Embed Size (px)

Citation preview

Willkommen

Asset Management Event 2017

8. Juni 2017

www.pwc.com

PwC

Agenda

2

08. Juni 2017Asset Management Event 2017

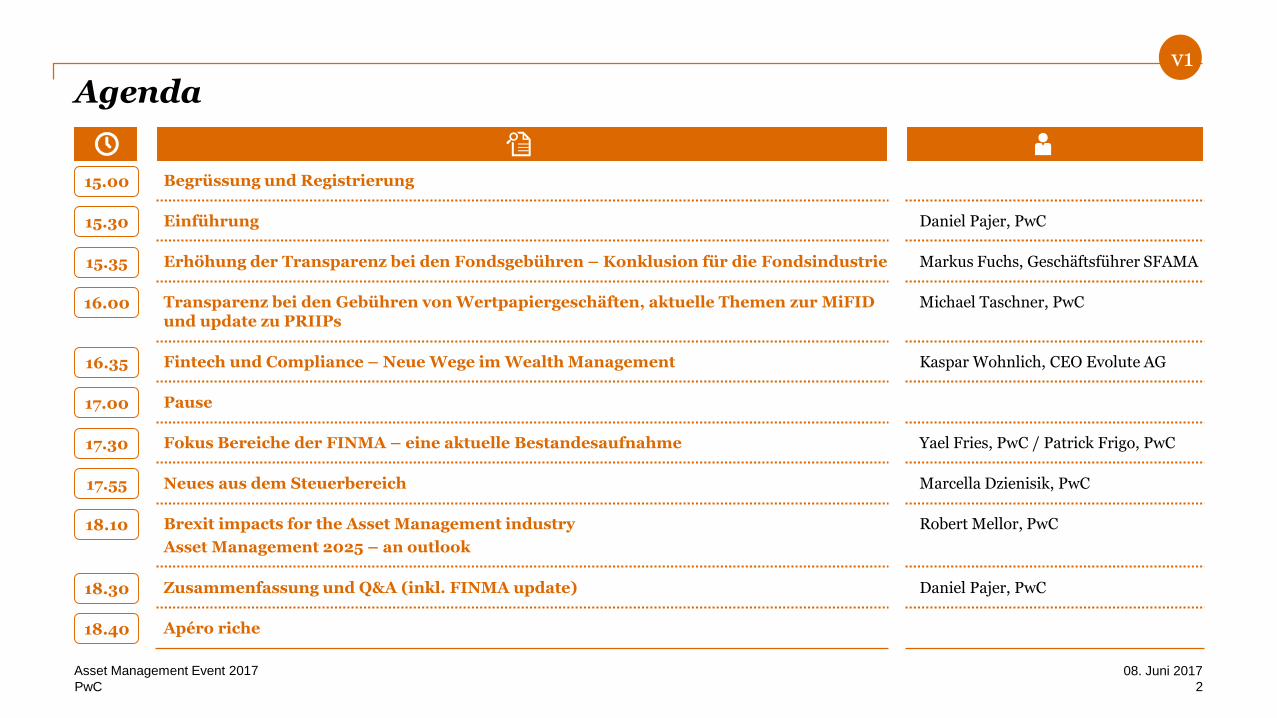

15.00 Begrüssung und Registrierung

17.00 Pause

15.30 Einführung Daniel Pajer, PwC

15.35 Erhöhung der Transparenz bei den Fondsgebühren – Konklusion für die Fondsindustrie Markus Fuchs, Geschäftsführer SFAMA

16.00 Transparenz bei den Gebühren von Wertpapiergeschäften, aktuelle Themen zur MiFIDund update zu PRIIPs

Michael Taschner, PwC

16.35 Fintech und Compliance – Neue Wege im Wealth Management Kaspar Wohnlich, CEO Evolute AG

17.30 Fokus Bereiche der FINMA – eine aktuelle Bestandesaufnahme Yael Fries, PwC / Patrick Frigo, PwC

17.55 Neues aus dem Steuerbereich Marcella Dzienisik, PwC

18.10 Brexit impacts for the Asset Management industry

Asset Management 2025 – an outlook

Robert Mellor, PwC

18.30 Zusammenfassung und Q&A (inkl. FINMA update) Daniel Pajer, PwC

18.40 Apéro riche

v1

PwC

Begrüssung & Einführung15:30 – 15:35

Daniel Pajer, PwC

3

08. Juni 2017Asset Management Event 2017

PwC

App herunterladen

• Gehen Sie auf www.pwc.ch/event-app oder suchen Sie nach «PwC Events CH» im App Store oder auf Google Play.

• Blackberry oder Windows Phone Benutzer klicken auf das HTML5 Logo unter www.pwc.ch/event-app.

Alle Informationen finden Sie auch auf der Rückseite Ihrer Member Card, die Ihnen am Empfang gegeben wurde.

4

08. Juni 2017Asset Management Event 2017

PwC

Haben Sie Fragen?

Stellen Sie Ihre Fragen direkt in der App.

5

08. Juni 2017Asset Management Event 2017

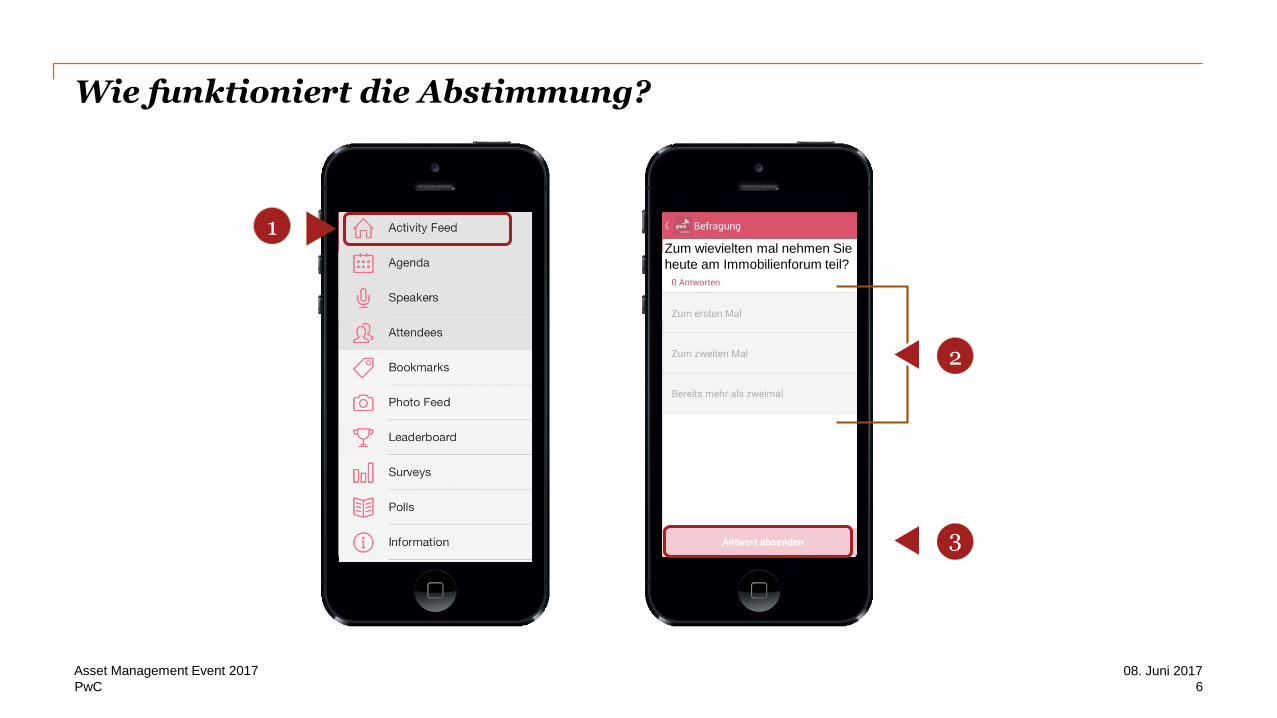

1

Klicken Sie auf das Icon rechts obenim Activity-Feed

2

2

PwC

Wie funktioniert die Abstimmung?

Zum wievielten mal nehmen Sie

heute am Immobilienforum teil?

6

08. Juni 2017Asset Management Event 2017

1

2

3

PwC

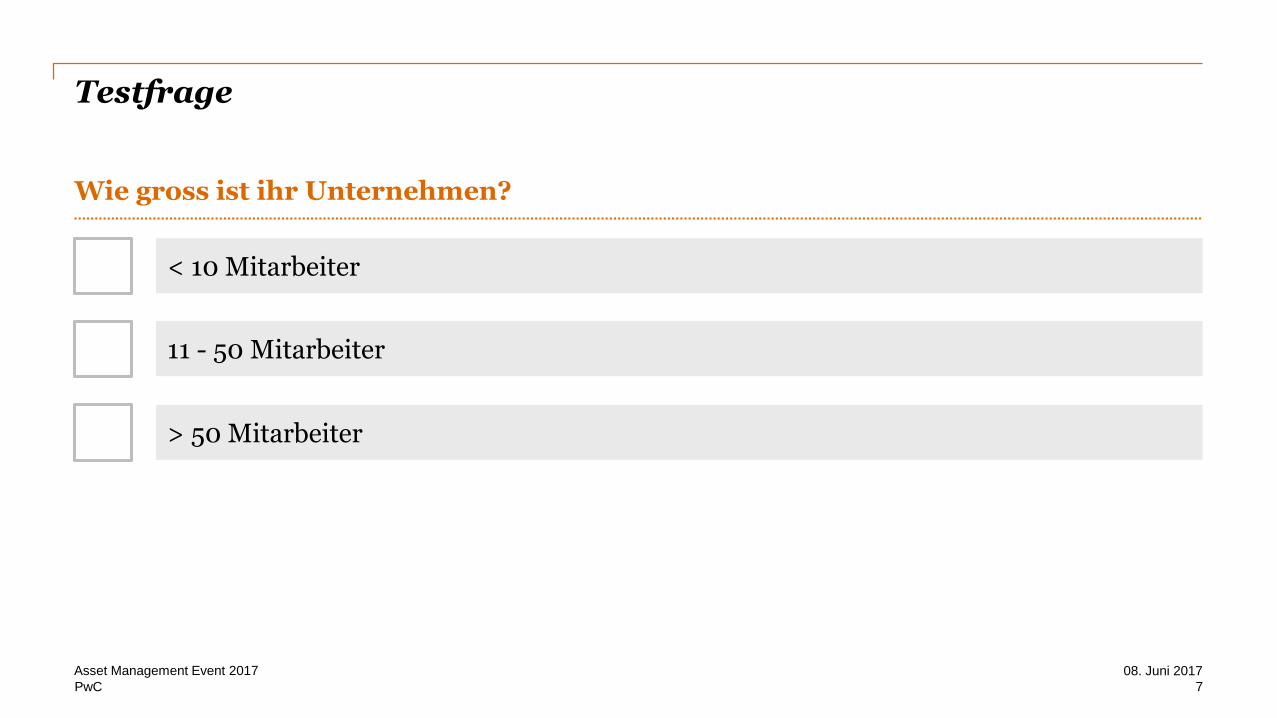

Testfrage

Wie gross ist ihr Unternehmen?

7

08. Juni 2017Asset Management Event 2017

< 10 Mitarbeiter

11 - 50 Mitarbeiter

> 50 Mitarbeiter

PwC

Erhöhung der Transparenz beider Fondsgebühren

8

08. Juni 2017Asset Management Event 2017

Anlagefonds sollen Schleier lüften

PwC

Erhöhung der Transparenz bei den Fondsgebühren15:35 – 16:00

Markus Fuchs

9

08. Juni 2017Asset Management Event 2017

Gebührentransparenz: Einordnung und

Konklusionen für die Fondsindustrie

Markus Fuchs, Geschäftsführer

PwC Asset Management Anlass: Zürich, 8. Juni 2017

PwC

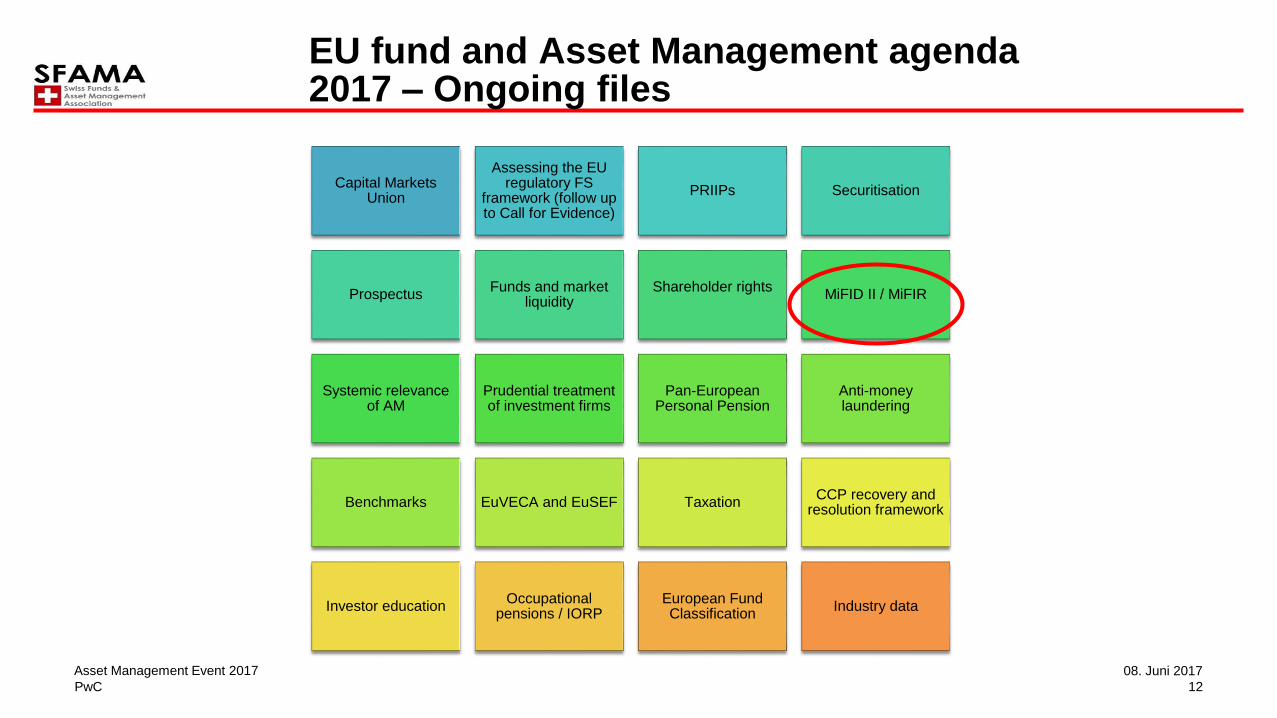

Fund and Asset Management agenda 2017

11

08. Juni 2017Asset Management Event 2017

PwC

Capital Markets Union

Assessing the EU regulatory FS

framework (follow up to Call for Evidence)

PRIIPs Securitisation

ProspectusFunds and market

liquidityShareholder rights

MiFID II / MiFIR

Systemic relevance of AM

Prudential treatment of investment firms

Pan-European Personal Pension

Anti-money laundering

Benchmarks EuVECA and EuSEF TaxationCCP recovery and

resolution framework

Investor educationOccupational

pensions / IORPEuropean Fund Classification

Industry data

EU fund and Asset Management agenda 2017 – Ongoing files

12

08. Juni 2017Asset Management Event 2017

PwC

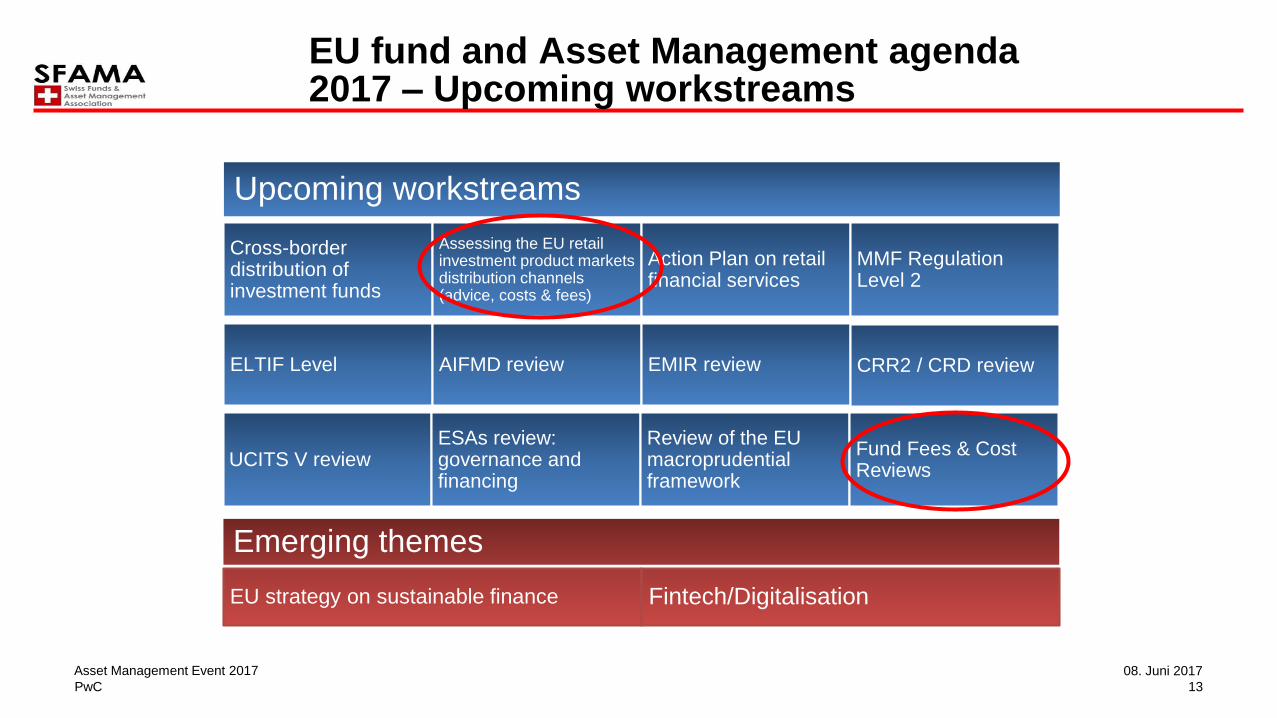

EU fund and Asset Management agenda 2017 – Upcoming workstreams

Upcoming workstreams

Cross-border distribution of investment funds

Assessing the EU retail investment product markets distribution channels (advice, costs & fees)

Action Plan on retail financial services

MMF Regulation Level 2

ELTIF Level AIFMD review EMIR review CRR2 / CRD review

UCITS V reviewESAs review: governance and financing

Review of the EU macroprudentialframework

Fund Fees & Cost Reviews

Emerging themes

EU strategy on sustainable finance Fintech/Digitalisation

13

08. Juni 2017Asset Management Event 2017

PwC

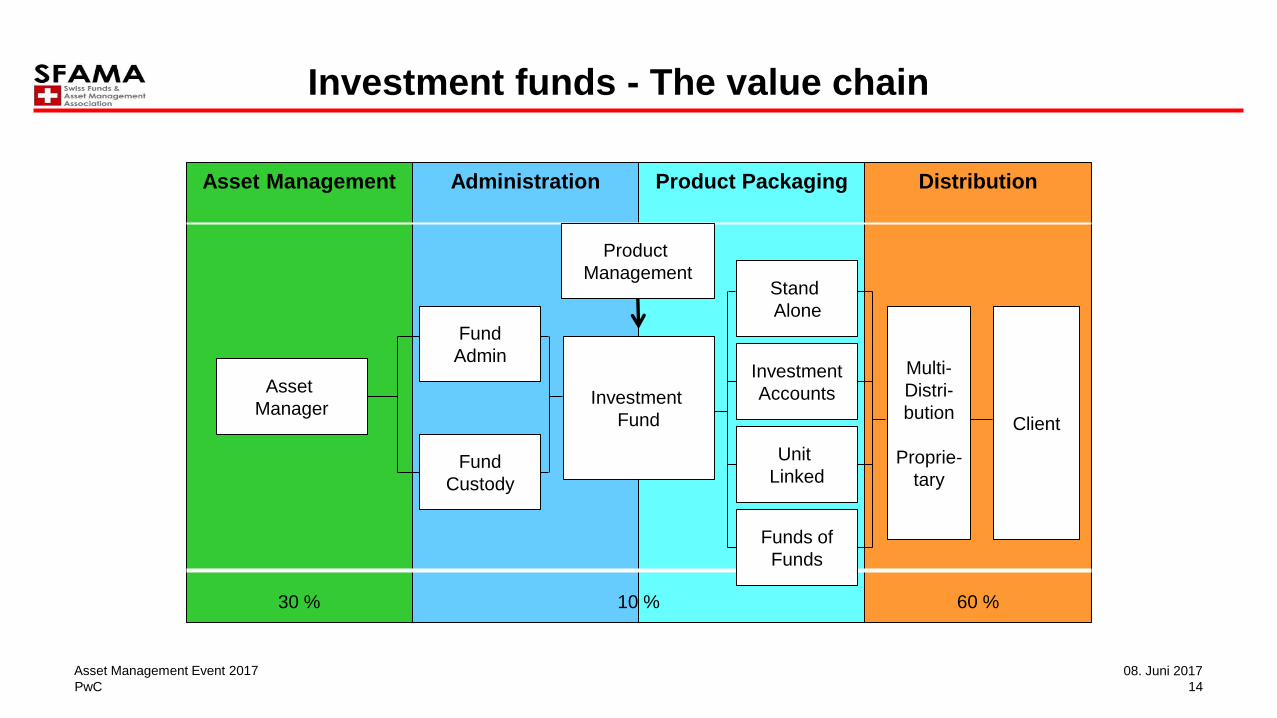

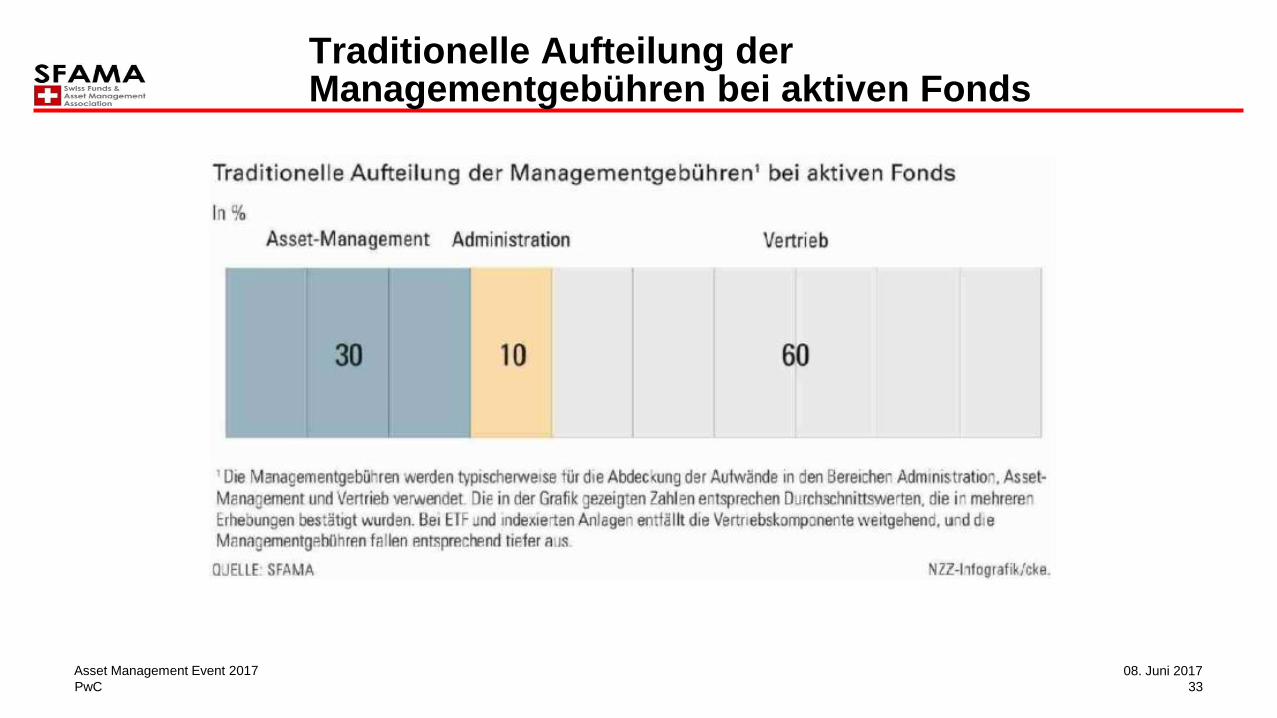

Investment funds - The value chain

Asset Management Administration Product Packaging Distribution

30 % 10 % 60 %

Asset

Manager

Product

Management

Fund

Admin

Fund

Custody

Investment

Fund

Stand

Alone

Investment

Accounts

Unit

Linked

Funds of

Funds

Multi-

Distri-

bution

Proprie-

tary

Client

14

08. Juni 2017Asset Management Event 2017

PwC

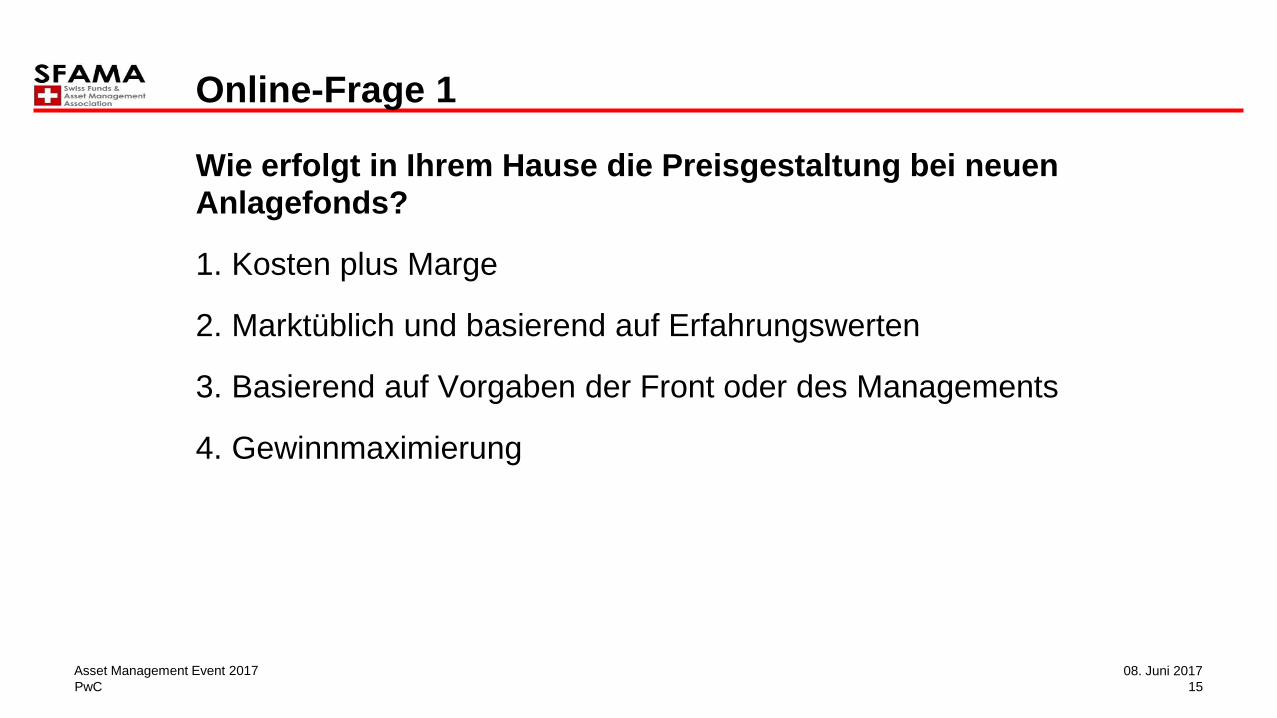

Wie erfolgt in Ihrem Hause die Preisgestaltung bei neuen Anlagefonds?

