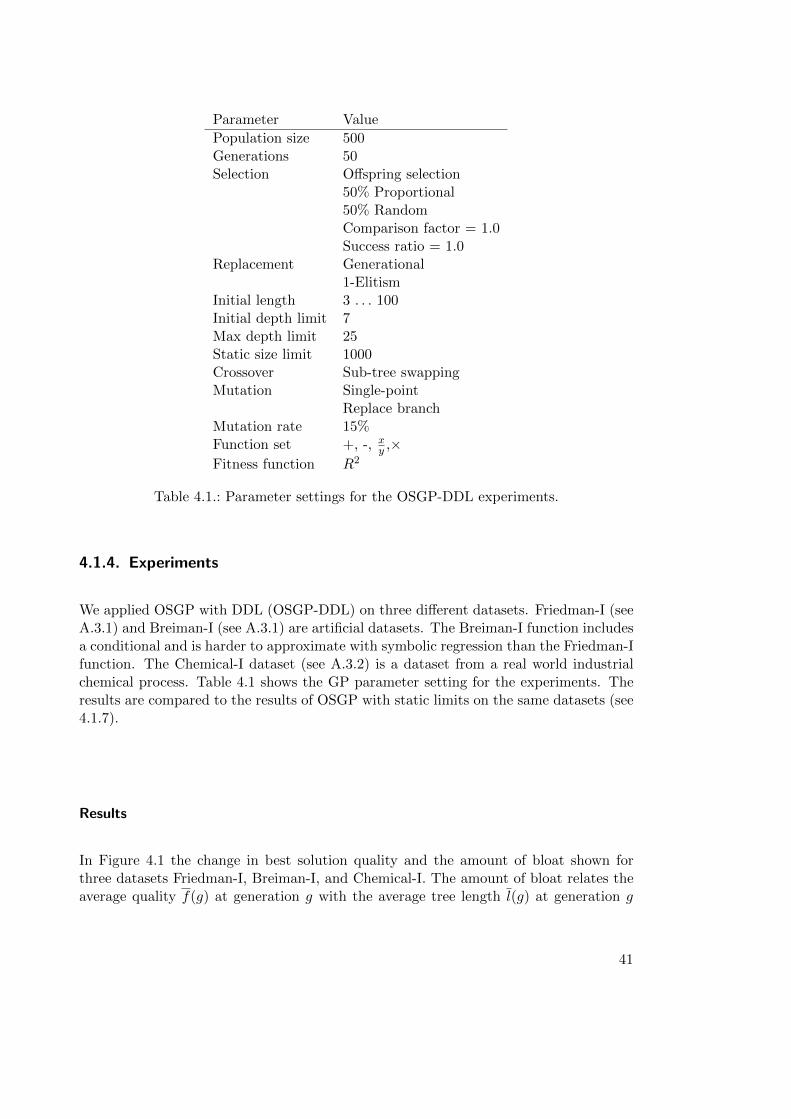

4. Interpretation and Simplification of Symbolic Regression Solutions 354.1. Bloat Control - Searching for Parsimonious Solutions . . . . . . . . . . . . 35

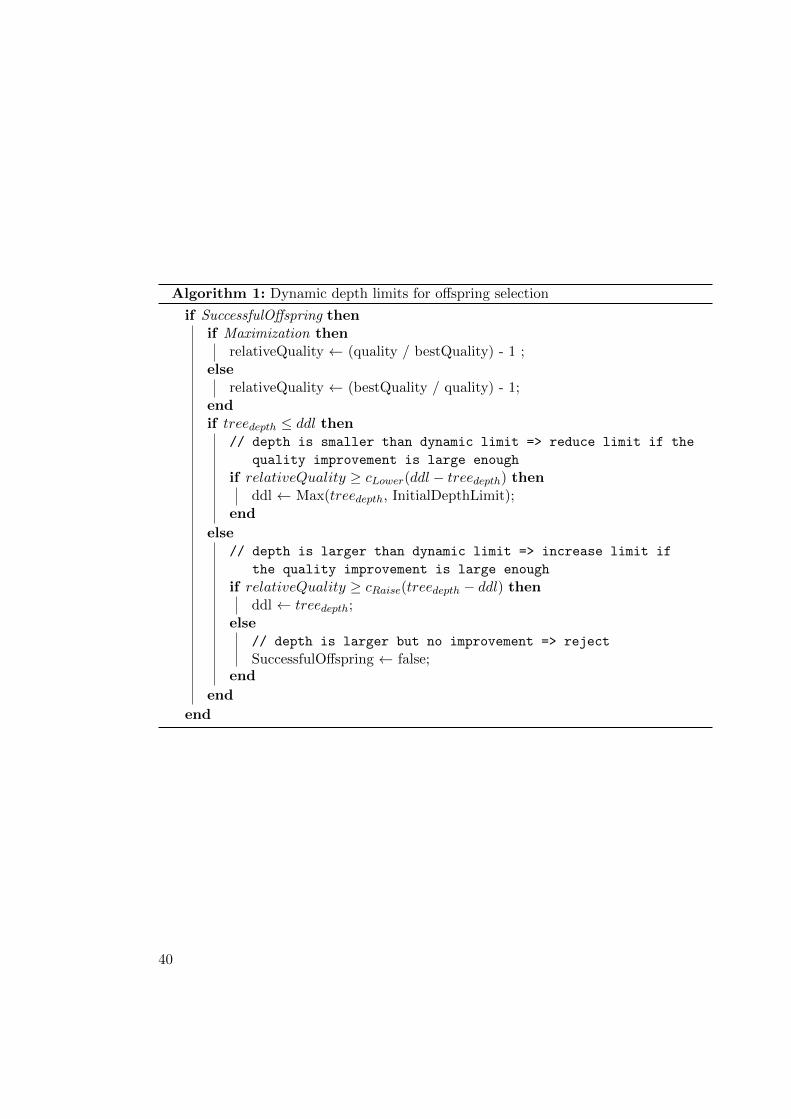

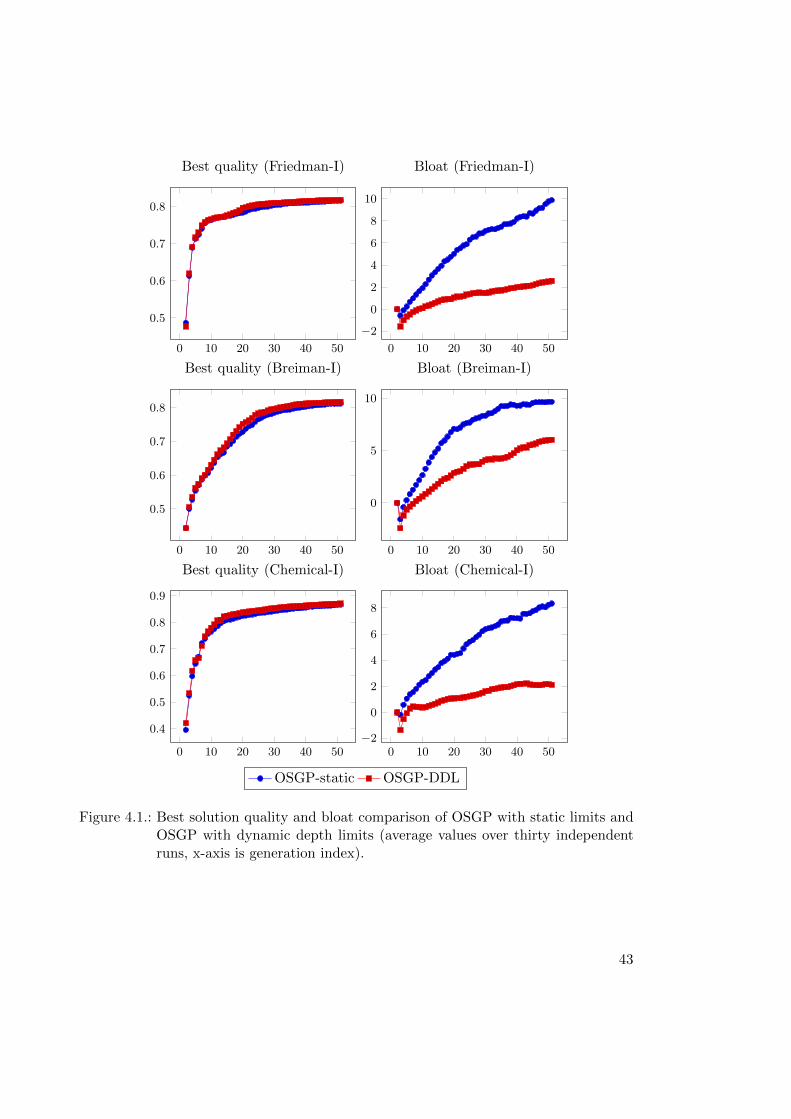

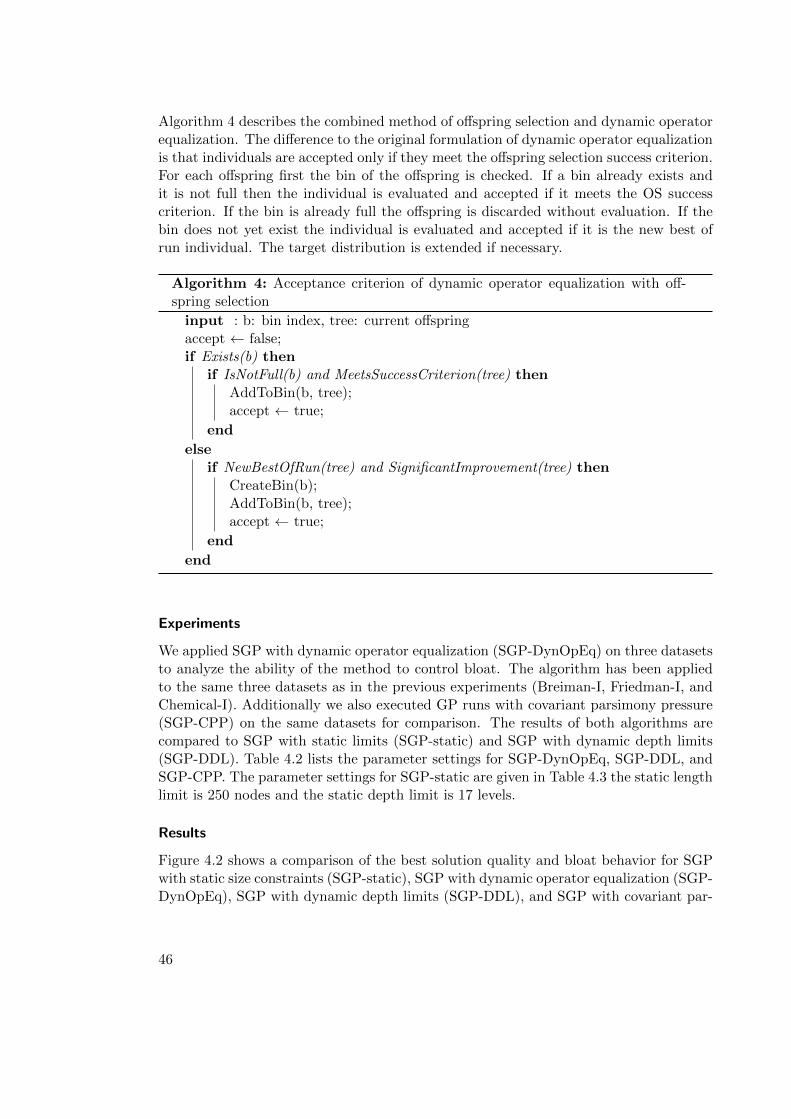

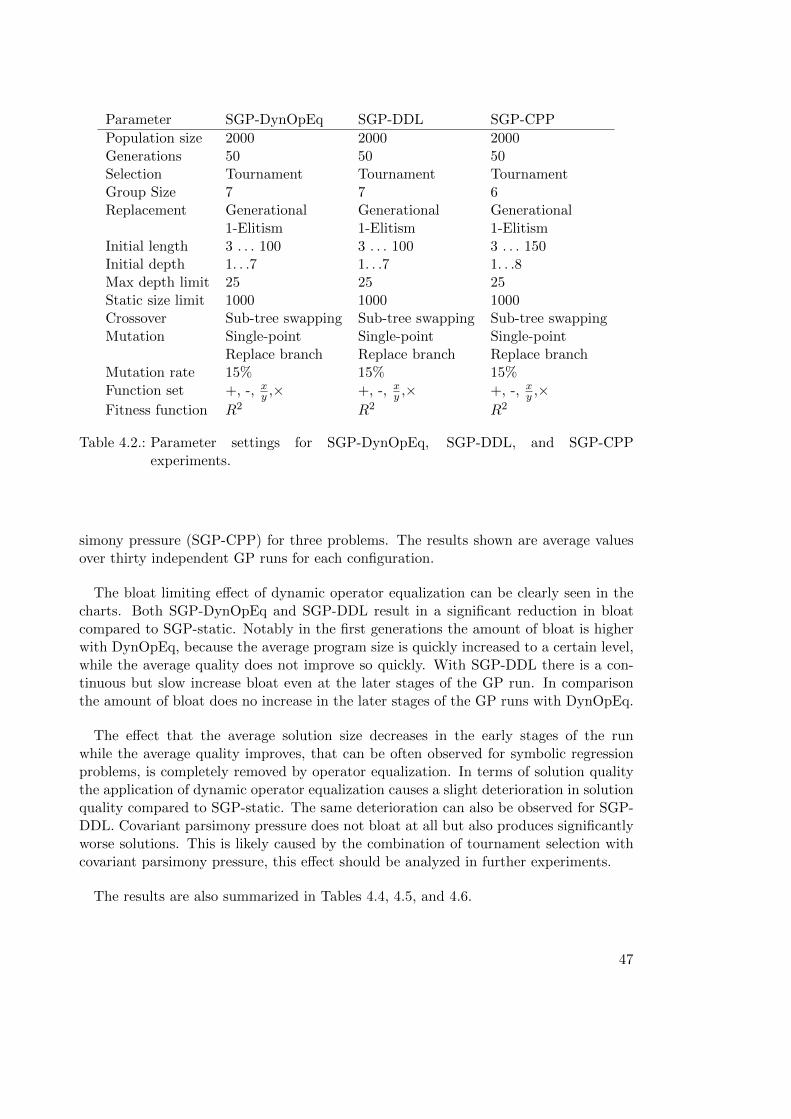

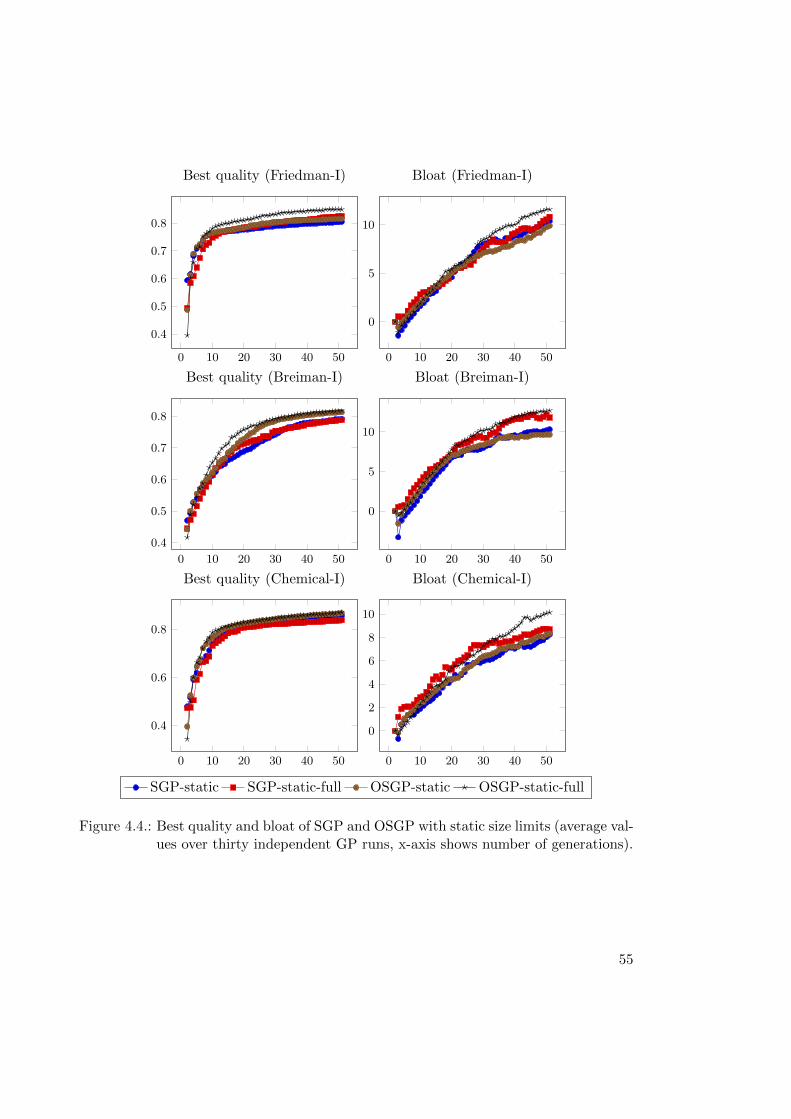

4.1.1. Static Depth and Length Limits . . . . . . . . . . . . . . . . . . . 364.1.2. Parsimony Pressure . . . . . . . . . . . . . . . . . . . . . . . . . . 364.1.3. Dynamic Depth Limits . . . . . . . . . . . . . . . . . . . . . . . . . 384.1.4. Experiments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 414.1.5. Operator Equalization . . . . . . . . . . . . . . . . . . . . . . . . . 42