1. Kosten plus Marge

2. Marktüblich und basierend auf Erfahrungswerten

3. Basierend auf Vorgaben der Front oder des Managements

4. Gewinnmaximierung

Online-Frage 1

15

08. Juni 2017Asset Management Event 2017

PwC

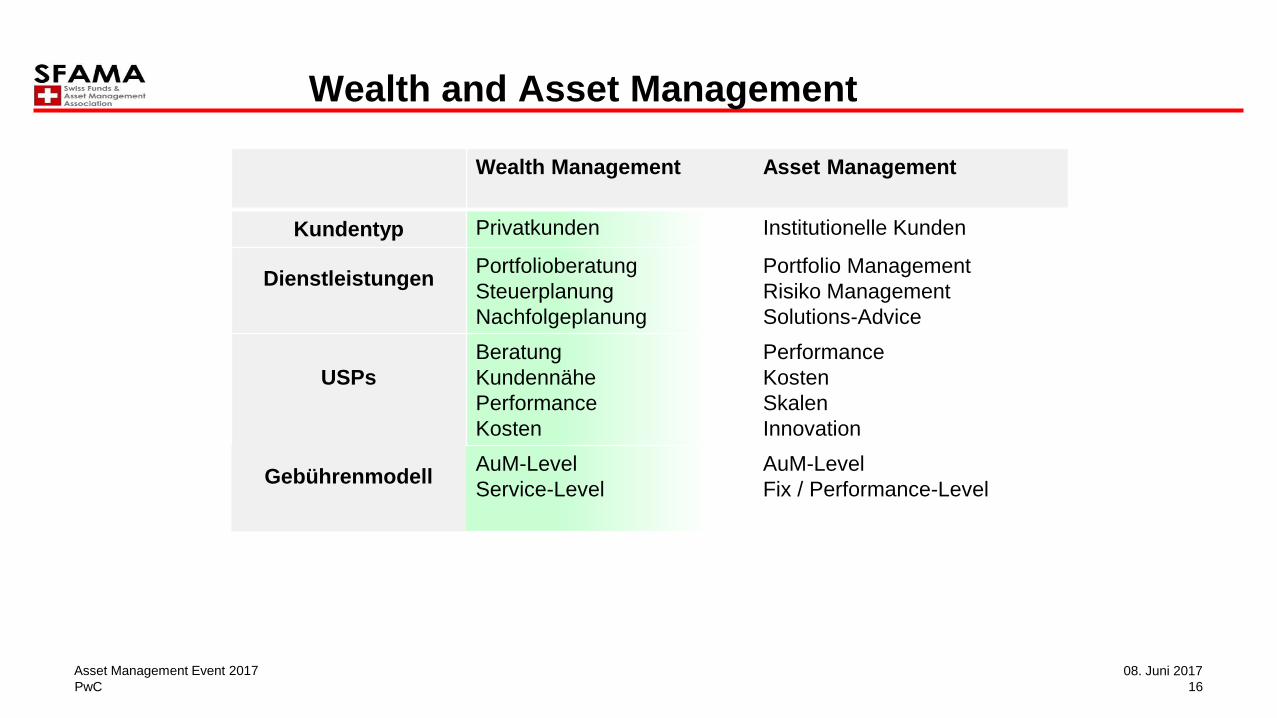

Wealth and Asset Management

Wealth Management Asset Management

Kundentyp Privatkunden Institutionelle Kunden

DienstleistungenPortfolioberatung Portfolio Management

Steuerplanung Risiko Management

Nachfolgeplanung Solutions-Advice

USPs

Beratung Performance

Kundennähe Kosten

Performance Skalen

Kosten Innovation

GebührenmodellAuM-Level AuM-Level

Service-Level Fix / Performance-Level

16

08. Juni 2017Asset Management Event 2017

PwC

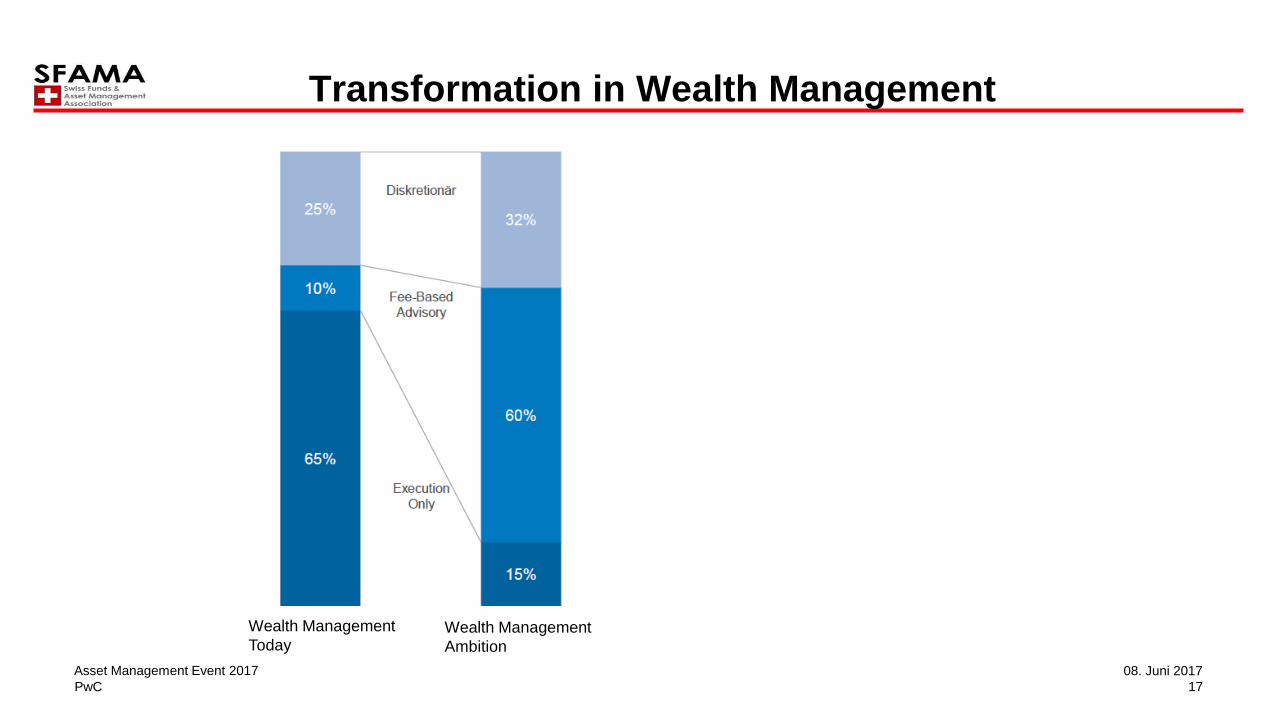

Transformation in Wealth Management

Wealth Management

TodayWealth Management

Ambition

17

08. Juni 2017Asset Management Event 2017

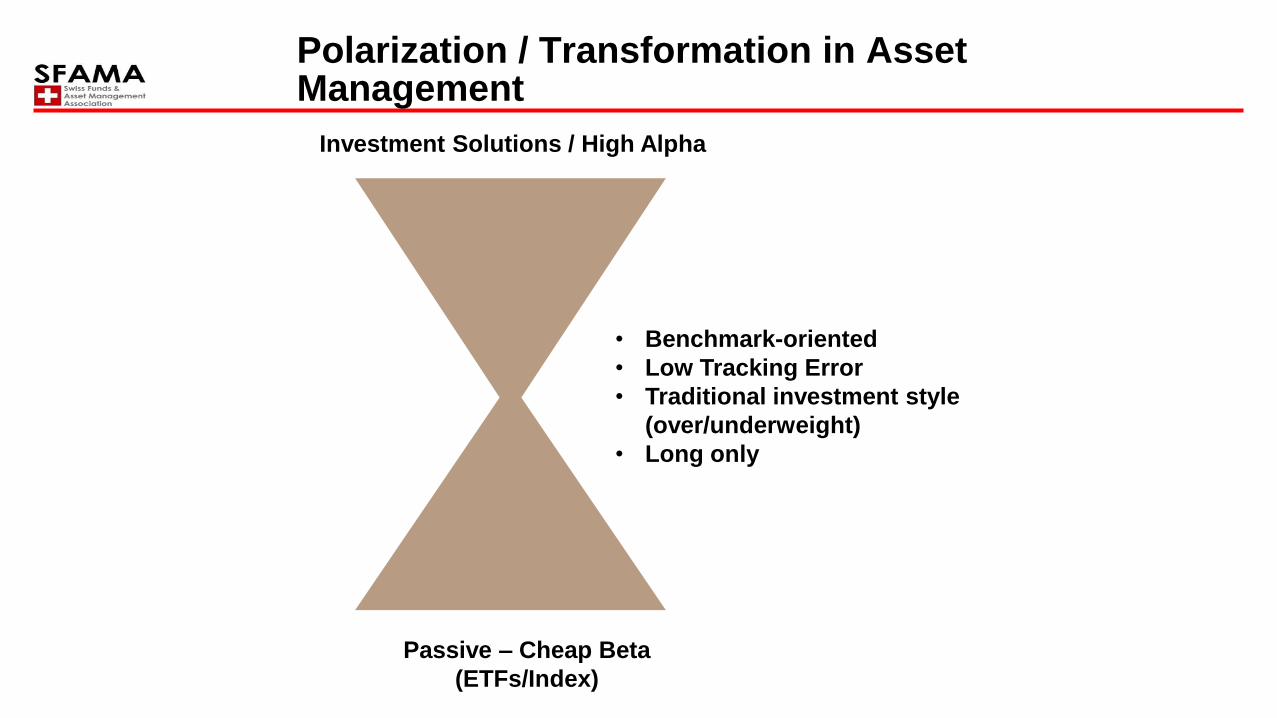

Polarization / Transformation in Asset Management

• Benchmark-oriented

• Low Tracking Error

• Traditional investment style

(over/underweight)

• Long only

Passive – Cheap Beta

(ETFs/Index)

Investment Solutions / High Alpha

PwC

Keywords / Buzzwords

• Closet Index Trackers / Closet Indexing / Index Hugging /

“Indexschmuser”

• Active versus passive Asset Management

• Fee and margin pressure: triggered by the investor, or the regulator, or

both

19

08. Juni 2017Asset Management Event 2017

PwC

Asset Management Market Studies

20

08. Juni 2017Asset Management Event 2017

PwC

«Herkömmliche» Reaktionsweisen

1. Behaupten, die Zahlen seien nicht wahr oder unkorrekt

2. Aufzeigen der Schwächen zur Methodologie

3. Anerkennen, dass die Gebührendiskussion geführt werden muss

21

08. Juni 2017Asset Management Event 2017

PwC

Wie reagieren Sie / Ihre PR-Stelle üblicherweise bei Vorwürfen wegen zu hohen Fondsgebühren?

1. Wir machen darauf aufmerksam, dass die Zahlen nicht

korrekt sind oder dass diese nicht isoliert betrachtet werden dürfen

2. Wir machen darauf aufmerksam, dass die Berechnungsmethodologie unkorrekt oder nicht adäquat ist

3. Wir machen darauf aufmerksam, dass wir die Gebührenhöhe regelmässig überprüfen

4. Wir betonen, dass unsere Kosten nicht zu hoch, sondern marktüblich sind

Online-Frage 2

22

08. Juni 2017Asset Management Event 2017

PwC

Zitate aus der Presse

• Nur schlechte Fonds sind zu teuer. Wir überprüfen unsere Fondspalette

regelmässig.

• Wir überprüfen unsere Gebührenstrukturen regelmässig und passen

unsere Preise an.

• Für unsere Mandatskunden setzen wir ausschliesslich retrofreie Fonds

ein.

• Der Trend geht in Richtung Beratungsmandate (“fee-based-advice”).

Retrofreie Produkte setzen sich deshalb zunehmend durch.

• Das Marktumfeld ist schwierig.

23

08. Juni 2017Asset Management Event 2017

PwC

Zitate aus der Presse (Fortsetzung)

• Aktive Fonds sind nicht zu teuer. Das Problem sind die im Produkt

inkludierten Vertriebsprovisionen.

• Inkludierte Vertriebsprovisionen sind gerechtfertigt, denn wir liefern

dafür auch ein Distributions-Alpha.

• If all investors adopt a purely passive approach, the market would

become highly inefficient.

24

08. Juni 2017Asset Management Event 2017

PwC

Fees & Costs: Light in the fog?

25

08. Juni 2017Asset Management Event 2017

PwC

Financial Conduct Authority (FCA) – Asset Management Market Study*

Key findings:

• Weak price competition in the retail market

• Degree of price clustering at specific levels

• Similar exposure of active and passive funds, but much higher fees for

many active products

• Unclear investment objectives

• Lack of awareness about the existence and level of charges

• Concerns about investment consultants’ incentives and conflicts of

interests

26

08. Juni 2017Asset Management Event 2017

PwC

Warum gibt es kaum „Discount“-Strategiefonds?

1. Mangelndes Bewusstsein der Investoren bezüglich Kosten und Gebühren / keine Nachfrage

2. Hohe Produktionskosten für diese Fondsklasse

3. Inkludierte Vertriebsentschädigungen

4. Interne Überlegungen

Online-Frage 3

27

08. Juni 2017Asset Management Event 2017

PwC

Financial Conduct Authority (FCA) – Asset Management Market Study*

Proposed remedies:

• Strengthening the duty to act in investors’ best interests

• Making it easier for retail investors to switch into better value share

classes

• Clearer communication of fund charges and their impact in pounds and

pence terms

• Enhancing transparency of fees

• Work on understanding the roles and costs of third party providers

involved in distribution to retail investors

28

08. Juni 2017Asset Management Event 2017

PwC

To sum up / At a glance

• Local regulators are implementing or studying cost-disclosure

frameworks

• Investors are becoming increasingly aware of their total costs

• Studies are finding increasing evidence of a lack of transparency

• There is little agreement on appropriate fee structures

• Legislation will push to unbundle management fees

• In countries without or few retrocession legislation already in place (e.g.

Switzerland), banks and asset managers take pre-emptive action to

reposition themselves ahead of the change

29

08. Juni 2017Asset Management Event 2017

PwC

Conclusions / Discussion points

• Questions are being asked about asset managers’ business models, as

investors raise doubts on their ability to deliver value for money.

• The (FCA) findings include, on average after charges, there was no

significant return over benchmark for institutional active investment

products.

• Active managers can outperform, but they keep all of the

outperformance and more for themselves, on average, rather than for

their clients.

• FCA finds that UK active funds have, on average, outperformed their

benchmarks before charges, they nevertheless underperformed after

charges.

30

08. Juni 2017Asset Management Event 2017

PwC

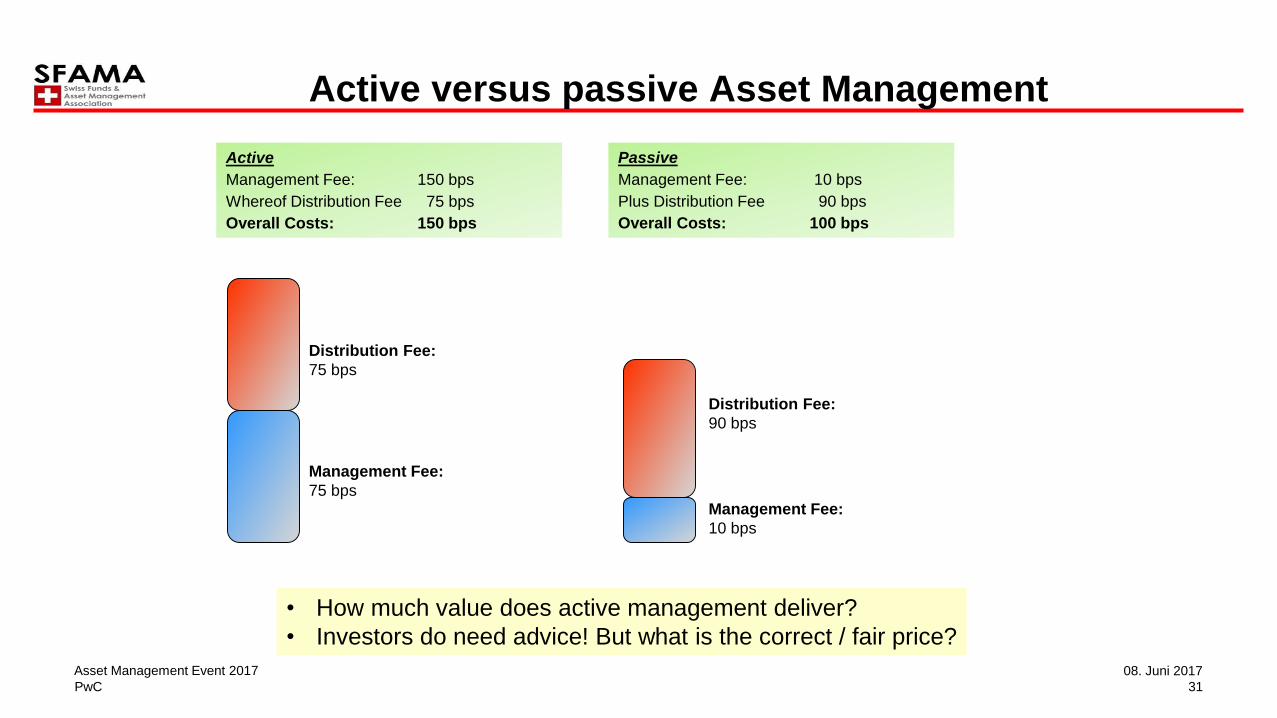

Active versus passive Asset Management

Active

Management Fee: 150 bps

Whereof Distribution Fee 75 bps

Overall Costs: 150 bps

• How much value does active management deliver?

• Investors do need advice! But what is the correct / fair price?

Passive

Management Fee: 10 bps

Plus Distribution Fee 90 bps

Overall Costs: 100 bps

Management Fee:

75 bpsManagement Fee:

10 bps

Distribution Fee:

75 bps

Distribution Fee:

90 bps

31

08. Juni 2017Asset Management Event 2017

PwC

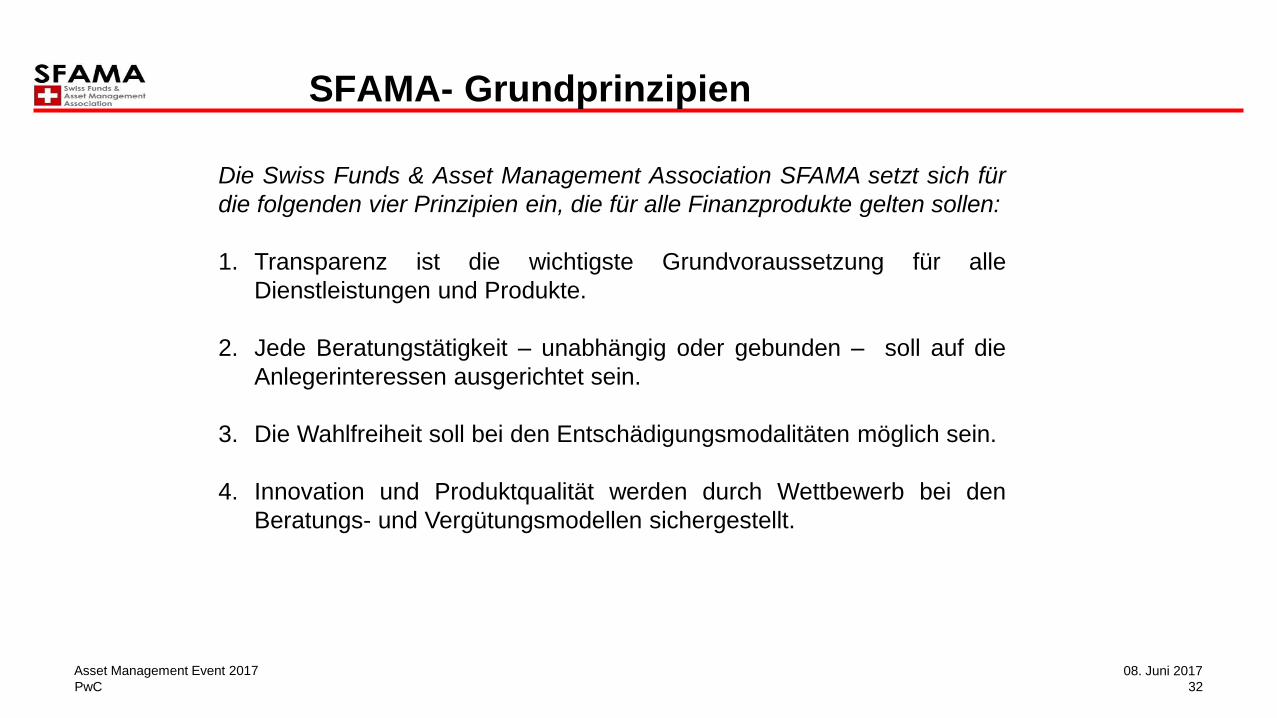

SFAMA- Grundprinzipien

Die Swiss Funds & Asset Management Association SFAMA setzt sich für

die folgenden vier Prinzipien ein, die für alle Finanzprodukte gelten sollen:

1. Transparenz ist die wichtigste Grundvoraussetzung für alle

Dienstleistungen und Produkte.

2. Jede Beratungstätigkeit – unabhängig oder gebunden – soll auf die

Anlegerinteressen ausgerichtet sein.

3. Die Wahlfreiheit soll bei den Entschädigungsmodalitäten möglich sein.

4. Innovation und Produktqualität werden durch Wettbewerb bei den

Beratungs- und Vergütungsmodellen sichergestellt.

32

08. Juni 2017Asset Management Event 2017

PwC

Traditionelle Aufteilung der Managementgebühren bei aktiven Fonds

33

08. Juni 2017Asset Management Event 2017

Herzlichen Dank für Ihre Aufmerksamkeit!

The Swiss Funds & Asset Management Association SFAMA (SFAMA), which was

established in 1992 with its registered office in Basel, is the representative

association of the Swiss fund and asset management industry. Its members include

all the major Swiss fund management companies, many asset managers, and

representatives of foreign collective investment schemes. Among SFAMA’s

members there are also numerous other service providers operating in the asset

management sector. SFAMA is an active member of the Brussels-based European

Fund and Asset Management Association (EFAMA) and the International Investment

Funds Association (IIFA) in Montreal. For further information, please visit

www.sfama.ch. You can also follow us on Twitter @SFAMAinfo.

PwC

Transparenz bei den Gebühren von Wertpapier-geschäften, aktuelle Themen zur MiFID und update zu PRIIPs16:00 – 16:35

PwC / Michael Taschner

36

08. Juni 2017Asset Management Event 2017

PwC

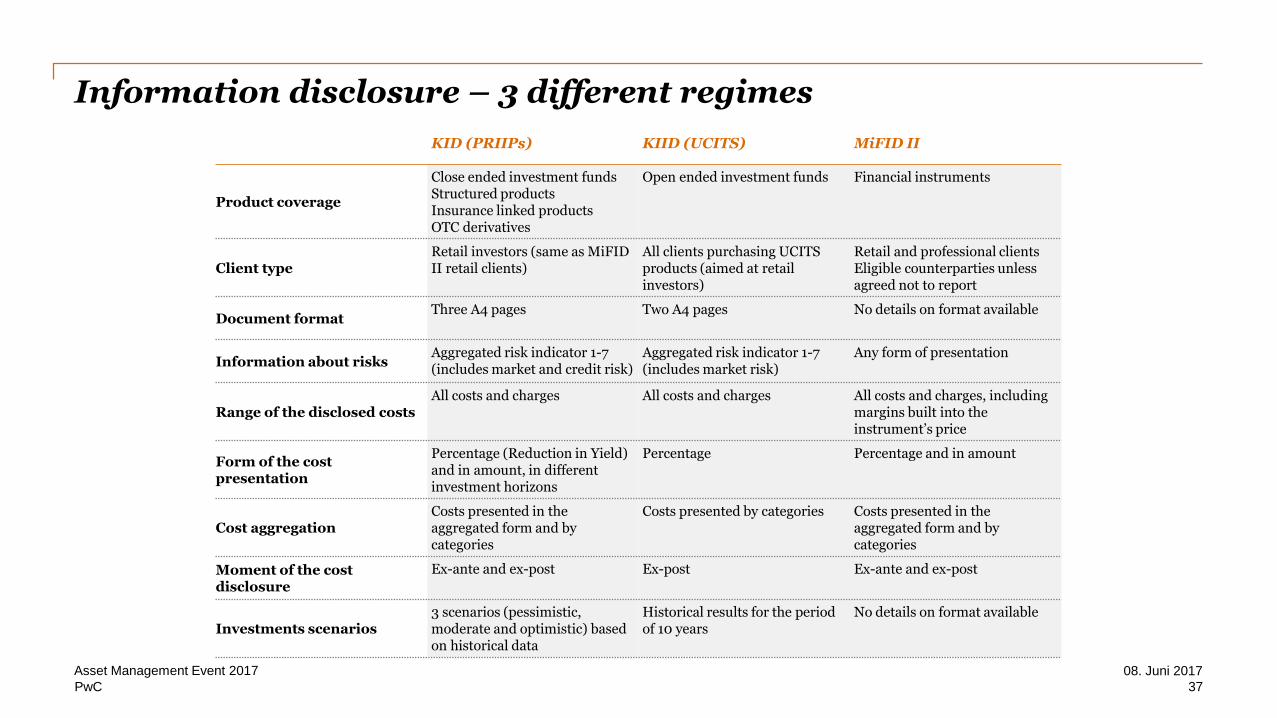

Information disclosure – 3 different regimes

KID (PRIIPs) KIID (UCITS) MiFID II

Product coverage

Close ended investment fundsStructured productsInsurance linked productsOTC derivatives

Open ended investment funds Financial instruments

Client typeRetail investors (same as MiFIDII retail clients)

All clients purchasing UCITS products (aimed at retail investors)

Retail and professional clientsEligible counterparties unless agreed not to report

Document formatThree A4 pages Two A4 pages No details on format available

Information about risksAggregated risk indicator 1-7 (includes market and credit risk)

Aggregated risk indicator 1-7 (includes market risk)

Any form of presentation

Range of the disclosed costsAll costs and charges All costs and charges All costs and charges, including

margins built into the instrument’s price

Form of the cost presentation

Percentage (Reduction in Yield) and in amount, in different investment horizons

Percentage Percentage and in amount

Cost aggregationCosts presented in the aggregated form and by categories

Costs presented by categories Costs presented in the aggregated form and by categories

Moment of the cost disclosure

Ex-ante and ex-post Ex-post Ex-ante and ex-post

Investments scenarios3 scenarios (pessimistic, moderate and optimistic) based on historical data

Historical results for the period of 10 years

No details on format available

37

08. Juni 2017Asset Management Event 2017

PwC

Cost disclosure under MiFID II

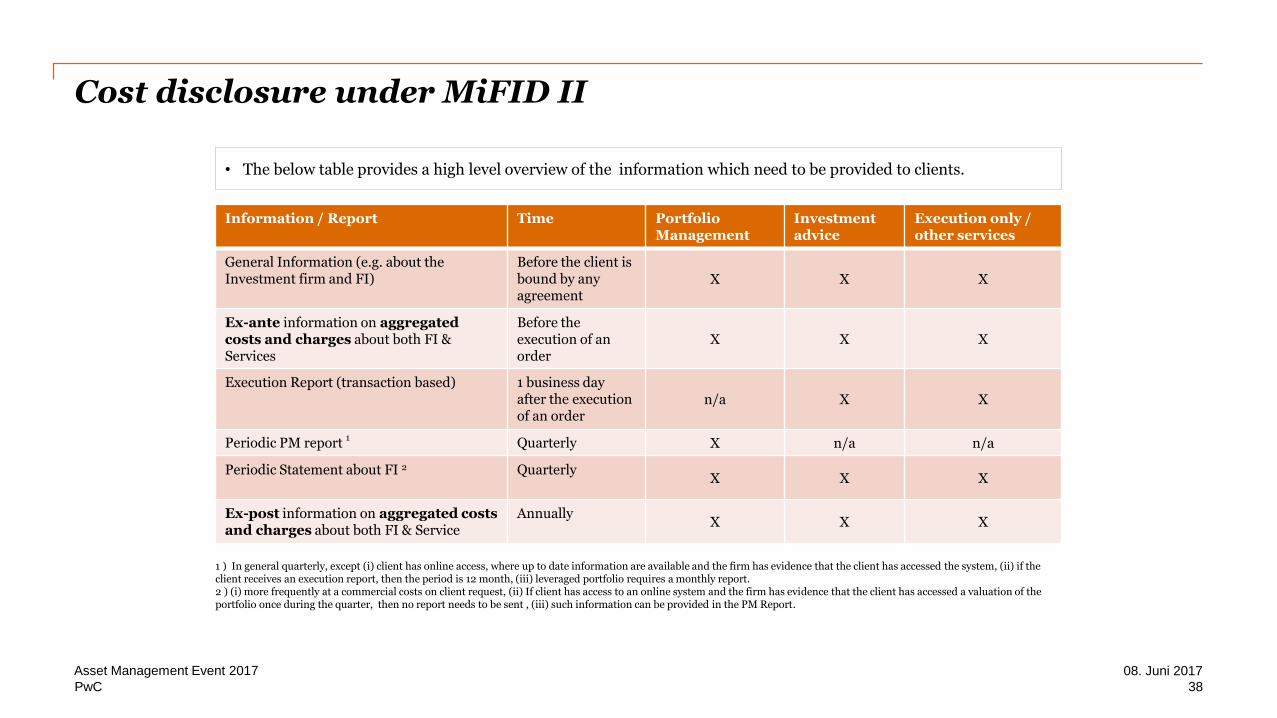

• The below table provides a high level overview of the information which need to be provided to clients.