1

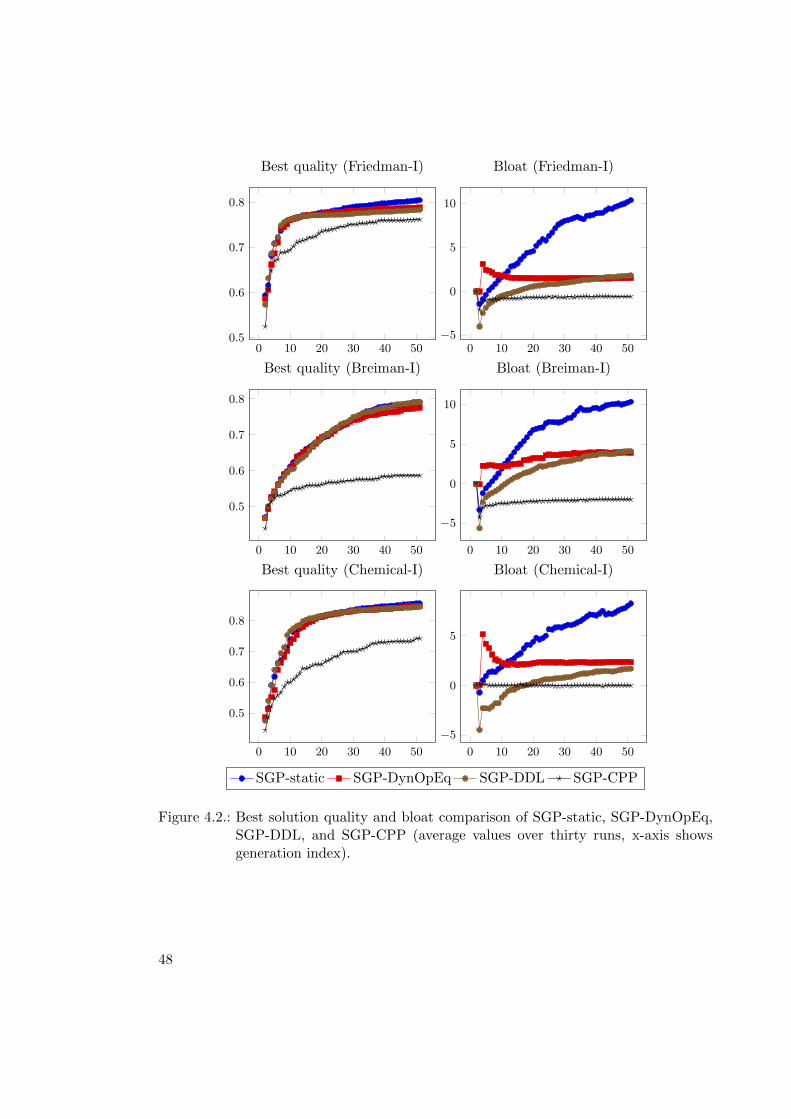

4.1.6. Pruning to Reduce Bloat . . . . . . . . . . . . . . . . . . . . . . . 49

4.1.7. Does Offspring Selection Reduce Bloat? . . . . . . . . . . . . . . . 50

4.1.8. Multi-objective GP . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

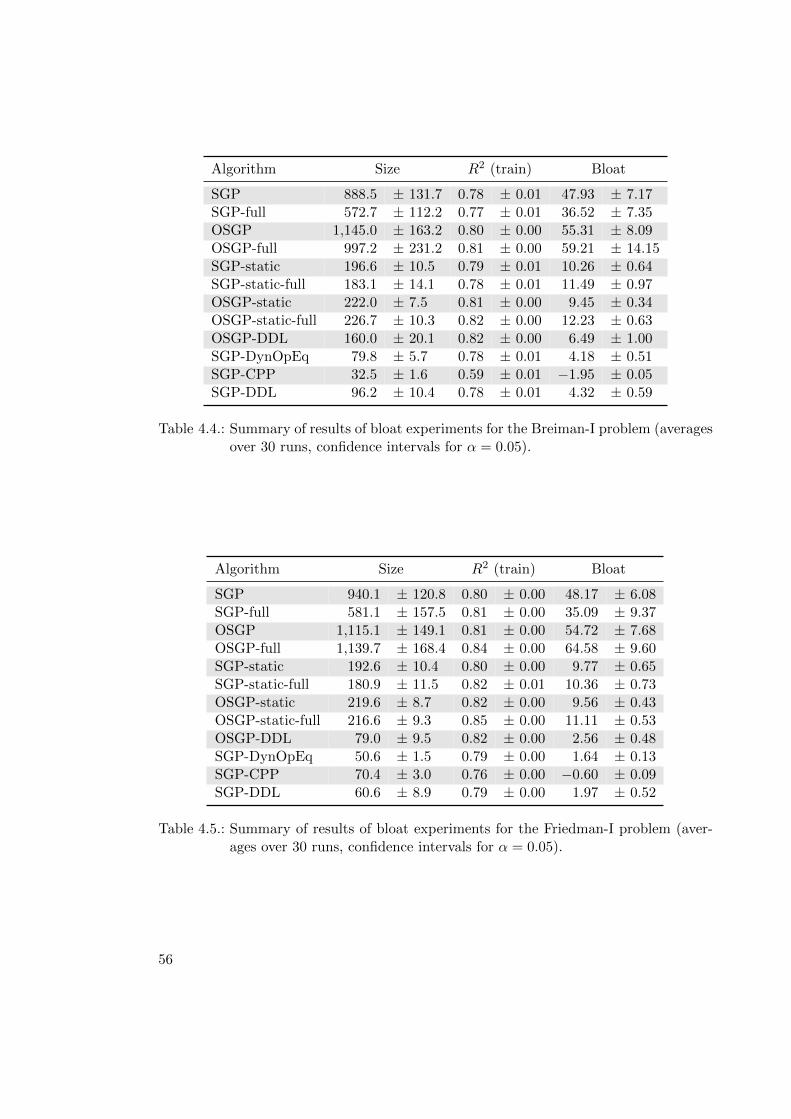

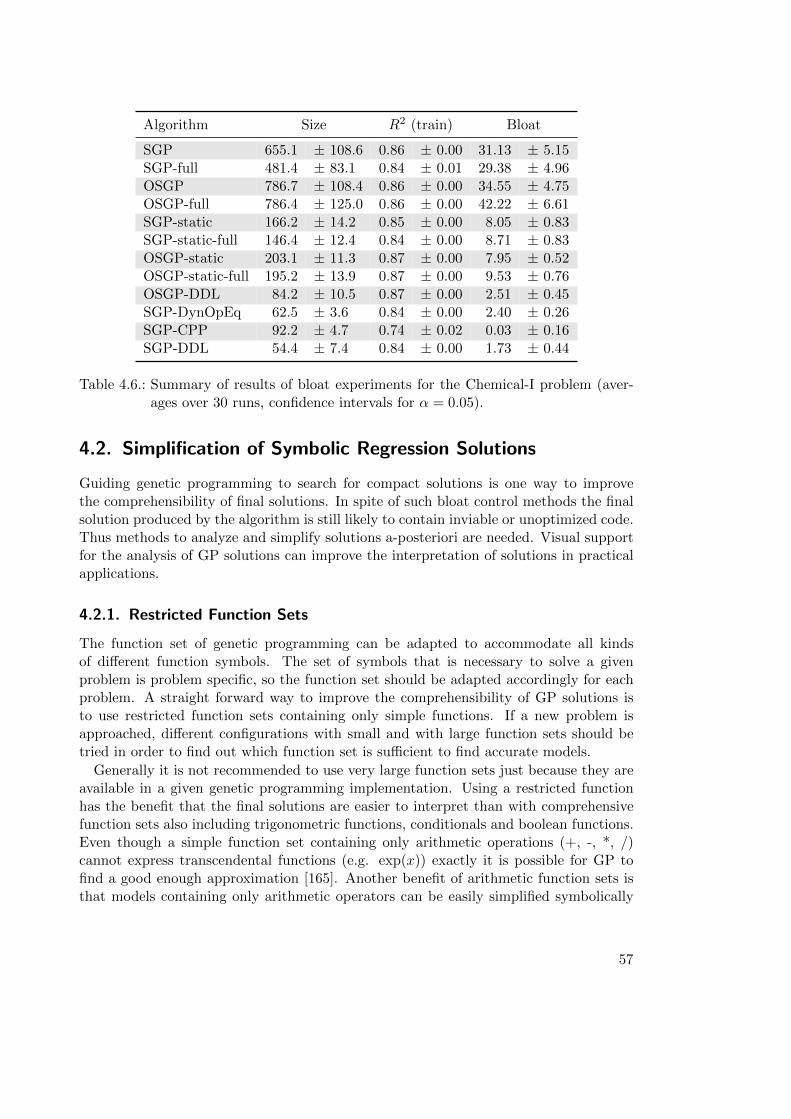

4.1.9. Summary of Results of Bloat Experiments . . . . . . . . . . . . . . 54

4.1.10. Effects of Bloat Control on Genetic Diversity . . . . . . . . . . . . 54

4.2. Simplification of Symbolic Regression Solutions . . . . . . . . . . . . . . . 57

4.2.1. Restricted Function Sets . . . . . . . . . . . . . . . . . . . . . . . . 57

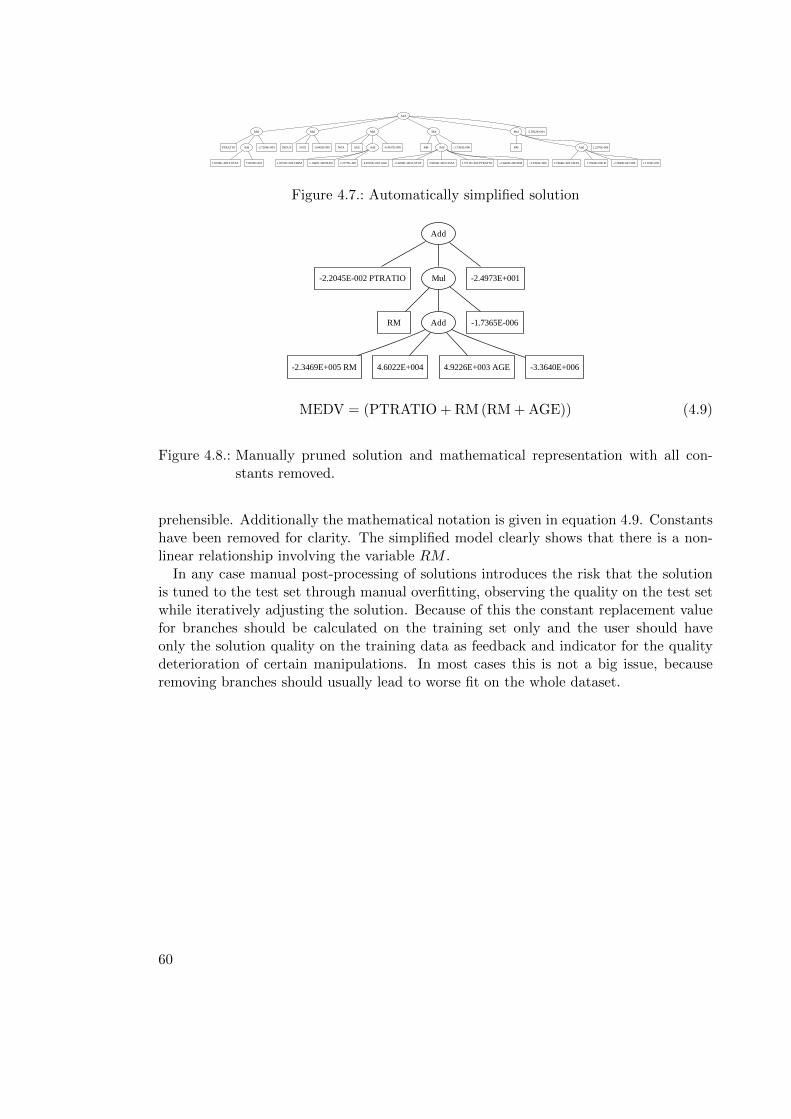

4.2.2. Automatic Simplification of Symbolic Expressions . . . . . . . . . 58

4.2.3. Branch Impact Metrics . . . . . . . . . . . . . . . . . . . . . . . . 58

4.2.4. Visual Support for Manual Simplification . . . . . . . . . . . . . . 58

5. Generalization in Genetic Programming 615.1. How to Detect Overfitting in GP . . . . . . . . . . . . . . . . . . . . . . . 62