Information / Report Time Portfolio Management

Investment advice

Execution only / other services

General Information (e.g. about the Investment firm and FI)

Before the client is bound by any agreement

X X X

Ex-ante information on aggregated costs and charges about both FI & Services

Before the execution of an order

X X X

Execution Report (transaction based) 1 business day after the execution of an order

n/a X X

Periodic PM report 1

Quarterly X n/a n/a

Periodic Statement about FI 2 QuarterlyX X X

Ex-post information on aggregated costs and charges about both FI & Service

AnnuallyX X X

1 ) In general quarterly, except (i) client has online access, where up to date information are available and the firm has evidence that the client has accessed the system, (ii) if the client receives an execution report, then the period is 12 month, (iii) leveraged portfolio requires a monthly report.2 ) (i) more frequently at a commercial costs on client request, (ii) If client has access to an online system and the firm has evidence that the client has accessed a valuation of the portfolio once during the quarter, then no report needs to be sent , (iii) such information can be provided in the PM Report.

38

08. Juni 2017Asset Management Event 2017

PwC

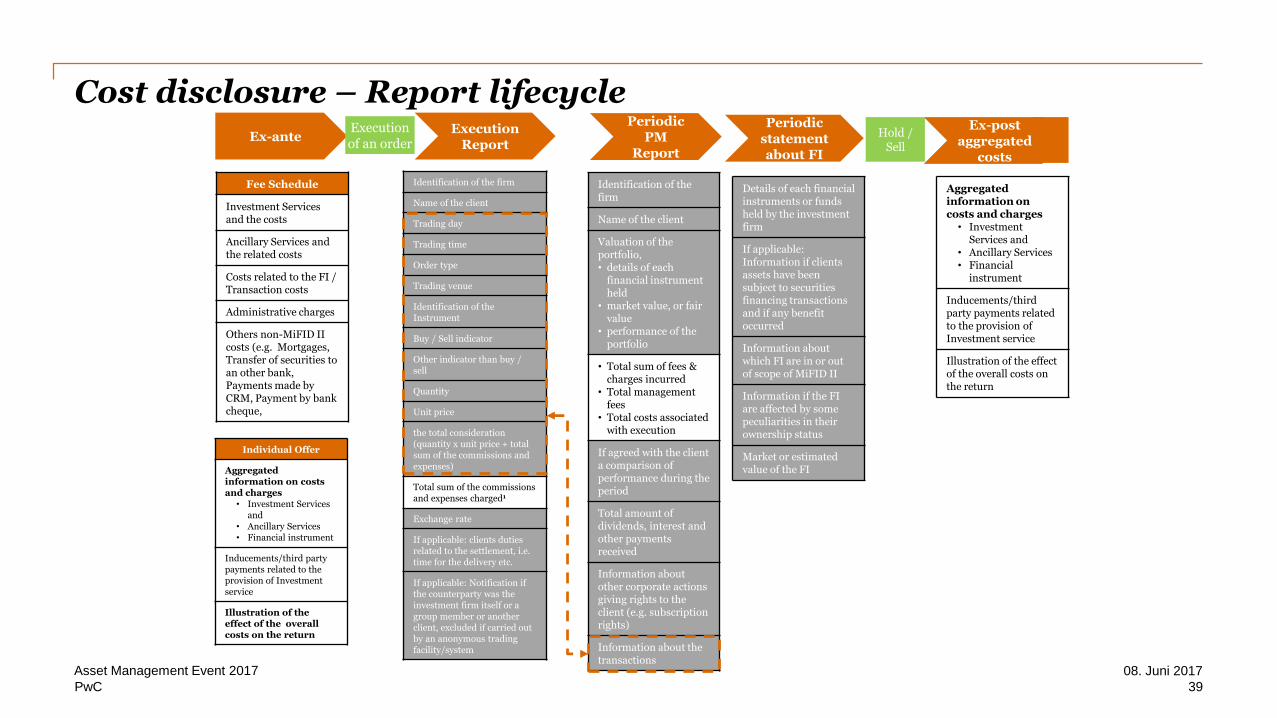

Cost disclosure – Report lifecycle

Identification of the firm

Name of the client

Trading day

Trading time

Order type

Trading venue

Identification of the Instrument

Buy / Sell indicator

Other indicator than buy / sell

Quantity

Unit price

the total consideration (quantity x unit price + total sum of the commissions and expenses)

Total sum of the commissions and expenses charged1

Exchange rate

If applicable: clients dutiesrelated to the settlement, i.e. time for the delivery etc.

If applicable: Notification if the counterparty was the investment firm itself or a group member or another client, excluded if carried out by an anonymous trading facility/system

Ex-anteExecution

Report

Periodic PM

Report

Periodic statement about FI

Ex-post aggregated

costs

Identification of the firm

Name of the client

Valuation of the portfolio, • details of each

financial instrument held

• market value, or fair value

• performance of the portfolio

• Total sum of fees & charges incurred

• Total management fees

• Total costs associated with execution

If agreed with the client a comparison of performance during the period

Total amount of dividends, interest and other payments received

Information about other corporate actions giving rights to the client (e.g. subscription rights)

Information about thetransactions

Fee Schedule

Investment Services and the costs

Ancillary Services and the related costs

Costs related to the FI / Transaction costs

Administrative charges

Others non-MiFID II costs (e.g. Mortgages, Transfer of securities to an other bank, Payments made by CRM, Payment by bank cheque,

Individual Offer

Aggregated information on costs and charges

• Investment Services and

• Ancillary Services• Financial instrument

Inducements/third party payments related to the provision of Investment service

Illustration of the effect of the overall costs on the return

Details of each financial instruments or funds held by the investment firm

If applicable: Information if clients assets have been subject to securities financing transactionsand if any benefit occurred

Information about which FI are in or out of scope of MiFID II

Information if the FIare affected by some peculiarities in their ownership status

Market or estimated value of the FI

Aggregated information on costs and charges

• Investment Services and

• Ancillary Services• Financial

instrument

Inducements/third party payments related to the provision of Investment service

Illustration of the effect of the overall costs on the return

Execution of an order

Hold /Sell

39

08. Juni 2017Asset Management Event 2017

PwC

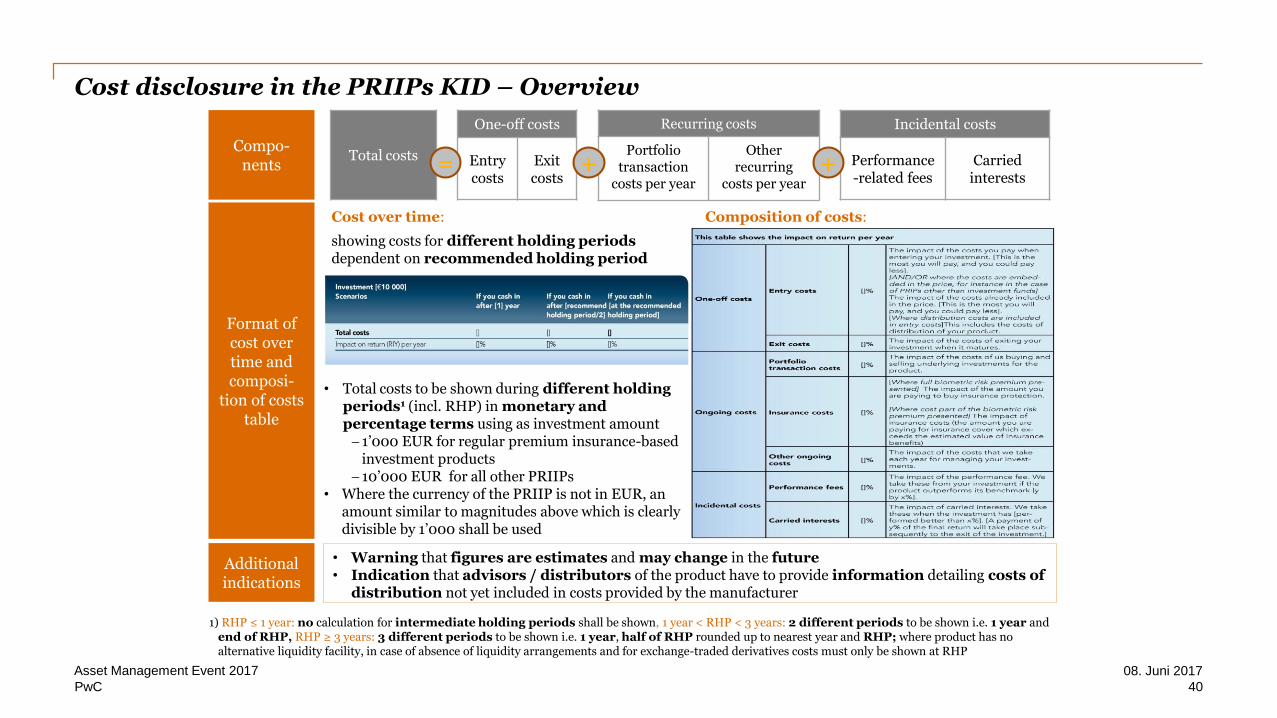

Cost disclosure in the PRIIPs KID – Overview

One-off costs

Entry costs

Exit costs

Recurring costs

Portfolio transaction

costs per year

Other recurring

costs per year

Incidental costs

Performance-related fees

Carriedinterests

Total costs = + +

Format of cost over time and composi-

tion of costs table

Composition of costs:

• Warning that figures are estimates and may change in the future• Indication that advisors / distributors of the product have to provide information detailing costs of

distribution not yet included in costs provided by the manufacturer

Compo-nents

Additional indications

Cost over time:

showing costs for different holding periods dependent on recommended holding period

• Total costs to be shown during different holding periods1 (incl. RHP) in monetary and percentage terms using as investment amount 1’000 EUR for regular premium insurance-based

investment products 10’000 EUR for all other PRIIPs

• Where the currency of the PRIIP is not in EUR, an amount similar to magnitudes above which is clearly divisible by 1’000 shall be used

1) RHP ≤ 1 year: no calculation for intermediate holding periods shall be shown, 1 year < RHP < 3 years: 2 different periods to be shown i.e. 1 year and end of RHP, RHP ≥ 3 years: 3 different periods to be shown i.e. 1 year, half of RHP rounded up to nearest year and RHP; where product has no alternative liquidity facility, in case of absence of liquidity arrangements and for exchange-traded derivatives costs must only be shown at RHP

40

08. Juni 2017Asset Management Event 2017

PwC

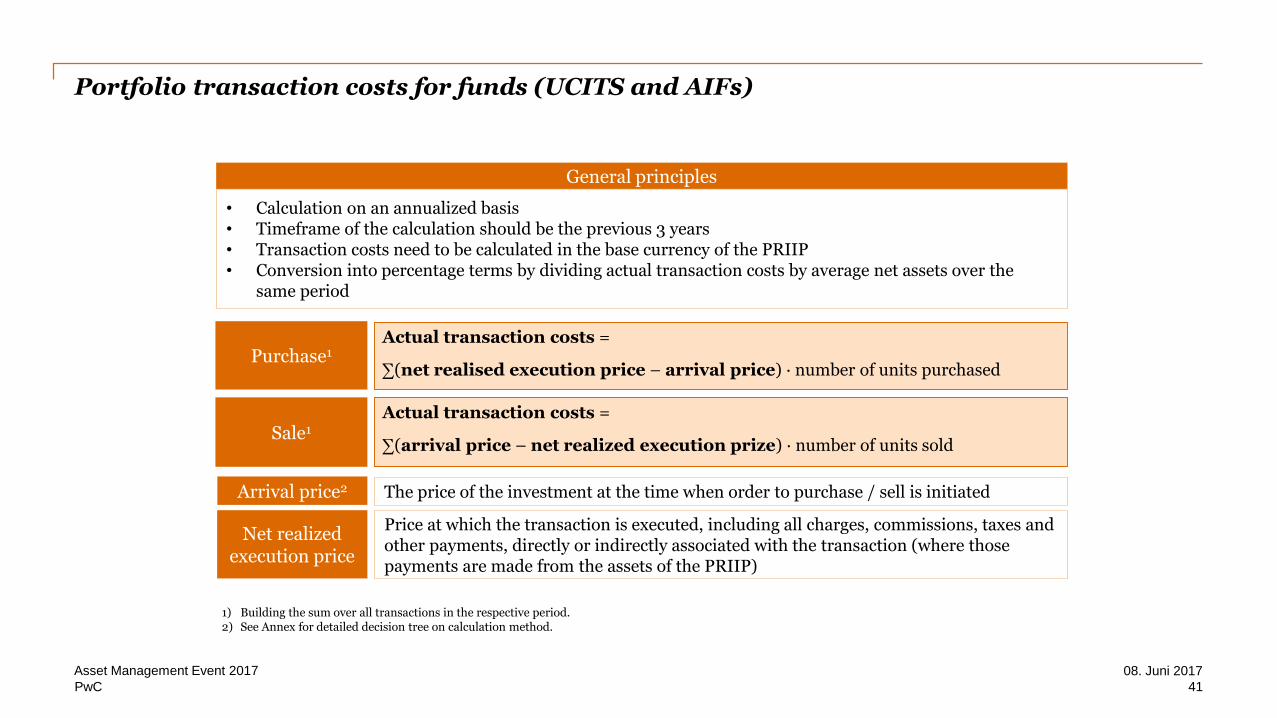

Portfolio transaction costs for funds (UCITS and AIFs)

Arrival price2 The price of the investment at the time when order to purchase / sell is initiated

• Calculation on an annualized basis • Timeframe of the calculation should be the previous 3 years• Transaction costs need to be calculated in the base currency of the PRIIP• Conversion into percentage terms by dividing actual transaction costs by average net assets over the

same period

General principles

Price at which the transaction is executed, including all charges, commissions, taxes and other payments, directly or indirectly associated with the transaction (where those payments are made from the assets of the PRIIP)

Net realized execution price

Actual transaction costs =

∑(net realised execution price – arrival price) ∙ number of units purchasedPurchase1

Sale1

Actual transaction costs =

∑(arrival price – net realized execution prize) ∙ number of units sold

1) Building the sum over all transactions in the respective period.2) See Annex for detailed decision tree on calculation method.

41

08. Juni 2017Asset Management Event 2017

PwC

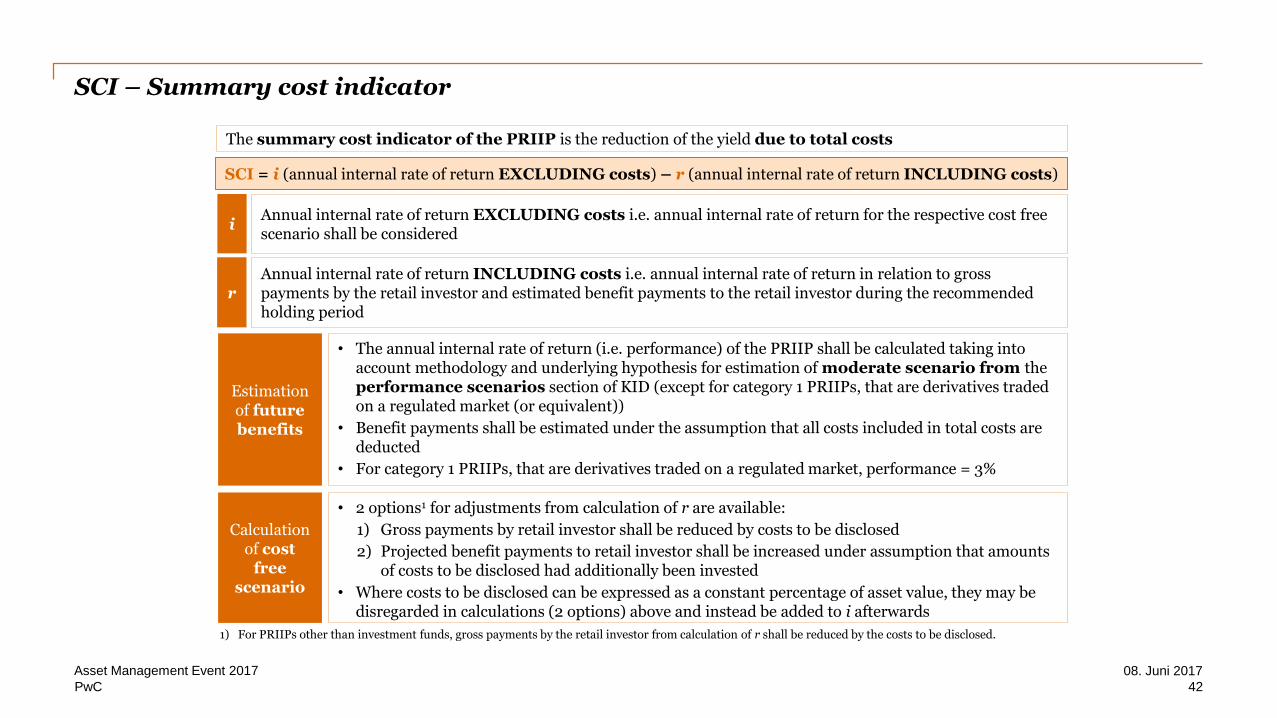

SCI – Summary cost indicator

iAnnual internal rate of return EXCLUDING costs i.e. annual internal rate of return for the respective cost free scenario shall be considered

The summary cost indicator of the PRIIP is the reduction of the yield due to total costs

Annual internal rate of return INCLUDING costs i.e. annual internal rate of return in relation to gross payments by the retail investor and estimated benefit payments to the retail investor during the recommended holding period

r

SCI = i (annual internal rate of return EXCLUDING costs) – r (annual internal rate of return INCLUDING costs)

Estimation of future benefits

• The annual internal rate of return (i.e. performance) of the PRIIP shall be calculated taking into account methodology and underlying hypothesis for estimation of moderate scenario from theperformance scenarios section of KID (except for category 1 PRIIPs, that are derivatives traded on a regulated market (or equivalent))

• Benefit payments shall be estimated under the assumption that all costs included in total costs are deducted

• For category 1 PRIIPs, that are derivatives traded on a regulated market, performance = 3%

Calculation of cost

free scenario

• 2 options1 for adjustments from calculation of r are available:

1) Gross payments by retail investor shall be reduced by costs to be disclosed

2) Projected benefit payments to retail investor shall be increased under assumption that amounts of costs to be disclosed had additionally been invested

• Where costs to be disclosed can be expressed as a constant percentage of asset value, they may be disregarded in calculations (2 options) above and instead be added to i afterwards

1) For PRIIPs other than investment funds, gross payments by the retail investor from calculation of r shall be reduced by the costs to be disclosed.

42

08. Juni 2017Asset Management Event 2017

PwC

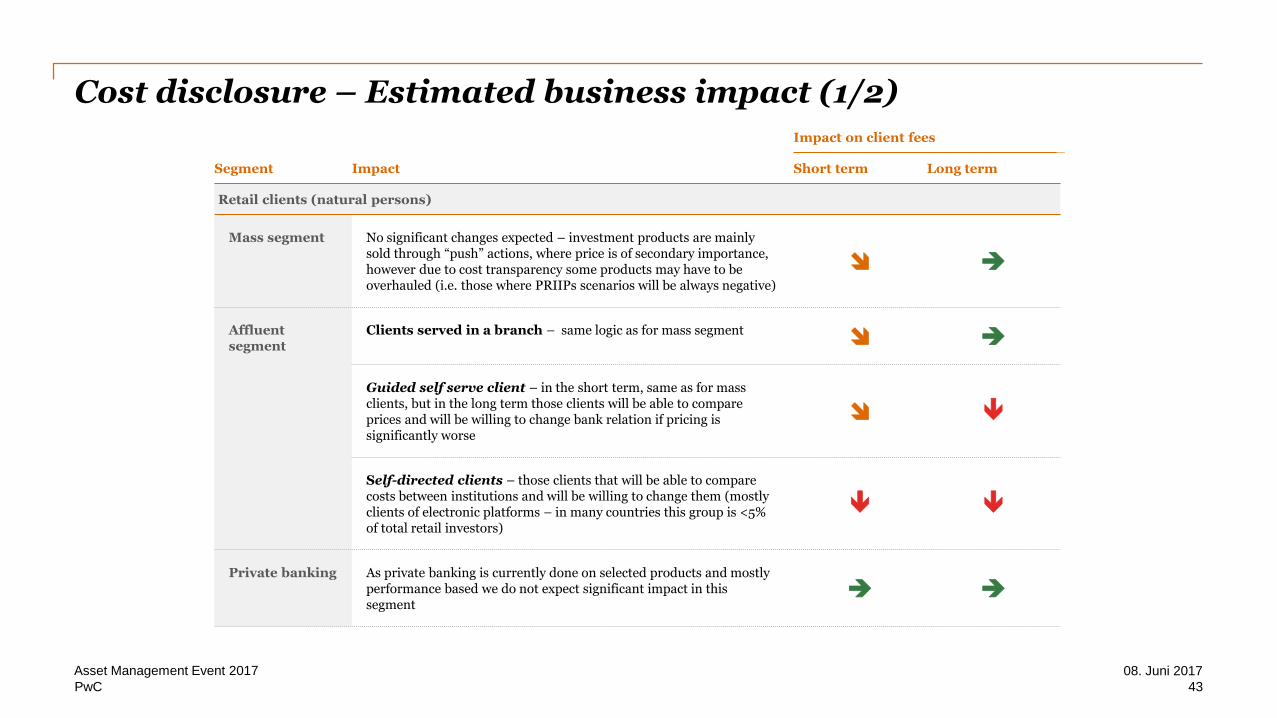

Cost disclosure – Estimated business impact (1/2)

Segment Impact

Impact on client fees

Short term Long term

Retail clients (natural persons)

Mass segment No significant changes expected – investment products are mainly sold through “push” actions, where price is of secondary importance, however due to cost transparency some products may have to be overhauled (i.e. those where PRIIPs scenarios will be always negative)

Affluent segment

Clients served in a branch – same logic as for mass segment

Guided self serve client – in the short term, same as for massclients, but in the long term those clients will be able to compare prices and will be willing to change bank relation if pricing is significantly worse

Self-directed clients – those clients that will be able to comparecosts between institutions and will be willing to change them (mostly clients of electronic platforms – in many countries this group is <5% of total retail investors)

Private banking As private banking is currently done on selected products and mostly performance based we do not expect significant impact in this segment

43

08. Juni 2017Asset Management Event 2017

PwC

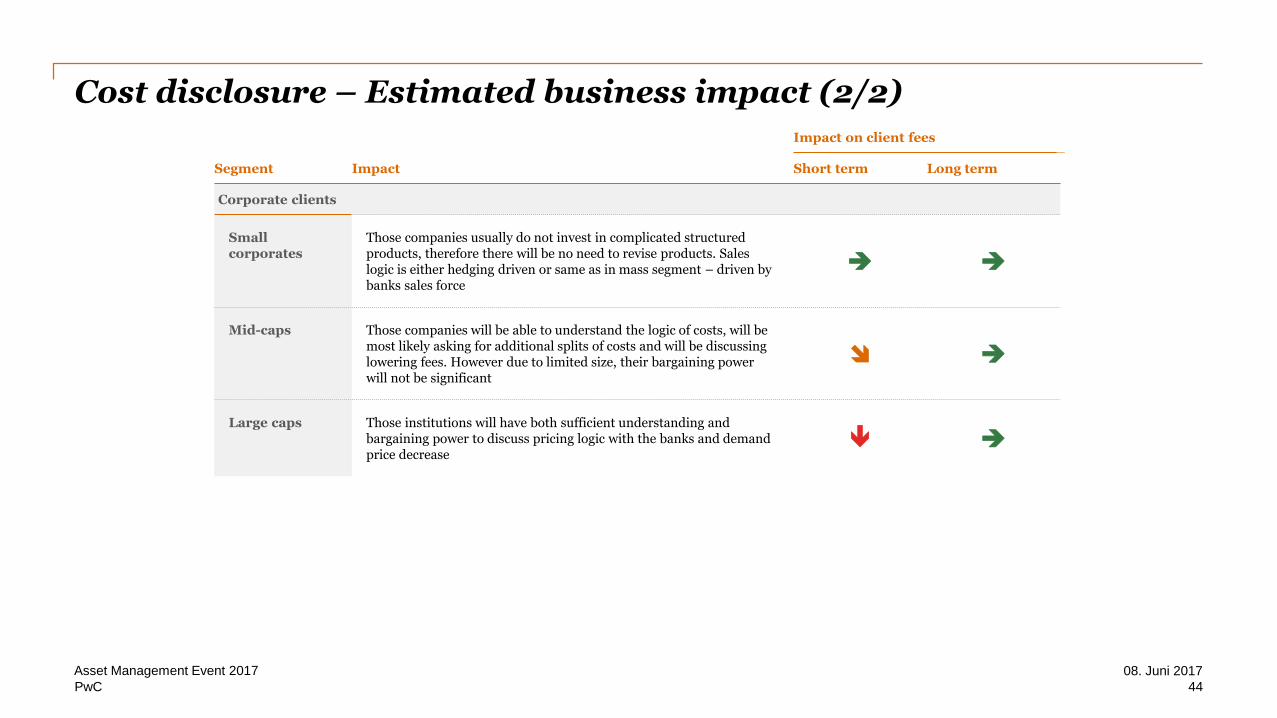

Cost disclosure – Estimated business impact (2/2)

Segment Impact

Impact on client fees

Short term Long term

Corporate clients

Small corporates

Those companies usually do not invest in complicated structuredproducts, therefore there will be no need to revise products. Sales logic is either hedging driven or same as in mass segment – driven by banks sales force

Mid-caps Those companies will be able to understand the logic of costs, will be most likely asking for additional splits of costs and will be discussing lowering fees. However due to limited size, their bargaining power will not be significant

Large caps Those institutions will have both sufficient understanding and bargaining power to discuss pricing logic with the banks and demand price decrease

44

08. Juni 2017Asset Management Event 2017

PwC 45

08. Juni 2017Asset Management Event 2017

PRIIP Regulatory update

PwC

The 8th March 2017 the EC published the amended RTS, bringing few – but significant – updates on the following:

• Multi-Option Products: UCITS KIIDs can be used for underlying investments that are UCITS or non-UCITS instead of PRIIP KID;

• Performance scenarios: addition of a 4th scenario – the “stressed scenario”;

• More details regarding the disclosure of the Comprehension Alert;

• Insurance costs removed from the “Composition of Costs” table.

Next steps?

The European Parliament and the Council of the European Union have three months – until earlyJune 2017 - to accept or reject these “final” RTS.

More presumably, RTS will be accepted quite rapidly.

ESAs are currently working on Level III measures which will be issued once RTS have beenapproved by European bodies.

Regulatory update

5008. Juni 2017Asset Management Event 2017

PwC

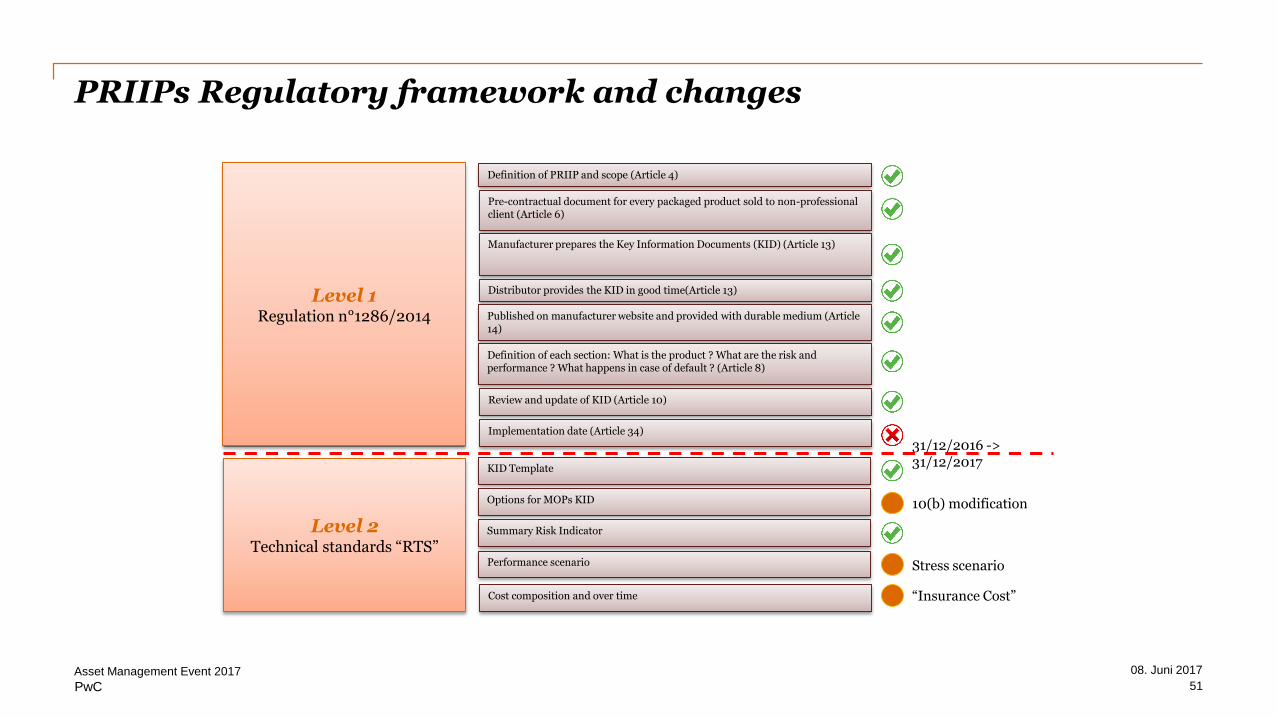

PRIIPs Regulatory framework and changes

Level 1Regulation n°1286/2014

Level 2Technical standards “RTS”

Definition of PRIIP and scope (Article 4)

Pre-contractual document for every packaged product sold to non-professional client (Article 6)

Manufacturer prepares the Key Information Documents (KID) (Article 13)

Distributor provides the KID in good time(Article 13)

Published on manufacturer website and provided with durable medium (Article 14)

Definition of each section: What is the product ? What are the risk and performance ? What happens in case of default ? (Article 8)

Review and update of KID (Article 10)

Implementation date (Article 34)

KID Template

Options for MOPs KID

Summary Risk Indicator

Performance scenario

Cost composition and over time

31/12/2016 -> 31/12/2017

10(b) modification

Stress scenario

“Insurance Cost”

51

08. Juni 2017Asset Management Event 2017

PwC

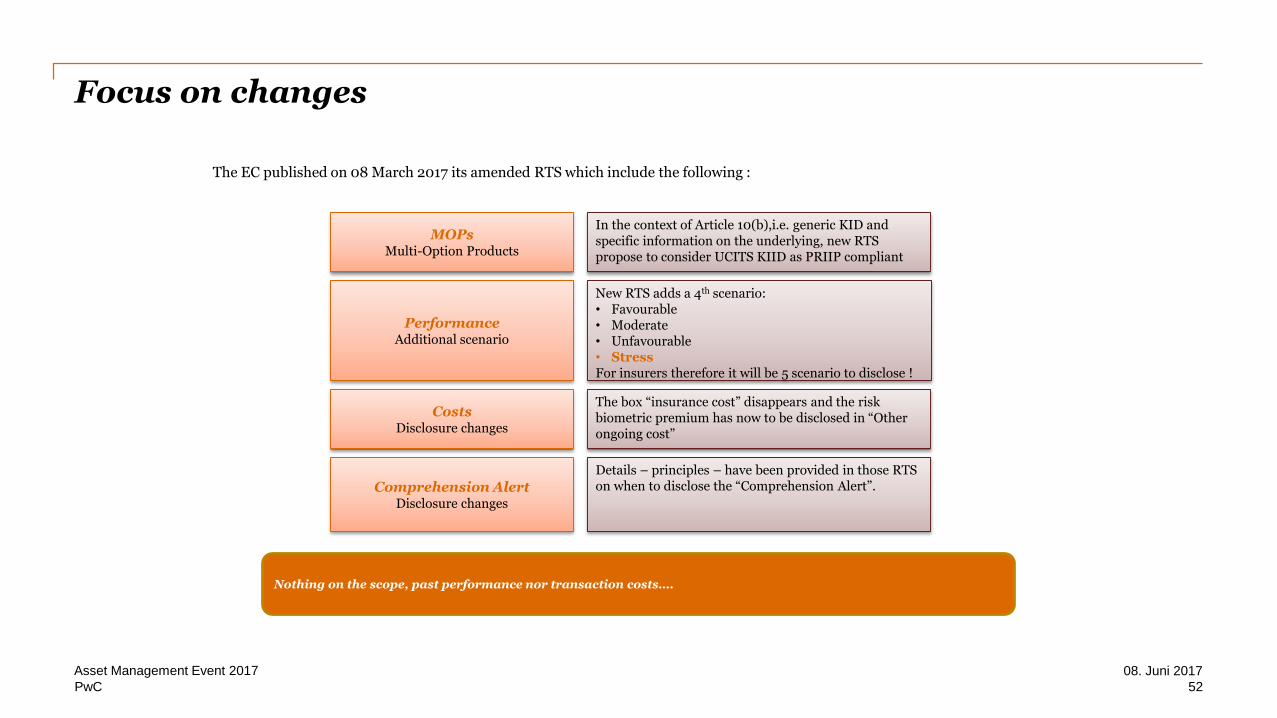

The EC published on 08 March 2017 its amended RTS which include the following :

Focus on changes

MOPsMulti-Option Products

In the context of Article 10(b),i.e. generic KID and specific information on the underlying, new RTS propose to consider UCITS KIID as PRIIP compliant

Nothing on the scope, past performance nor transaction costs….

PerformanceAdditional scenario

New RTS adds a 4th scenario:• Favourable• Moderate• Unfavourable• StressFor insurers therefore it will be 5 scenario to disclose !

CostsDisclosure changes

The box “insurance cost” disappears and the risk biometric premium has now to be disclosed in “Other ongoing cost”

Comprehension AlertDisclosure changes

Details – principles – have been provided in those RTS on when to disclose the “Comprehension Alert”.

52

08. Juni 2017Asset Management Event 2017

PwC 53

08. Juni 2017Asset Management Event 2017

MiFID II Transparancy Requirements for Trading and Brokerage Commissions

PwC

Summary of analysis

54

PwC conducted an analysis aiming to diagnose methods of payment for research and RPA account usage on different European markets.

According to the analysis, there is still a lot of uncertainty in the markets with regard to the final solutions:

Many asset managers plan to pay for research using their own funds. Some of them intend to take advantage of adjusted CSA contracts (RPA involved). The rest of market participants is about to create RPA accounts which would be funded with additional funds acquired form clients

If a RPA is implemented, the method of payment for research and form of funding will probably depend on a type of client (retail clients – changes in prospectus, institutional clients – changes of contracts)

Every increase in research budget for RPA means that clients have to be informed about the fact via letter

Costs of research will be calculated and allocated on clients by either asset managers or by transfer agents

Methods of allocation of research costs may be very simple (based only on size of assets under management) or more complex (analysis of research content, frequency of receiving research, end-users of research)

PwC

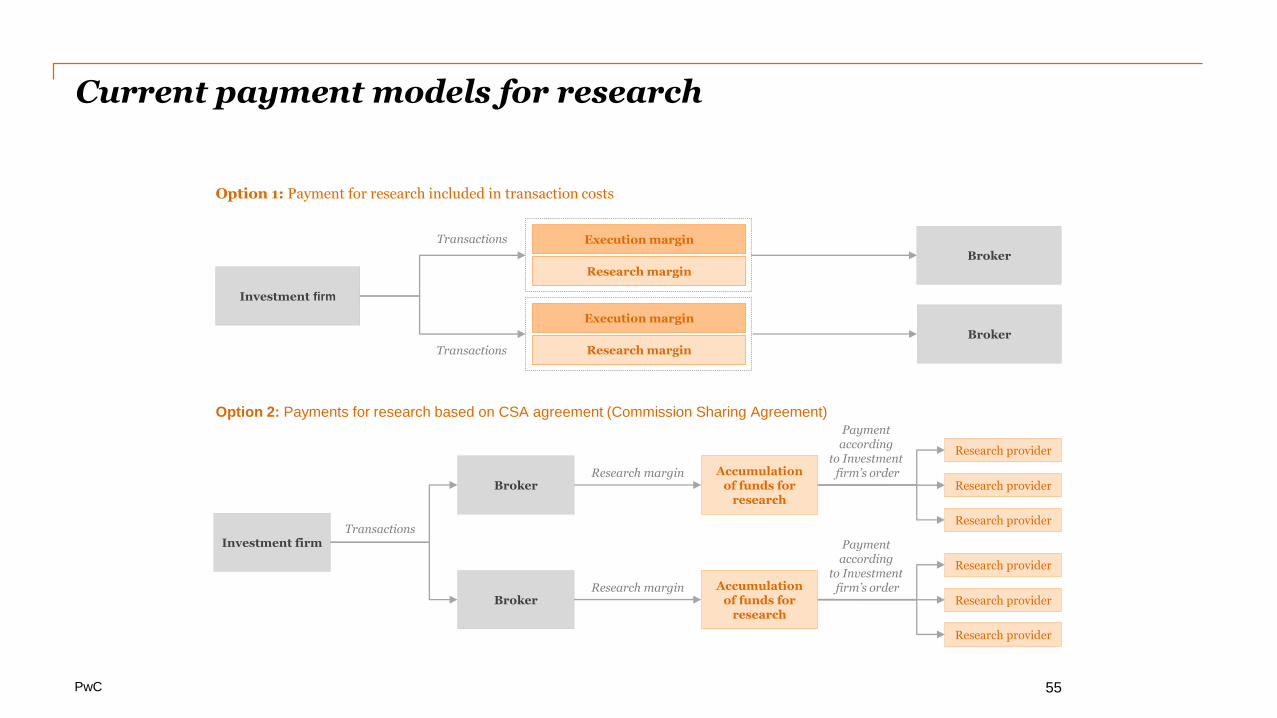

Current payment models for research

Option 1: Payment for research included in transaction costs

Investment firm

Broker

Research provider

Research provider

Research provider

Accumulation of funds for

research

Broker

Research provider

Research provider

Research provider

Accumulation of funds for

research

Transactions

Research margin

Research margin

Payment according

to Investment firm’s order

Payment according

to Investment firm’s order

Option 2: Payments for research based on CSA agreement (Commission Sharing Agreement)

Broker

Investment firm

Broker

Transactions

Transactions

Execution margin

Research margin

Execution margin

Research margin

55

PwC

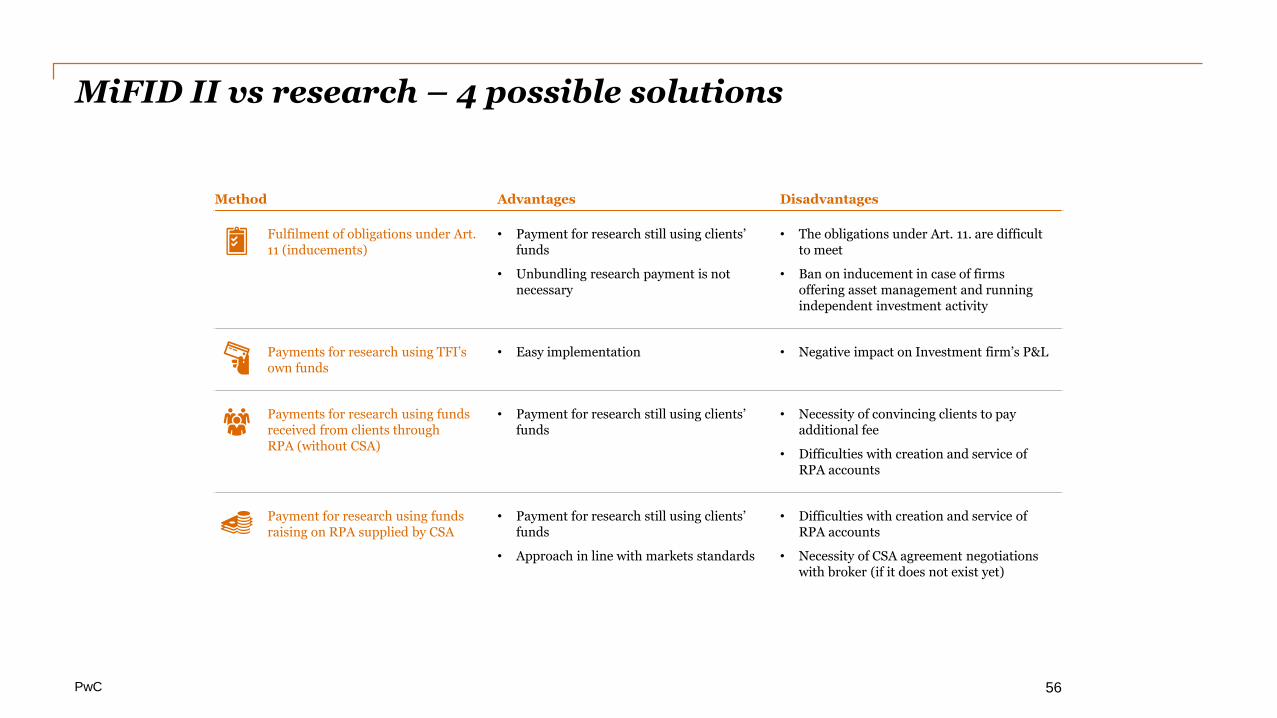

MiFID II vs research – 4 possible solutions

56

Method Advantages Disadvantages

Fulfilment of obligations under Art. 11 (inducements)

• Payment for research still using clients’ funds

• Unbundling research payment is not necessary

• The obligations under Art. 11. are difficult to meet

• Ban on inducement in case of firms offering asset management and running independent investment activity

Payments for research using TFI’s own funds

• Easy implementation • Negative impact on Investment firm’s P&L

Payments for research using funds received from clients throughRPA (without CSA)

• Payment for research still using clients’ funds

• Necessity of convincing clients to pay additional fee

• Difficulties with creation and service of RPA accounts

Payment for research using funds raising on RPA supplied by CSA

• Payment for research still using clients’ funds

• Approach in line with markets standards

• Difficulties with creation and service of RPA accounts

• Necessity of CSA agreement negotiations with broker (if it does not exist yet)

PwC

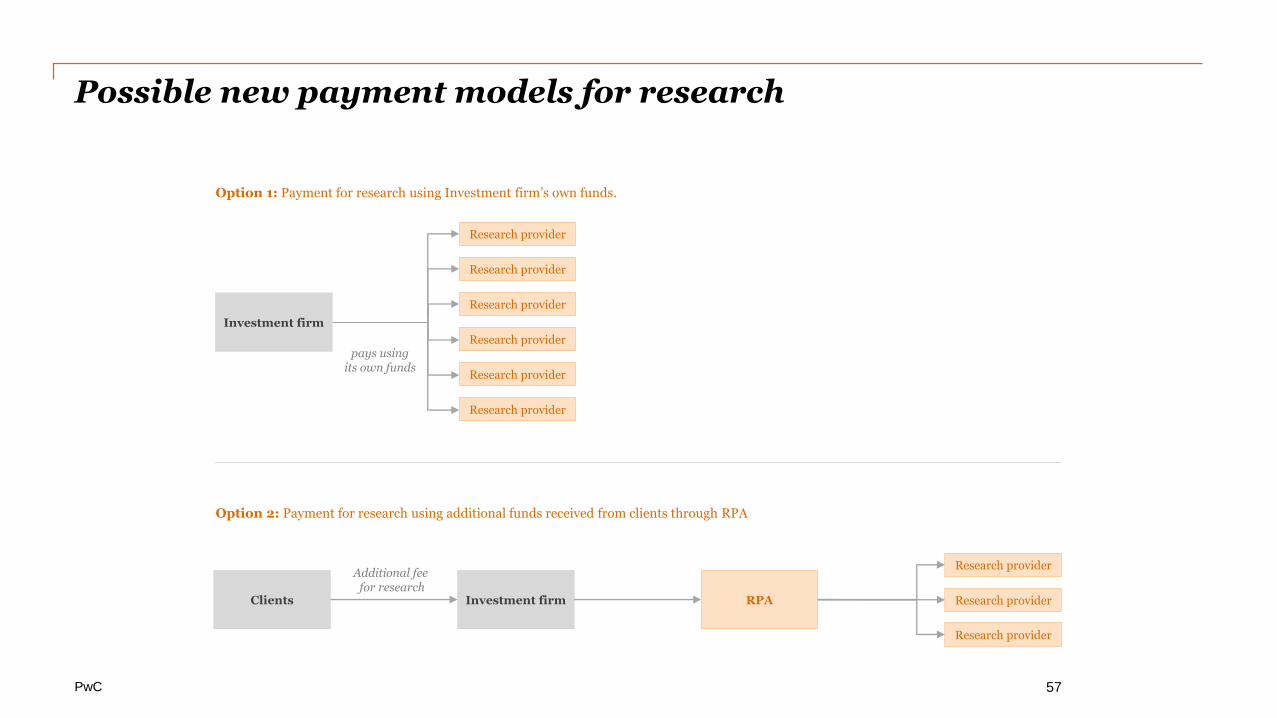

Possible new payment models for research

Option 2: Payment for research using additional funds received from clients through RPA

Option 1: Payment for research using Investment firm’s own funds.

Clients Investment firm

Research provider

Research provider

Research provider

RPA

Additional fee for research

Research provider

Research provider

Research provider

Investment firm

Research provider

Research provider

Research provider

pays using its own funds

57

PwC

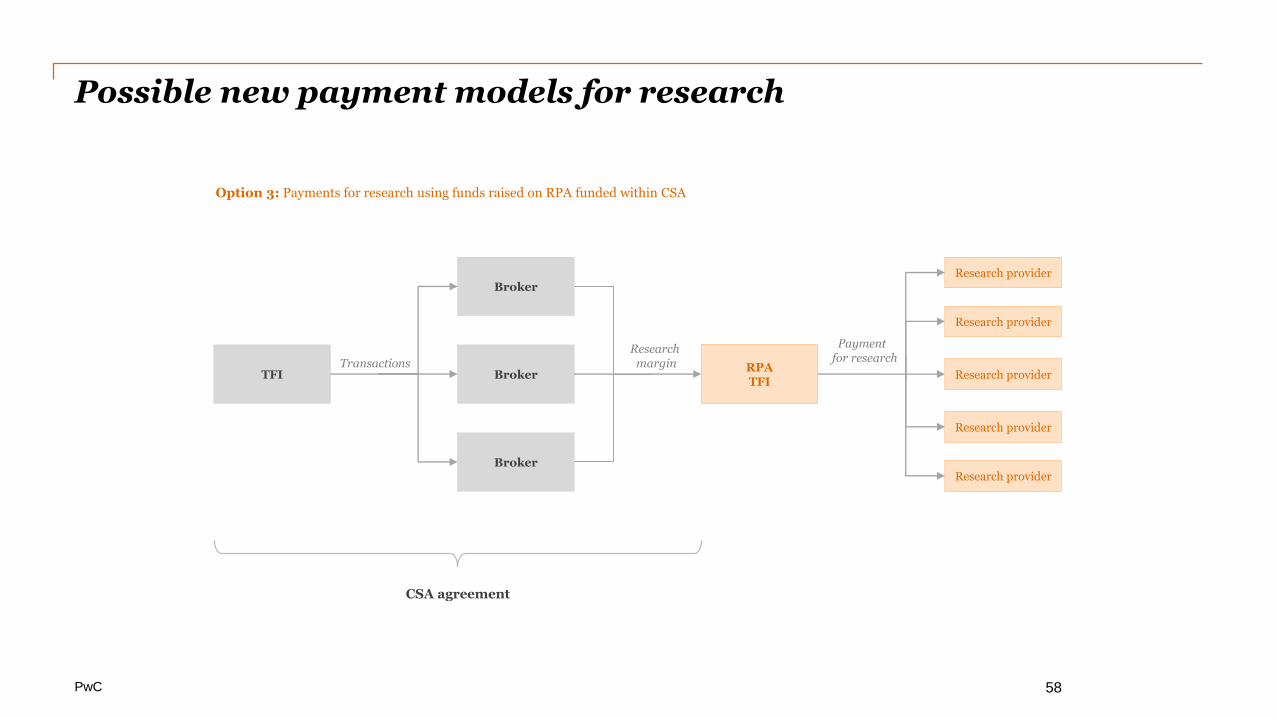

Possible new payment models for research

Option 3: Payments for research using funds raised on RPA funded within CSA

CSA agreement

TFI Broker

Research provider

Research provider

Research providerRPATFI

Transactions

Payment for research

Broker

Broker

Research provider

Research provider

Research margin

58

PwC

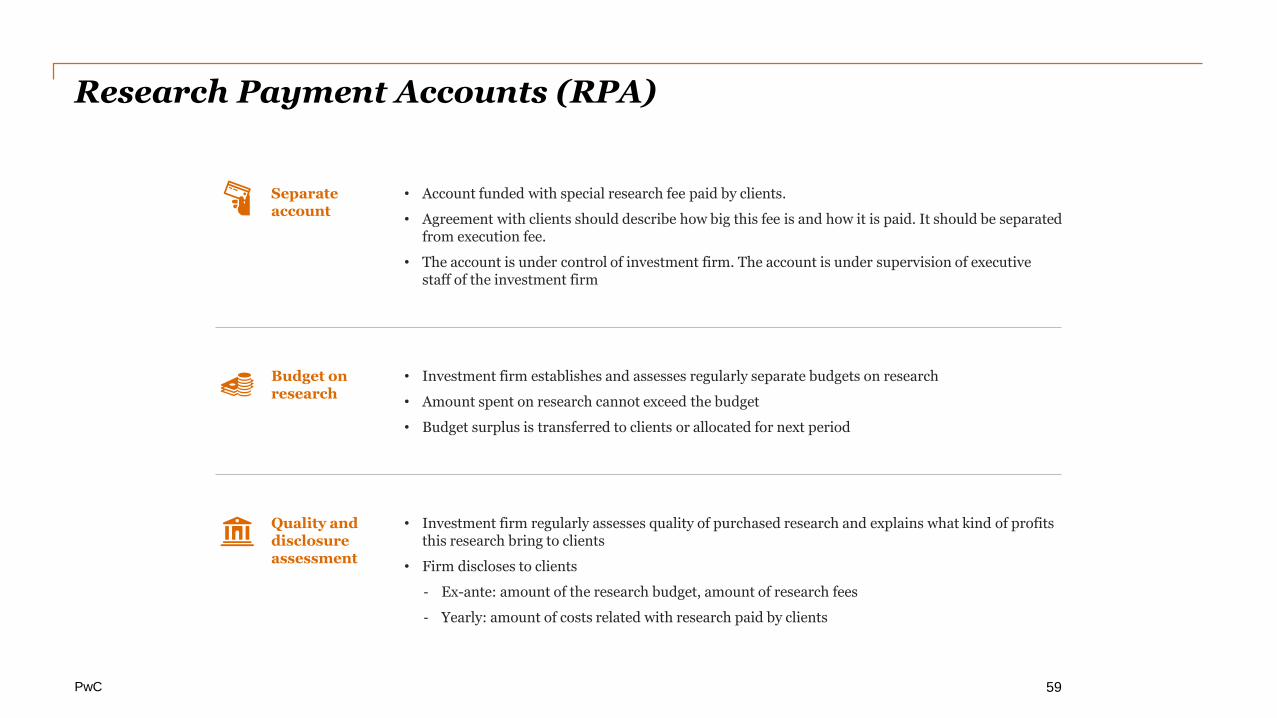

Research Payment Accounts (RPA)

• Account funded with special research fee paid by clients.

• Agreement with clients should describe how big this fee is and how it is paid. It should be separated from execution fee.

• The account is under control of investment firm. The account is under supervision of executive staff of the investment firm

Separate account

• Investment firm establishes and assesses regularly separate budgets on research

• Amount spent on research cannot exceed the budget

• Budget surplus is transferred to clients or allocated for next period

Budget on research

• Investment firm regularly assesses quality of purchased research and explains what kind of profits this research bring to clients

• Firm discloses to clients

- Ex-ante: amount of the research budget, amount of research fees

- Yearly: amount of costs related with research paid by clients

Quality and disclosure assessment

59

PwC

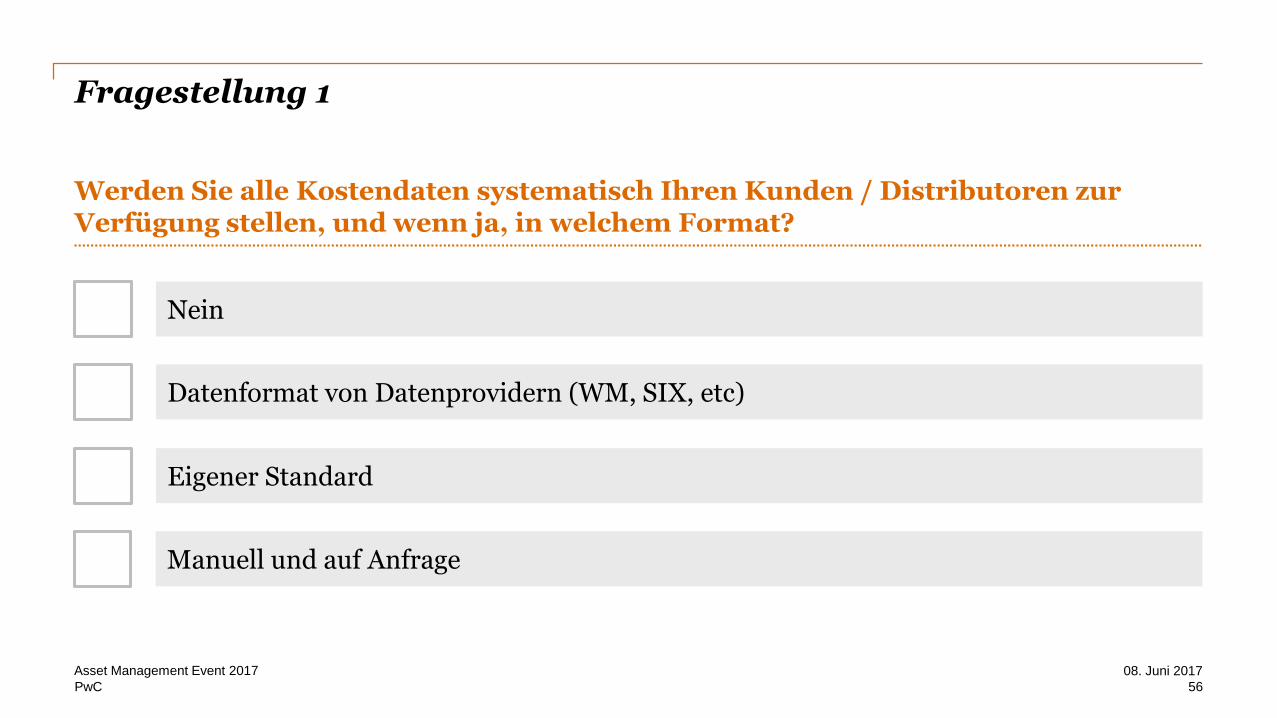

Fragestellung 1

56

08. Juni 2017Asset Management Event 2017

Werden Sie alle Kostendaten systematisch Ihren Kunden / Distributoren zur Verfügung stellen, und wenn ja, in welchem Format?