5.2. Countermeasures Against Overfitting . . . . . . . . . . . . . . . . . . . . . 64

5.2.1. Restarts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

5.2.2. Parsimony Pressure Against Overfitting . . . . . . . . . . . . . . . 65

5.2.3. Pruning Against Overfitting . . . . . . . . . . . . . . . . . . . . . . 65

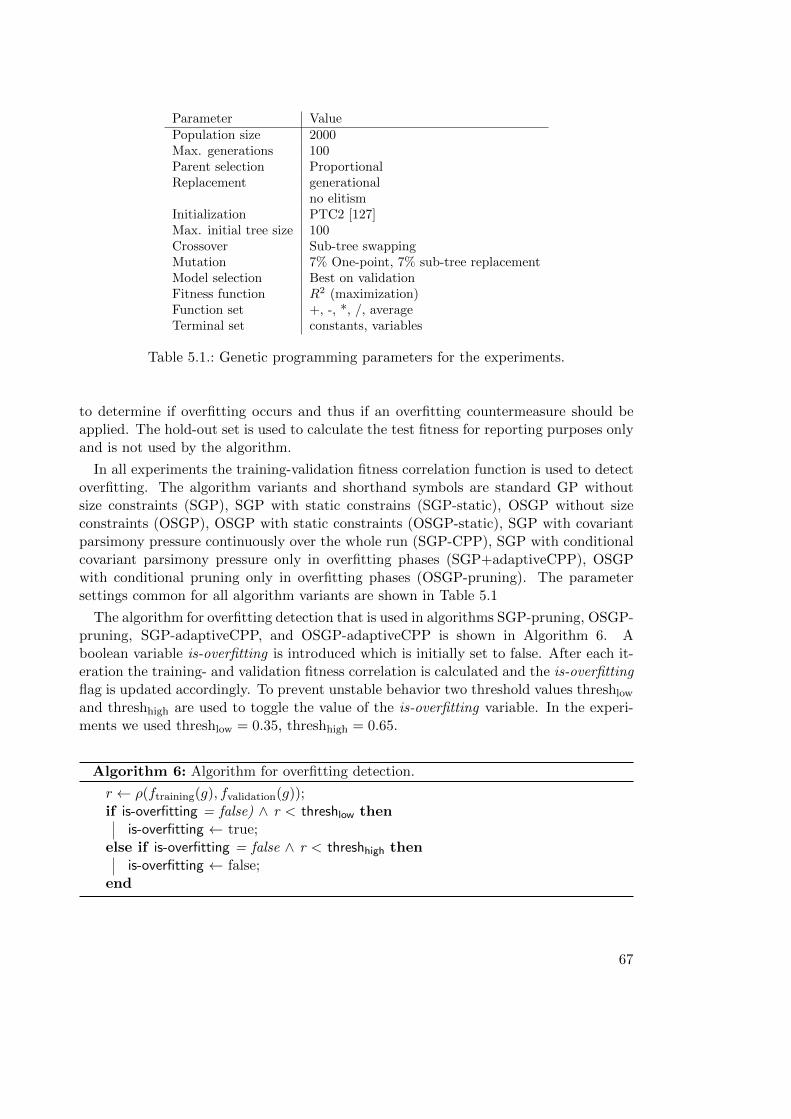

5.3. Experiments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

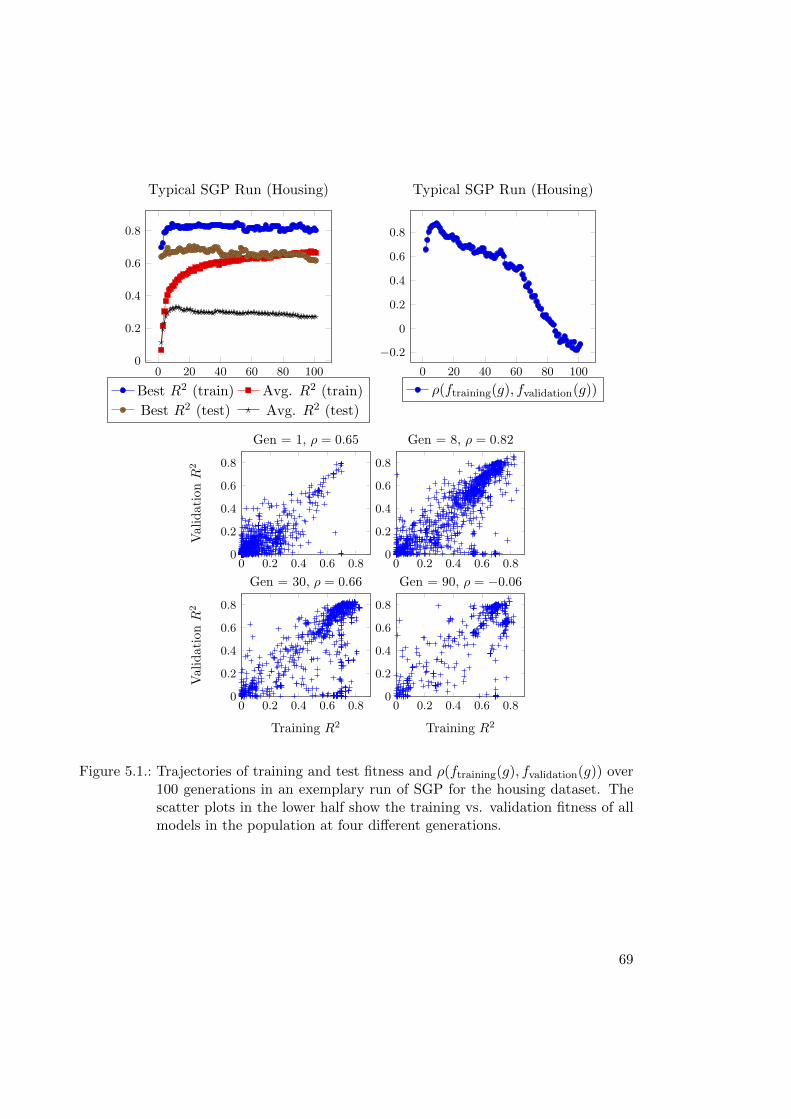

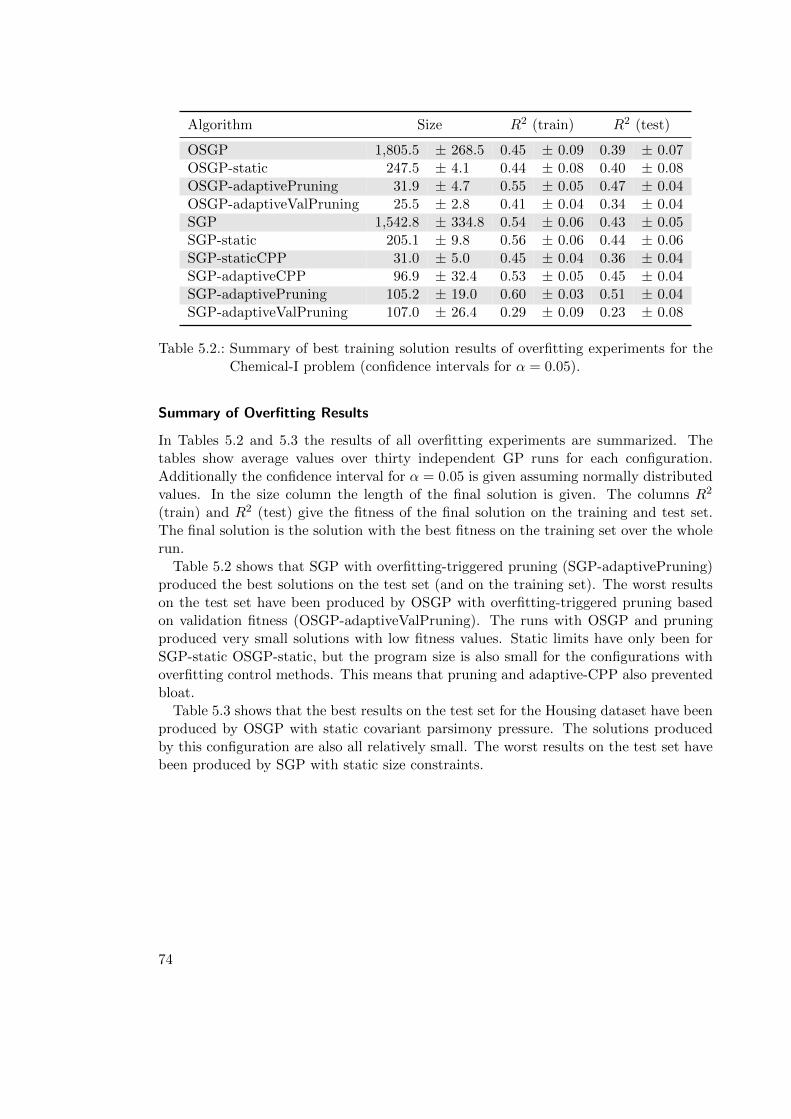

5.4. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

5.4.1. Results: Covariant Parsimony Pressure . . . . . . . . . . . . . . . 68

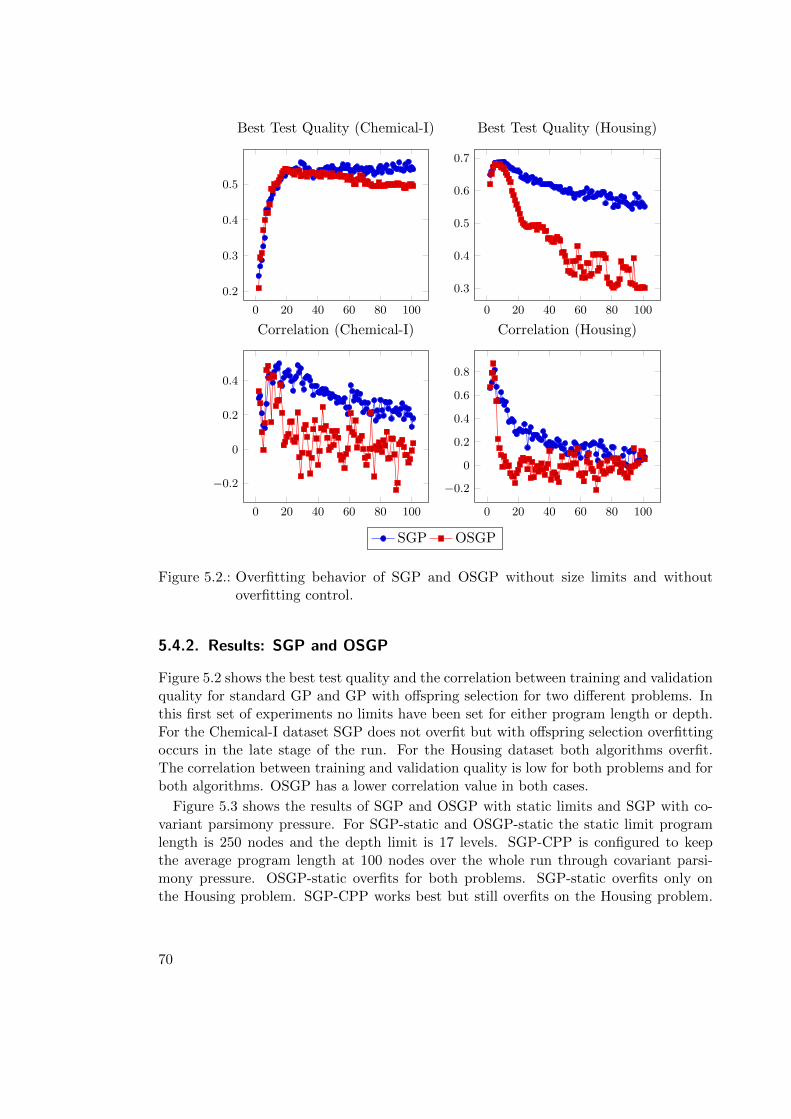

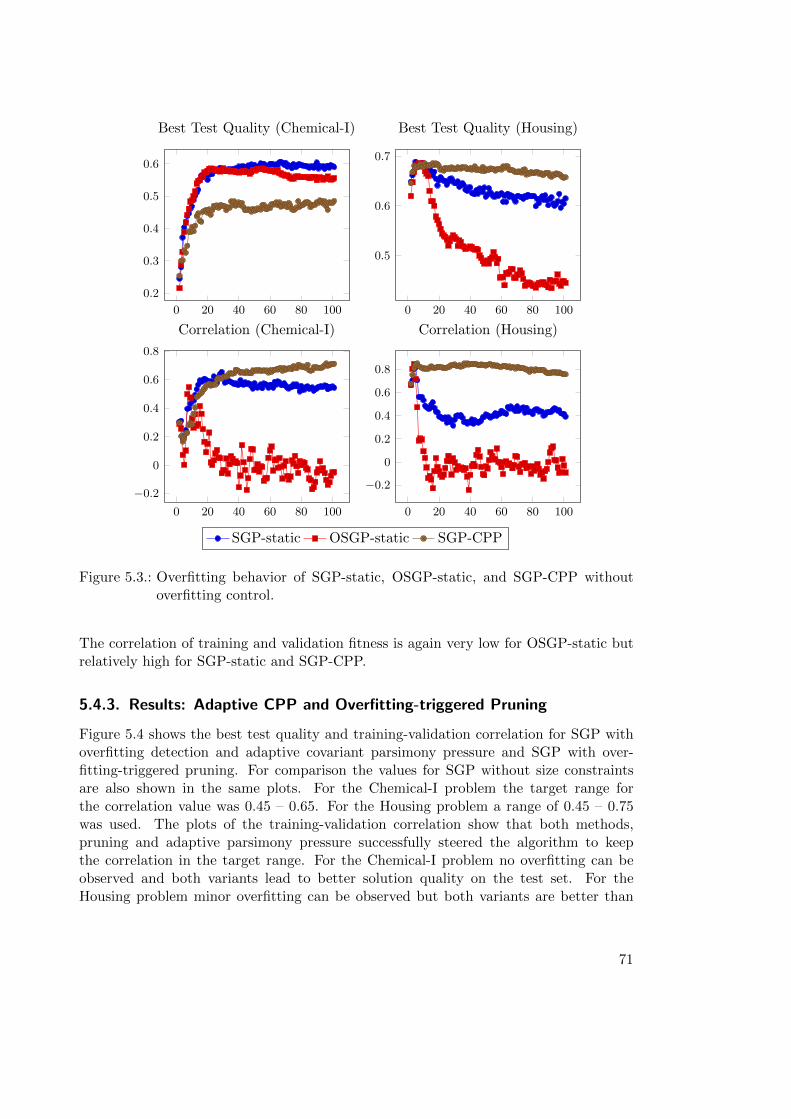

5.4.2. Results: SGP and OSGP . . . . . . . . . . . . . . . . . . . . . . . 70

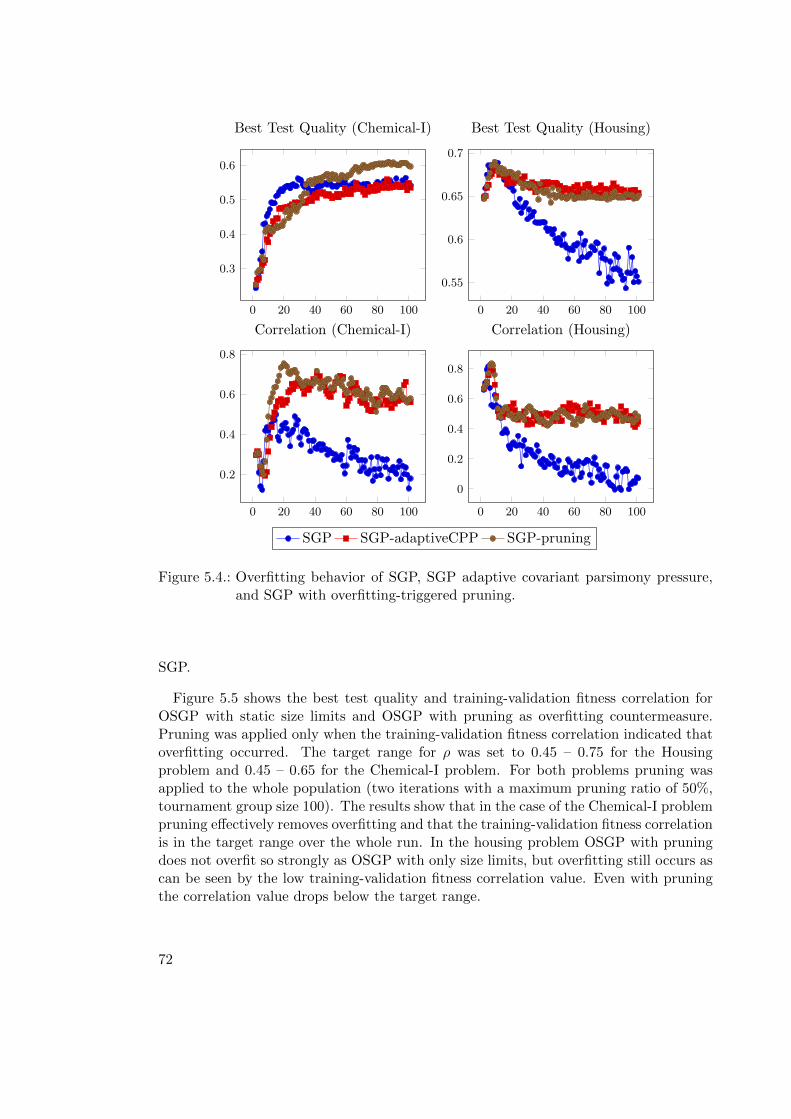

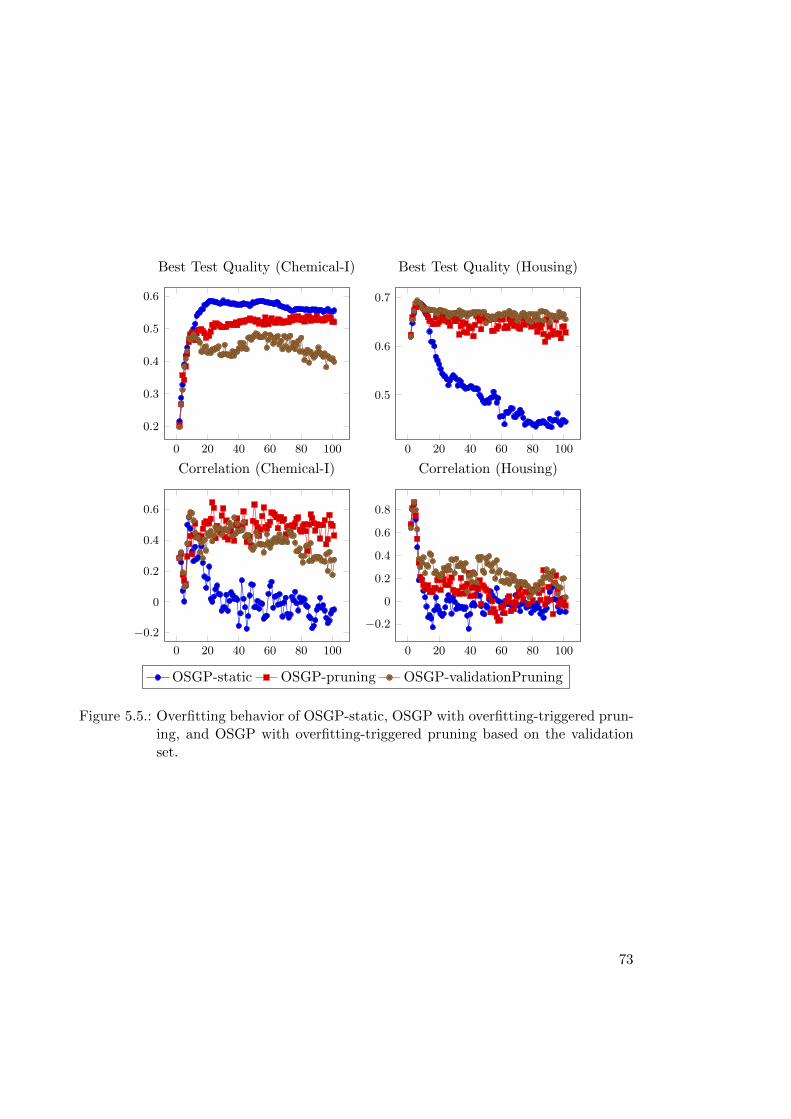

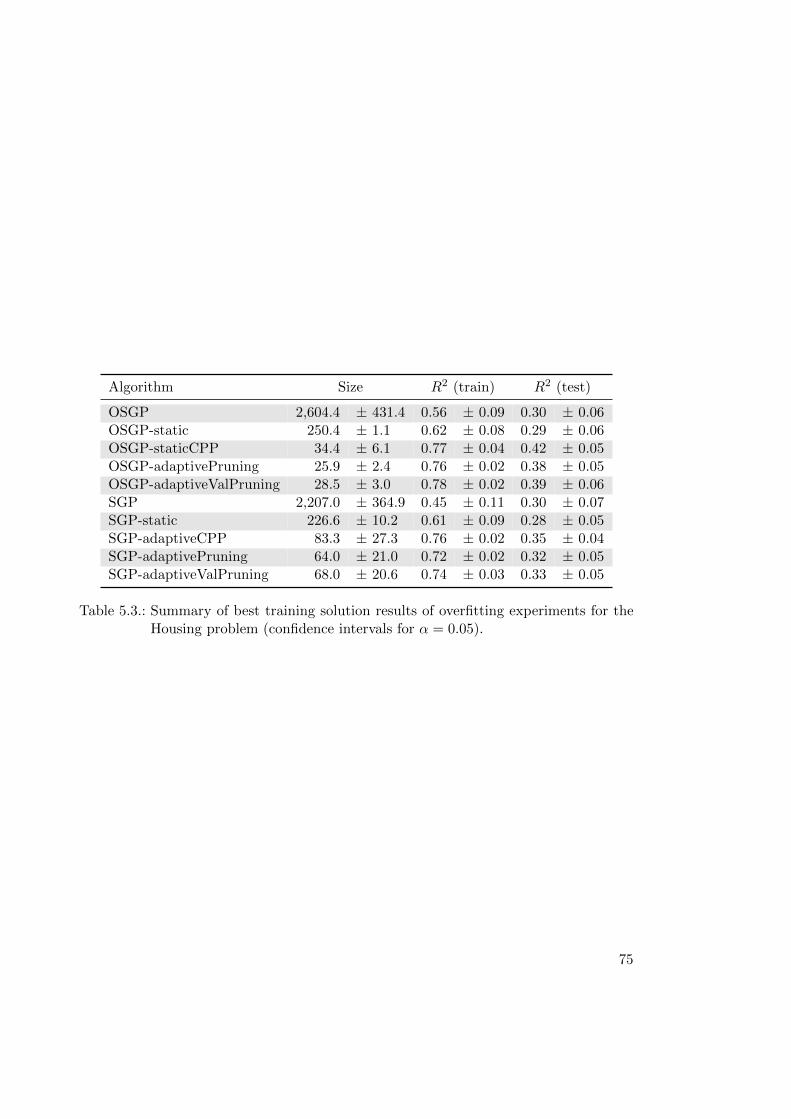

5.4.3. Results: Adaptive CPP and Overfitting-triggered Pruning . . . . . 71

6. Genetic Programming and Data Mining 776.1. Genetic Programming . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

6.1.1. Flexible Model Representation . . . . . . . . . . . . . . . . . . . . 77

6.1.2. Implicit Feature Selection . . . . . . . . . . . . . . . . . . . . . . . 77

6.1.3. Non-Determinism . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

6.1.4. Training Performance . . . . . . . . . . . . . . . . . . . . . . . . . 79

6.1.5. Predictive Accuracy . . . . . . . . . . . . . . . . . . . . . . . . . . 79

6.2. Analysis of Relevant Variables . . . . . . . . . . . . . . . . . . . . . . . . . 80

6.2.1. Relation to Feature Selection . . . . . . . . . . . . . . . . . . . . . 80

6.2.2. Relative Variable Importance in Linear Models . . . . . . . . . . . 81

6.2.3. Variable Importance in GP . . . . . . . . . . . . . . . . . . . . . . 81

6.2.4. Variable Importance in Random Forests . . . . . . . . . . . . . . . 85

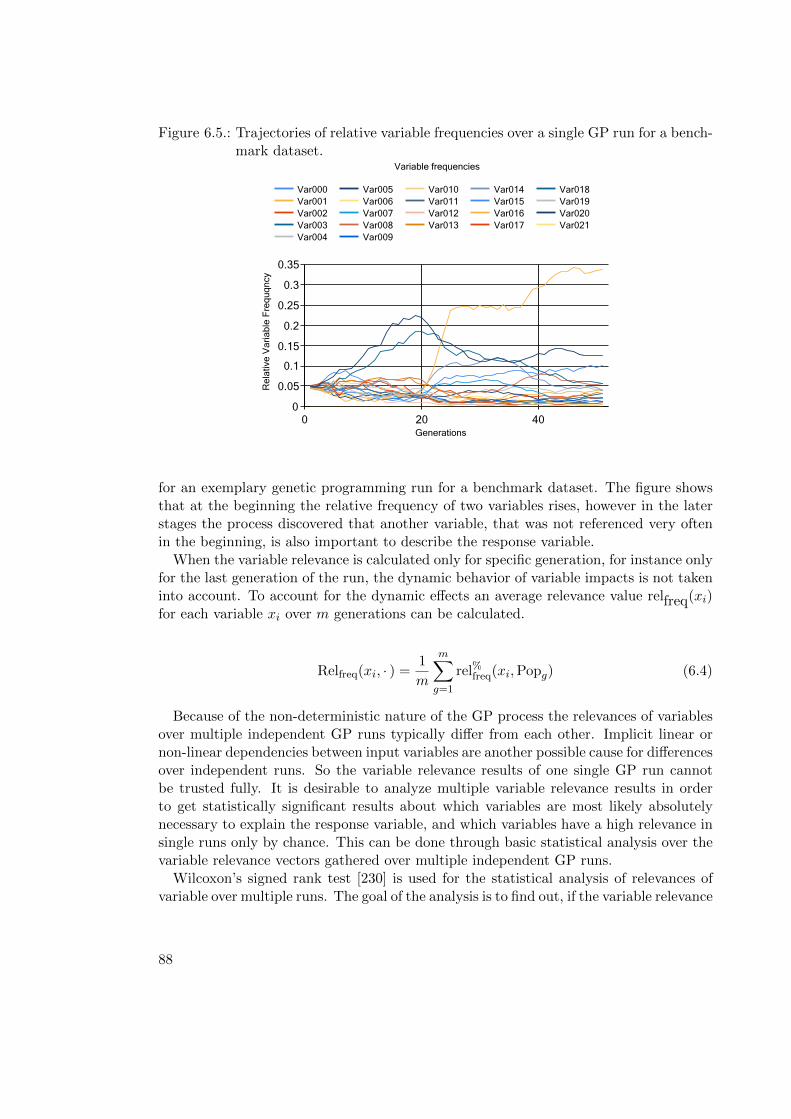

6.2.5. Generalized Variable Importance . . . . . . . . . . . . . . . . . . . 86

6.2.6. Improved Formulations of Variable Importance Metrics for GP . . 87

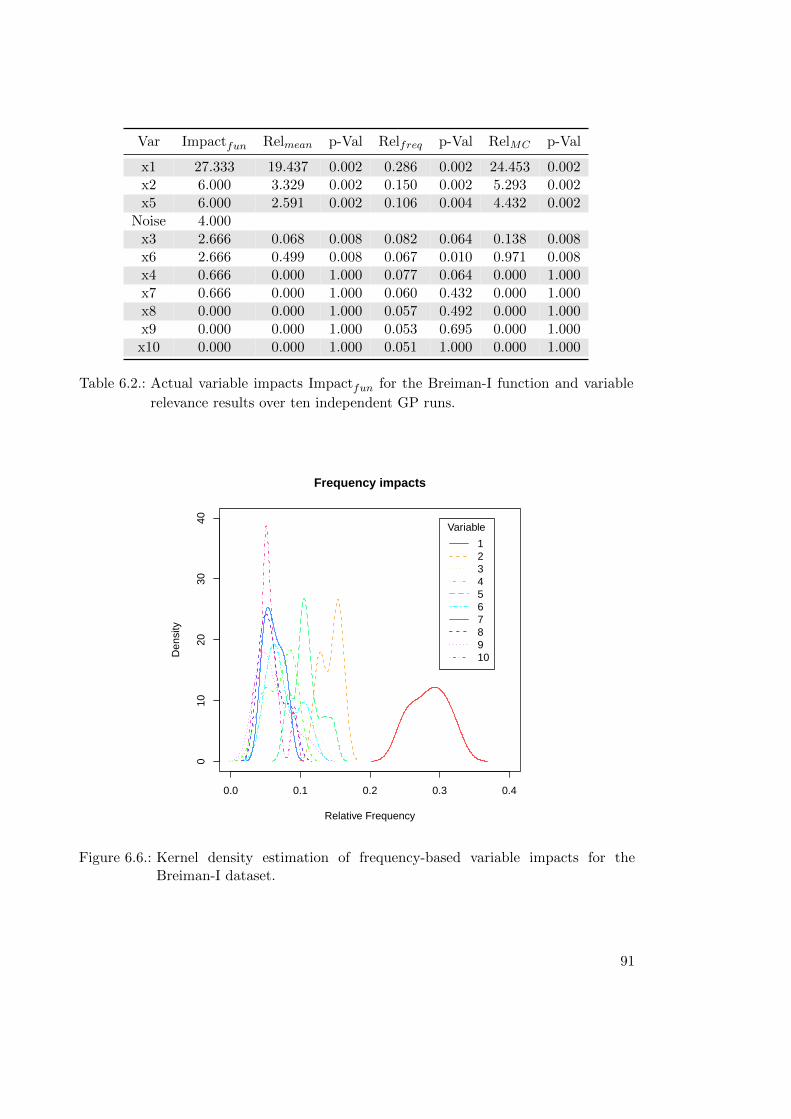

6.2.7. Validation of Variable Relevance Metrics . . . . . . . . . . . . . . . 89

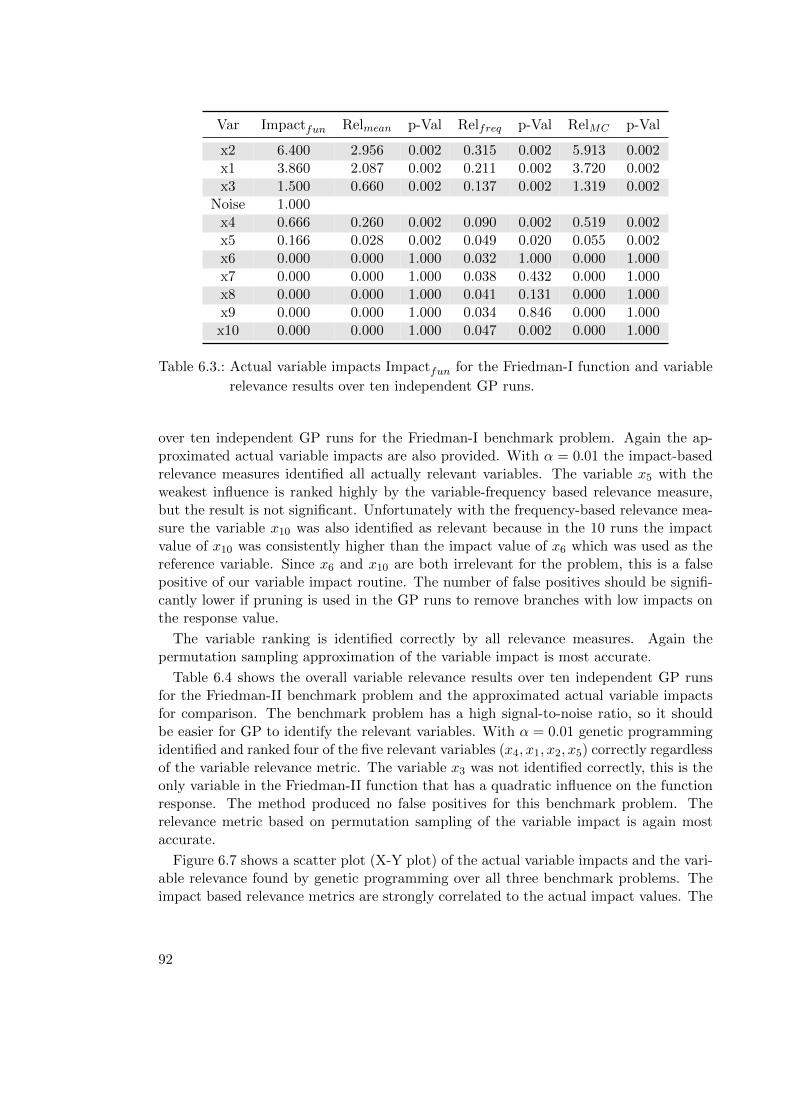

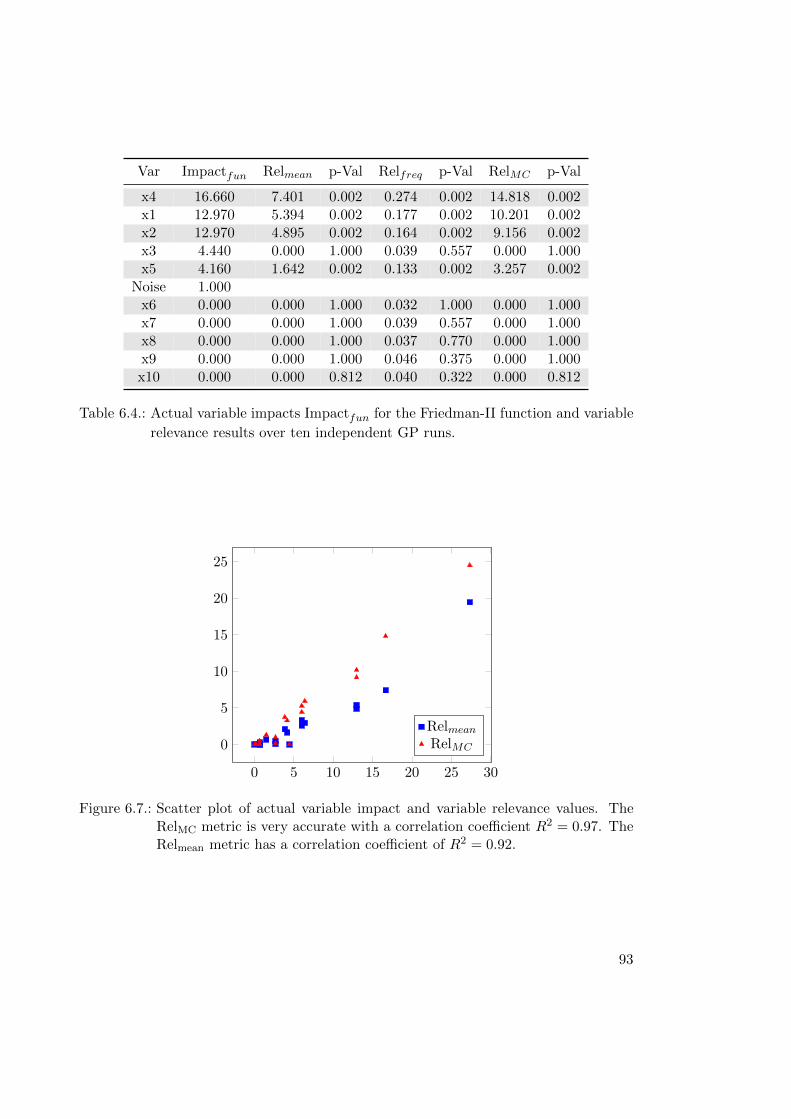

6.3. Data Mining and Symbolic Regression . . . . . . . . . . . . . . . . . . . . 95

6.4. GP-Based Search for Implicit Equations . . . . . . . . . . . . . . . . . . . 95

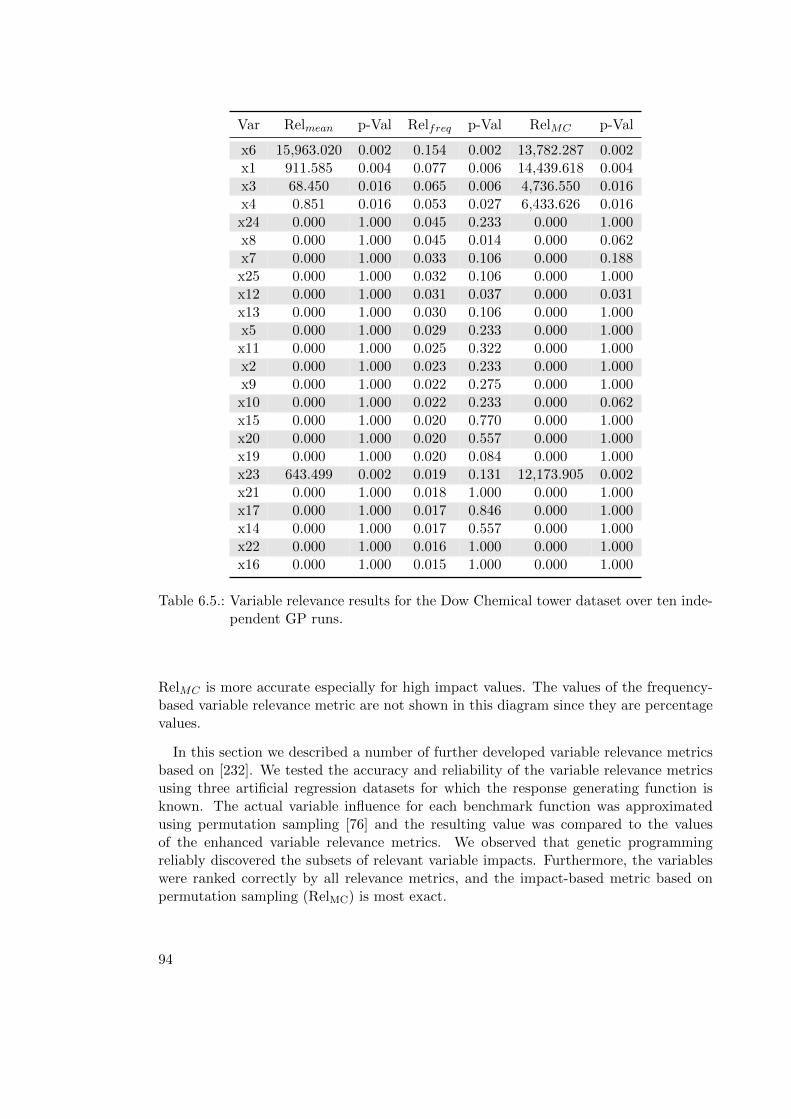

6.5. Comprehensive Search for Symbolic Regression Models . . . . . . . . . . . 96

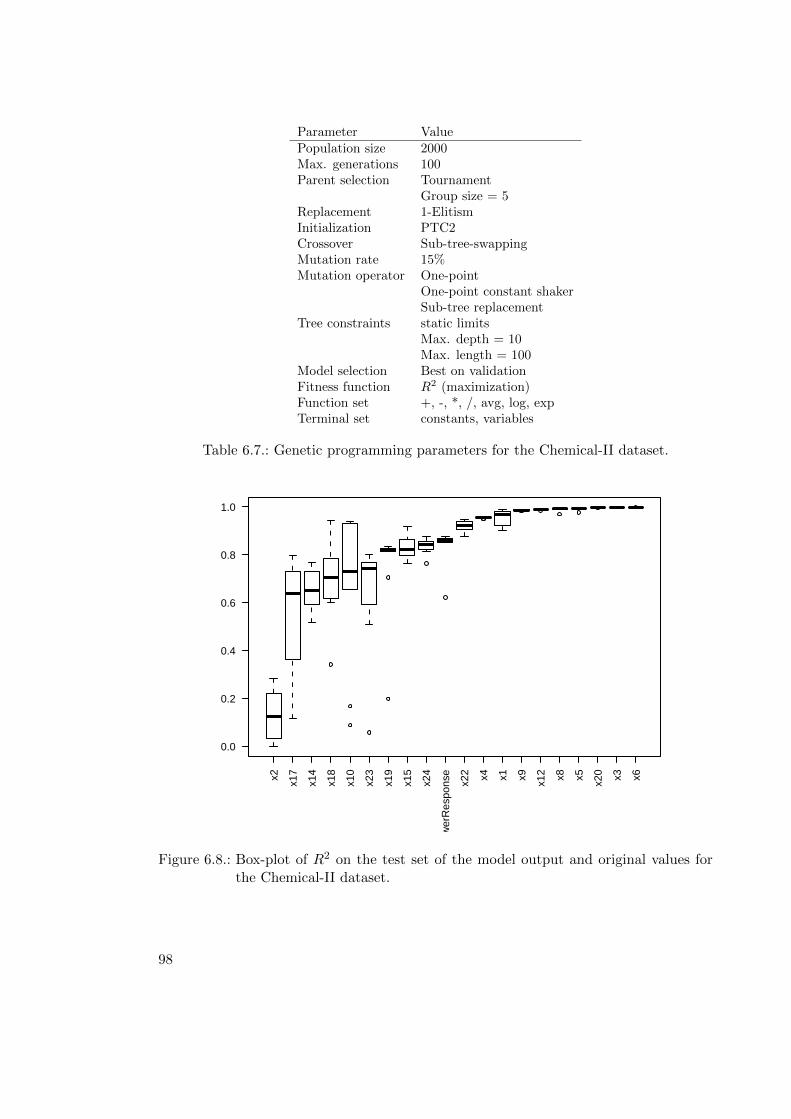

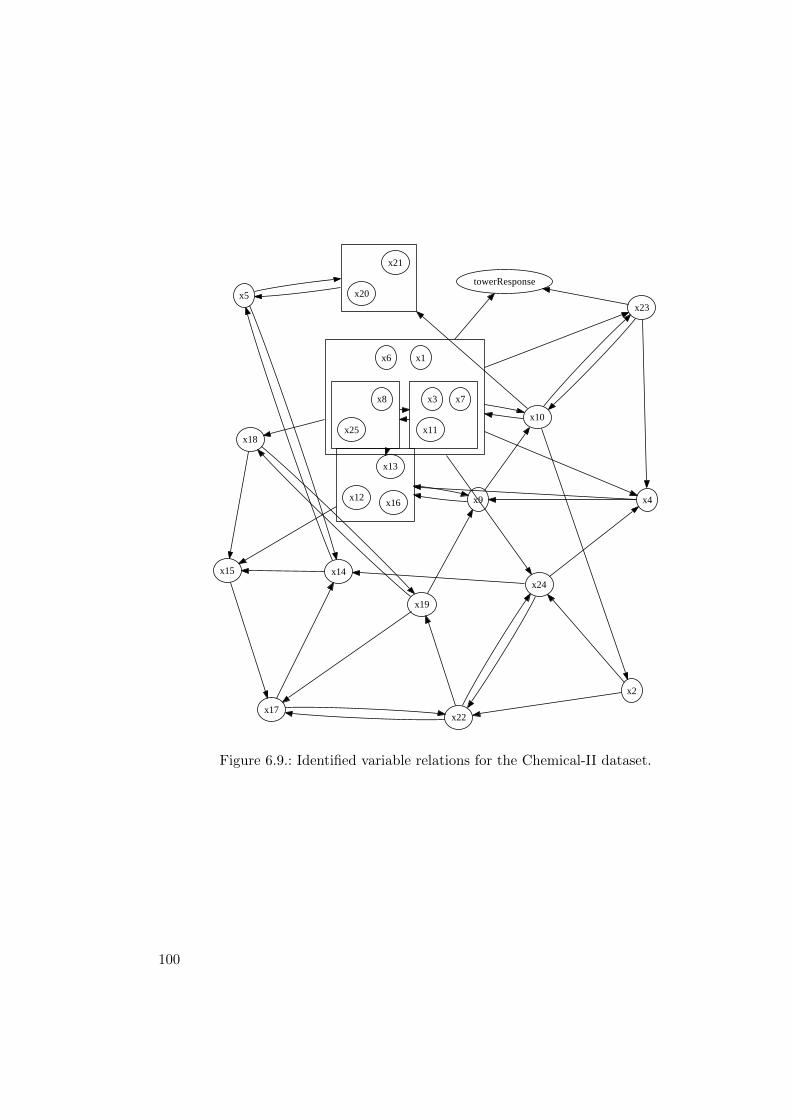

6.5.1. Case Study: Chemical-II Dataset . . . . . . . . . . . . . . . . . . . 96

6.6. Improving GP Performance . . . . . . . . . . . . . . . . . . . . . . . . . . 102

6.6.1. Parallelization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

2

6.6.2. Improving Fitness Evaluation Performance . . . . . . . . . . . . . 103

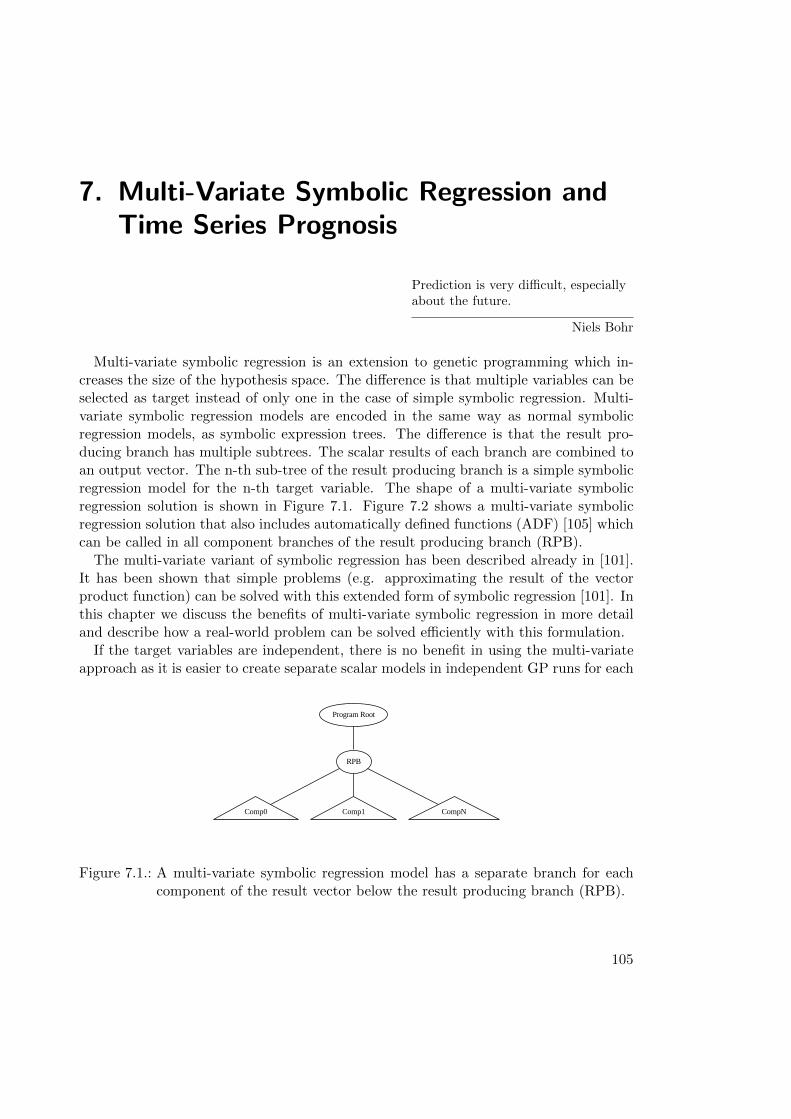

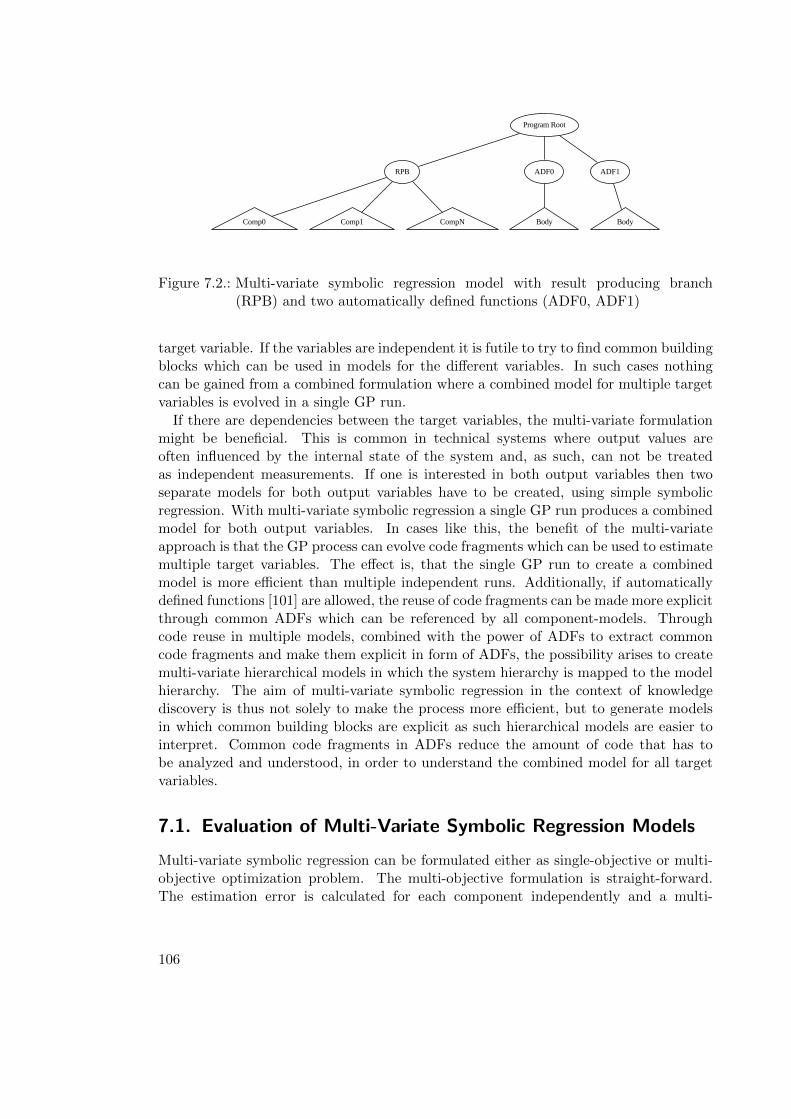

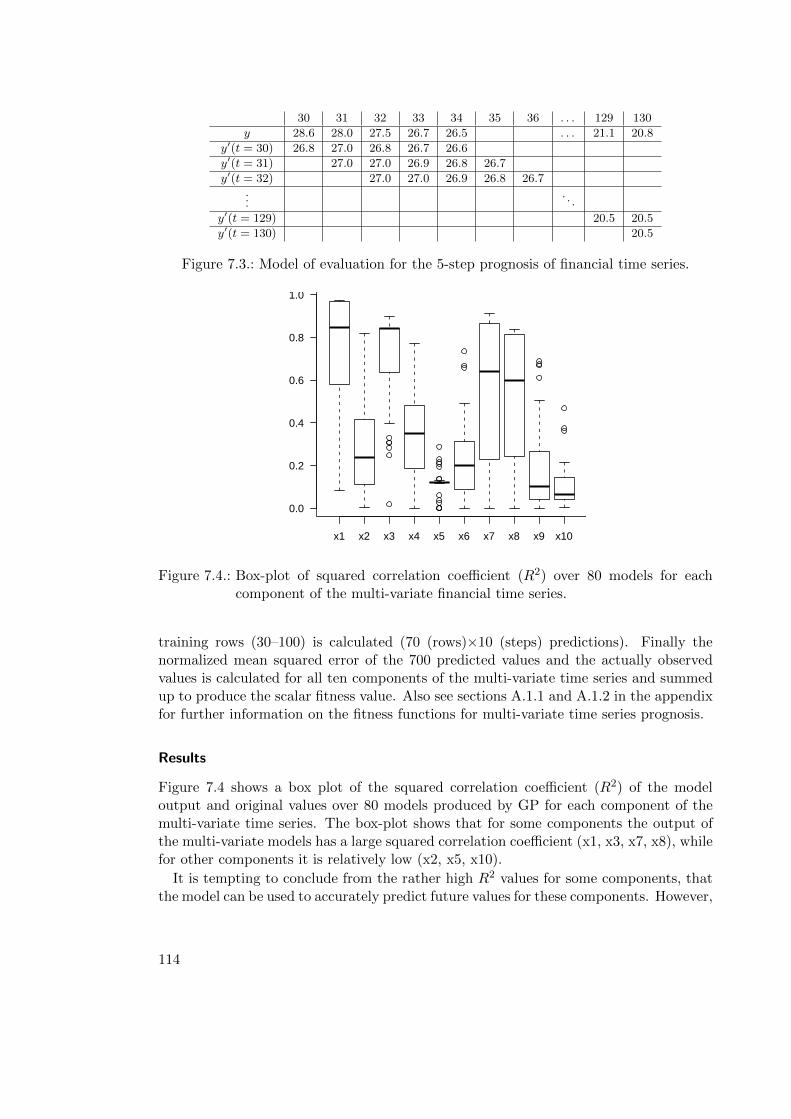

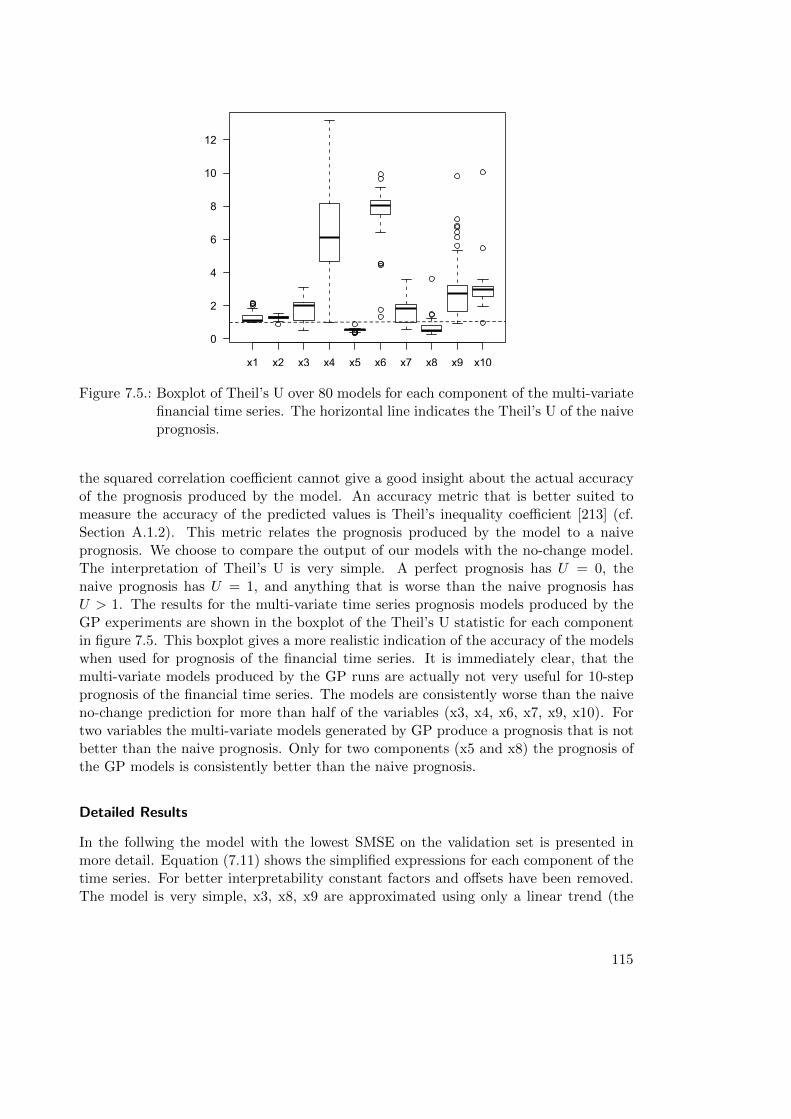

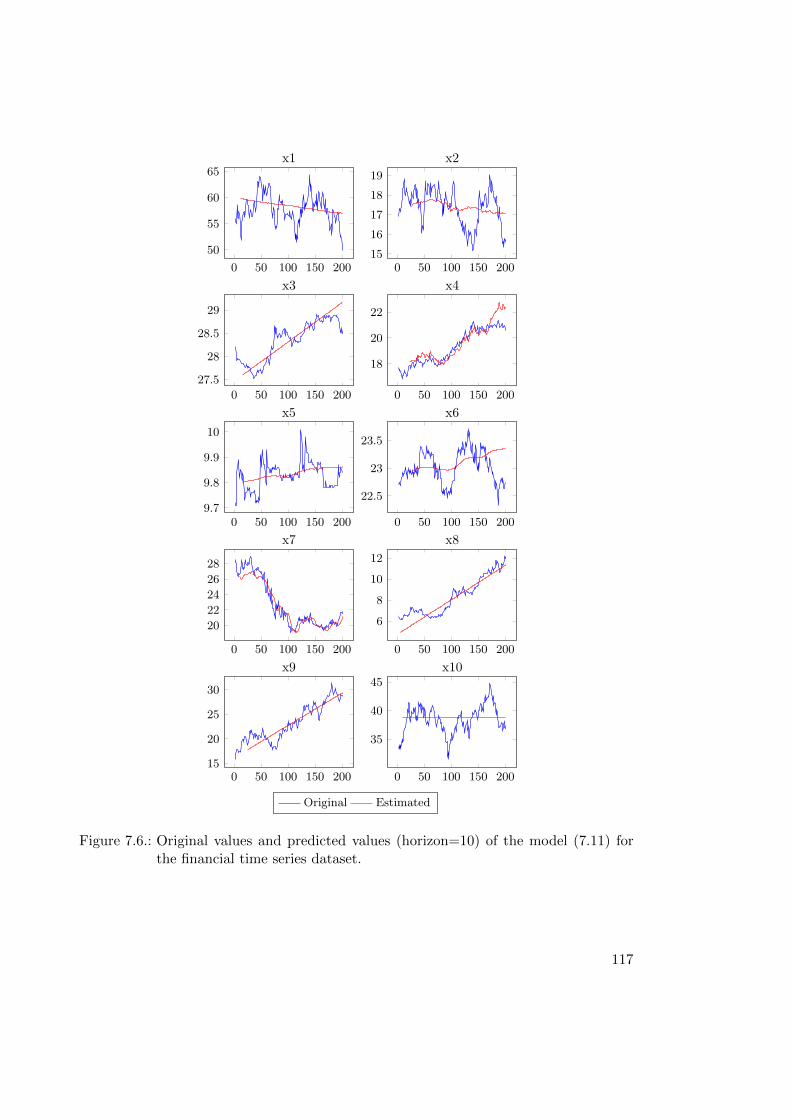

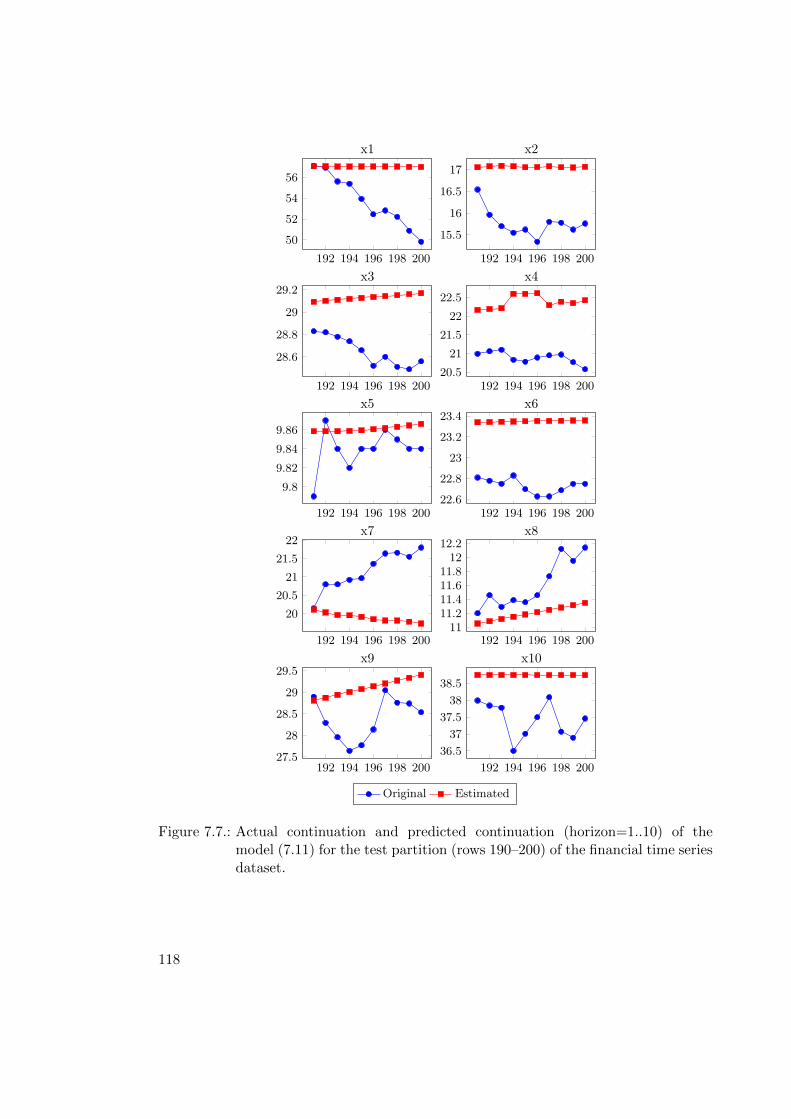

7. Multi-Variate Symbolic Regression and Time Series Prognosis 1057.1. Evaluation of Multi-Variate Symbolic Regression Models . . . . . . . . . . 106

7.1.1. Curse of Dimensionality . . . . . . . . . . . . . . . . . . . . . . . . 1087.2. Multi-variate Time Series Modeling and Prognosis . . . . . . . . . . . . . 108

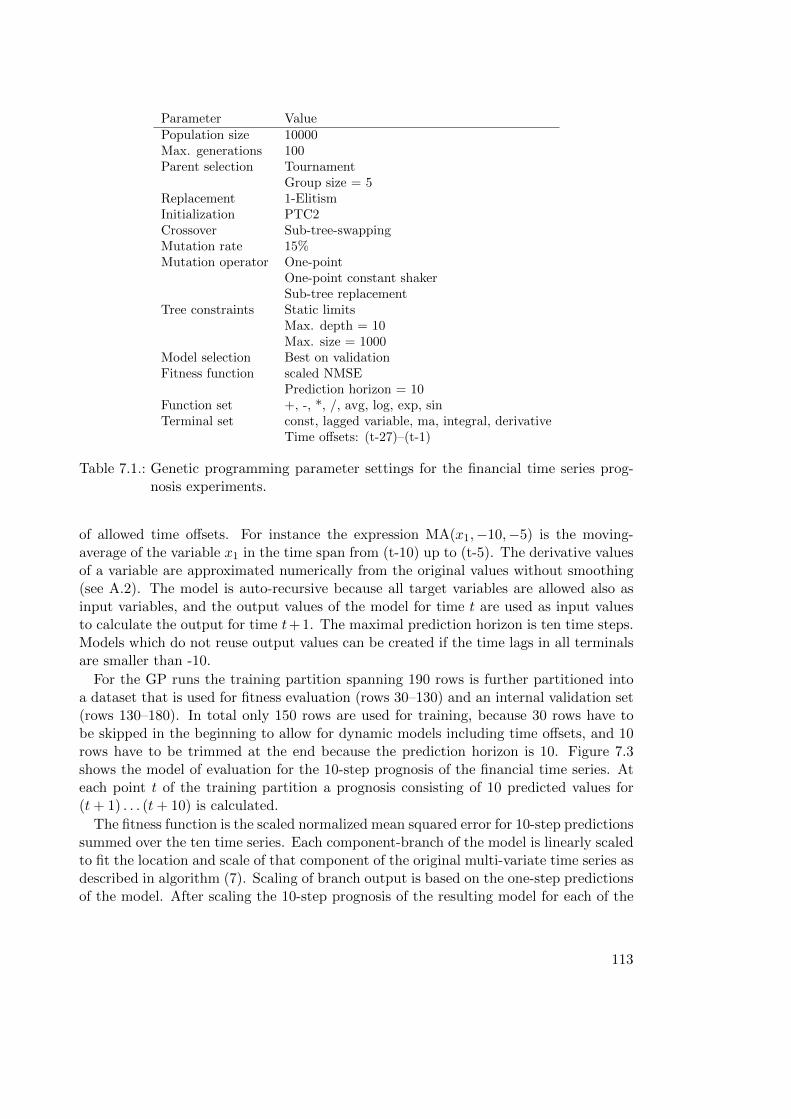

7.2.1. Evaluation of Multi-variate Time Series Prognosis Models . . . . . 1107.2.2. Case Study: Financial Time Series Prognosis . . . . . . . . . . . . 111

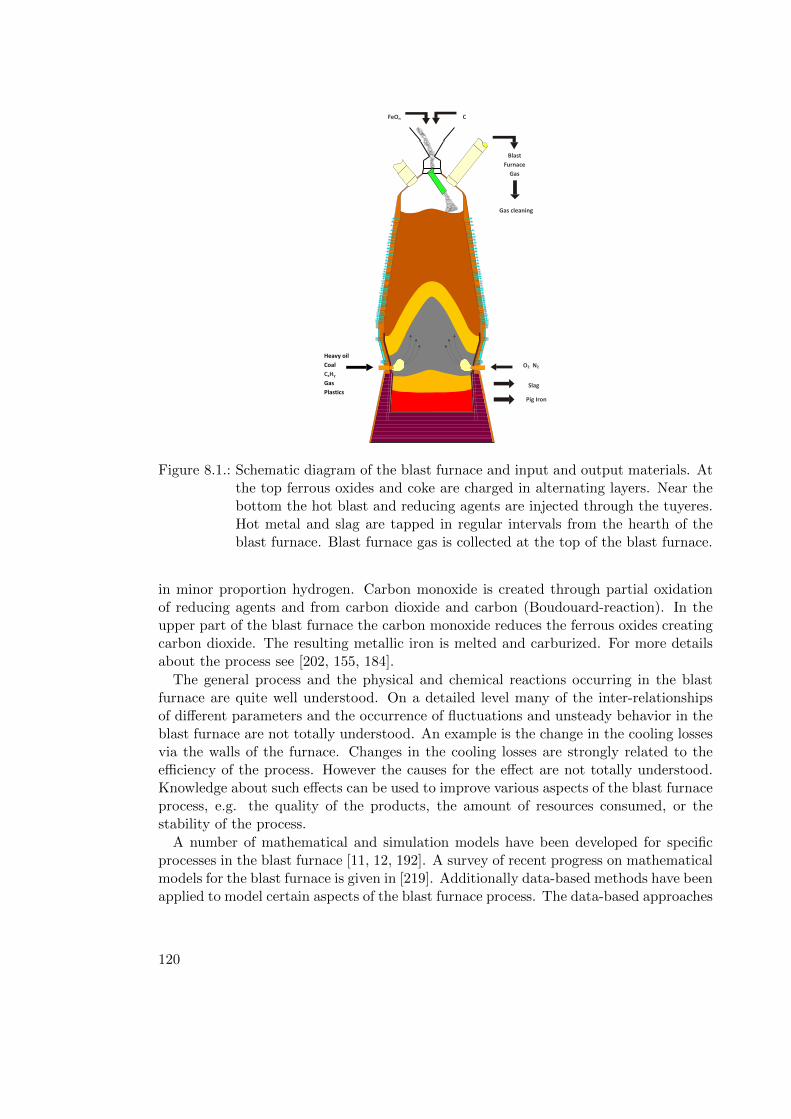

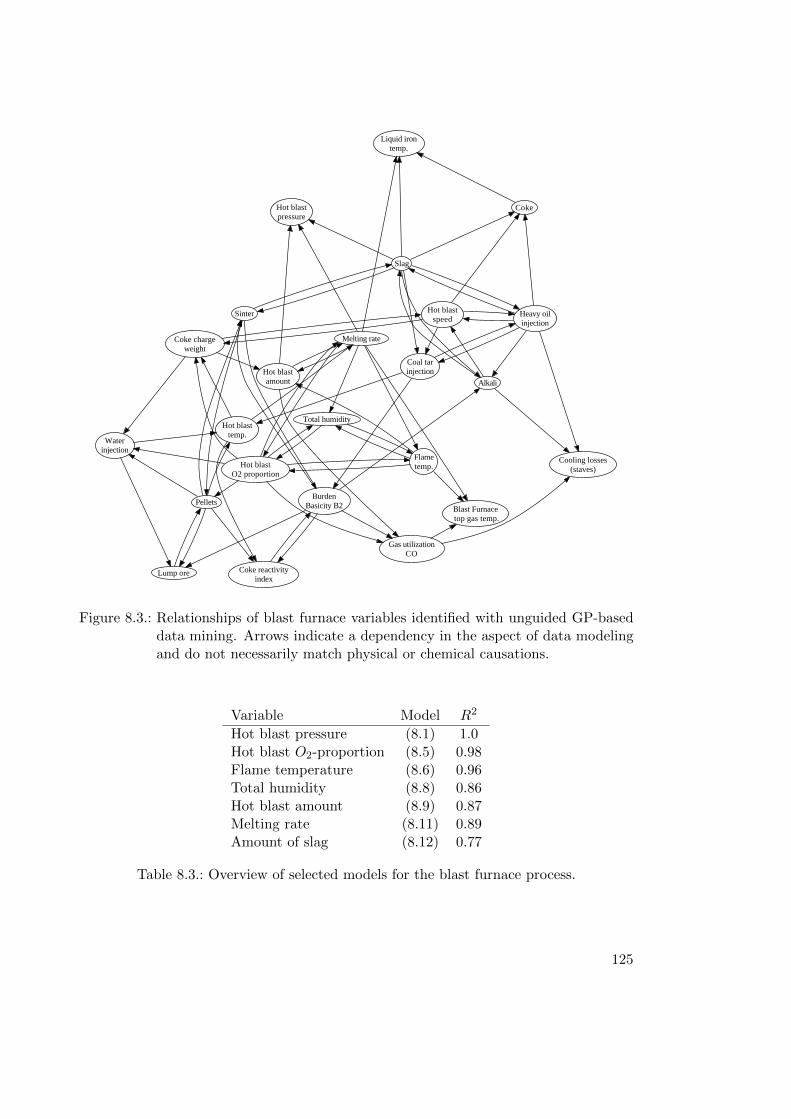

8. Applications and Case Studies 1198.1. Blast Furnace . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

8.1.1. Modeling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1218.1.2. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1218.1.3. Result Details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1248.1.4. Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . 130