Nein

Datenformat von Datenprovidern (WM, SIX, etc)

Eigener Standard

Manuell und auf Anfrage

PwC

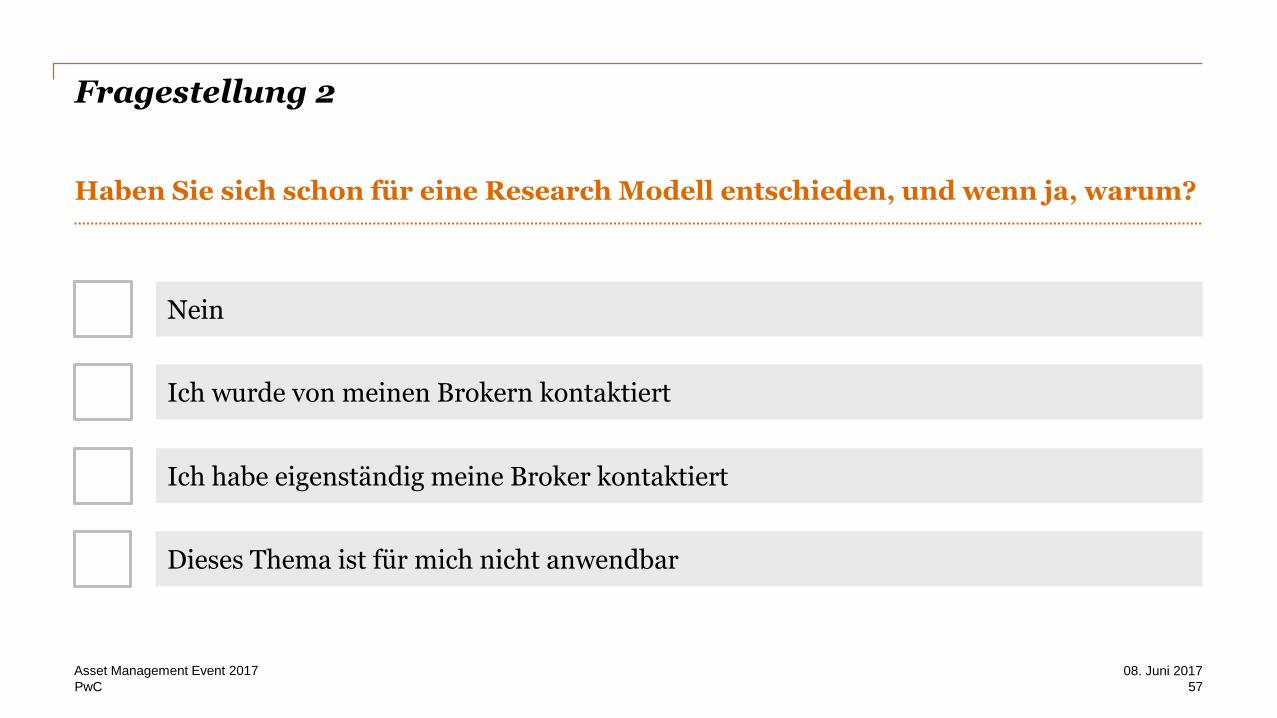

Fragestellung 2

57

08. Juni 2017Asset Management Event 2017

Haben Sie sich schon für eine Research Modell entschieden, und wenn ja, warum?

Nein

Ich wurde von meinen Brokern kontaktiert

Ich habe eigenständig meine Broker kontaktiert

Dieses Thema ist für mich nicht anwendbar

PwC

Fintech und Compliance – Neue Wege im WealthManagement16:35 – 17:00

Kaspar Wohnlich, CEO Evolute AG

58

08. Juni 2017Asset Management Event 2017

PwC

Pause17:00

59

08. Juni 2017Asset Management Event 2017

PwC

Fokus Bereiche der FINMA – aktuelle Bestandesaufnahme17:30 – 17:55

Yael Fries; Patrick Frigo, PwC

60

08. Juni 2017Asset Management Event 2017

PwC

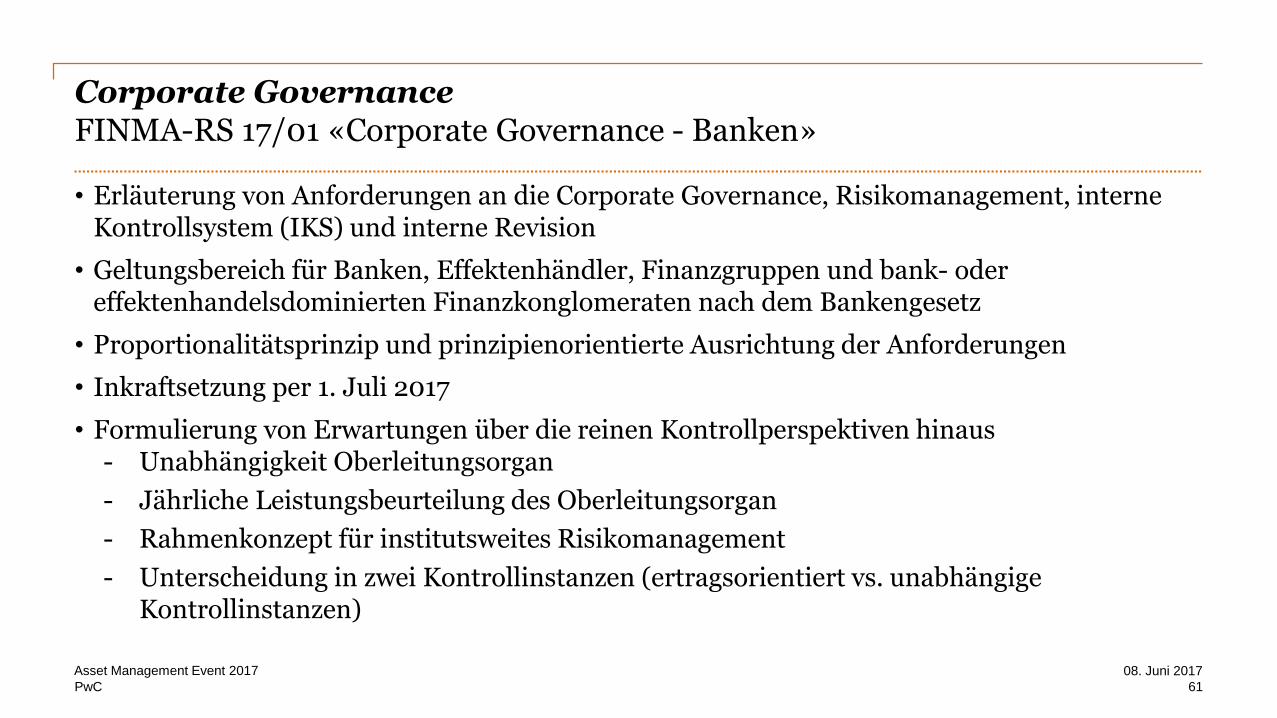

Corporate GovernanceFINMA-RS 17/01 «Corporate Governance - Banken»

• Erläuterung von Anforderungen an die Corporate Governance, Risikomanagement, interne Kontrollsystem (IKS) und interne Revision

• Geltungsbereich für Banken, Effektenhändler, Finanzgruppen und bank- odereffektenhandelsdominierten Finanzkonglomeraten nach dem Bankengesetz

• Proportionalitätsprinzip und prinzipienorientierte Ausrichtung der Anforderungen

• Inkraftsetzung per 1. Juli 2017

• Formulierung von Erwartungen über die reinen Kontrollperspektiven hinaus- Unabhängigkeit Oberleitungsorgan

- Jährliche Leistungsbeurteilung des Oberleitungsorgan

- Rahmenkonzept für institutsweites Risikomanagement

- Unterscheidung in zwei Kontrollinstanzen (ertragsorientiert vs. unabhängige Kontrollinstanzen)

61

08. Juni 2017Asset Management Event 2017

PwC

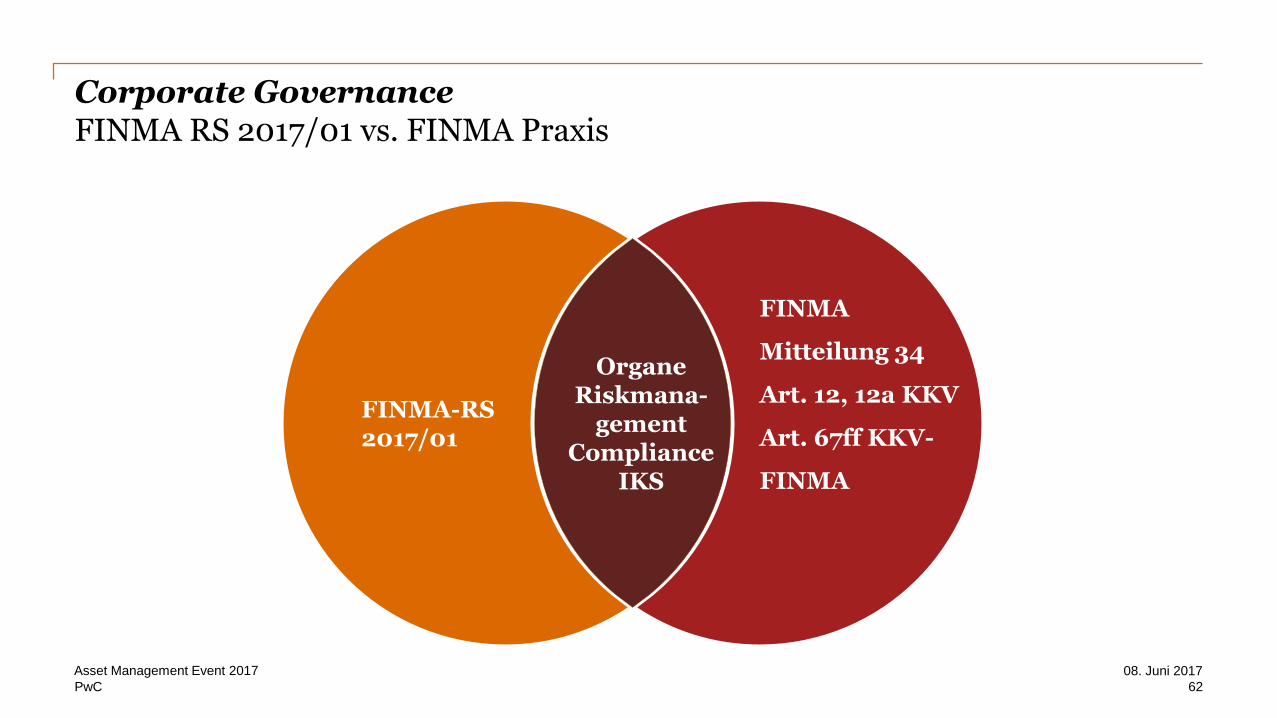

Corporate GovernanceFINMA RS 2017/01 vs. FINMA Praxis

62

08. Juni 2017Asset Management Event 2017

FINMA-RS 2017/01

FINMA

Mitteilung 34

Art. 12, 12a KKV

Art. 67ff KKV-

FINMA

OrganeRiskmana-

gementCompliance

IKS

PwC

Corporate GovernanceUnabhängigkeit des Oberleitungsorgans

KAG Institute

Mind. 1/3 der Mitglieder des Verwaltungsrats müssen unabhängig und mehrheitlich nicht operativ tätig sein

63

08. Juni 2017Asset Management Event 2017

FINMA-RS 17/01

Mind. 1/3 der Mitglieder des Oberleitungsorgans müssen unabhängig sein

PwC

Fragestellung 1Corporate Governance

64

08. Juni 2017Asset Management Event 2017

Hat die Wahl eines nicht operativ tätigen Verwaltungsrates Ihrer Gesellschaft einen Mehrwert gebracht?

Ja

Nein

PwC

Fragestellung 2Corporate Governance

65

08. Juni 2017Asset Management Event 2017

Welche Kompetenz hat sich Ihre Gesellschaft durch Einbezug eines nicht operativ tätigen Verwaltungsrates verschafft?

Risikomanagement

Compliance & Legal

Netzwerk/Beziehungen

PwC

Corporate GovernanceLeistungsbeurteilung des Oberleitungsorgans

66

08. Juni 2017Asset Management Event 2017

KAG Institute

Keine vergleichbare Regelung für KAG Institute

FINMA-RS 17/01

Jährliche Leistungsbeurteilung des Oberleitungsorgan

PwC

Corporate GovernanceRisikomanagement

67

08. Juni 2017Asset Management Event 2017

KAG Institute

Grundsätze des Risikomanagements: Feststellung, Bewertung, Steuerung und Überwachung aller wesentlichen Risiken.

FINMA-RS 17/01

Rahmenkonzept für institutsweites Risikomanagement: Allgemeine Grundsätze zur Risikopolitik, Risikotoleranz und Risikolimiten in allen wesentlichen Risiko-kategorien

PwC

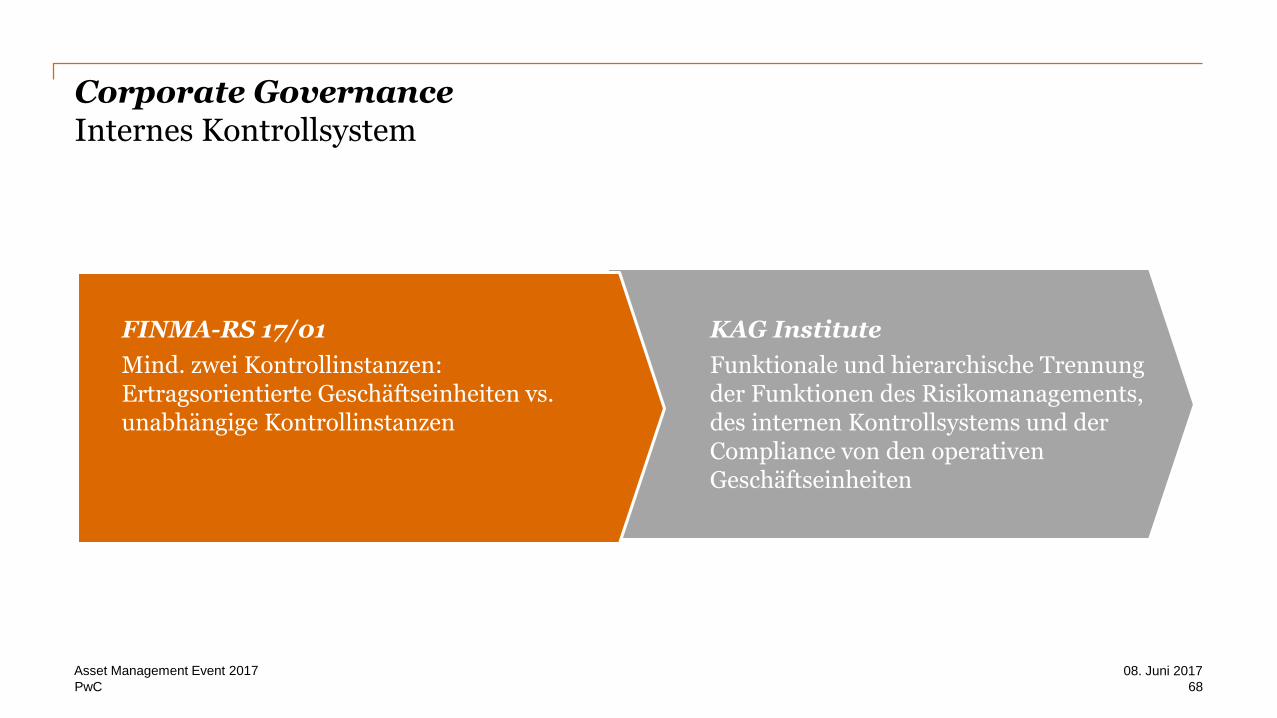

Corporate GovernanceInternes Kontrollsystem

68

08. Juni 2017Asset Management Event 2017

KAG Institute

Funktionale und hierarchische Trennung der Funktionen des Risikomanagements, des internen Kontrollsystems und der Compliance von den operativen Geschäftseinheiten

FINMA-RS 17/01

Mind. zwei Kontrollinstanzen:Ertragsorientierte Geschäftseinheiten vs. unabhängige Kontrollinstanzen

PwC

Grenzüberschreitende TätigkeitenFINMA-RS 08/21 «Operationelle Risiken - Banken»

• Regelt neben Eigenmittelanforderungen qualitative Anforderungen für operationelle Risiken

• Geltungsbereich für Banken, Finanzgruppen und -konglomerate sowie Effektenhändler

• Definiert Operationelle Risiken und stellt qualitative Grundanforderungen auf

• Inkraftsetzung per 1. Juli 2017

• Grundsatz 7 regelt die Risiken aus grenzüberschreitenden Dienstleistungsgeschäft

- Nimmt die Prinzipien des Positionspapiers vom 22. Oktober 2010 auf

- Erfassung, Begrenzung und Kontrolle der ausländischen Rechtsrisiken

- Umfasst insb. Steuer-, Straf- und Geldwäschereirecht

- Länderspezifisches Fachwissen, Definition von länderspezifischem Fachwissen, Schulung Mitarbeiter, Vergütungs- und Sanktionsmodelle zur Einhaltung

- Umfasst andere Dienstleister, Partner und ausländische Gesellschaften

69

08. Juni 2017Asset Management Event 2017

PwC

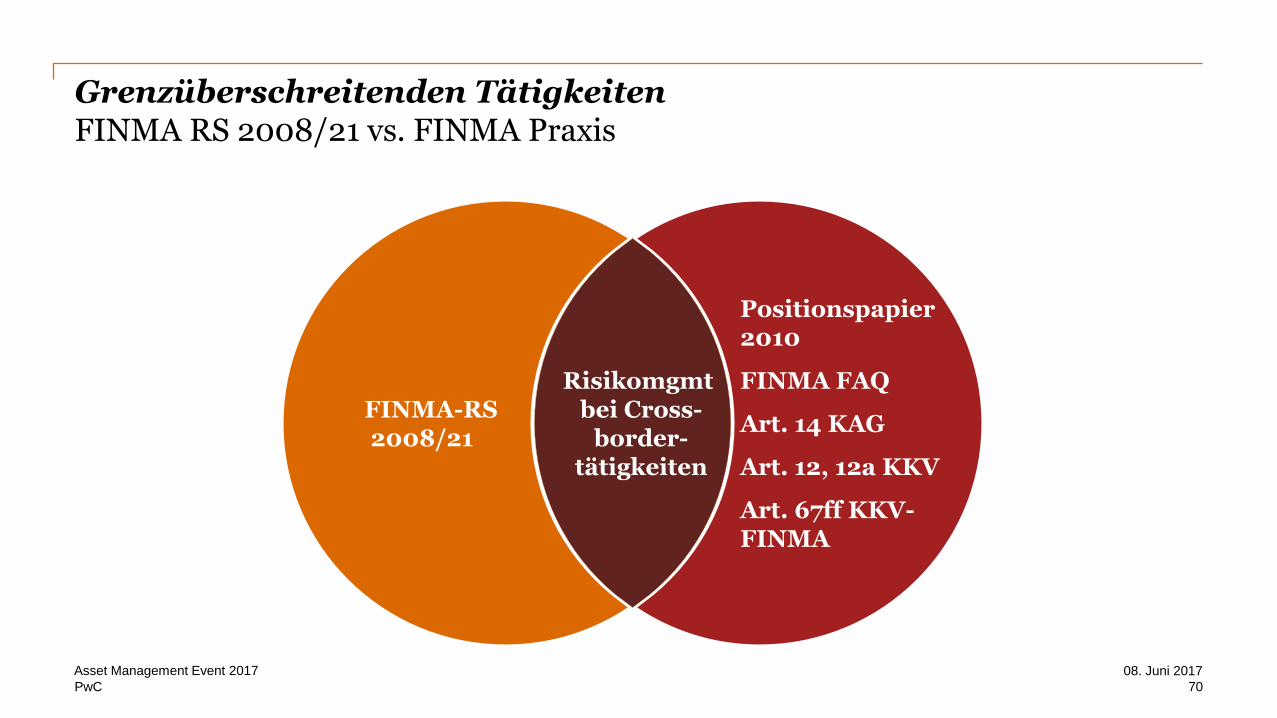

Grenzüberschreitenden TätigkeitenFINMA RS 2008/21 vs. FINMA Praxis

70

08. Juni 2017Asset Management Event 2017

FINMA-RS2008/21

Positionspapier 2010

FINMA FAQ

Art. 14 KAG

Art. 12, 12a KKV

Art. 67ff KKV-FINMA

Risikomgmtbei Cross-

border-tätigkeiten

PwC

Fragestellung 1Grenzüberschreitende Tätigkeiten

71

08. Juni 2017Asset Management Event 2017

Was haben sie betreffend grenzüberschreitende Dienstleistungen bei Ihrer Gesellschaft für Massnahmen getroffen?

Keine Massnahmen oder keine grenzüberschreitende Tätigkeit

Limitierung der Länder/Kunden, welche bereist/betreut werden dürfen

Genehmigung der Risikobereitschaft und –toleranz im Verwaltungsrat

Umfassendes cross border framework erstellt und Schulungen durchgeführt

PwC

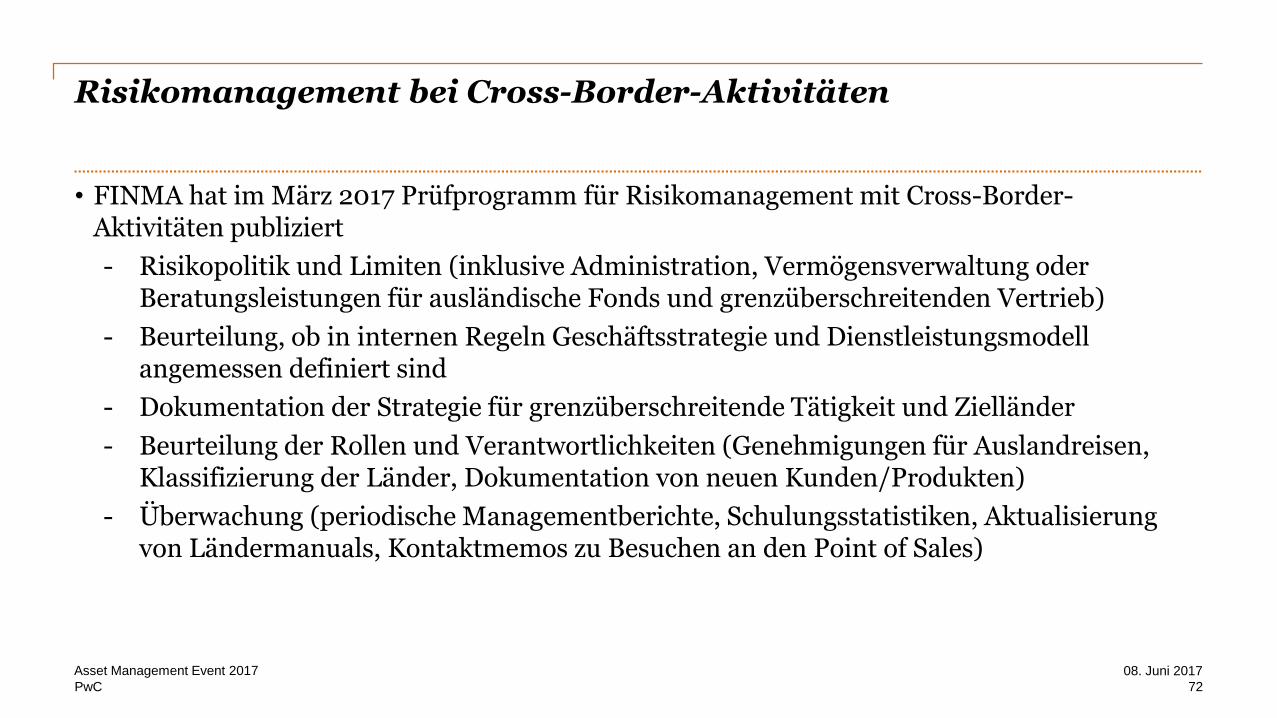

Risikomanagement bei Cross-Border-Aktivitäten

• FINMA hat im März 2017 Prüfprogramm für Risikomanagement mit Cross-Border-Aktivitäten publiziert

- Risikopolitik und Limiten (inklusive Administration, Vermögensverwaltung oder Beratungsleistungen für ausländische Fonds und grenzüberschreitenden Vertrieb)

- Beurteilung, ob in internen Regeln Geschäftsstrategie und Dienstleistungsmodell angemessen definiert sind

- Dokumentation der Strategie für grenzüberschreitende Tätigkeit und Zielländer

- Beurteilung der Rollen und Verantwortlichkeiten (Genehmigungen für Auslandreisen, Klassifizierung der Länder, Dokumentation von neuen Kunden/Produkten)

- Überwachung (periodische Managementberichte, Schulungsstatistiken, Aktualisierung von Ländermanuals, Kontaktmemos zu Besuchen an den Point of Sales)

72

08. Juni 2017Asset Management Event 2017

PwC

Fragestellung 2Grenzüberschreitende Tätigkeiten

73

08. Juni 2017Asset Management Event 2017

Wie stufen Sie die Crossborder-Risiken bei Ihrer Gesellschaft ein?

Hohe Risiken

Mittelhohe Risiken

Überschaubare Risiken

Minimale Risiken

PwC

Neues aus dem Steuerbereich17:55-18:10

Marcella Dzienisik, PwC

74

08. Juni 2017Asset Management Event 2017

PwC

Fragestellung

75

08. Juni 2017Asset Management Event 2017

Beim Thema Steuern denke ich zuerst:

Oh weh!

Ich habe sämtliche Steuerthemen im Griff

Ich delegiere meine Steuerthemen an PwC

PwC

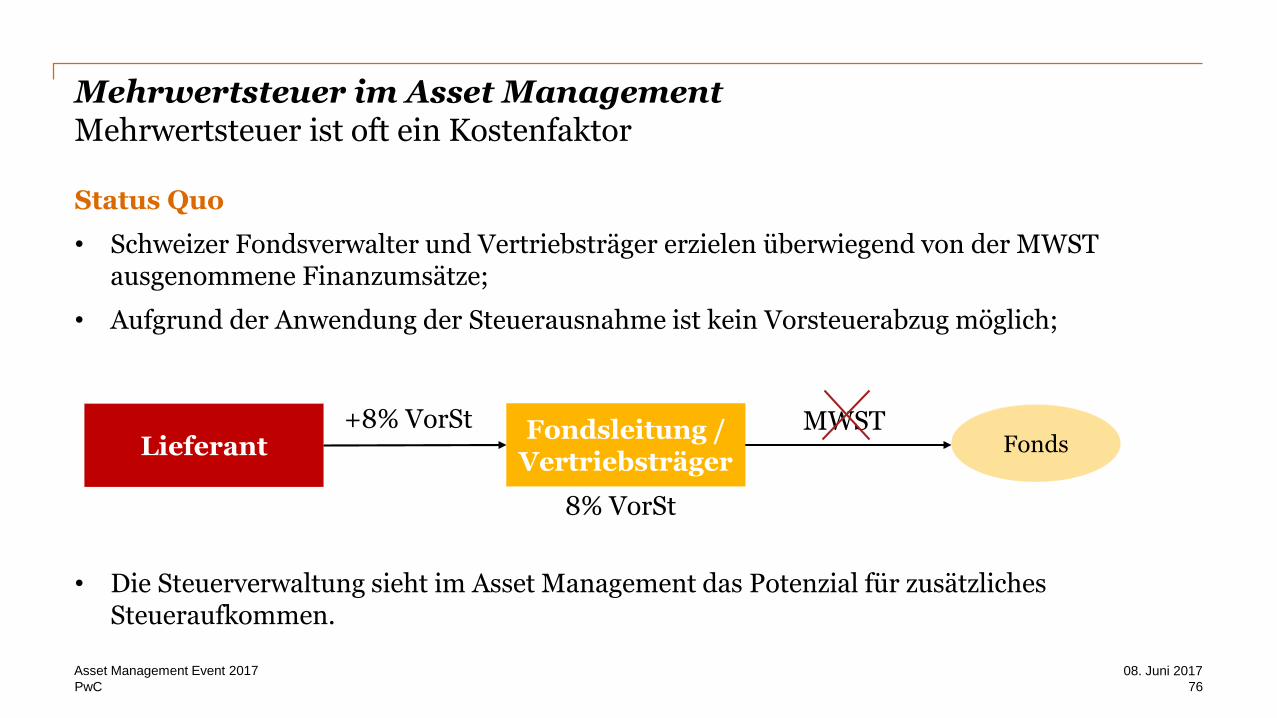

Mehrwertsteuer im Asset Management Mehrwertsteuer ist oft ein Kostenfaktor

Status Quo

• Schweizer Fondsverwalter und Vertriebsträger erzielen überwiegend von der MWST ausgenommene Finanzumsätze;

• Aufgrund der Anwendung der Steuerausnahme ist kein Vorsteuerabzug möglich;

• Die Steuerverwaltung sieht im Asset Management das Potenzial für zusätzliches Steueraufkommen.