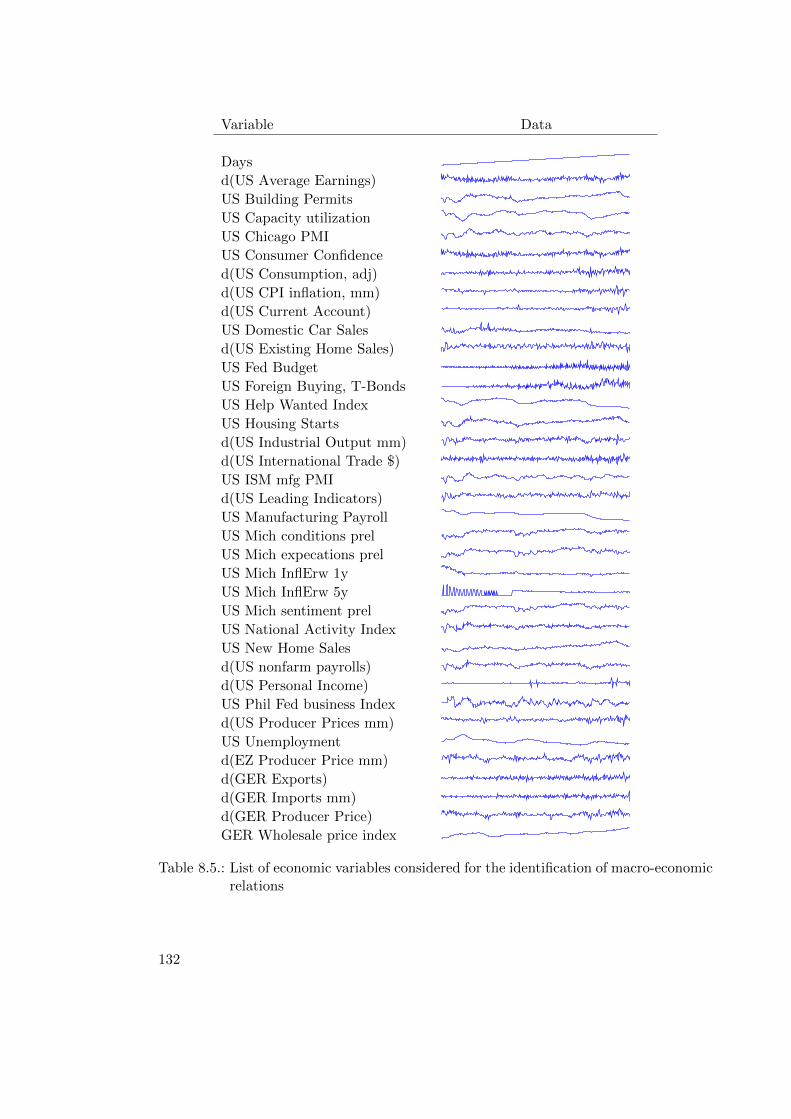

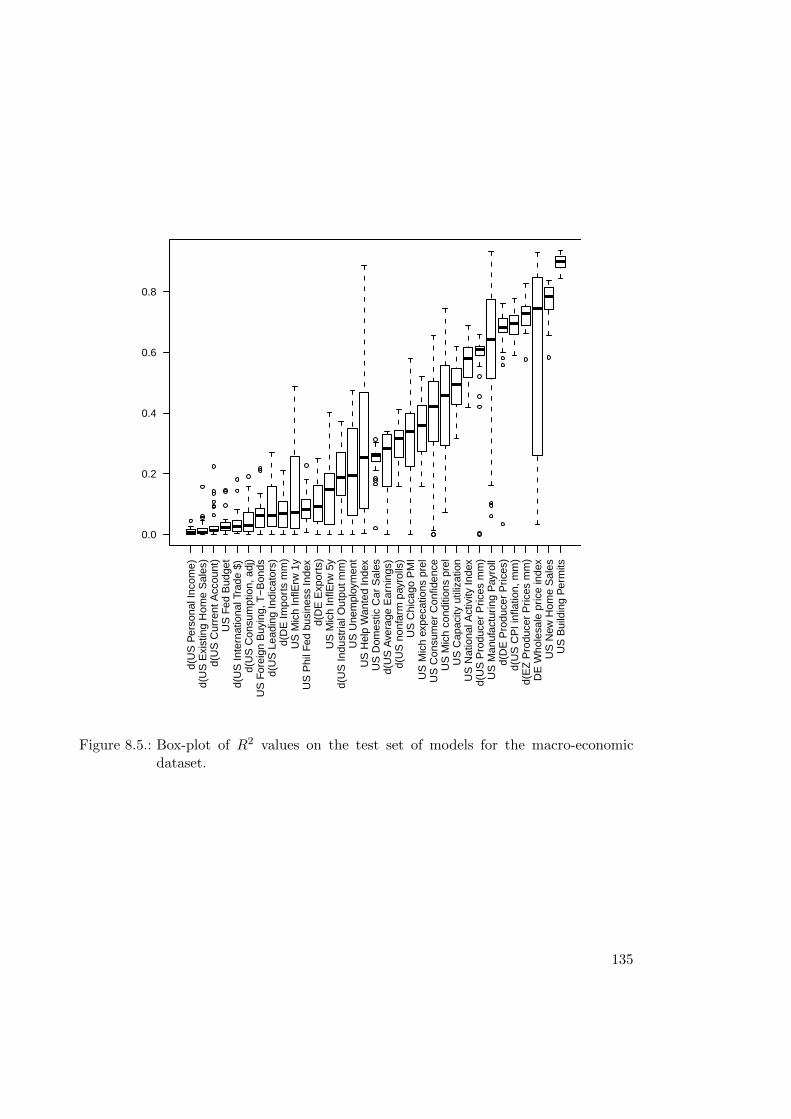

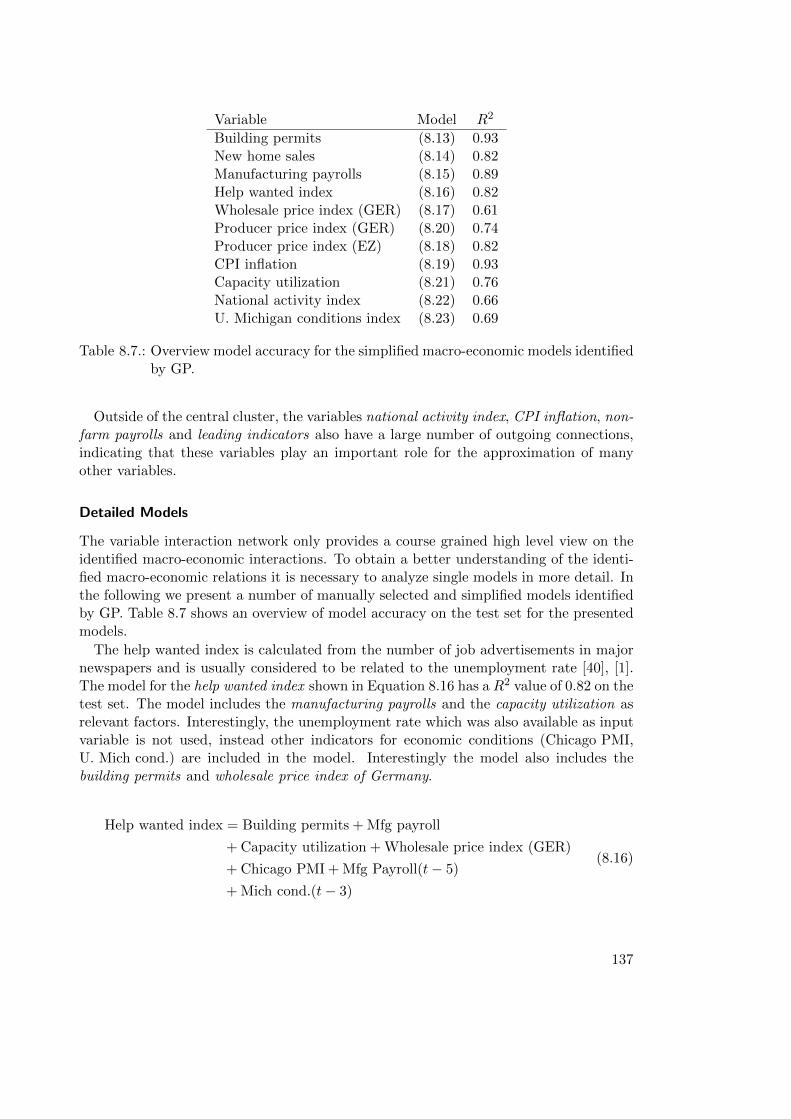

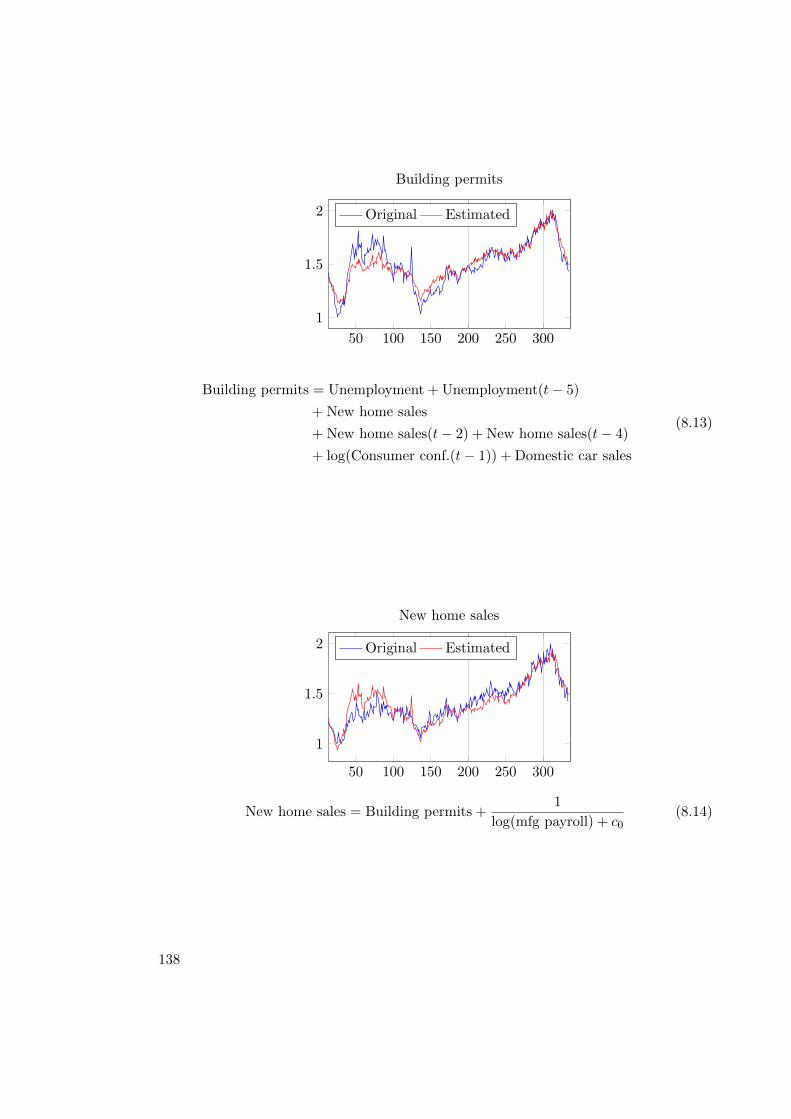

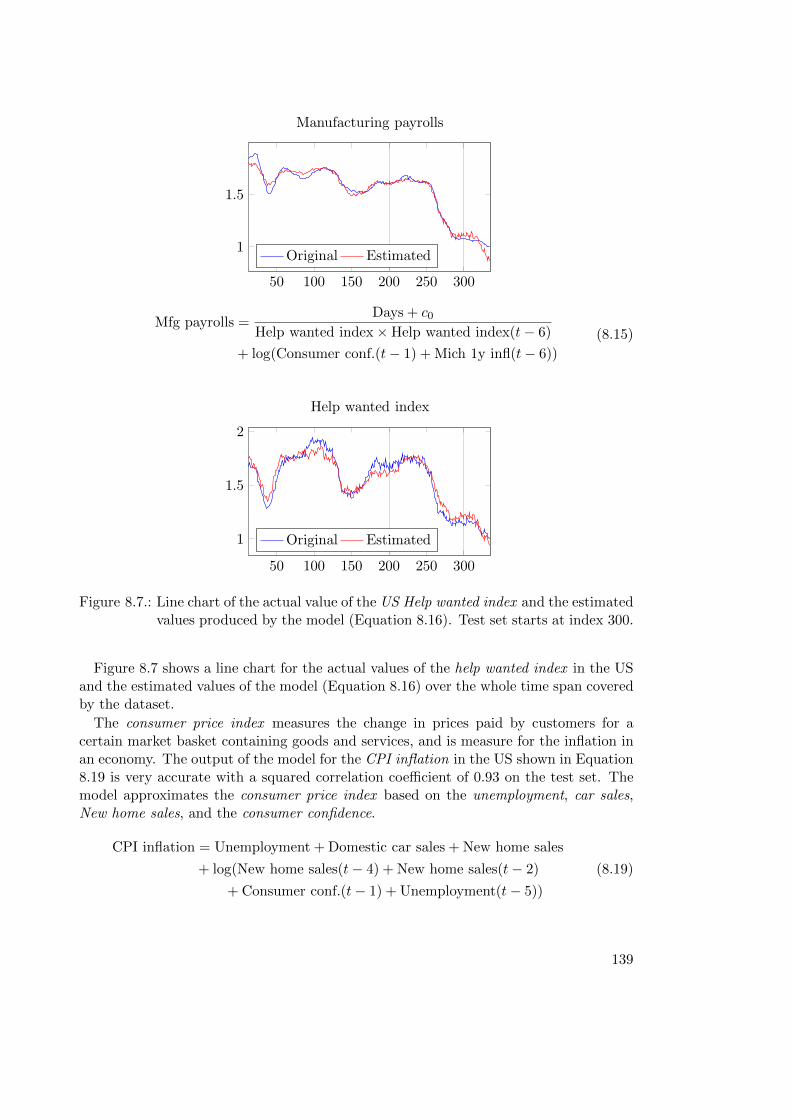

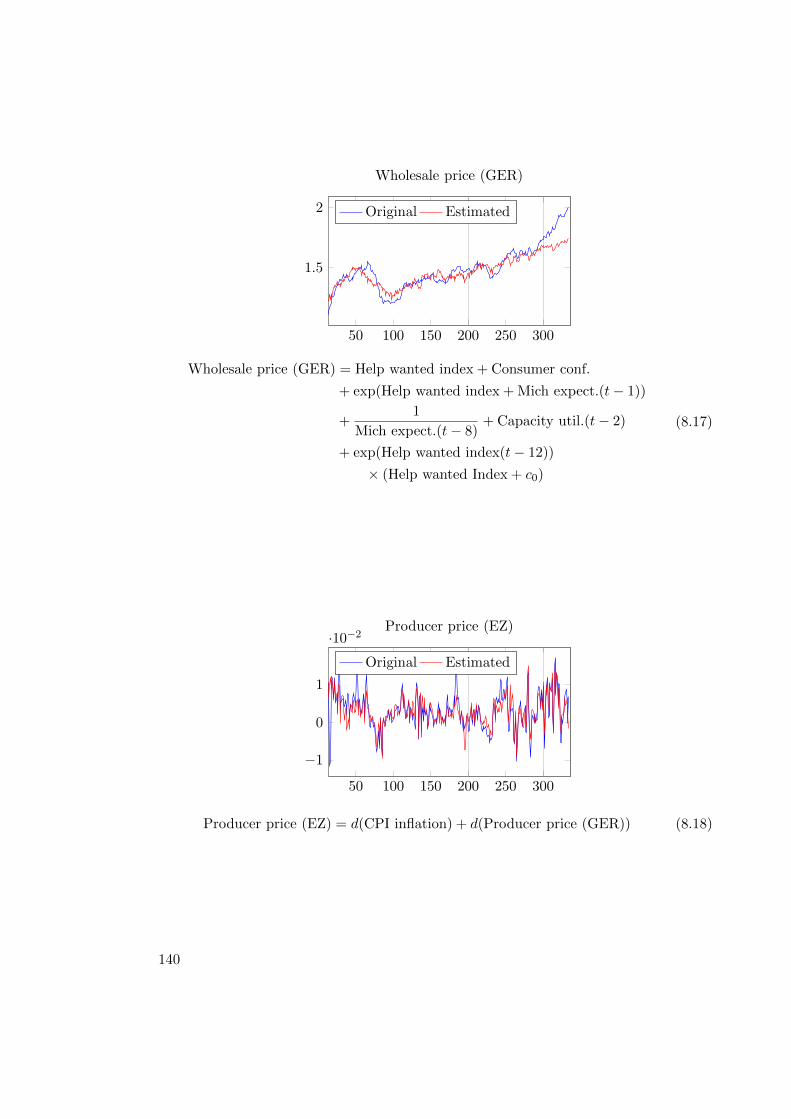

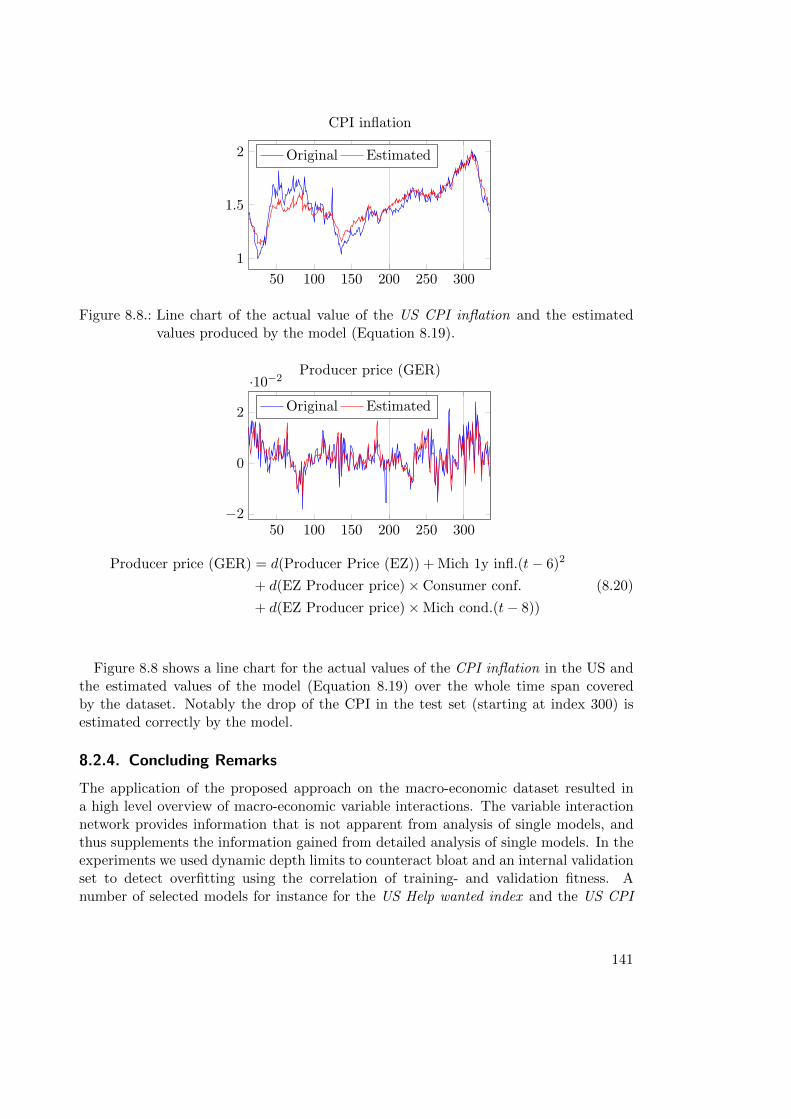

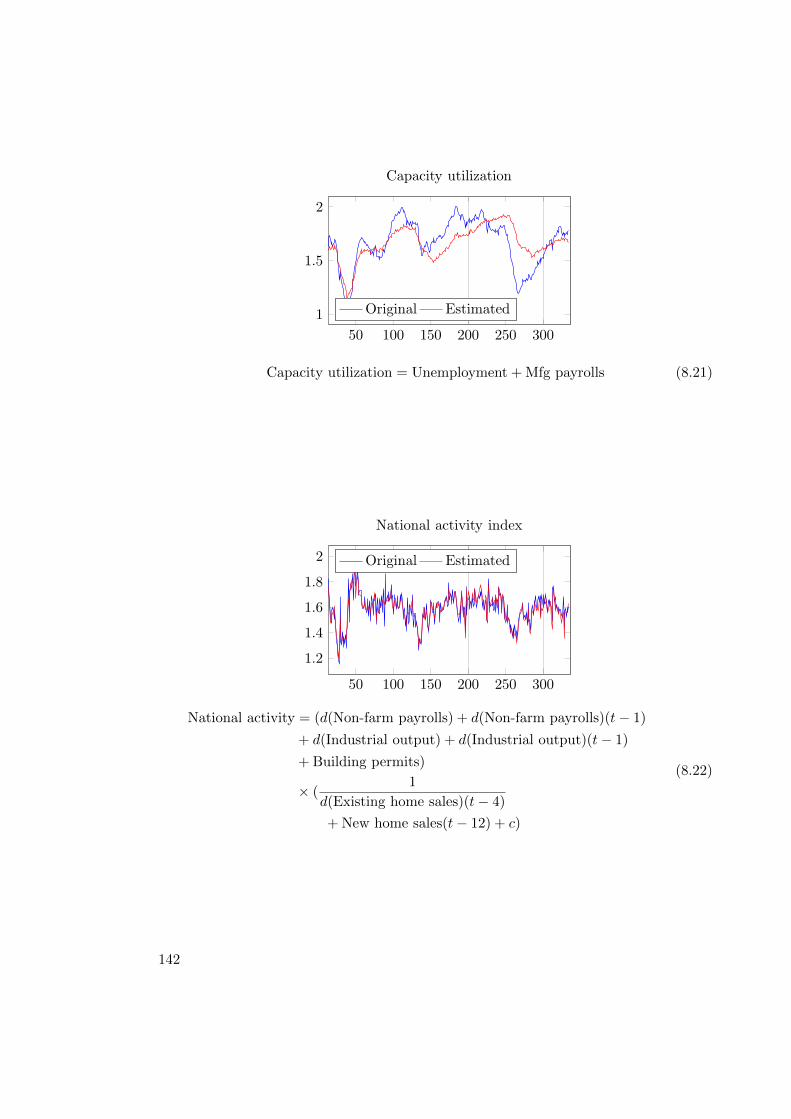

8.2. Econometric Modeling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1318.2.1. Macro-Economic Dataset . . . . . . . . . . . . . . . . . . . . . . . 1318.2.2. Modeling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1338.2.3. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1348.2.4. Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . 141

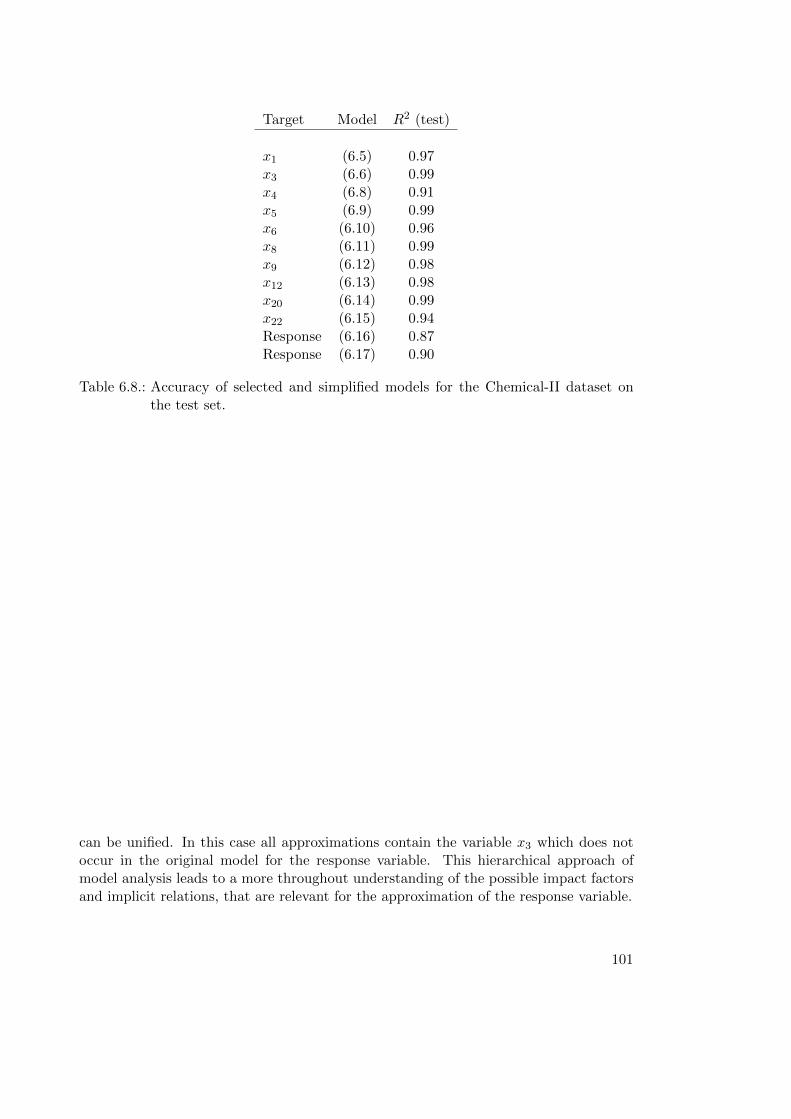

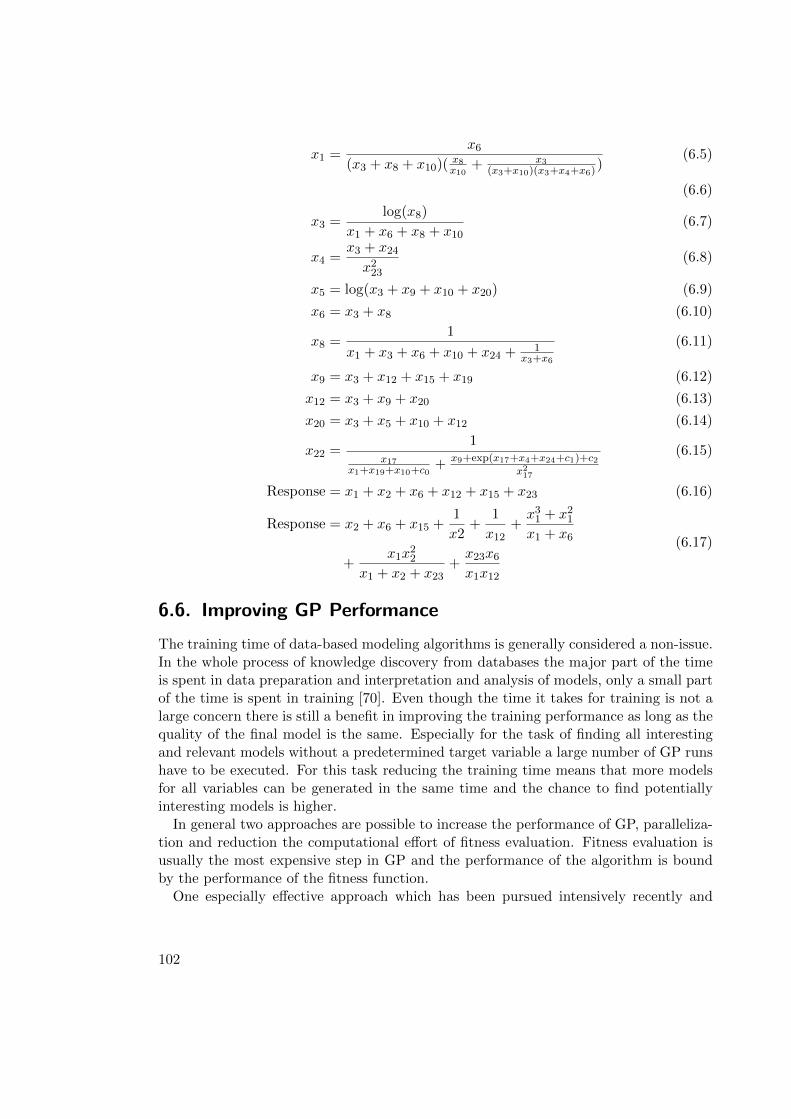

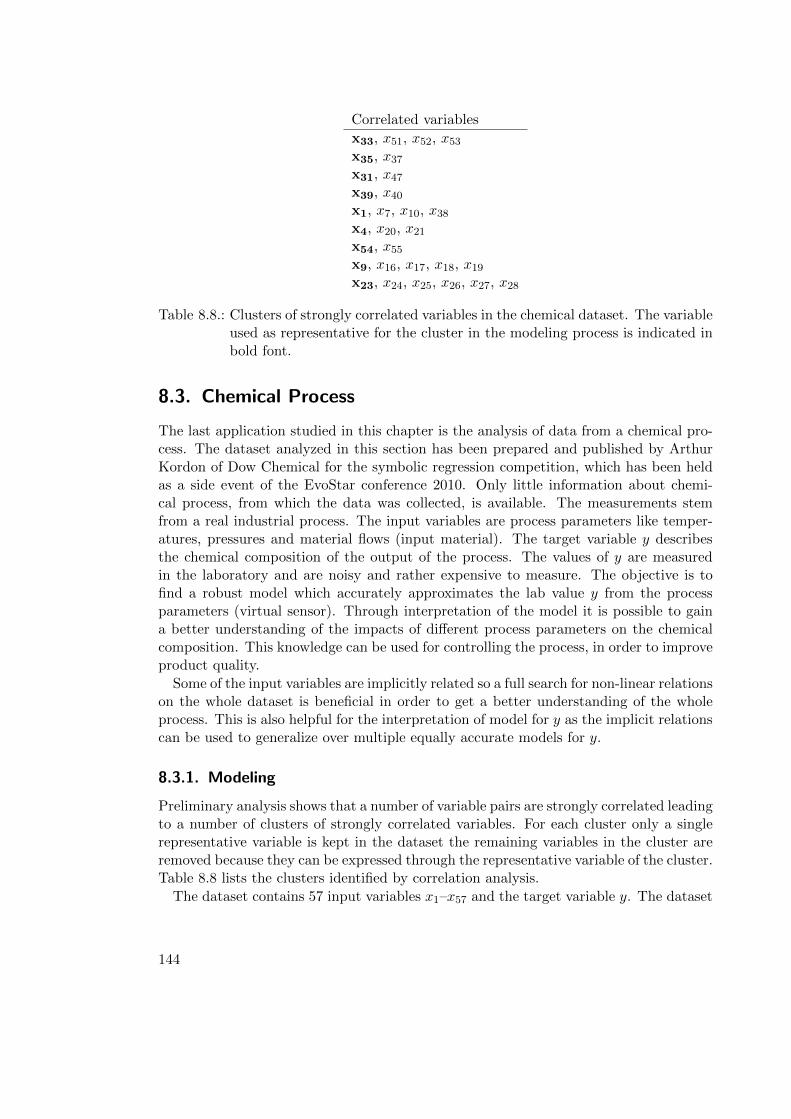

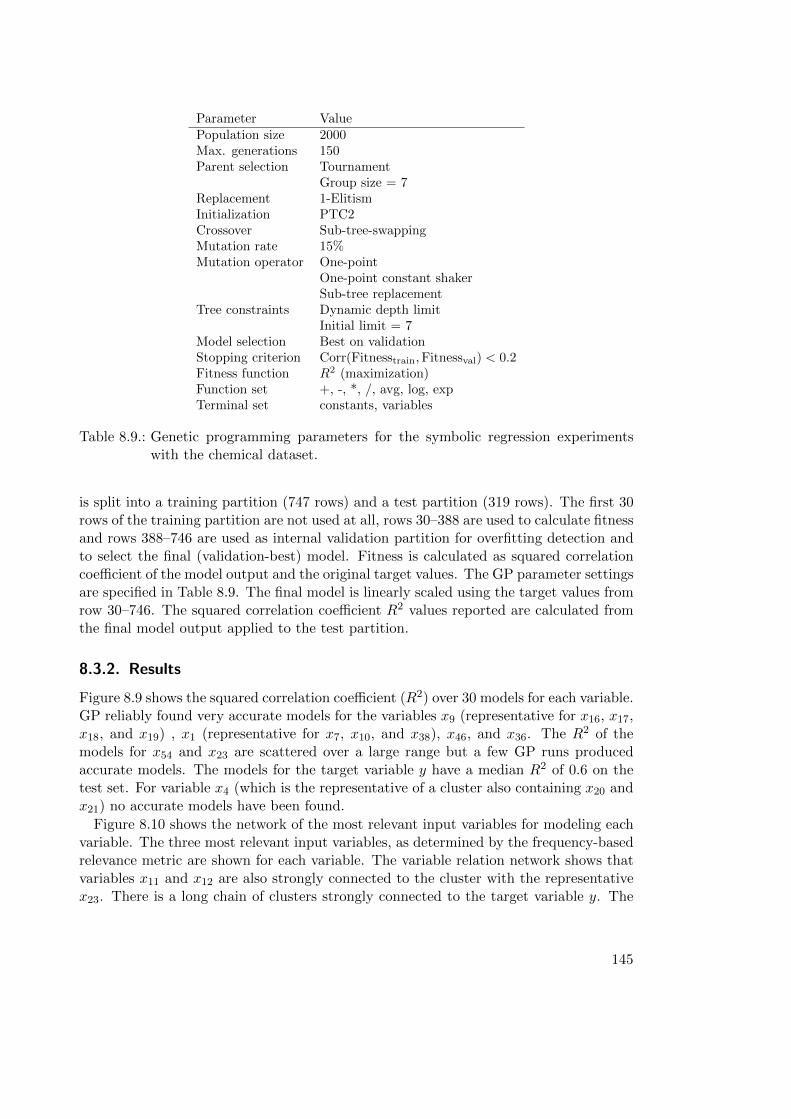

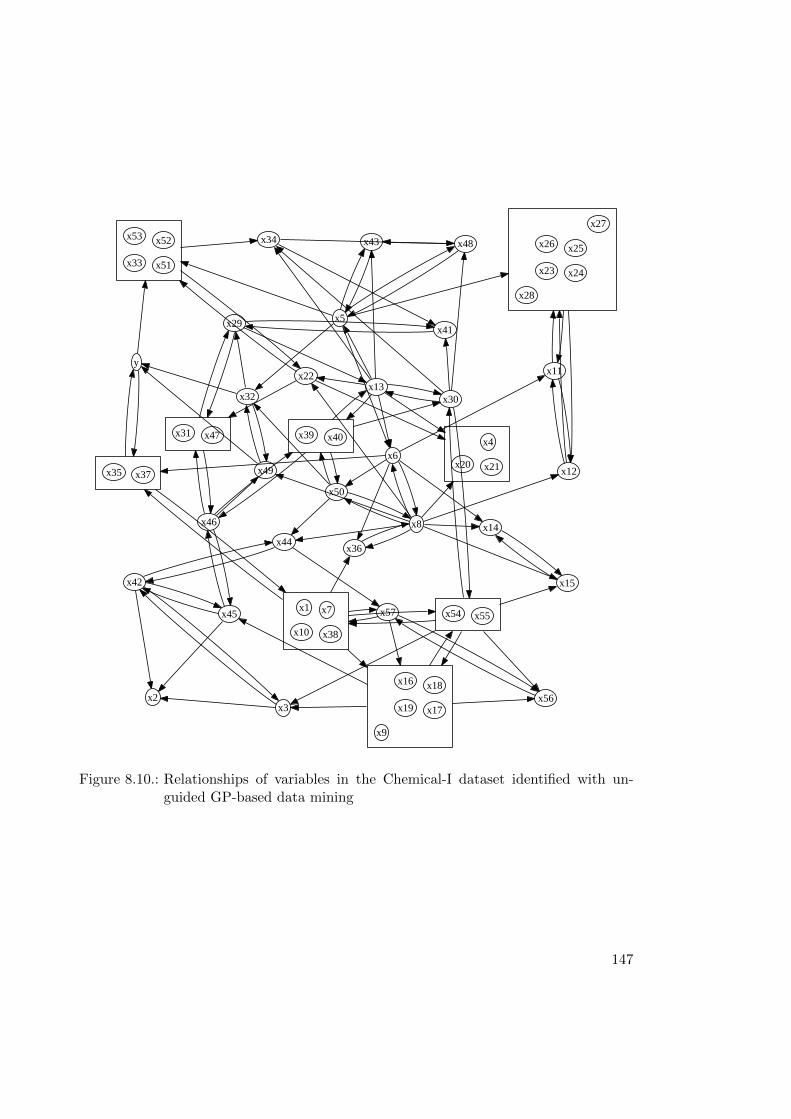

8.3. Chemical Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1448.3.1. Modeling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1448.3.2. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1458.3.3. Detailed Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

9. Concluding Remarks 151

A. Additional Material 155A.1. Model Accuracy Metrics . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

A.1.1. Regression Models . . . . . . . . . . . . . . . . . . . . . . . . . . . 155A.1.2. Time Series Models . . . . . . . . . . . . . . . . . . . . . . . . . . 158

A.2. Numerical Approximation of Derivatives . . . . . . . . . . . . . . . . . . . 161A.3. Datasets Used in Experiments . . . . . . . . . . . . . . . . . . . . . . . . . 161

A.3.1. Artificial benchmark datasets . . . . . . . . . . . . . . . . . . . . . 162A.3.2. Real World Datasets . . . . . . . . . . . . . . . . . . . . . . . . . . 163

A.4. Colophon . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 195

Bibliography 195

Curriculum Vitae 195

3

Overview

The main theme of this work is how genetic programming (GP) can be used for knowl-edge discovery. In particular, adaptations of GP to search for accurate, interesting,and understandable models are discussed. Additionally ways to filter and present theinformation gathered through GP runs are presented that aim to improve knowledgediscovery process and lead to a better understanding of the examined system or pro-cess. This work puts strong emphasis on producing comprehensible models with GP, theaccuracy of the output of the models is only secondary.

This work mainly concentrates on the practitioners view of GP and symbolic regres-sion. Thus the majority of this work is about practical aspects, theoretic aspects areonly treated briefly. GP theory has seen a lot of progress in the recent years. Thesecontributions are very relevant for a better understanding of the internal dynamics of GPand provide a solid basis on which to conduct empirical or practically oriented research.

The main advantage of GP compared to other data-analysis methods is that it pro-duces white-box models that might lead to new knowledge about the examined system.The price to pay for this is that GP also requires more computational resources thanother data-analysis methods. The internal dynamics of genetic programming often leadsto final solutions that are relatively complex and hard to understand. In the literaturea large number of possible remedies for this issue have been described and analyzed,however, from a practitioners point of view the results are not satisfactory. In the firstpart the following novel concepts are presented:

• Comprehensive GP-based identification of interesting models or interactions in agiven data-set.

• Data-based methods to quantify and visualize relevant interrelations of variablesof a system.

The following issues relate to the main objectives and are also discussed in the first part:

• Methods to create compact and comprehensible models with GP.

• Methods to detect and avoid overfitting with GP.

• Symbolic vector-regression for the identification of multi-variate models.

• GP-based time series modeling for prognosis.

In the second part the concepts described in the first part are applied to a number ofreal world data mining problems.

5

1. Introduction

Well organized and accurate data have become increasingly important as a potentialsource of profits for businesses. As more and more data are generated and stored inlarge repositories the desire to generate value from the available data grows. Businessintelligence as a discipline is intimately related to the collection, aggregation and analysisof business-relevant data. Decision support systems play an important role in businessintelligence to analyze and summarize relevant data often in form of charts and condensedreports. The main purpose of decision support systems is to support managers to makecorrect profitable decisions. Decision support systems of various complexity are alreadyubiquitously implemented in many areas (politics, finance, health, industries...) andhave an impact on our everyday life.

A large number of data-analysis methods for different applications have been describedranging from very simple methods to mathematically complex and powerful algorithms.The methods can be categorized in one or multiple of the following partially overlappingdisciplines: System theory, statistics, machine learning, and data mining. All these dis-ciplines have in common that they cover the topic of data-based modeling [124, 72, 27].Additional research areas related to these disciplines are artificial neural networks andreinforcement learning [210]. “Artificial neural networks are a development of the Per-ceptron [173] [. . . ] and the area has transformed into a community of its own [...]. Thisis quite remarkable, since the topic is but a flexible way of parameterizing arbitrary hy-persurfaces for regression and classification. The main reason for the interest is thatthese structures have proved to be very effective for solving a large number of nonlinearestimation problems.” [124]. Recently a number of novel contributions have been pub-lished discussing learning for so-called deep networks with very many hidden layers forwhich back-propagation learning algorithms do not work well [85, 60, 132].

Data mining includes a wide range of different techniques to analyze, filter, exploreand visualize data [79, 233]. Fayyad et al. define data mining in the following way: “Datamining is the application of specific algorithms for extracting patterns from data” [61].Another definition is given by Hand et al.: “Data mining is the analysis of (often large)observational data sets to find unsuspected relationships and to summarize the data innovel ways that are both understandable and useful to the data owner.” [79]. Based onthese definitions many data-based modeling approaches can also be called data miningmethods. Data mining also includes exploratory elements like drilling down into inter-esting facts in an interactive cyclic process of model construction and interpretation.Fayyad et al. define data mining as a step in the process of knowledge discovery fromdatabases. The whole process also includes data selection, preprocessing and trans-formation as necessary preparatory steps for data mining and the interpretation andevaluation of the results obtained from data mining as a necessary follow up step to

7

achieve the stated goal of knowledge discovery. An essential requirement for effectivedata mining is that results are presented in a clear and informative way in order to allowa data miner to evaluate and interpret the results easily. Methods and principles forthe visual display of quantitative data [217, 218] are closely related to data mining andknowledge discovery.

This work concentrates on the application of genetic programming for data mining ofdata collections that fit entirely into main memory. In particular, this work does notcover issues and solutions related to very large data collections that must be read sequen-tially from external memory. Genetic programming is a nature inspired meta-heuristicwhich is applicable to a wide range of problems in its general formulation. The idea ofGP is to imitate aspects of biological evolution such as selection, recombination, andmutation for find computer programs that solve a given problem in small evolutionarysteps starting with an initial population of random programs. Genetic programming inits most general formulation can be called an “invention machine” [104, 105]. In mostcases, however, problem-specific variants of GP are used to solve well defined problems.One example for a specific and rather simple GP approach is symbolic regression; inthis application GP is used to search for models that can be represented as symbolicexpressions and approximate the response of a system based on observations of the inputand output behavior of the system. Symbolic regression relies on the power of GP tofind the correct structure for the model in combination with the model parameters. Thisproperty makes GP especially suitable for data-analysis tasks where only little informa-tion about the origin of the data and the examined system is available. Multiple authors[94, 232, 3, 231, 191, 126, 174, 18] have demonstrated that problem-specific GP variantsfor data-analysis can find very good solutions for specialized tasks like regression andclassification. A more general approach is introduced in [154] which uses GP to generateclassification algorithms which can later be executed to produce classifiers based on aspecific data-set.

The general formulation of GP has the drawback that it often takes more computa-tional effort to achieve solutions of comparable accuracy than it would take with othermore specific methods. This disadvantage is often accepted as the time spent for modeltraining is usually not critical. The time spent for training is often only a small partof the total time spent in the knowledge discovery process. A major part of the timeis spent on data preparation and model interpretation and analysis [70]. If genetic pro-gramming is to be used to search for interesting patterns in large datasets it is beneficialif the training time can be reduced as more potentially interesting patterns can be un-covered in the same time frame. The chance to find previously unknown interrelationsin the data grows with the number of good models. In Section 6.6 we describe methodsto increase the training performance of GP that do not have a negative effect on themodel accuracy.

Data analysis methods can be classified based the representation of models producedby the method. The spectrum ranges from comprehensible white-box models on the oneend to complex black-box models on the other end. Often the distinction is not clearand various shades of gray-box models are located in between the two extremes. Modelsproduced by symbolic regression are located near the white-box end of the spectrum.

8

Typically symbolic regression models are mathematical expressions which can be directlyinterpreted in order to gain knowledge about the patterns which were found in thedataset. Support vector machines are an example for an approach that produces black-box models located on the other end of the spectrum. Artificial neural network modelsare usually said to be gray-box models because the network structure can be interpretedbut it is hard to gain a full understanding of the interrelations in the network.

While the fact that GP produces white-box models is often stated as an advantagethis is often not apparent in practice. The models presented as final result is oftenrather complex and difficult to understand. Even though the model is a mathematicalexpression it is often impossible to gain an understanding of the model when it containsdeeply nested functions. This problem is also a major topic in [94] which discusses theapplication of genetic programming for scientific discovery. One cause for this is thatgenetic programming has the tendency to build ever larger and more complex programsover time without a proportional improvement in program fitness. In the GP communitythis phenomenon is called code bloat and a lot of effort has been put into designingcounter-measures that reduce or prevent this behavior. In Chapter 4 this phenomenonand a few selected counter-measures will be described in more detail. Even though anumber of counter-measures has been described in the literature [188] there is not yet aconsensus which methods are effective in practical applications. If symbolic regressionis used for an unguided search for interesting patterns in a dataset then an effectiveanti-bloat strategy is very important because only small and at the same time accurateand generalizable models are interesting as a source for new insights into the nature ofthe dataset.

Another reason why it is important to create compact, comprehensible models is thatthe data miner is more likely to trust a model to be true when it is understandableand and easy to validate. The issue of models which can be trusted should not beunderestimated [99] as it is the first and foremost criterion that a data miner trusts themodel before the model is examined in more detail. Demonstrating that a model canbe trusted is even more important than the accuracy of the model. Models that are tooaccurate to be true might raise concerns that the model might be over trained and thuscannot be trusted (for a more detailed discussion of overfitting see Chapter 5). One wayto increase the chance that a model is trusted is to reduce the complexity of the model,making it easier to validate and analyze the model. Another way is to demonstrateclearly that the model also is accurate on new data, for instance through validation ona hold-out set or through cross-validation. Even though such validation methods arecommon practice in the machine learning community these standards are not yet fullyimplemented in the evolutionary computation community [59]. In a recent contributionO’Neill et al. state that: “[...] this issue in GP has not received the attention it deservesand only few papers dealing with the problem of generalization have appeared [...]” [148].

In the original formulation of symbolic regression with genetic programming a singlevariable must be explicitly declared as the target variable [101]. However, often it is notimmediately clear which variable is the variable of interest or there are multiple variablesthat could be declared as a target variable. So it is often necessary to explore the optionswith multiple symbolic regressions runs with different configurations.