Fondsleitung / Vertriebsträger

FondsLieferantMWST+8% VorSt

8% VorSt

08. Juni 2017Asset Management Event 2017

76

PwC

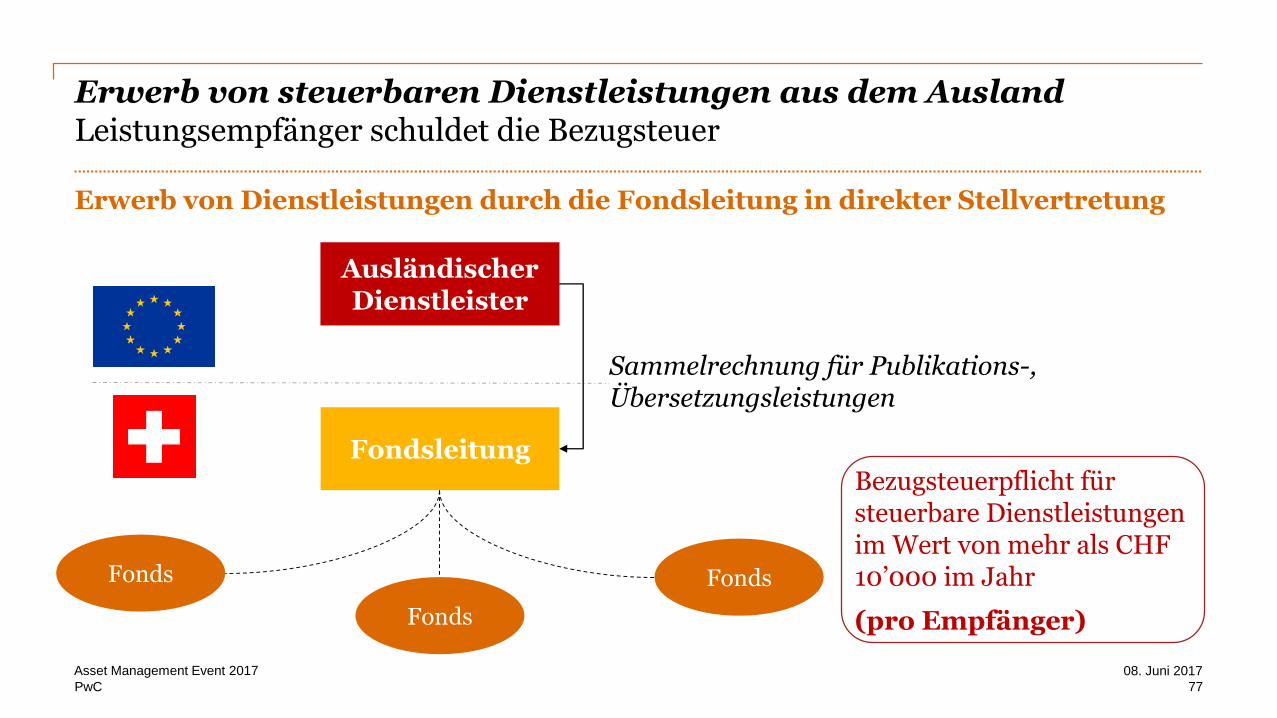

Erwerb von steuerbaren Dienstleistungen aus dem AuslandLeistungsempfänger schuldet die Bezugsteuer

Erwerb von Dienstleistungen durch die Fondsleitung in direkter Stellvertretung

Bezugsteuerpflicht für steuerbare Dienstleistungen im Wert von mehr als CHF 10’000 im Jahr

(pro Empfänger)

Ausländischer Dienstleister

Fondsleitung

Fonds

Fonds

Fonds

Sammelrechnung für Publikations-, Übersetzungsleistungen

77

08. Juni 2017Asset Management Event 2017

PwC

Neutralisierung der Bezugsteuer durch Weiterverrechnung der Kosten

(Freiwillige) MWST-Registrierung ist die Voraussetzung für den Vorsteuerabzug

Ausländischer Plattform-betreiber

Vertriebsträger

Plattformgebühren

Ausländischer Fondsanbieter / Vertriebsträger

Weiterverrechnung von Plattformgebühren

78

08. Juni 2017Asset Management Event 2017

+ 8% Bezugsteuer

- 8% Vorsteuer

PwC

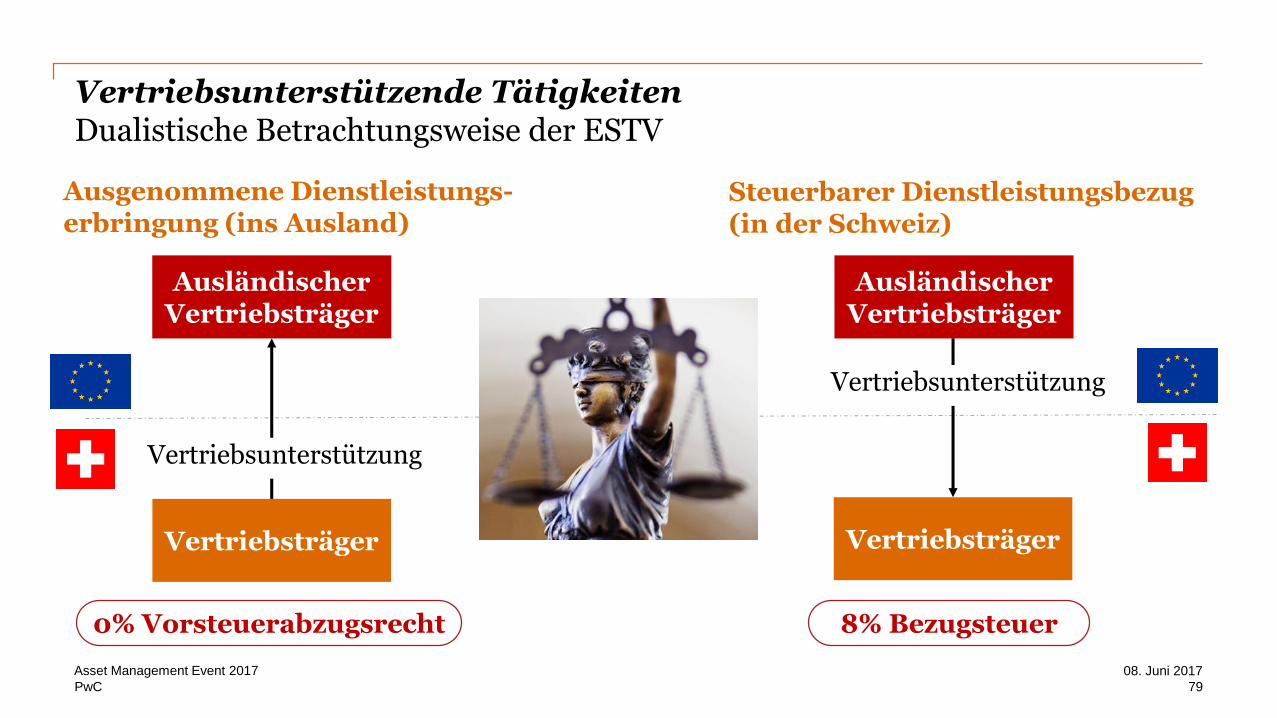

Vertriebsunterstützende TätigkeitenDualistische Betrachtungsweise der ESTV

Ausgenommene Dienstleistungs-erbringung (ins Ausland)

AusländischerVertriebsträger

Vertriebsträger

Steuerbarer Dienstleistungsbezug (in der Schweiz)

AusländischerVertriebsträger

Vertriebsträger

Vertriebsunterstützung

Vertriebsunterstützung

0% Vorsteuerabzugsrecht 8% Bezugsteuer

79

08. Juni 2017Asset Management Event 2017

PwC

Brexit impacts for the Asset Management industryAsset Management 2025 – an outlook18:10 – 18:30

Robert Mellor, PwC UK

80

08. Juni 2017Asset Management Event 2017

PwC

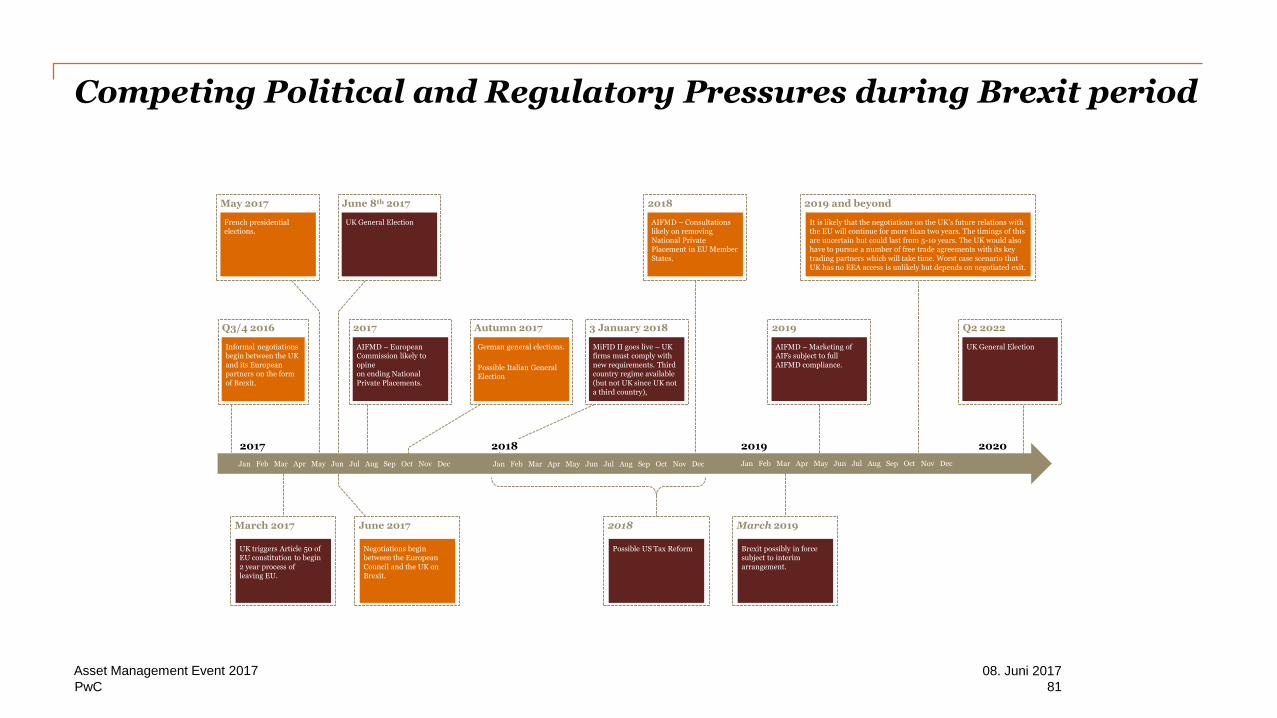

Competing Political and Regulatory Pressures during Brexit period

Q3/4 2016

Informal negotiations begin between the UK and its European partners on the form

of Brexit.

June 8th 2017

UK General Election

June 2017

Negotiations begin between the European Council and the UK on Brexit.

2019 and beyond

It is likely that the negotiations on the UK’s future relations with the EU will continue for more than two years. The timings of this are uncertain but could last from 5-10 years. The UK would also have to pursue a number of free trade agreements with its key trading partners which will take time. Worst case scenario that UK has no EEA access is unlikely but depends on negotiated exit.

2017 2019 2020

March 2017

UK triggers Article 50 of EU constitution to begin 2 year process of leaving EU.

2018

AIFMD – Consultations likely on removing National Private Placement in EU Member States.

May 2017

French presidential elections.

2017

AIFMD – European Commission likely to opine on ending National

Private Placements.

Autumn 2017

German general elections.

Possible Italian General Election

3 January 2018

MiFID II goes live – UK firms must comply with new requirements. Third country regime available

(but not UK since UK not a third country),

March 2019

Brexit possibly in force subject to interim arrangement.

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2018

Possible US Tax Reform

08. Juni 2017Asset Management Event 2017

81

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019

AIFMD – Marketing of AIFs subject to full AIFMD compliance.

Q2 2022

UK General Election

2018

PwC

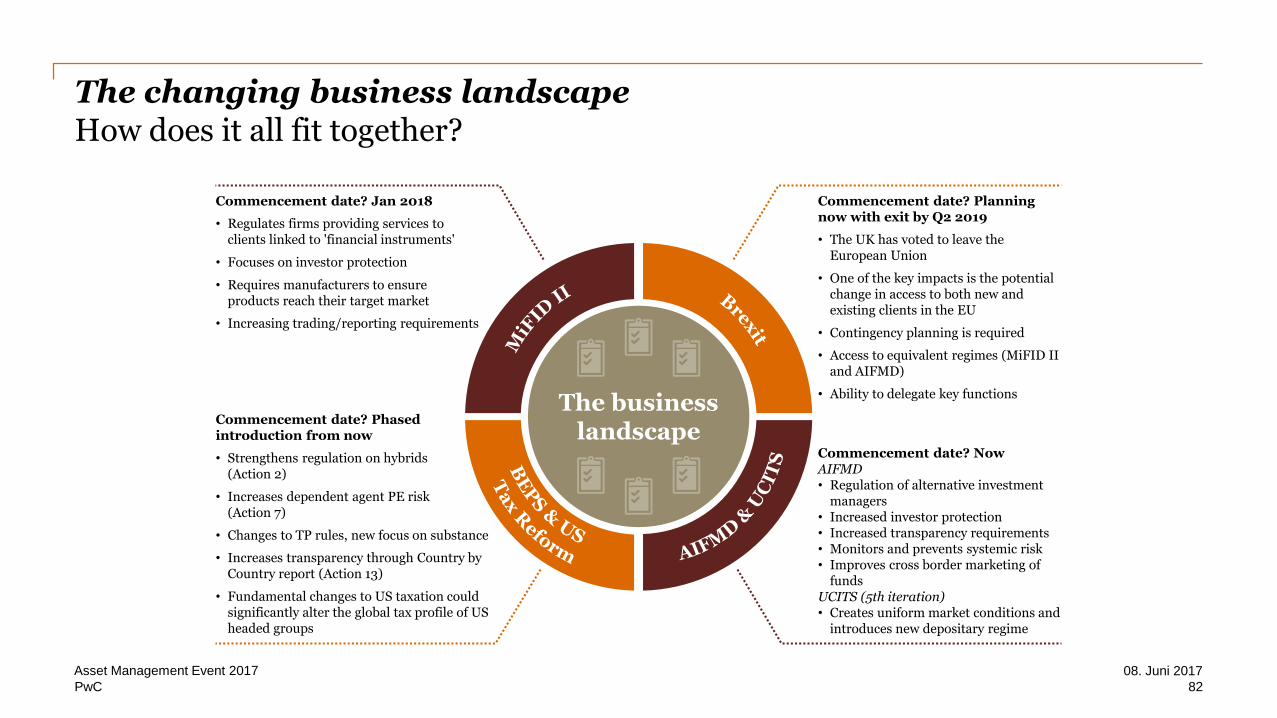

The changing business landscapeHow does it all fit together?

08. Juni 2017Asset Management Event 2017

82

Commencement date? Planning now with exit by Q2 2019

• The UK has voted to leave the European Union

• One of the key impacts is the potential change in access to both new and existing clients in the EU

• Contingency planning is required

• Access to equivalent regimes (MiFID II and AIFMD)

• Ability to delegate key functions

Commencement date? Jan 2018

• Regulates firms providing services to clients linked to 'financial instruments'

• Focuses on investor protection

• Requires manufacturers to ensure products reach their target market

• Increasing trading/reporting requirements

Commencement date? Phased introduction from now

• Strengthens regulation on hybrids (Action 2)

• Increases dependent agent PE risk (Action 7)

• Changes to TP rules, new focus on substance

• Increases transparency through Country by Country report (Action 13)

• Fundamental changes to US taxation could significantly alter the global tax profile of US headed groups

Commencement date? Now AIFMD• Regulation of alternative investment

managers• Increased investor protection• Increased transparency requirements• Monitors and prevents systemic risk• Improves cross border marketing of

fundsUCITS (5th iteration)• Creates uniform market conditions and

introduces new depositary regime

The business landscape

PwC

Four Possible post Brexit scenarios

EEA memberNo access

agreementScenario

Norway

Bespokebilateral deal

Switzerland USCase study

Free tradeagreement (FTA)

Canada

Disruption to economy

Low Medium Medium High

Access to single market

High – Via passport/regulatory equivalence.

Medium – UK would retain free trade in goods with the EU, but non-tariff barriers such as divergence in standards and regulations could emerge.

Medium – If EU allows UK corporations to operate like Swiss banks in a legal grey area.

Low

Influence over EU regulations

Some – No voting rights but limited formal engagement. Some autonomy in other areas.

No No No

Application of EU regulations

Yes, including social and labour law (Working Time Directive). Some contributions to the EU.

Medium The UK would have to comply with EU regulations around the goods covered by the FTA.

Technically no, but required in practice if domiciling in other territories (e.g. Swiss banks operating out of UK). Some contributions to the EU.

Technically no, but limited discretion in reality if third country equivalence is required.

Independentimmigration policy

No – All four freedoms retained. Yes Some autonomy, but Switzerland cannot restrict EU immigration

Yes

Independent trade policy

Yes – UK may negotiate free trade agreements (FTA) with other countries.

Yes – UK may negotiate FTAs with other countries.

Yes – UK may negotiate FTAs with other countries.

Yes – UK may negotiate FTAs with other countries in FS and other services.

08. Juni 2017Asset Management Event 2017

83

Note: Scenario C could take the form of other non-EEA European states that have negotiated limited access to the EU single market.

The UK remains part of the EEA and keeps the four freedoms of labour, capital, goods and services

UK will need to make a substantial contribution to the EU budget and comply with EU social, employment and product regulation.

The UK does not establish any new trade agreementswith the EU

Only WTO terms are still applied –UK goods and services would be treated in the same way as American ones in the EU.

Analysis

The UK enters into a bilateral integration treaty with the EU

UK would have access to some areas of the Single Market, at the cost of adopting the relevant EU regulations

UK negotiates a Free Trade Agreement (FTA) with the EU.

Tariff-free trade between the UK and the EU in goods (but not services). UK grandfathers all existing FTAs between the EU and third-party countries. Likely to require free movement of people, fiscal contribution.

B C DA

PwC

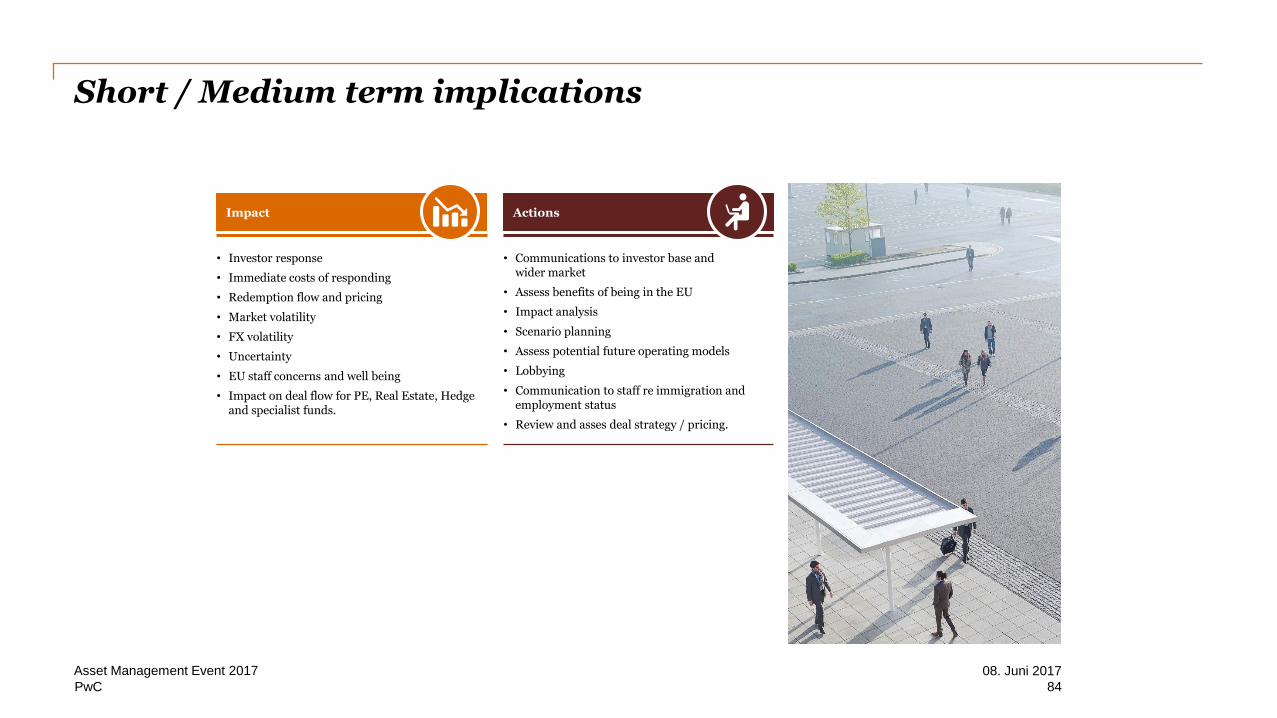

08. Juni 2017Asset Management Event 2017

84

Impact

• Investor response

• Immediate costs of responding

• Redemption flow and pricing

• Market volatility

• FX volatility

• Uncertainty

• EU staff concerns and well being

• Impact on deal flow for PE, Real Estate, Hedge and specialist funds.

Actions

• Communications to investor base and wider market

• Assess benefits of being in the EU

• Impact analysis

• Scenario planning

• Assess potential future operating models

• Lobbying

• Communication to staff re immigration and employment status

• Review and asses deal strategy / pricing.

Short / Medium term implications

PwC

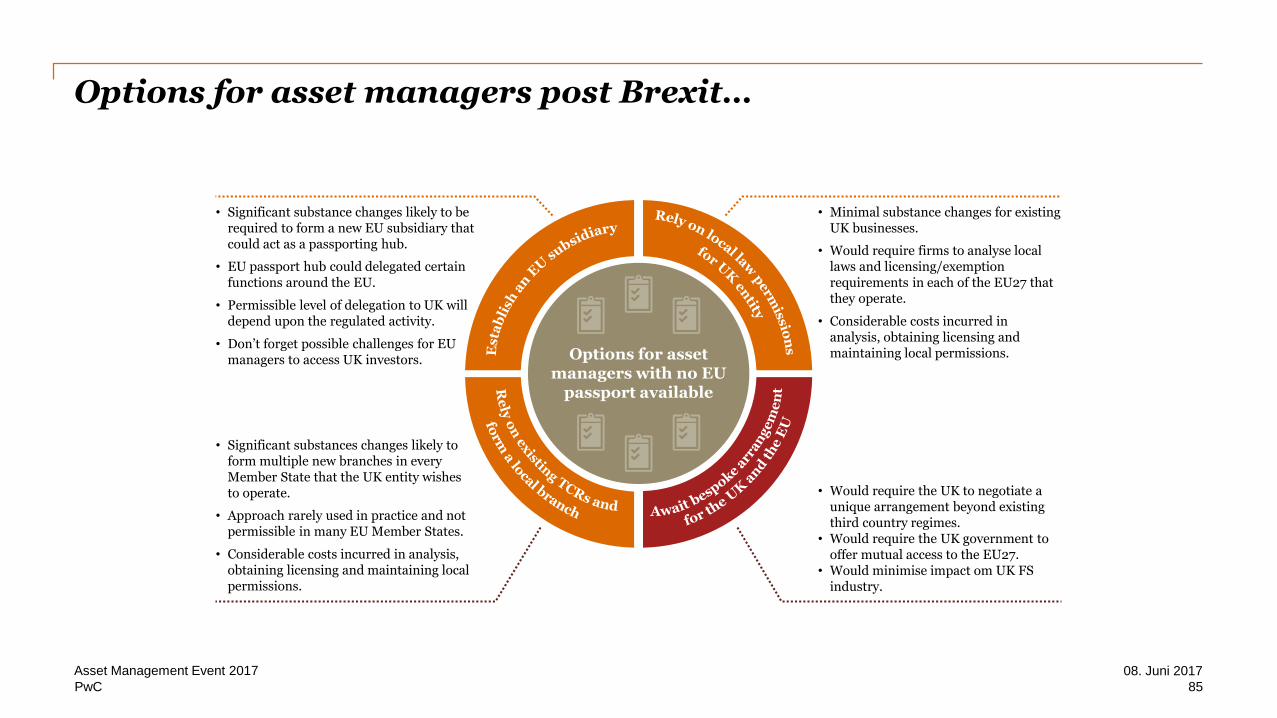

Options for asset managers post Brexit…

08. Juni 2017Asset Management Event 2017

85

• Minimal substance changes for existing UK businesses.

• Would require firms to analyse local laws and licensing/exemption requirements in each of the EU27 that they operate.

• Considerable costs incurred in analysis, obtaining licensing and maintaining local permissions.

• Significant substance changes likely to be required to form a new EU subsidiary that could act as a passporting hub.

• EU passport hub could delegated certain functions around the EU.

• Permissible level of delegation to UK will depend upon the regulated activity.

• Don’t forget possible challenges for EU managers to access UK investors.

• Significant substances changes likely to form multiple new branches in every Member State that the UK entity wishes to operate.

• Approach rarely used in practice and not permissible in many EU Member States.

• Considerable costs incurred in analysis, obtaining licensing and maintaining local permissions.

• Would require the UK to negotiate a unique arrangement beyond existing third country regimes.

• Would require the UK government to offer mutual access to the EU27.

• Would minimise impact om UK FS industry.

Options for asset managers with no EU

passport available

PwC

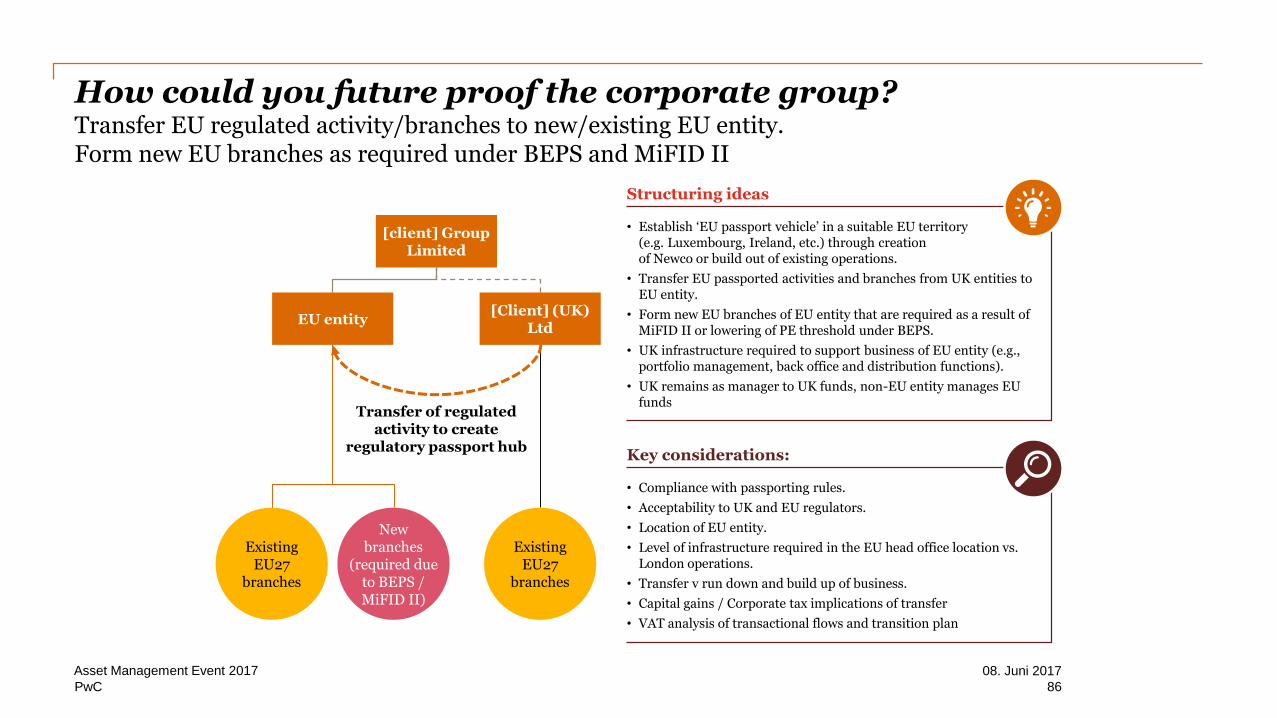

How could you future proof the corporate group?Transfer EU regulated activity/branches to new/existing EU entity. Form new EU branches as required under BEPS and MiFID II

Structuring ideas

• Establish ‘EU passport vehicle’ in a suitable EU territory (e.g. Luxembourg, Ireland, etc.) through creation of Newco or build out of existing operations.

• Transfer EU passported activities and branches from UK entities to EU entity.

• Form new EU branches of EU entity that are required as a result of MiFID II or lowering of PE threshold under BEPS.

• UK infrastructure required to support business of EU entity (e.g., portfolio management, back office and distribution functions).

• UK remains as manager to UK funds, non-EU entity manages EU funds

Key considerations:

• Compliance with passporting rules.

• Acceptability to UK and EU regulators.

• Location of EU entity.

• Level of infrastructure required in the EU head office location vs. London operations.

• Transfer v run down and build up of business.

• Capital gains / Corporate tax implications of transfer

• VAT analysis of transactional flows and transition plan

[Client] (UK) Ltd

[client] Group Limited

EU entity

ExistingEU27

branches

Newbranches

(required dueto BEPS /MiFID II)

ExistingEU27

branches

Transfer of regulated activity to create

regulatory passport hub

08. Juni 2017Asset Management Event 2017

86

PwC

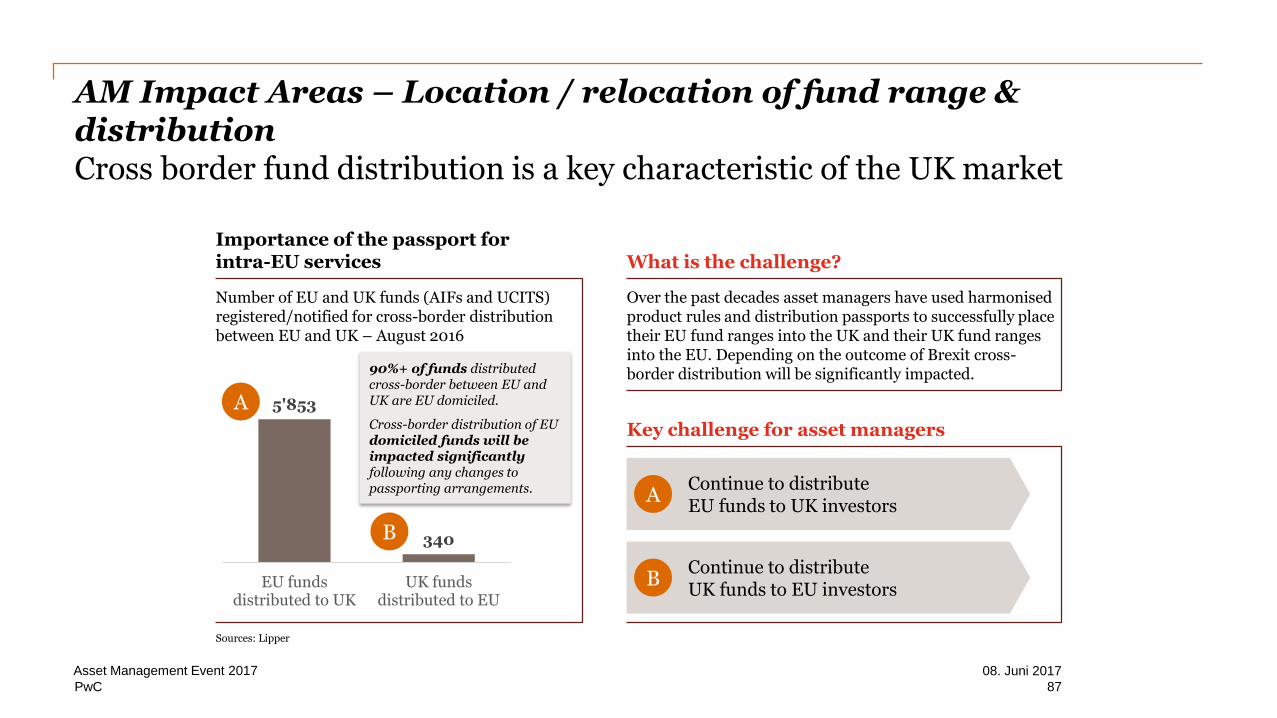

AM Impact Areas – Location / relocation of fund range & distributionCross border fund distribution is a key characteristic of the UK market

Importance of the passport for intra-EU services

Sources: Lipper

08. Juni 2017Asset Management Event 2017

87

What is the challenge?

Over the past decades asset managers have used harmonisedproduct rules and distribution passports to successfully place their EU fund ranges into the UK and their UK fund ranges into the EU. Depending on the outcome of Brexit cross-border distribution will be significantly impacted.

Key challenge for asset managers

Continue to distribute EU funds to UK investors

A

Continue to distributeUK funds to EU investors

B

Number of EU and UK funds (AIFs and UCITS) registered/notified for cross-border distribution between EU and UK – August 2016

5'853

340

EU fundsdistributed to UK

UK fundsdistributed to EU

A

B

90%+ of funds distributed cross-border between EU and UK are EU domiciled.

Cross-border distribution of EU domiciled funds will be impacted significantly following any changes to passporting arrangements.

PwC

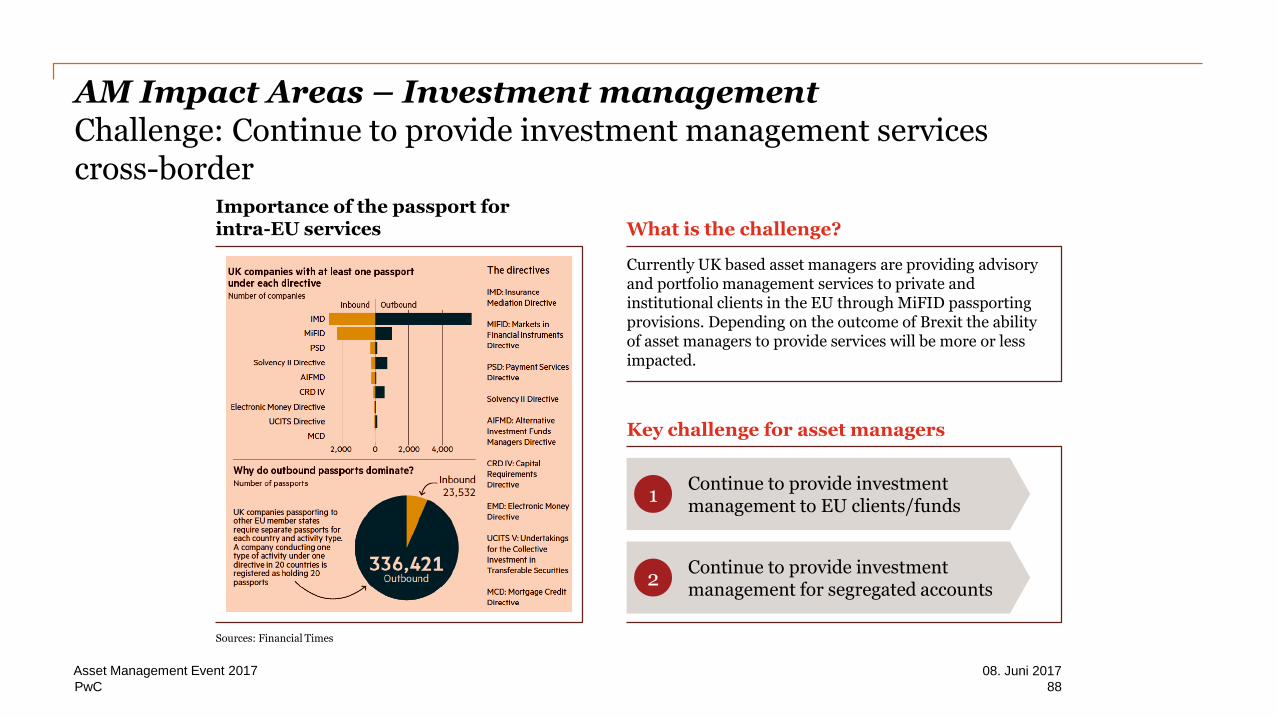

AM Impact Areas – Investment managementChallenge: Continue to provide investment management services cross-border

Importance of the passport for intra-EU services

Sources: Financial Times

08. Juni 2017Asset Management Event 2017

88

What is the challenge?

Currently UK based asset managers are providing advisory and portfolio management services to private and institutional clients in the EU through MiFID passporting provisions. Depending on the outcome of Brexit the ability of asset managers to provide services will be more or less impacted.

Key challenge for asset managers

Continue to provide investment management to EU clients/funds

1

Continue to provide investment management for segregated accounts

2

PwC

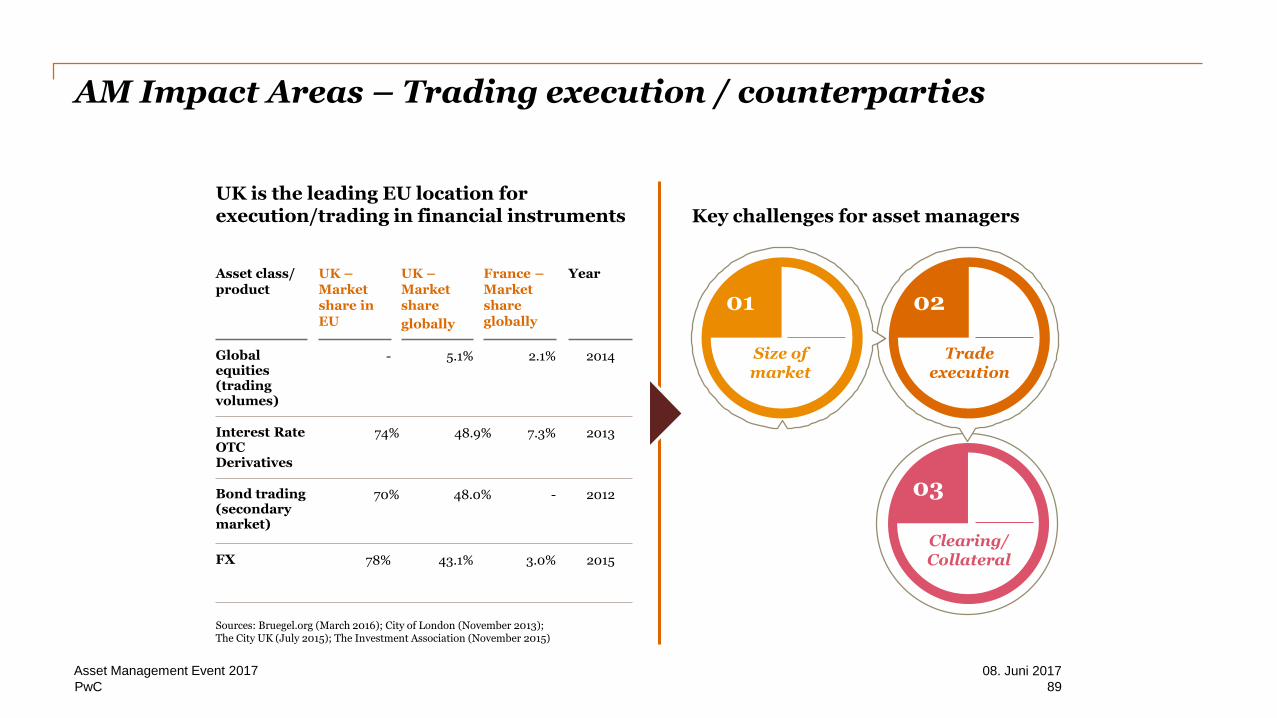

AM Impact Areas – Trading execution / counterparties

Sources: Bruegel.org (March 2016); City of London (November 2013); The City UK (July 2015); The Investment Association (November 2015)

01 02

03

Size ofmarket

Trade execution

Clearing/Collateral

Key challenges for asset managers

08. Juni 2017Asset Management Event 2017

89

UK is the leading EU location for execution/trading in financial instruments

Global equities (trading volumes)

Asset class/ product

Interest Rate OTC Derivatives

74% 48.9% 7.3%

Bond trading (secondary market)

70% 48.0% -

FX

-

UK –Market share in EU

5.1%

UK –Market share

globally

2.1%

France –Market share globally

78% 43.1% 3.0%

2014

Year

2013

2012

2015

PwC

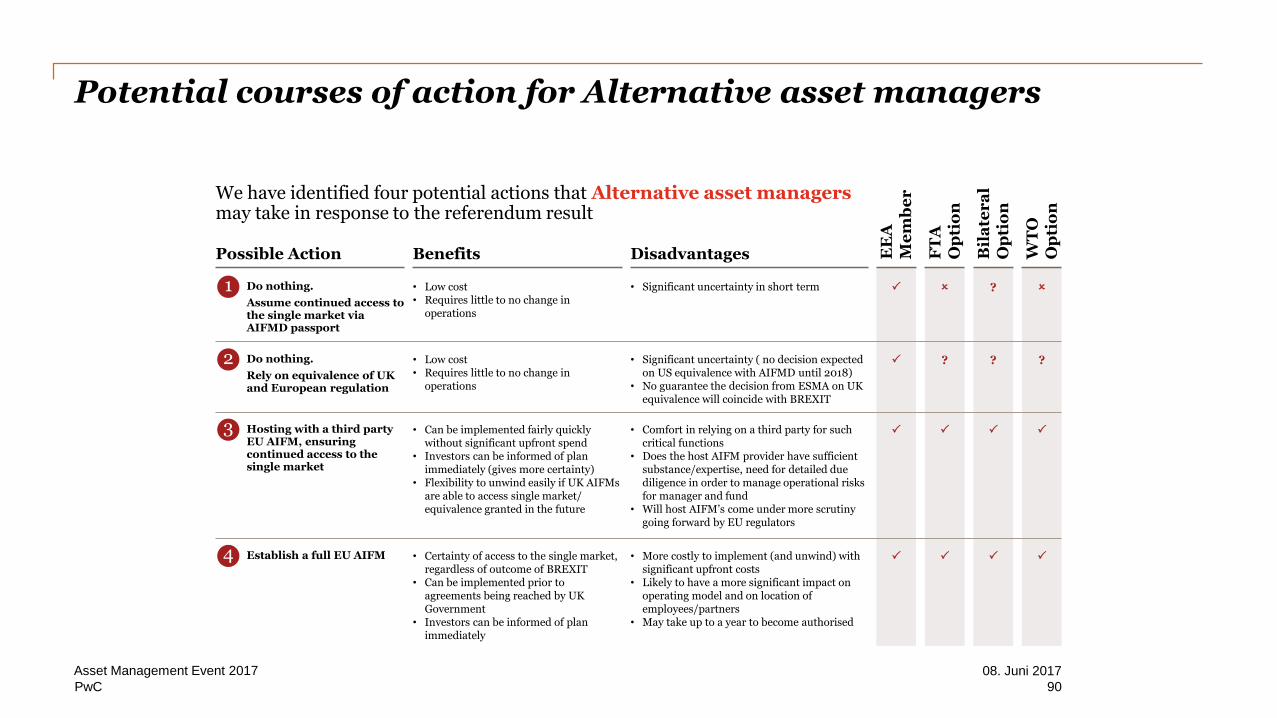

Do nothing.

Assume continued access to the single market via AIFMD passport

Possible Action

Potential courses of action for Alternative asset managers

1

EE

A

Me

mb

er

FT

A

Op

tio

n

Bil

ate

ra

l O

pti

on

?

WT

O

Op

tio

n

• Low cost• Requires little to no change in

operations

Benefits

• Significant uncertainty in short term

Disadvantages

Do nothing.

Rely on equivalence of UK and European regulation

2 ? ? ?• Low cost• Requires little to no change in

operations

• Significant uncertainty ( no decision expected on US equivalence with AIFMD until 2018)

• No guarantee the decision from ESMA on UK equivalence will coincide with BREXIT

Hosting with a third party EU AIFM, ensuring continued access to the single market

3 • Can be implemented fairly quickly without significant upfront spend

• Investors can be informed of plan immediately (gives more certainty)

• Flexibility to unwind easily if UK AIFMs are able to access single market/ equivalence granted in the future

• Comfort in relying on a third party for such critical functions

• Does the host AIFM provider have sufficient substance/expertise, need for detailed due diligence in order to manage operational risks for manager and fund

• Will host AIFM’s come under more scrutiny going forward by EU regulators

• Certainty of access to the single market, regardless of outcome of BREXIT

• Can be implemented prior to agreements being reached by UK Government

• Investors can be informed of plan immediately

• More costly to implement (and unwind) with significant upfront costs

• Likely to have a more significant impact on operating model and on location of employees/partners

• May take up to a year to become authorised

Establish a full EU AIFM4

08. Juni 2017Asset Management Event 2017

90

We have identified four potential actions that Alternative asset managers may take in response to the referendum result

PwC

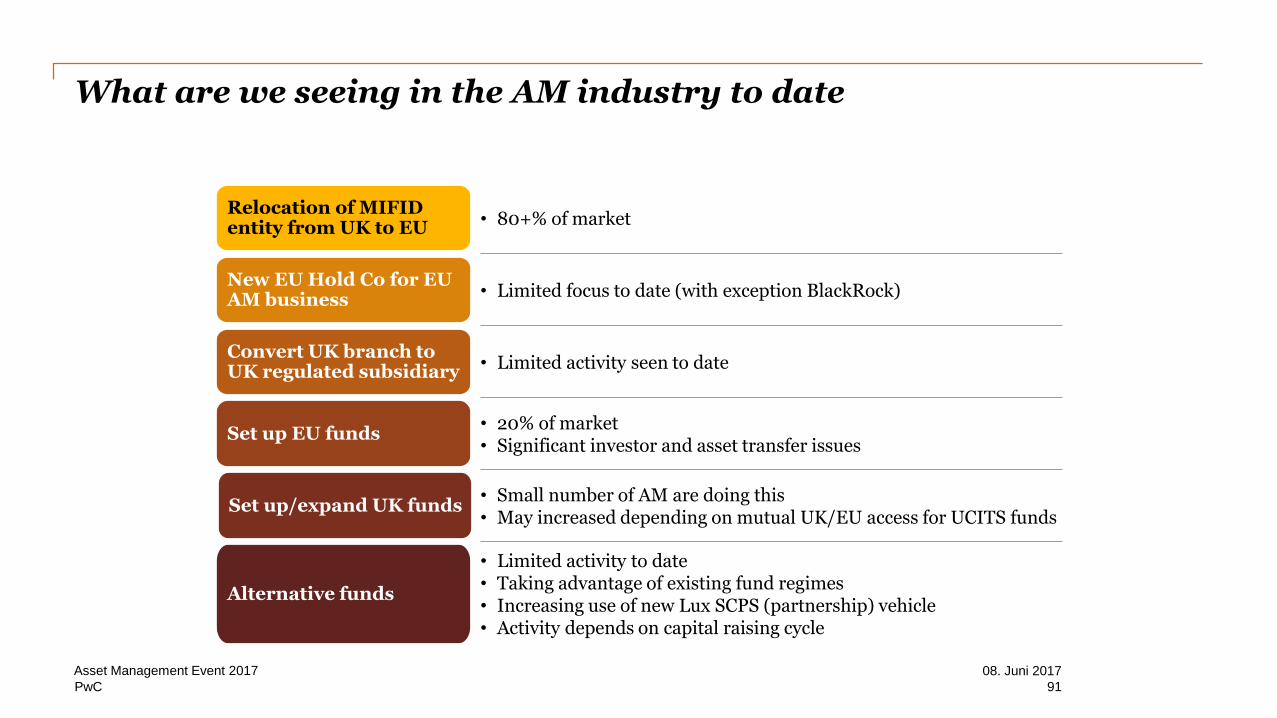

What are we seeing in the AM industry to date

Relocation of MIFID entity from UK to EU

New EU Hold Co for EU AM business

Convert UK branch to UK regulated subsidiary

Set up EU funds

Set up/expand UK funds

Alternative funds

• 80+% of market

• Limited focus to date (with exception BlackRock)

• Limited activity seen to date

• 20% of market• Significant investor and asset transfer issues

• Limited activity to date• Taking advantage of existing fund regimes • Increasing use of new Lux SCPS (partnership) vehicle• Activity depends on capital raising cycle

• Small number of AM are doing this• May increased depending on mutual UK/EU access for UCITS funds

08. Juni 2017Asset Management Event 2017

91

PwC

What actions are asset servicers taking?

08. Juni 2017Asset Management Event 2017

92

Review legal entity/booking model and services set-up and client book to understand business at risk and opportunities

Set-up EU wide/cross-divisional Brexit task force

Develop client communication strategy

Identify any new authorisations, legal entity structures and operating model changes required and prepare implementation plan

Setup ongoing Brexit negotiation / regulatory intelligence

PwC

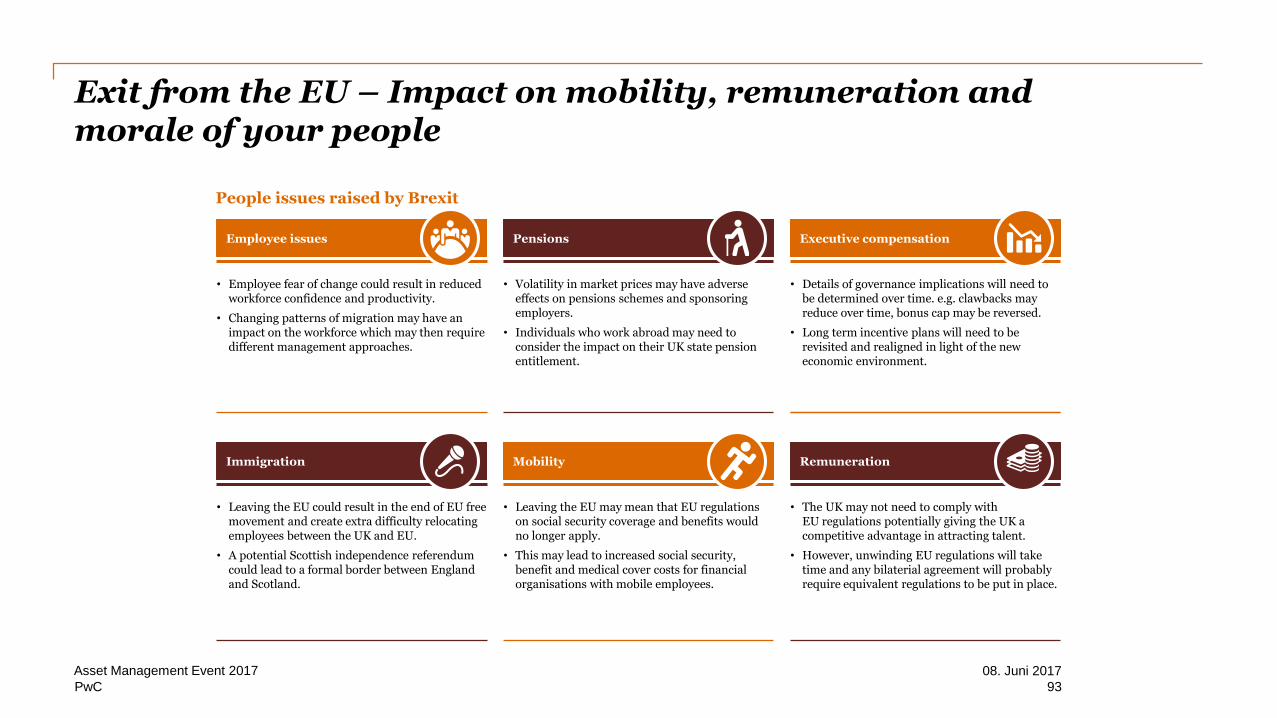

Exit from the EU – Impact on mobility, remuneration and morale of your people

Employee issues

• Employee fear of change could result in reduced workforce confidence and productivity.

• Changing patterns of migration may have an impact on the workforce which may then require different management approaches.

Executive compensation

• Details of governance implications will need to be determined over time. e.g. clawbacks may reduce over time, bonus cap may be reversed.

• Long term incentive plans will need to be revisited and realigned in light of the new economic environment.

Immigration

• Leaving the EU could result in the end of EU free movement and create extra difficulty relocating employees between the UK and EU.

• A potential Scottish independence referendum could lead to a formal border between England and Scotland.

Pensions

• Volatility in market prices may have adverse effects on pensions schemes and sponsoring employers.

• Individuals who work abroad may need to consider the impact on their UK state pension entitlement.

Mobility

• Leaving the EU may mean that EU regulations on social security coverage and benefits would no longer apply.

• This may lead to increased social security, benefit and medical cover costs for financial organisations with mobile employees.

Remuneration

• The UK may not need to comply with EU regulations potentially giving the UK a competitive advantage in attracting talent.

• However, unwinding EU regulations will take time and any bilaterial agreement will probably require equivalent regulations to be put in place.

People issues raised by Brexit

08. Juni 2017Asset Management Event 2017

93

PwC

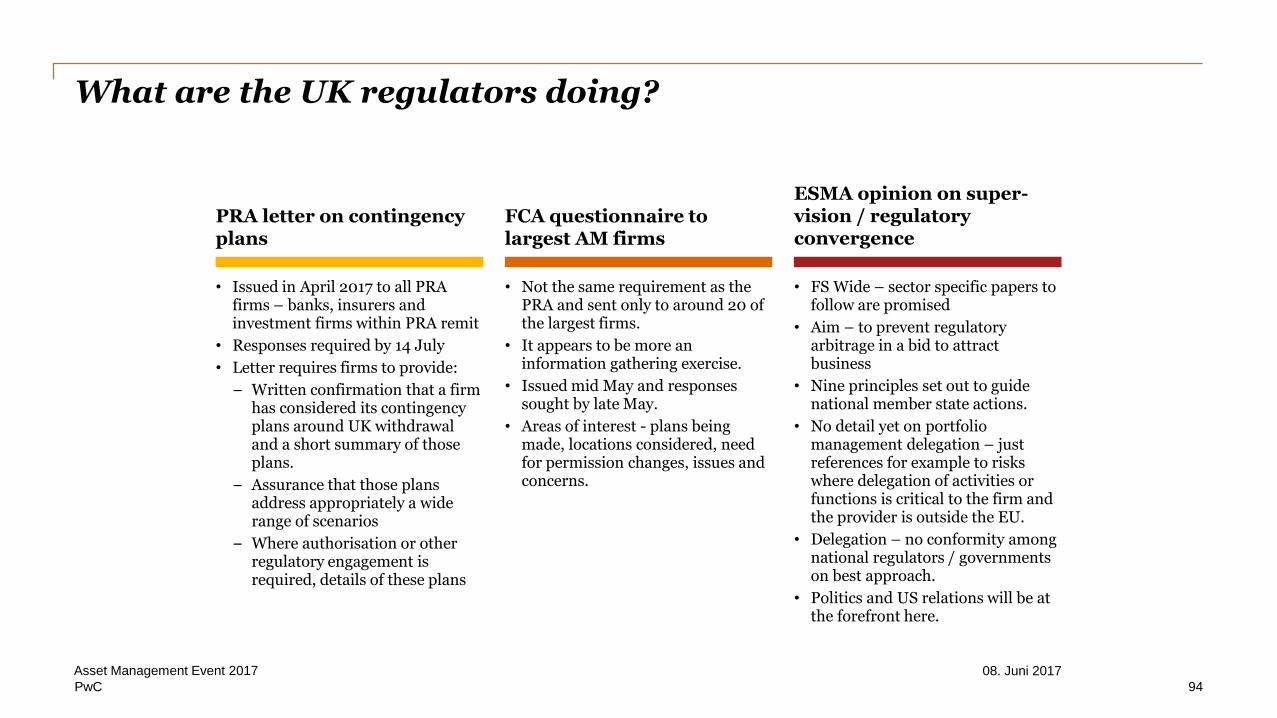

What are the UK regulators doing?

94

• Issued in April 2017 to all PRA firms – banks, insurers and investment firms within PRA remit

• Responses required by 14 July

• Letter requires firms to provide:

– Written confirmation that a firm has considered its contingency plans around UK withdrawal and a short summary of those plans.