9

Another data mining task that is relevant in practice but has not yet been treatedextensively in the GP literature, is multi-variate symbolic regression. In this approachGP has to find a symbolic multi-variate regression model that approximates all targetvariables. If GP is to be used for unguided data mining without an explicit target variablethe solution representation and the search process of genetic programming have to beextended. In Chapter 6 a simple approach of independent runs to create and collectmodels for all variables of the dataset is described. In Chapter 7 several extensionsof the solution representation for the simultaneous modeling of multiple variables aredescribed.

1.1. Thesis Statement

To summarize the previous paragraphs genetic programming can be used for data min-ing to find potentially interesting patterns or interactions in large datasets when thetraditional symbolic regression approach is extended and adapted appropriately.

• Solution representation: Instead of a single target variable the process shouldidentify the potentially interesting variables automatically. This work describesseveral different ways to extend the solution representation for data mining tasksand introduces ways to manage the potentially large set identified models.

• Model complexity and presentation: In order to facilitate knowledge discovery fromGP models, appropriate and effective methods for reduction of model complexityhave to be integrated into the search process. This work describes different methodsto reduce the model complexity and introduces new ways of visualizing results tosimplify detailed analysis of models.

• Trustable models: Results presented by the process must be clearly validated toenable the data miner to estimate how trustable a model is. This work describes avalidation procedure for GP that is effective in practical applications and describeshow visualizations can be used to improve the trustability of models.

• Performance: In order to make unguided search for interesting patterns in largedata sets feasible it is necessary to reduce the training time of GP. In this workbriefly discusses possible ways to increase GP performance.

Chapter 2 gives a cursory introduction of machine learning and data mining includingcommonly used terms. Chapter 3 discusses relevant previous work in the area of evo-lutionary algorithms in general and genetic programming specifically. Chapter 4 is thefirst core chapter of this thesis and discusses the problem of bloat and countermeasuresto reduce bloat and also describes ways to simplify solutions with pruning. Chapter 5introduces an effective way to detect overfitting and countermeasures against overfittingin GP. Chapter 6 describes unconstrained GP-based search for interesting models andhow the information collected in those experiments can be prepared and visualized toimprove the knowledge acquisition process. In Chapter 6 the topic of variable relevance

10

metrics is discussed as it is necessary for the representation of variable relation networks.Chapter 7 describes an approach to create multi-variate symbolic regression models withGP and how multi-variate auto-regressive time series models can be used for the progno-sis of future values of a multi-variate time series. Finally, Chapter 8 demonstrates howthe methods discussed in the previous chapters can be applied to real world applications.

1.2. Research Project Background

This thesis mainly reflects research work done within the Josef Ressel-center for heuristicoptimization “Heureka!” at the Upper Austria University of Applied Sciences, CampusHagenberg. The center “Heureka!” is supported within the program “Josef Ressel-Centers” by the Austrian Research Promotion Agency (FFG) on behalf of the AustrianFederal Ministry of Economy, Family and Youth (BMWFJ).

11

2. Machine Learning and Data Mining

Essentially, all models are wrong, butsome are useful.

George Box

This chapter gives a brief overview of the disciplines of machine learning and datamining. A number of terms frequently in the machine learning literature that are nec-essary to understand the core of the work are explained in the following sections. Thereader who is already familiar with machine learning can skip this chapter and advanceto the chapter.

Learning is the process of knowledge acquisition from observations. Knowledge is de-fined by the Oxford Dictionary of English as: “(i) facts, information, and skills acquiredthrough experience or education; the theoretical or practical understanding of a subject;(ii) the sum of what is known; (iii) information held on a computer system.” [152]. Oneof the goals of machine learning as a research discipline is to define algorithms whichwhen executed by a computer enable it to learn general facts from examples in sucha way that previously unseen examples can also be recognized and a correct action istriggered.

As such the knowledge learned by the machine learning method should be specific torecognize known examples and general to also recognize slightly different new examples.In statistics the learning or training phase is called model estimation. Model estimationis the process of selecting a specific model from a class of models that fits the availabledata best.

Typically a discrimination is made between the two terms features and variables. Inmachine learning the term variable usually indicates the original variable while a featurecan be a combination of multiple variables. Often kernel functions are used to transforma combination of variables to features. In this work no distinction between the two termsis made and the terms variable and feature are used interchangeably.

2.1. Supervised Learning and Unsupervised Learning

Learning methods can be categorized into two general classes: supervised and unsuper-vised methods. The methods have different goals and are also different by the way howexamples are presented in the training or learning phase.

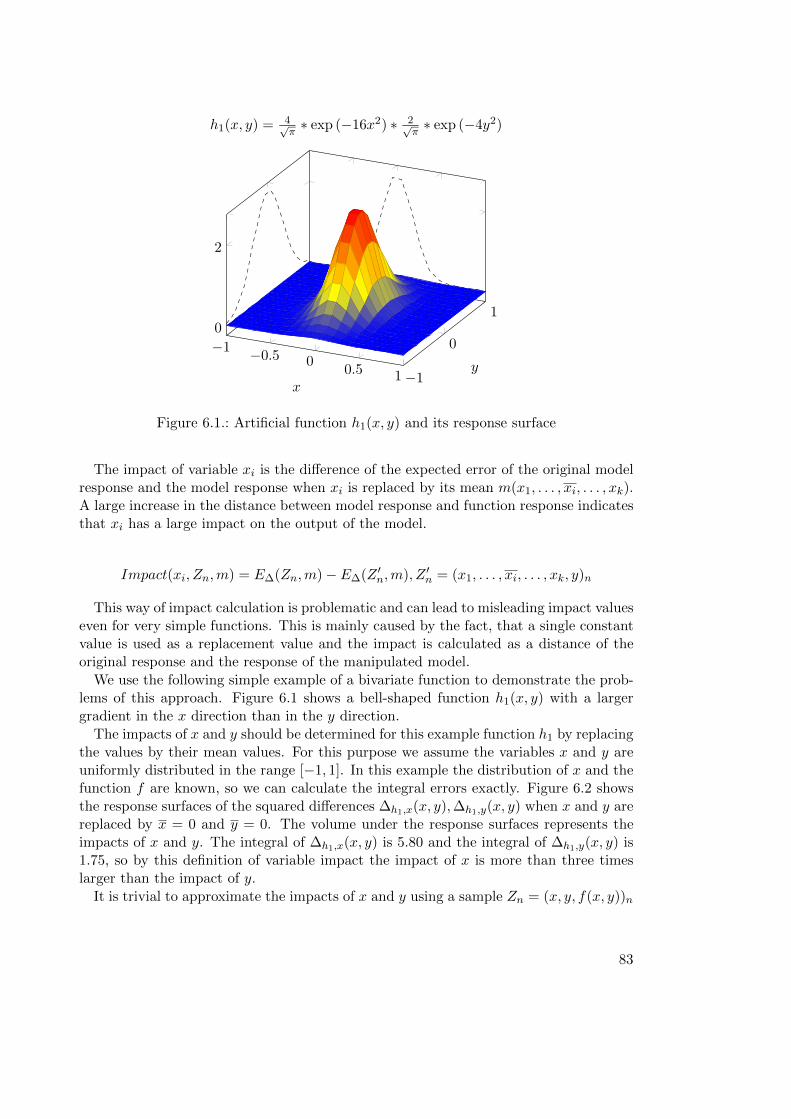

Supervised learning methods accept pairs of training examples with a correct label asinput. From these training examples the algorithm should learn how to correctly label

13

new examples in a generalizable way and learn from these examples which label fits bestfor future unseen examples.

Unsupervised learning methods accept training examples without labeling future inputexamples are compared to the previously learned training examples and one or multiplesamples, that are most similar to the current example, are produced as output.

The semi-supervised learning hybrid approach is also possible. This is often usefulwhen a large number of examples are available but only a small part of them is labeled.Semi-supervised learning methods determine labels for the unlabeled examples by find-ing similar labeled representatives and then use the unlabeled examples for training.Typical tasks solved by supervised learning methods are classification and regression;unsupervised learning is often used for clustering.

2.2. Classification, Regression and Clustering

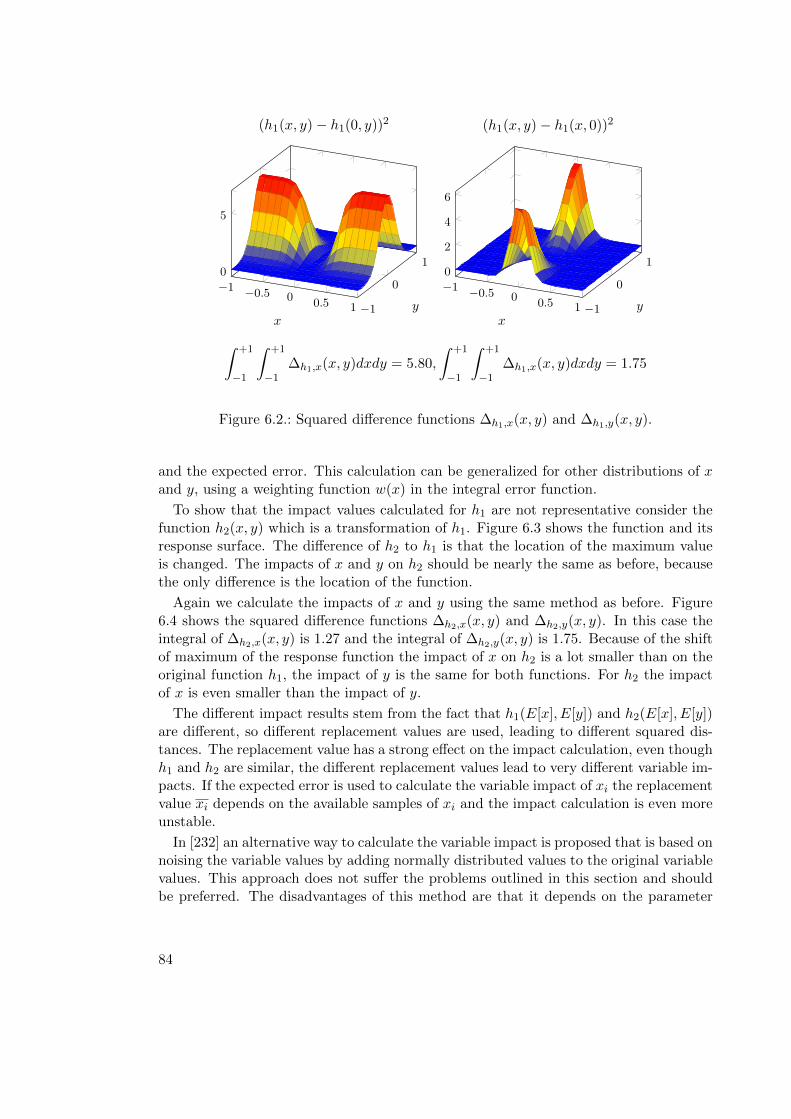

The input data for classification, regression and clustering are usually a collection of ntraining examples. Each example in the training data is a row vector of k values. Theset of training examples can be represented as a matrix T(n,k).

For the classification task the training samples have class values from a finite usuallysmall domain. The most common case is binary classification, meaning that the classlabels can have only two values (e.g. 0 or 1, malign or benign). However classificationfor three or more distinct class labels is also possible. It is not necessary that an orderingrelation can be defined on the class labels. The goal of classification algorithms is tolearn from the presented training samples in which class to categorize new and previ-ously unseen data points. The quality of classification algorithms is measured by a lossfunction. Usually the loss function compares the class predicted by the algorithm withthe actual class of the data point and then calculated from the number of correctly andincorrectly classified data points. Examples for classification algorithms are: linear dis-criminant analysis, C4.5 (decision tree learning) [169], support vector machines (SVM)[222, 41], k-nearest-neighbor (kNN) [42, 65], classification and regression trees (CART)[28].

For the regression task the training samples usually in Rn are labeled with values in R.The algorithm should learn the value linked with each data point so that it can generatea predicted value for new and previously unseen data points. Labels can be ordered sothe loss of a regression model is often measured as a distance of the predicted from theactual target values. Examples for regression algorithms are: linear regression, CART[28], SVM regression [221].

The task of binary classification can be reformulated into the regression task of findinga discriminant function g : Rn → R. The classification is achieved by assuming a constantseparator value c so that class = 0 if g < c and class = 1 if g ≥ c. A perfect predictioncan be achieved when a value c exists that separates both classes perfectly.

Regressing and classification are supervised learning tasks. In contrast, clustering isan unsupervised learning task [79, 83]. The goal of clustering is to group examples bysimilarity into a number of representative clusters. Each cluster is a set of examples and

14

a representative example. New examples are assigned to one of the learned clusters intowhich the new examples fits best. Clustering can also be applied to unlabeled examples.

A typical example of clustering is market basket analysis based recommender systems.The system uses a clustering method to find clusters of customers who purchased similarproducts. Based on the clustering the recommender system can suggest related productsbased on the products that other customers in the same cluster frequently purchased.Examples for clustering algorithms are: k-Means [125], expectation-maximization (EM)[49], and methods based on principal component analysis (PCA) [156, 89].

2.3. Reinforcement Learning

Reinforcement learning is a branch of machine learning that does not fit into the cate-gories supervised vs. unsupervised learning. Reinforcement learning is concerned withonline processes in which an agent can take actions and receives rewards for actions[210]. The acquisition of new observations which implicitly cause an unknown loss isintegrated directly in the learning process The objective is to find a policy for the agentthat minimizes the regret, which is the difference of the reward that the agent receivedto the reward that the agent could have received, if it would have executed the optimalactions at all times. The difference to supervised learning is that the correct actions arenever explicitly presented to the agent.

The best example to illustrate reinforcement learning methods is the multi-armedbandit problem that describes the situation of a rigged casino, a bandit gambling machinewith multiple arms with a different rate of winning plays and possibly unequal rewards.The goal for a player is to allocate plays to the machines in such a way, as to maximize theexpected total reward. The probability distribution of rewards for each arm is unknown,so an effective strategy has to be found that balances exploration of new arms andexploitation of the best arm so far. The K-armed bandit problem can be described asK random variables with Xi(0 ≤ i < K), where Xi is the stochastic reward given by thearm with index i. The rewards Xi are independent and the distributions are generallynot identical. The laws of the distributions and the expected value µi for the rewards Xi

are unknown. The goal is to find an allocation strategy that determines the next armto play, based on past plays and received rewards, that maximizes the expected totalreward for the player. Or put in other words: to find a way of playing that minimizesthe regret, which is defined as the expected loss occurred by not playing the optimalarm each time.

Since a player does not know which of the arms is the best he can only make as-sumptions based on previous plays and received rewards and concentrate his efforts onthe arm that gave the highest rewards so far. However it is necessary to strike a goodbalance between exploiting the currently best arm and exploring the other arms to makesure that an arm with a higher expected reward value can be discovered.

15

2.4. Time Series Forecasting

The notable difference of time series forecasting in comparison to regression or classifi-cation is that there is a time-dependent structure in the processed data points. Specialcare has to be taken in the training phase and when using the trained model so thatthe time-dependency or the ordering of the data points is not destroyed. In particularit is not valid to shuffle the data points in the training phase as this would destroy theinternal structure.

The goal of time series forecasting is to predict future values of a variable based onpast values of the variable and optionally other related variables. If the method uses pastvalues of the target variable for the prediction of future values it is an auto-regressivemethod.

Time series forecasting is a traditional application of statistics. Since the very firstformulations of time series models a large corpus of ever refined modeling approaches hasbeen described ranging from simple linear auto-regressive and moving average models[74, 90] to intricate models including trends and seasonal changes and multivariate timeseries [229]. For an extensive discussion of statistic approaches to time series modelingsee [23, 29, 30, 157, 57, 82].

Genetic programming has also been effectively used for time series prognosis tasks[101]. The power of genetic programming to evolve the structure of solution candidatesin combination with the parameters enables the process to automatically adjust themodel structure appropriately for instance to account for seasonal changes, trends orrecurrent events if such elements are detected in the data.

Chapter 7 discusses multi-variate time series modeling with genetic programming.

2.5. Generalization and Overfitting

Any data-based model, regardless of which learning or estimation process is used, mustgeneralize well in order to be useful. Models which generalize well are models that alsowork consistently for new observations. In contrast models that do no generalize wellproduce inaccurate or even largely incorrect estimations for new observations and arethus useless in practice. The generalization ability of a given model can be estimatedby using a hold out dataset which contains samples that are not used in the trainingprocess. The fit on the hold-out is an indicator for the fit on new observations. If themodel performs equally well on the training set and on the hold-out set it can be assumedthat the model generalizes well. This assumption only holds in general when a numberof assumptions about the analyzed system and the selection the training set and thehold-out set are fulfilled. The number of different states of the system must be limitedand the training set and the hold-out set must be a representative sample of the wholepopulation of observable states of the analyzed system. If these assumptions hold newobservations from the same system will be similar to observations in the training- andhold-out set, and the fit on the hold-out set is an accurate estimator for the expected fitfor new observations.

16

2 4 6 8 100

0.2

0.4

0.6

0.8

1

1.2

Complexity

Error

Training error

Expected generalization error

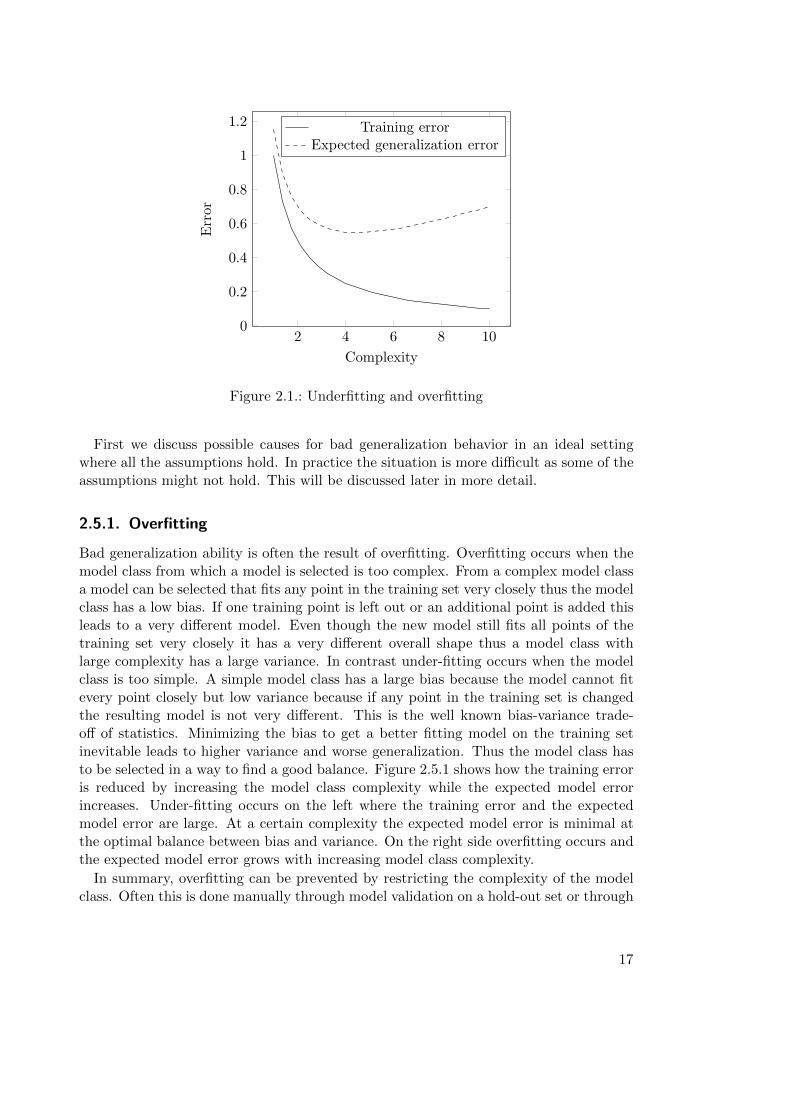

Figure 2.1.: Underfitting and overfitting

First we discuss possible causes for bad generalization behavior in an ideal settingwhere all the assumptions hold. In practice the situation is more difficult as some of theassumptions might not hold. This will be discussed later in more detail.

2.5.1. Overfitting

Bad generalization ability is often the result of overfitting. Overfitting occurs when themodel class from which a model is selected is too complex. From a complex model classa model can be selected that fits any point in the training set very closely thus the modelclass has a low bias. If one training point is left out or an additional point is added thisleads to a very different model. Even though the new model still fits all points of thetraining set very closely it has a very different overall shape thus a model class withlarge complexity has a large variance. In contrast under-fitting occurs when the modelclass is too simple. A simple model class has a large bias because the model cannot fitevery point closely but low variance because if any point in the training set is changedthe resulting model is not very different. This is the well known bias-variance trade-off of statistics. Minimizing the bias to get a better fitting model on the training setinevitable leads to higher variance and worse generalization. Thus the model class hasto be selected in a way to find a good balance. Figure 2.5.1 shows how the training erroris reduced by increasing the model class complexity while the expected model errorincreases. Under-fitting occurs on the left where the training error and the expectedmodel error are large. At a certain complexity the expected model error is minimal atthe optimal balance between bias and variance. On the right side overfitting occurs andthe expected model error grows with increasing model class complexity.

In summary, overfitting can be prevented by restricting the complexity of the modelclass. Often this is done manually through model validation on a hold-out set or through

17

cross-validation. Such methods can be used with any kind of data-based modeling algo-rithm. Some algorithms include countermeasures for overfitting into the learning process.Often this is done by adding a complexity term to the objective function so that themodel accuracy is optimized together in combination with the model complexity as forinstance used in SVMs. Another approach is to use an internal validation set to controlthe complexity of models as for instance used in enhanced implementations of ANN.

2.5.2. Bad Generalization because of Incomplete Data

In real world scenarios bad generalization can often be the result of incomplete data.The assumption that the training set is a set of independently sampled observations andrepresentative for the whole population of possible observations does often not hold.

If the training set does not contain examples for all system states that are likely tobe observed, it is not possible to create a model that will generalize well to all newobservations. The learning algorithm can only build a model based on the incompleteinformation in the training set. If the state of the analyzed system or its inputs arechanged the system behavior will also change and the model does not fit anymore. Amodel trained from an incomplete training set will not generalize well if the behaviorof the underlying system changes. It should be noted that this problem is independentof overfitting. Even if the model showed good fit via cross-validation the generalizationerror can be large as cross-validation assumes that the samples in the training set andhold out were sampled independently. Even though the bad generalization is in this casenot caused by overfitting in the original definition but by incomplete data the remediesto improve the generalization are similar. Reduction of complexity to increase the biasand reduce the variance of the model class should lead to better generalization behaviorin both situations. In the remainder of this work we will thus refer to both causes forbad generalization as overfitting.

2.5.3. Time Series Modeling Pitfalls

Time series have an implicit time-dependent structure which must be preserved for mod-eling and estimation. In particular two observations of a time series are not independent.It should be noted that many collections of observations are by definition a time seriesas the observations are usually made over a certain timespan and not simultaneously.Often the original time-dependency is dropped, however, when it can be argued that theobservations are independent. In order to drop the time-dependency it must be shownthat all pairs of observations x(i) and x(j)(i > j) are independent (nothing that effectedobservation x(i) can have an effect on observation x(j)). In particular x(t+ 1) must beindependent from x(t). A simple but non-sufficient criteria to check is if x(t) and x(t+k)are correlated. Alternatively visual examination is also a quick way to determine if thedata has a time-dependent structure.

In many situations the time-dependency must be preserved. Examples are series ofmeasurements of technical systems, financial or economic time series, series of diagnosticvalues of patients over time.

18

As a consequence shuffling of examples is not allowed for time series as it would breakup the time-dependency. Shuffling of examples is often done as preparatory step beforetraining or cross-validation, and is implemented in this way in many algorithm imple-mentations (e.g. libSVM [32]). For time series the examples in the training- and hold-outset must be a set of consecutive observations. Semantically it is more appropriate to usesamples x(0) to x(k) as training set and samples x(k + i)i ∈ [1..n − k] as hold-out set,forecasting from previous observations.

19

3. Evolutionary Algorithms and GeneticProgramming

3.1. Evolutionary Algorithms

Evolutionary algorithms imitate aspects of biological evolution such as selection, recom-bination, and mutation to find a solution to a given problem starting with an initialpopulation of random solution candidates. From the initial population two solutioncandidates are selected as parents and recombined to produce one or two offspring in-dividuals which are then optionally mutated and subsequently added to the population.Parent selection has a higher chance to select solution candidates with an above averagefitness and recombination has the effect to combine the traits of the parent individualsin the offspring individuals. This is related to the principle of “survival of the fittest”in biological evolution. The selective bias and the combination of positive traits in in-dividuals have the effect, that the average fitness of the population increases over manygenerations producing better and better solution candidates over time.

The pioneers of evolutionary algorithms are Fogel who first described evolutionary pro-gramming [67], Rechenberg who first described evolution strategies [171], and Hollandwho first described genetic algorithms [86] at around the same time. The three algo-rithms all imitate aspects of biological evolution, however, each of the authors used aslightly different approach. The first descriptions of genetic algorithms use a binarysolution encoding and emphasize the aspect of parental selection and sexual reproduc-tion and recombination of positive traits. In contrast the first descriptions of evolutionstrategies use a real-valued encoding and emphasize the aspect of mutation and selectionfor survival of excess offspring. Self-adaptive aspects also play a large role in evolutionstrategies and have been integrated to improve the algorithm already very early [185]. Inthe first description of evolutionary programming graphical models in the form of finitestate machines for the prediction of a series of symbols are evolved through a combi-nation of sexual reproduction with crossover and mutation. Evolutionary programmingalso emphasizes the selection of offspring with above average fitness [66] and has thusbeen compared mainly with evolution strategies.

The fundamentally different approaches of genetic algorithms, evolution strategies,and evolutionary programming initially lead to a fragmentation of the research com-munities in separate camps. However, this initial fragmentation became gradually lessdistinct over the years, as the approaches have been further developed and aspects ofgenetic algorithms have also been integrated into evolution strategies, and vice versa.

21

3.2. Genetic Programming

Genetic programming [101] is an evolutionary algorithm to find computer programs thatsolve a given problem when executed. In contrast to genetic algorithms and evolutionstrategies which directly evolve solution candidates for the problem, the individuals inGP are computer programs which can be interpreted or executed to produce a solution tothe original problem. The structure of GP solution candidates is not fixed, in particular,the length of programs evolved in GP is not predetermined. This is a major differenceto other evolutionary algorithms which use fixed-length solution encodings for instancereal-valued vectors, bit-strings, or permutation arrays.

Solution candidates in GP are most often encoded as symbolic expression trees thatrepresent computer programs. The set of allowed symbols in a tree and the evaluationof trees are problem specific, and can be adjusted through algorithm parameters. Theseparameters are the function set, terminal set, and the fitness function. The function setcontains symbols that can be used as internal nodes of the tree and the terminal setcontains symbols which are allowed as terminal nodes.

Generally genetic programming can be used to evolve solutions for a given problem, ifit is possible to define a language describing possible solutions and a fitness function forsuch solutions. Genetic programming has been used to find novel and human competitivesolutions to hard problems and to find re-discover previously patented solutions [103,14, 19, 105, 6, 133, 102].

3.2.1. Genetic Programming Variants

Many different variants of genetic programming have been studied in the literature andthere is no precise definition of a genetic programming algorithm. Instead the termgenetic programming encompasses all the different algorithm variants. As stated by Poliet al., “At the most abstract level GP is a systematic, domain-independent method forgetting computers to solve problems automatically starting from a high-level statementof what needs to be done.”.

The different variants of GP can be differentiated into different classes by the wayhow the programs are represented (solution encoding). Koza-style GP [101], often calledstandard GP, uses a tree-based solution encoding. This representation of programs hasthe advantage that recombination and manipulation operators are relatively easy to im-plement. One problem of Koza-style GP is the requirement that the function set musthave the closure property, which means that the types of all terminals, function results,and function arguments must be compatible. This property is necessary to guaranteethat all possible tree shapes can be evaluated. The only syntactic constraint available instandard GP is the number of sub-trees allowed for each function symbol. This simpleassumptions of standard GP make it possible to define effective and easy to implementrecombination and mutation operators for the evolution of trees. More complex GP vari-ants are often more powerful but also significantly more difficult to implement correctly,especially because the evolutionary operators are often more complex.

In some applications it is necessary that the possible structure and characteristic of GP

22

solutions can be defined more precisely. This issue has been addressed in two differentbut related ways, leading to the definition of grammar-based GP and strongly typed GP.

Grammar-based GP

In grammar-based GP [228, 234] all possible GP solutions are defined through a grammarfor GP solutions. The grammar defines the syntax of the programming language usedby GP to express solutions, in the same way as the grammar of a programming languagedefines the possible programs that can be written in this language. In grammar-based GPit is easy to restrict the structure of GP solutions. This is for instance necessary if GP isused to evolve programs for a given existing programming language. Grammar-based GPhas for instance been used successfully to evolve classification algorithms represented asJava programs [154]. A successful variant using this approach is grammatical evolution[147]. In grammar-based GP the grammar is used only to restrict the possible shapesof solutions. In grammatical evolution the grammar is also used to construct trees andfrom a linear representation. The solution is encoded as a variable-length list of integers.Each element defines which branch in a syntax rule must be taken to construct a validtree. The translation process starts with the first element of the list and the main entrypoint of the grammar.

Strongly-typed GP

In strongly typed GP [136] the types of terminals, functions, and function arguments aredeclared. Each time the GP system produces a new tree for instance through crossover, itmust make sure that the type of the argument is compatible to the type of the parameterof the function. As long as the number of possible types handled by the GP system israther small the type constraints can be handled also through syntactical constructsusing grammar-based GP, however, a strongly-typed GP system is more appropriate ifthe GP system must be capable to handle many different types.

Strongly-typed GP and grammar-based GP define constraints for the construction oftrees, thus in the implementation of such GP systems the operators for initialization,recombination, and mutation must be extended to check all constraints. Both variantsare generalizations of standard GP, which is essentially a strongly typed GP systemwith only one type instance and a very simple grammar that specifies only the numberof arguments of functions.

Linear GP

In linear GP [21] the program code is evolved directly in a variable-length linear repre-sentation instead of a tree-based representation. The solutions represented in linear formare closer to the executing machine than the tree-based programs and thus evaluation ofsolution candidates is usually more efficient in linear GP than in tree-based GP variants.In the most extreme case linear GP directly evolves machine code [145]. Because linearcode lacks the structure available in tree-based representations memory operations to

23

read and write stores or registers are necessary. In a recent contribution a linear GPapproach to evolve Java byte-code is described [150].

PushGP [198] is an especially interesting strongly-typed linear GP system which uses astack-oriented execution model. In the execution of Push expressions a separate evalua-tion stack is used for each occurring type and it is allowed to push quoted code-fragments.Thereby, it is possible to manipulate and transform the program code before execution.It has been suggested that PushGP can be used as an “autoconstructive evolution sys-tem” [198, 197], where the evolutionary operators used to recombine and manipulateoperators are evolved simultaneously with the solutions. This is a very powerful andgeneral approach which allows the GP system to self-adapt to the specific problem thatmust be solved.

Graph-based GP

In graph-based GP solution candidates are represented in form of a graph which isa more general data-structure than a tree. Graph-based programs can potentially beexecuted in parallel fashion [159]. The drawback of the approach is that the implemen-tation of crossover and mutation operators for the evolution of graphs is more complex.Additionally, the interpretation of solutions is difficult.

Cartesian GP [81, 135] is a special form of graph-based GP. The execution model alsouses a graph-based program representation, but in Cartesian GP a level of indirectionis introduced as the graph is encoded in linear form. The evolutionary operators aredefined on the variable-length linear representation which is translated into a graphdata-structure for evaluation. The solutions are encoded as integer tuples each onedescribing the properties of a cell in a two-dimensional grid. The elements in the tuplesdefine the symbol of the node, and the incoming edges from other cells. Cartesian GPwas initially introduced for the evolution of electronic circuits [134]. Recently extensionsto Cartesian GP have been described to allow to allow the definition and execution ofself modifying programs [81]

3.3. Bloat

The term bloat in genetic programming relates to the growth of program length overa run without a proportional improvement in fitness [117]. The effect has also beendescribed as “survival of the fattest” [58]. Genetic programming uses a variable-lengthsolution encoding so average program length of the solution candidates in the popula-tion can grow or shrink over a GP run. The randomly generated programs in the firstgeneration are limited to a certain range of possible sizes. Changes in average programsize are thus a result of the evolutionary operators acting on the population. It hasbeen observed already early that standard GP bloats without special countermeasuresto prevent unlimited growth of programs. Bloat is problematic because of the memoryconsumption and the increased computational effort necessary to evaluate bloated solu-tions. Additionally, bloated solutions produced by GP are difficult to understand andvalidate. Thus the topic has been studied intensively in the literature and a number

24

of different hypotheses for the cause of bloat and methods to control bloat have beendescribed.

3.3.1. Inviable Code and Unoptimized Code

Bloated programs contain a lot of code that has no or only minor effect on the outputof the program. The ineffective code fragments can be differentiated into two classes,namely inviable code and unoptimized code [16, 188, 238]. Inviable code fragments(introns [17]) are not executed at all and so have no effect on the program behavior.Introns can occur when non-sequential execution flow for instance conditional evaluationof code fragments is possible in the GP solutions. Is relatively easy to detect inviablecode through dynamic code analysis. All code fragments that are not visited when theprogram is executed are inviable code and can be removed easily without altering theprogram behavior.

Unoptimized code fragments, in comparison, are executed and have an effect on theprogram output. However, the code fragment is either detrimental to the fitness ofthe program, or its contribution to fitness is not proportional to its length. In generalunoptimized code is executed but can be replaced by more compact code or even re-moved completely in the case of detrimental code fragments. It is rather difficult todetect or replace unoptimized code. One approach that can be used to partially removeunoptimized code fragments for tree-based GP is pruning [232]. Pruning determinesunoptimized branches by calculating for each branch of the original program the fitnessof a transformed program where that branch has been replaced by neutral code. If thefitness of the transformed program is not significantly worse than the fitness of the orig-inal program the branch is unoptimized code and can be removed. In Chapters 4 and 5we discuss pruning in more detail.

It has been suggested that symbolic regression is not prone to the propagation ofinviable code, but very much affected by unoptimized code [186, 187]. This is howeverstill an open question [129].

3.3.2. Bloat Control in Practice

Out of the necessity to control bloat a number of effective methods have been proposedfor practical applications. A straight forward approach is to add static size and depthlimits for trees [101]. The crossover and mutation operators check if newly created treesare within the size limits and invalid trees are discarded. Another approach are size-fairevolutionary operators that produce a new tree that has the same size as the originaltree [112, 165] or mutation operators that actively reduce the program length [96, 15].Alternatively, selection can be adjusted to control bloat. Parsimony pressure increasesthe probability to select smaller individuals by including a weighted penalty term thatdepends on program length into the fitness function [239]. Lexicographic tournamentselection is an extension of tournament selection where the smaller solution is selectedif two solutions have the same fitness value [128].

25

3.3.3. Bloat Theory

Even though the bloating effect of GP has been observed already early, the cause forbloat has long remained an open question. Over the time different theories for the causeof bloat have been formulated often in combination with methods to control bloat. Inthe following a number of frequently cited hypothesis for bloat are discussed, as the topicis also very relevant for this thesis. A good survey of past and current bloat theories isgiven in [188]. The topic will be revisited in Chapter 4.

Defense against crossover

An early theory for bloat was that bloated solutions are more robust against disruptivechanges by crossover [10]. The probability that crossover has a strong negative effect onthe fitness of an individual is smaller for solutions that bloated and contain many intronsrelative to compact solutions. This means bloated individuals are preferred by selectionas they are not destructed by crossover so easily and over time the evolutionary processleads to more bloated individuals in the population. The theory has been disputed [188]and is currently not considered to be a valid theory for the cause of bloat in tree-basedGP.

Removal Bias

The removal bias theory of bloat [195] is closely related to the defense against crossovertheory and also relates the cause for bloat to the fact that a surplus of inviable code makesit easier to add more code without negative effects on fitness. In particular, fitness isnot effected strongly when crossover affects an inviable branch. In such crossover eventsthere is an asymmetry, namely that the sub-branch which is removed from the inviablebranch has a limited size, but the branch that is inserted from the other parent can beof any size and in particular larger than the removed branch. This asymmetry can leadto code growth even when the crossover is protected, producing only offspring that arestrictly better than their parents. The removal bias theory has also been superseded bythe more recent crossover bias theory.

Fitness causes bloat

The fitness causes bloat theory relates the cause for bloat to the nature of the programsearch space [111, 116]. In this theory introns are merely an effect of bloat but not acause, in contrast to removed bias theory or defense against crossover theory. Fitnesscauses bloat theory proceeds from the assumption that bloat does not occur when noselection pressure is applied to the population. It has been shown that bloat does notoccur when a constant or random fitness function is used [20, 116, 110]. If crossover isapplied repeatedly on a number of solutions with only random selection (or with flatfitness) no code growth can be observed.

The theory states that bloat occurs if the program search space has the property thatany solution can be expressed in many alternative but semantically equivalent ways,

26

and that there are more longer than shorter alternative representations. An additionalrequirement for the occurrence of bloat is a static fitness function that assigns the samefitness to all semantically equivalent programs regardless of their size. The length dis-tribution of equivalent programs causes a drift to larger solutions.

The theory is general and is applicable to all iterative search algorithms with a discretevariable-length solution encoding and a static fitness function. In particular, bloat is notspecific to population-based algorithms but can also occur in trajectory-based algorithmsand in algorithms that do not use a crossover operator.

Crossover bias

Crossover bias theory [164, 52] is related to fitness causes bloat theory and is the mostrecent theory for the cause of bloat. It states that bloat occurs because of a bias of thecombination of sub-tree crossover and selection. As stated in the fitness causes bloattheory bloat only occurs in the presence of selection pressure and a program search spacewhere for a given fitness many more larger solutions than small solutions exist.

Crossover bias theory is based on the observation that sub-tree swapping crossoverin tree-based genetic programming produces offspring with a particular size distribution(Lagrange distribution of the second kind). The average size of offspring is not alteredby sub-tree swapping crossover, as the removed branch and the inserted branch have thesame size on average. However, crossover produces more smaller individuals then largeindividuals. It has been shown that the size distribution of individuals produced bycrossover depends on the symbols in the function set and on the number of parametersof the functions [55].

The combined effect of this crossover bias in combination with a fitness landscapewhere smaller individuals are more likely to have lower fitness than larger individualscauses a drift to larger individuals. Actually, any operator that produces a surplus ofsmaller individuals leads to bloat. Thus, it has been suggested recently to rename thetheory to operator length bias theory [55].

3.3.4. Theoretically Motivated Bloat Control

A number of effective bloat control methods are based on crossover bias theory. Asbloat control is a major topic in this thesis theses methods are discussed briefly in thefollowing. In Chapters 4 and 5 bloat control methods are discussed in more detail.

Tarpeian Method

Tarpeian bloat control sets the fitness of individuals with above average length to a verylow value which effectively zeros the chance of selection of this individual. This methodof bloat control is very simple and can be controlled through only one parameter thatdetermines the chance that a given individual is assigned a zero fitness. The effectof Tarpeian bloat control is that the dynamic holes in the fitness landscape reduce thechance of selecting larger individuals and bloat is prevented or at least reduced. Recently,the covariant Tarpeian method for bloat control has been introduced [161], where the

27

probability that a solutions fitness is zeroed, is automatically adapted based on thecovariance of program lengths and fitnesses in the population.

Covariant Parsimony Pressure

The covariant parsimony pressure method to control bloat [163] is based on the sizeevolution equation [162]. The parsimony pressure method adjusts selection probabilityto prefer smaller individuals relative to larger individuals with the same fitness. For thisan adjusted fitness value is calculated that includes not only the raw fitness but adds apenalty term depending on the length of the solution. In covariant parsimony pressurethe penalty term is adjusted dynamically based on the covariance of fitness and lengthover all individuals in the population. It has been shown that the average program lengthcan be controlled tightly using covariant parsimony pressure to completely remove bloat.

Operator Equalization

The operator equalization method to control bloat [54] is also based on crossover biastheory and removes bloat by adjusting the distribution of individuals produced by theevolutionary operators. This is accomplished by an equalization step which filters newlycreated individuals, so that the length distribution of solutions in the next populationmatches a specific target distribution. As soon as the frequency of individuals of a spe-cific size matches the target frequency, newly created individuals of the same size arediscarded. The method continues creating new offspring using the evolutionary opera-tors until the population can be fully filled and the size distribution in the populationmatches the specified target distribution. A self-adaptive variant of operator equaliza-tion has also been described, where the target size distribution is adjusted to follow thefitness distribution while still preventing bloat [189, 190]. In comparison to Tarpeianbloat control which hooks into fitness evaluation to control bloat, operator equalizationremoves the other necessary ingredient for bloat, namely the operator length bias.

3.3.5. Quantification of Bloat

In a recent contribution a measure for bloat has been defined that can be used to comparethe relative amount of bloat in GP runs [220]. Bloat is the disproportional growth ofprogram length relative to fitness improvement, thus the function shown in Equation 3.1measures the amount of bloat at generation g as the relative change of average programlength δ from the initial generation to generation g over the relative change of averagefitness f in the same interval.

bloat(g) =(δ(g)− δ(0))/δ(0)

(f(0)− f(g))/f(0)(3.1)

If no bloat has occurred the function bloat(g) has a value of one, indicating that theaverage program size and the average fitness changed by the same amount. Notably,the function can also become negative if the average program length decreases while theaverage fitness increases.

28

The original definition shown in Equation 3.1 only works for minimization problems,for maximization problems the relative change in fitness can be calculated as (f(g) −f(0))/f(0). A problem occurs when f(0) is close to zero which leads to unstable results.This can happen for instance when the squared correlation coefficient is used as fitnessmeasure. To mitigate such problems the calculation of the relative change in fitnessshould be adjusted accordingly as shown in Equation 3.2.

bloat(g)max =(δ(g)− δ(0))/δ(0)

(f(g)− f(0))/(1 + f(0))(3.2)

In Chapter 4 this function is used to compare the effect of different bloat controlmethods.

3.4. Data-based modeling with Genetic Programming

3.4.1. Symbolic Regression

One possible problem that can be solved by genetic programming is symbolic regression.Symbolic regression [101] is concerned about finding a model f(x) (functional expres-sion), that is a good approximation of the values of the target variable y given a numberof input variables x. The values of the target variable are produced by an unknownresponse function of the studied system f(x). The input for symbolic regression is adataset with n observed values of each variable of the studied system. The result isa functional expression f(x) encoded as a symbolic expression tree. For symbolic re-gression the GP function set usually includes at the arithmetic operators (+,-,*,/), andthe terminal set includes all allowed input variables and constant values. A possibleand frequently used fitness function is the mean of the squared errors (MSE) of theapproximated values calculated by the symbolic regression model f(x) and the actuallyobserved values y.

MSE(fx, y) =1

n

n∑

i=1

(f(x)i − yi)2 (3.3)

The observed values y of the target function f(x) include a certain amount of noise,so the error term to be minimized in symbolic regression is the sum of the error of themodel εmodel and the error of the measurements εnoise. The aim is to approximate theunknown function f(x), however, the implicit measurement error εnoise in y cannot becompletely removed and is the limiting factor for the accuracy of the approximations ofthe model relative to the response function f(x) of the studied system.

f(x) = y + εmodel

y = f(x) + εnoise(3.4)

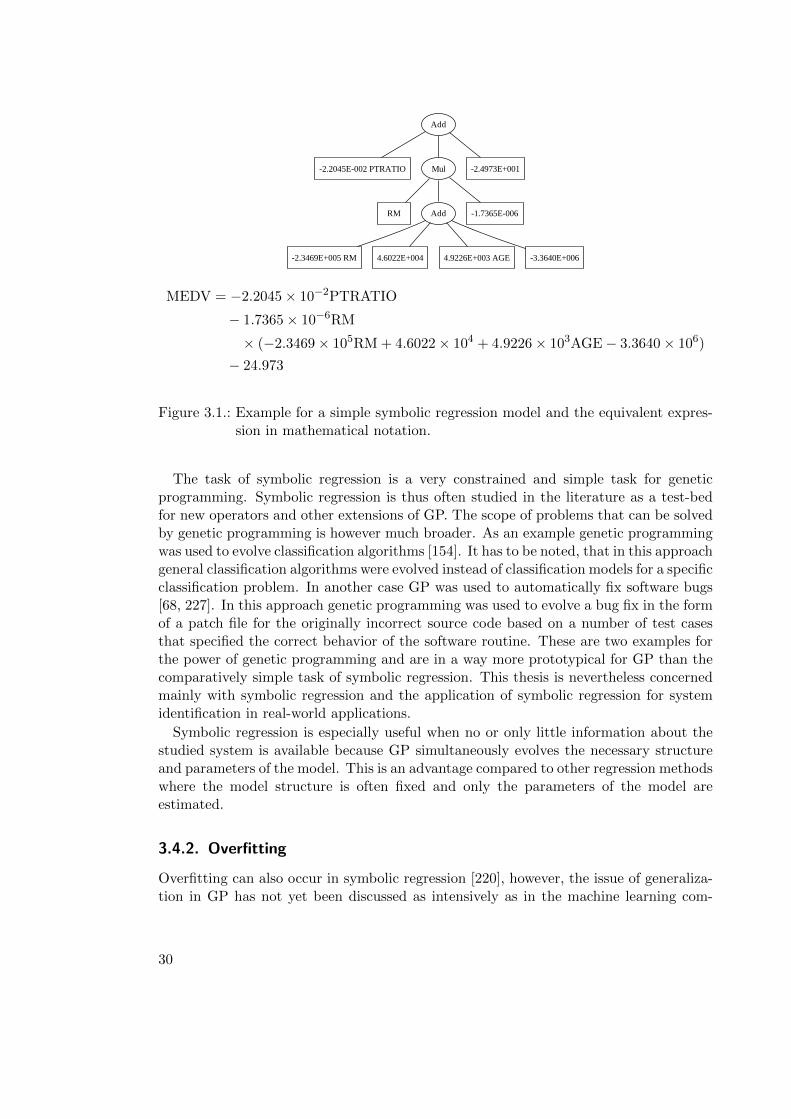

Figure 3.1 shows an example for a symbolic regression model and the equivalent ex-pression in mathematical notation.

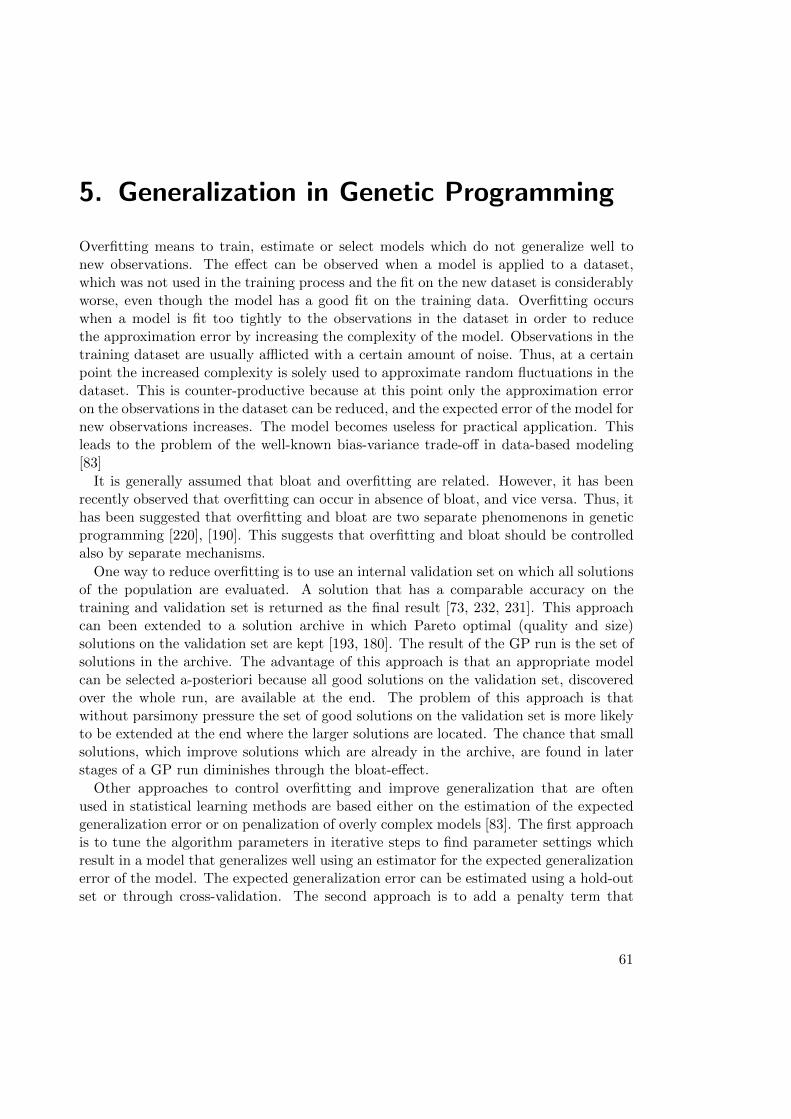

29

Add

-2.2045E-002 PTRATIO Mul -2.4973E+001

RM Add -1.7365E-006