– Assurance that those plans address appropriately a wide range of scenarios

– Where authorisation or other regulatory engagement is required, details of these plans

• Not the same requirement as the PRA and sent only to around 20 of the largest firms.

• It appears to be more an information gathering exercise.

• Issued mid May and responses sought by late May.

• Areas of interest - plans being made, locations considered, need for permission changes, issues and concerns.

• FS Wide – sector specific papers to follow are promised

• Aim – to prevent regulatory arbitrage in a bid to attract business

• Nine principles set out to guide national member state actions.

• No detail yet on portfolio management delegation – just references for example to risks where delegation of activities or functions is critical to the firm and the provider is outside the EU.

• Delegation – no conformity among national regulators / governments on best approach.

• Politics and US relations will be at the forefront here.

PRA letter on contingency plans

FCA questionnaire to largest AM firms

ESMA opinion on super-vision / regulatory convergence

08. Juni 2017Asset Management Event 2017

PwC

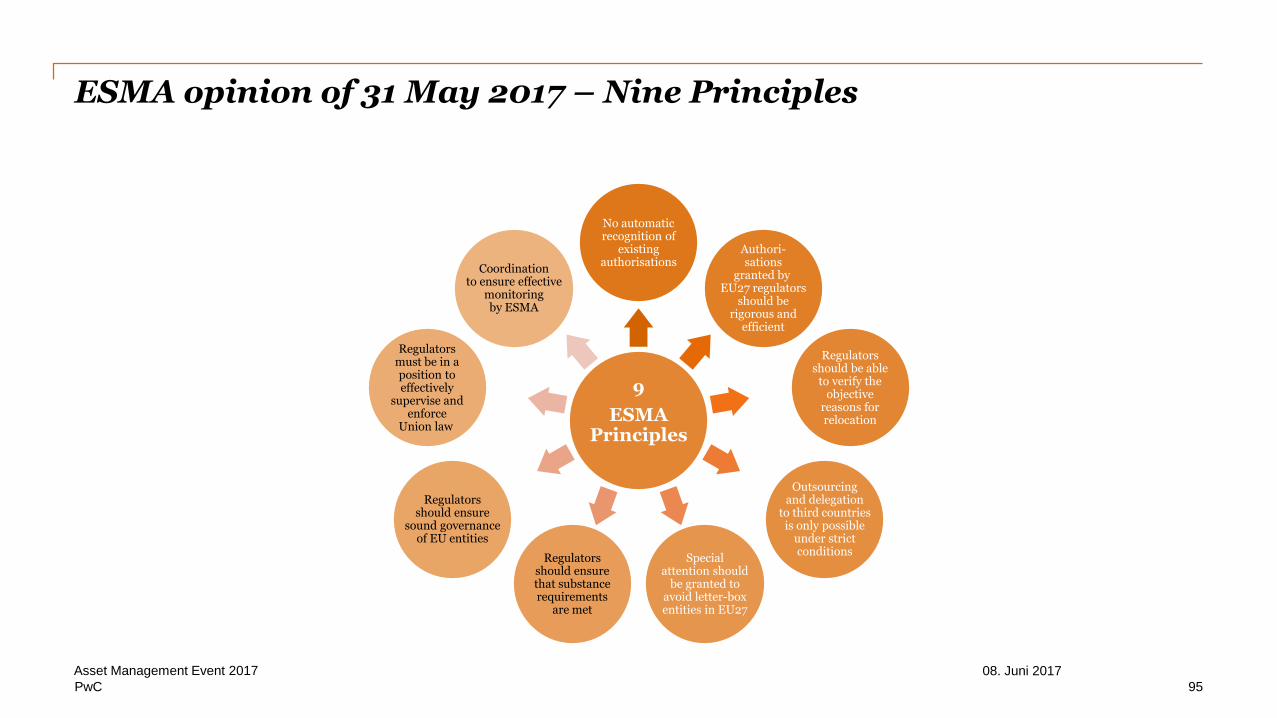

ESMA opinion of 31 May 2017 – Nine Principles

95

No automaticrecognition of

existingauthorisations

Specialattention should

be granted toavoid letter-boxentities in EU27

Regulatorsshould ensurethat substancerequirements

are met

Outsourcingand delegation

to third countriesis only possible

under strictconditions

Regulatorsshould ensure

sound governanceof EU entities

Regulatorsshould be able

to verify theobjective

reasons forrelocation

Regulatorsmust be in aposition toeffectively

supervise andenforce

Union law

Authori-sations

granted by EU27 regulators

should berigorous and

efficient

Coordinationto ensure effective

monitoringby ESMA

9

ESMAPrinciples

08. Juni 2017Asset Management Event 2017

PwC

Our assessment of the top 5 locations…

France Ireland

The Netherlands Germany Luxembourg

1Option

Pursuit of post-Brexit opportunities with collaboration from industry, regulators and government

Actively pursuing post-Brexit relocations with new BaFin website targeting foreign banks

Set up new teams in order to manage Brexit-related authorisation queries FS

Partnership between government and Luxembourg Financial Industry Federation to develop location as a major financial centre

Preference is for a solution that causes the least harm to economic interactions between the UK and the EU.

2Option

3Option

4Option

5Option

• 2 AMs in the top 400 AM ranking

• High satisfaction with schools and educational facilities & one of the safest countries in Europe

• Lowest labour force base but over 26k is employed in FS sector

• Highest score for activities which are auxiliary to FS.

• 27 AMs in top 400 AM ranking

• Very good score in culture and environment assessment

• Strong labour force base

• Strong financial sector market infrastructure

• 3 AMs in top 400 AM ranking

• Low score for infrastructure compared to other jurisdictions

• Average salaries within FS sector

• Strong financial market infrastructure

• 16 AMs in the top 400 AM ranking

• Well developed infrastructure

• Highest score in the human capital index

• Affordable office space and highest office availability of over 15%

• 32 AMs in the top 400 AM ranking

• Well developed infrastructure and affordable housing

• Biggest labour force base and high number employed in FS

• Office availability could become an issue and expectation of rent rises

Regulator response

96

08. Juni 2017Asset Management Event 2017

PwC

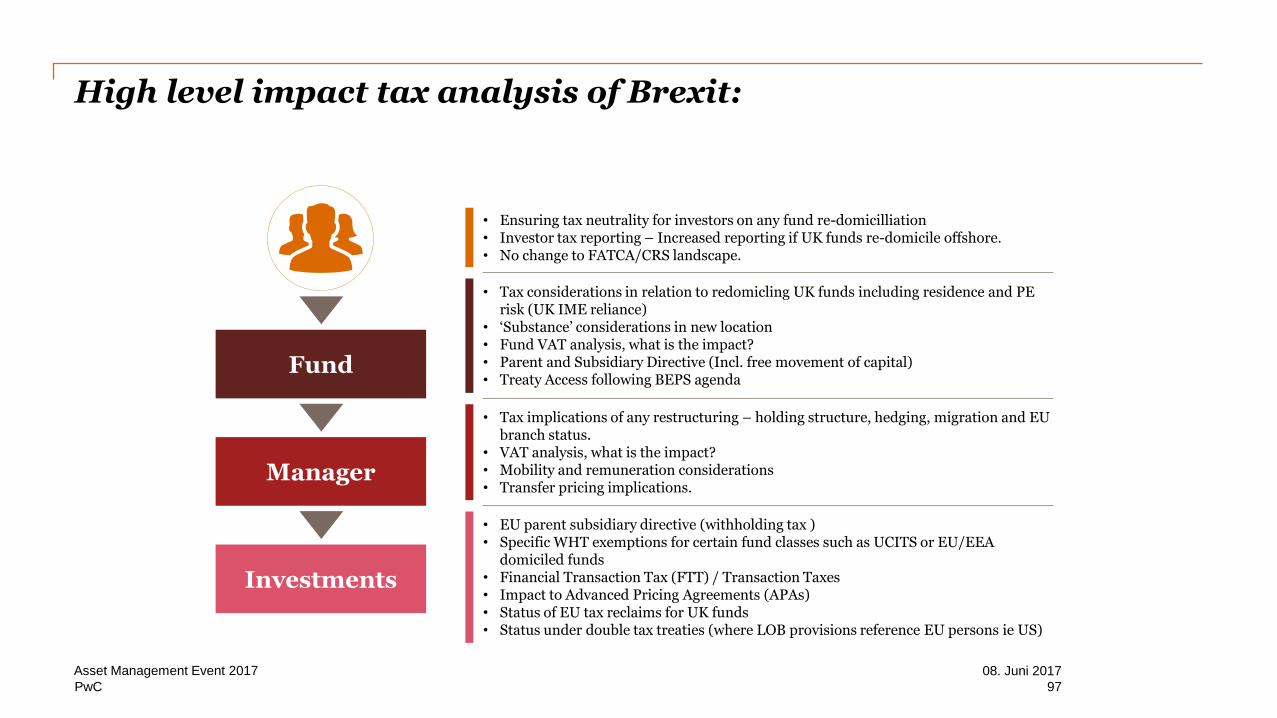

High level impact tax analysis of Brexit:

Fund

Investments

Manager

97

08. Juni 2017Asset Management Event 2017

• Ensuring tax neutrality for investors on any fund re-domicilliation• Investor tax reporting – Increased reporting if UK funds re-domicile offshore.• No change to FATCA/CRS landscape.

• Tax considerations in relation to redomicling UK funds including residence and PE risk (UK IME reliance)

• ‘Substance’ considerations in new location • Fund VAT analysis, what is the impact?• Parent and Subsidiary Directive (Incl. free movement of capital)• Treaty Access following BEPS agenda

• Tax implications of any restructuring – holding structure, hedging, migration and EU branch status.

• VAT analysis, what is the impact?• Mobility and remuneration considerations• Transfer pricing implications.

• EU parent subsidiary directive (withholding tax )• Specific WHT exemptions for certain fund classes such as UCITS or EU/EEA

domiciled funds• Financial Transaction Tax (FTT) / Transaction Taxes• Impact to Advanced Pricing Agreements (APAs)• Status of EU tax reclaims for UK funds• Status under double tax treaties (where LOB provisions reference EU persons ie US)

PwC

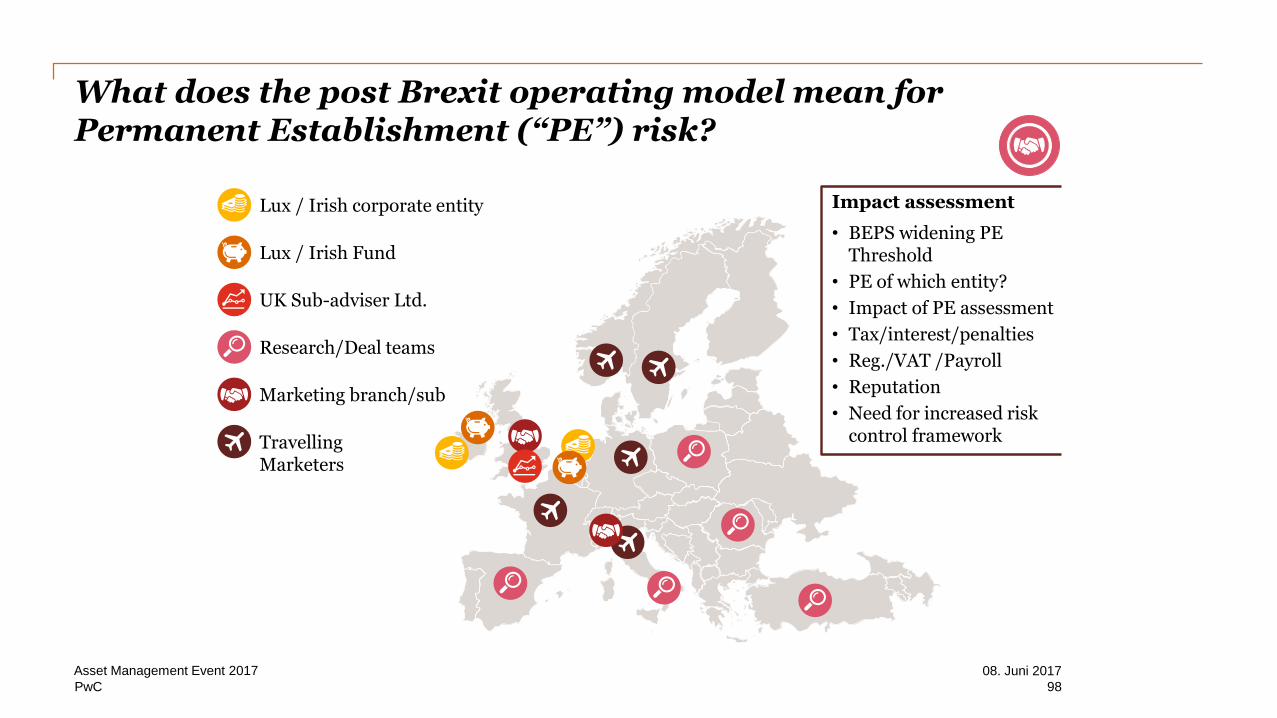

UK Sub-adviser Ltd.

Marketing branch/sub

Lux / Irish corporate entity

Research/Deal teams

Travelling Marketers

Lux / Irish Fund

What does the post Brexit operating model mean for Permanent Establishment (“PE”) risk?

Impact assessment

• BEPS widening PE Threshold

• PE of which entity?

• Impact of PE assessment

• Tax/interest/penalties

• Reg./VAT /Payroll

• Reputation

• Need for increased risk control framework

98

08. Juni 2017Asset Management Event 2017

PwC

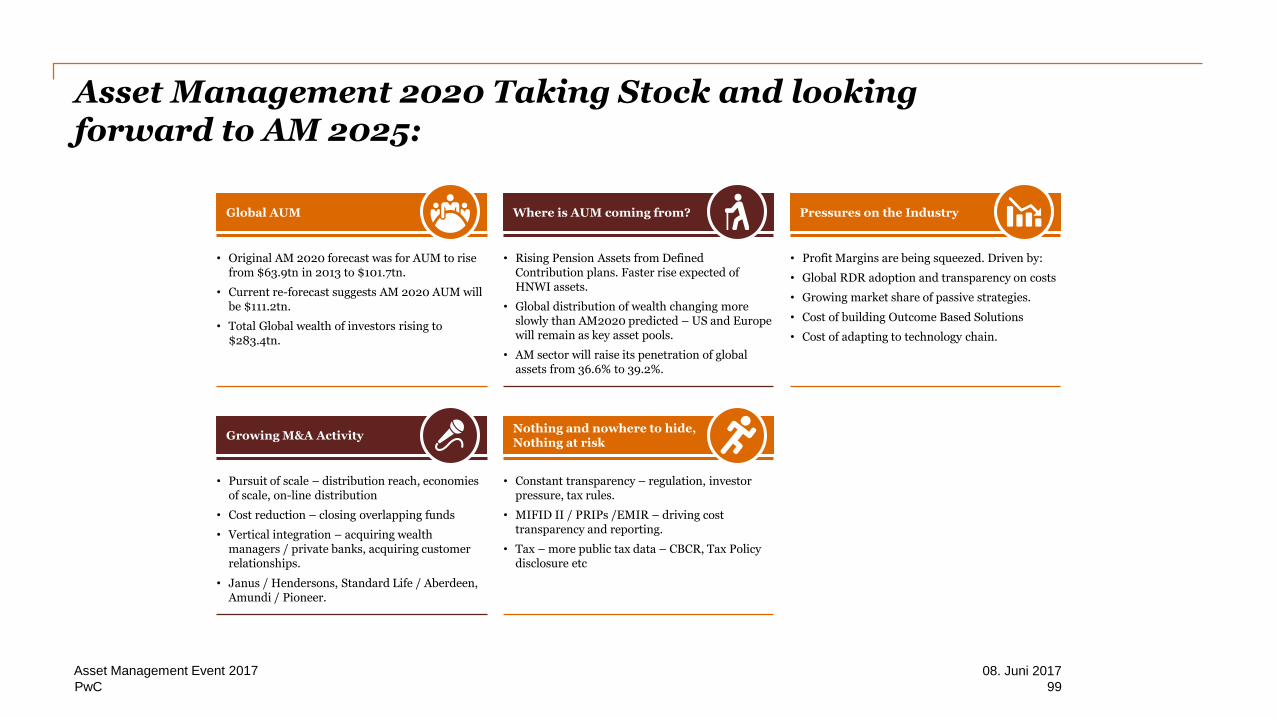

Asset Management 2020 Taking Stock and looking forward to AM 2025:

Global AUM

• Original AM 2020 forecast was for AUM to rise from $63.9tn in 2013 to $101.7tn.

• Current re-forecast suggests AM 2020 AUM will be $111.2tn.

• Total Global wealth of investors rising to $283.4tn.

Pressures on the Industry

• Profit Margins are being squeezed. Driven by:

• Global RDR adoption and transparency on costs

• Growing market share of passive strategies.

• Cost of building Outcome Based Solutions

• Cost of adapting to technology chain.

Growing M&A Activity

• Pursuit of scale – distribution reach, economies of scale, on-line distribution

• Cost reduction – closing overlapping funds

• Vertical integration – acquiring wealth managers / private banks, acquiring customer relationships.

• Janus / Hendersons, Standard Life / Aberdeen, Amundi / Pioneer.

Where is AUM coming from?

• Rising Pension Assets from Defined Contribution plans. Faster rise expected of HNWI assets.

• Global distribution of wealth changing more slowly than AM2020 predicted – US and Europe will remain as key asset pools.

• AM sector will raise its penetration of global assets from 36.6% to 39.2%.

Nothing and nowhere to hide, Nothing at risk

• Constant transparency – regulation, investor pressure, tax rules.

• MIFID II / PRIPs /EMIR – driving cost transparency and reporting.

• Tax – more public tax data – CBCR, Tax Policy disclosure etc

99

08. Juni 2017Asset Management Event 2017

PwC

Asset Management 2020 Taking Stock and looking forward to AM 2025:

Global AUM

• Current estimate AUM will almost doubled from 2105 to be $145tn.

• AUM growth will be uneven across time period and globally.

• Political and Economic risks – Populism, Brexit, Europe, China’s economy, US policy and regulation.

Product Diversification

• New financing opportunities will arise for Funds.

• Financing real assets, real economy funding.

• Facilitating individual pension provision.

• Global Banks will continue to be constrained by regulation.

Drive for tailored solutions

• Move to Solutions delivery

• Active, passive and Alts strategies become building blocks multi-asset, outcome driven solutions.

• ESG and Impact Investing will continue to rise.

• Drive AM firms to achieve scale and product diversity.

Investor Power

• Balance of power shifting to investors

• Regulation, transparency and new entrants disrupting traditional value chains.

• Real time data availability and analytics make financial products and markets transparent.

• Clear differentiation between Alpha and Beta. Beta becomes commoditized and fees will fall.

Technology

• Technology will accelerate and drive change across the value chain and impact:

• Client acquisition, customization of investment advice, client engagement and distribution.

• Research and portfolio management

• Middle and Back office processes

Growing M&A Activity

• Largest Firms will have – Scale, be Price competitive and strong Technology.

• Smaller, specialist firms will focus on excellent investment performance or service.

100

08. Juni 2017Asset Management Event 2017

PwC

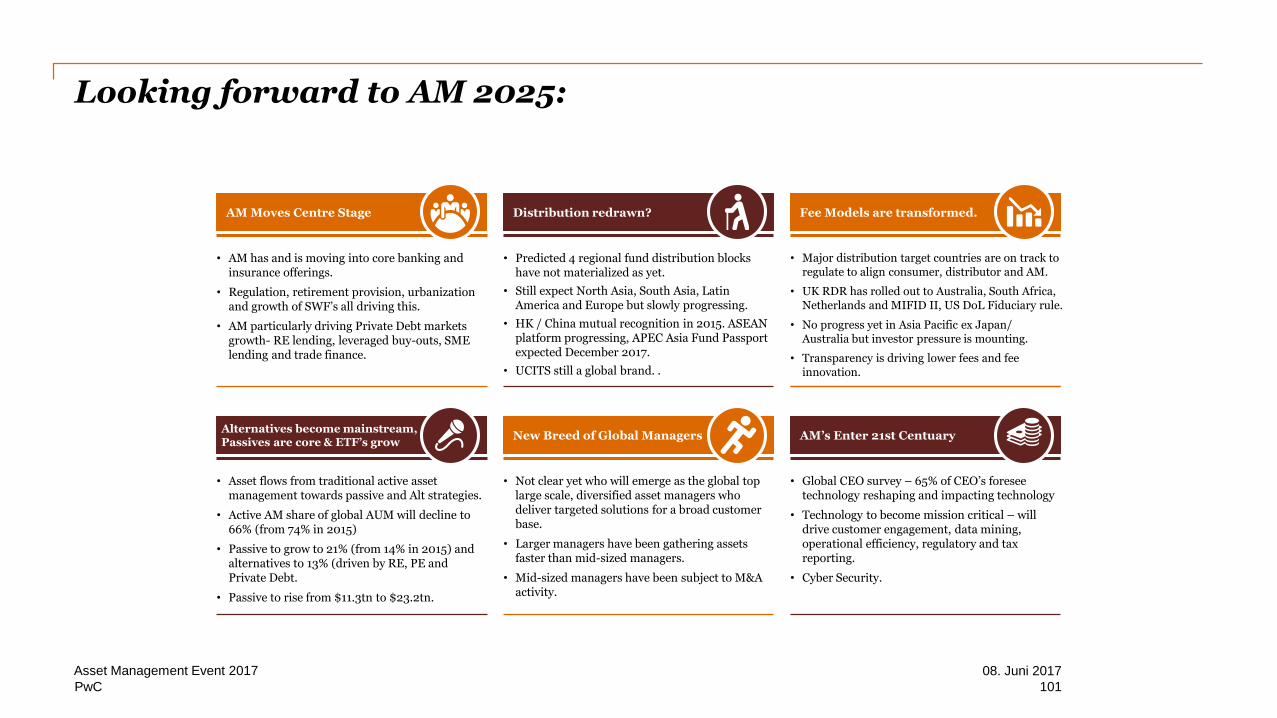

Looking forward to AM 2025:

AM Moves Centre Stage

• AM has and is moving into core banking and insurance offerings.

• Regulation, retirement provision, urbanization and growth of SWF’s all driving this.

• AM particularly driving Private Debt markets growth- RE lending, leveraged buy-outs, SME lending and trade finance.

Fee Models are transformed.

• Major distribution target countries are on track to regulate to align consumer, distributor and AM.

• UK RDR has rolled out to Australia, South Africa, Netherlands and MIFID II, US DoL Fiduciary rule.

• No progress yet in Asia Pacific ex Japan/Australia but investor pressure is mounting.

• Transparency is driving lower fees and fee innovation.

Alternatives become mainstream, Passives are core & ETF’s grow

• Asset flows from traditional active asset management towards passive and Alt strategies.

• Active AM share of global AUM will decline to 66% (from 74% in 2015)

• Passive to grow to 21% (from 14% in 2015) and alternatives to 13% (driven by RE, PE and Private Debt.

• Passive to rise from $11.3tn to $23.2tn.

Distribution redrawn?

• Predicted 4 regional fund distribution blocks have not materialized as yet.

• Still expect North Asia, South Asia, Latin America and Europe but slowly progressing.

• HK / China mutual recognition in 2015. ASEAN platform progressing, APEC Asia Fund Passport expected December 2017.

• UCITS still a global brand. .

New Breed of Global Managers

• Not clear yet who will emerge as the global top large scale, diversified asset managers who deliver targeted solutions for a broad customer base.

• Larger managers have been gathering assets faster than mid-sized managers.

• Mid-sized managers have been subject to M&A activity.

AM’s Enter 21st Centuary

• Global CEO survey – 65% of CEO’s foresee technology reshaping and impacting technology

• Technology to become mission critical – will drive customer engagement, data mining, operational efficiency, regulatory and tax reporting.

• Cyber Security.

101

08. Juni 2017Asset Management Event 2017

PwC

Any questions?

102

08. Juni 2017Asset Management Event 2017

PwC

Zusammenfassung / Q&A18:30

Daniel Pajer, PwC

103

08. Juni 2017Asset Management Event 2017

Wie hat Ihnen die Veranstaltung gefallen?

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional

advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No

representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this

publication, and, to the extent permitted by law, PricewaterhouseCoopers AG, its members, employees and agents do not

accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to

act, in reliance on the information contained in this publication or for any decision based on it.

© 2017 PricewaterhouseCoopers AG. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers AG

which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal

entity.

Wir freuen uns auf Ihr Feedback.

PwC

Annex

105

08. Juni 2017Asset Management Event 2017

PwC

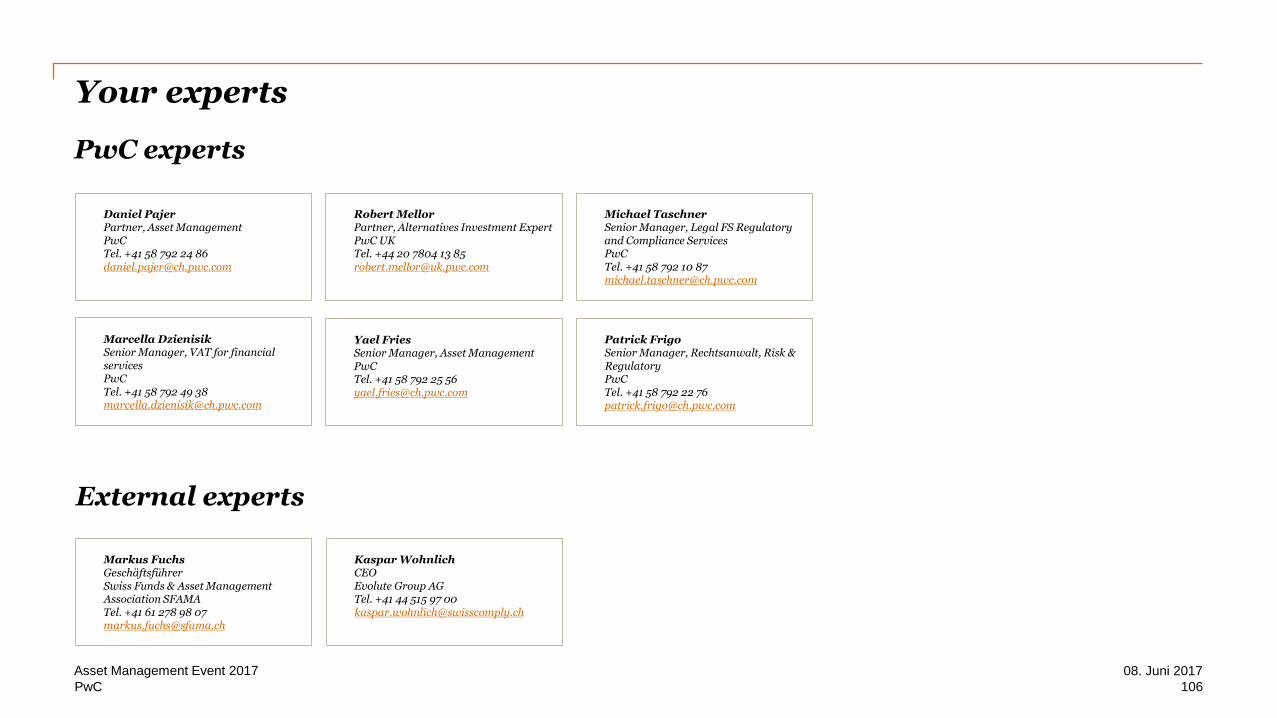

Your experts

106

08. Juni 2017Asset Management Event 2017

Yael FriesSenior Manager, Asset ManagementPwCTel. +41 58 792 25 [email protected]

Daniel PajerPartner, Asset ManagementPwCTel. +41 58 792 24 [email protected]

Michael TaschnerSenior Manager, Legal FS Regulatory and Compliance ServicesPwCTel. +41 58 792 10 [email protected]

Robert MellorPartner, Alternatives Investment ExpertPwC UKTel. +44 20 7804 13 [email protected]

Patrick FrigoSenior Manager, Rechtsanwalt, Risk & RegulatoryPwCTel. +41 58 792 22 [email protected]

Marcella DzienisikSenior Manager, VAT for financialservicesPwCTel. +41 58 792 49 [email protected]

Markus FuchsGeschäftsführerSwiss Funds & Asset Management Association SFAMATel. +41 61 278 98 [email protected]

Kaspar WohnlichCEOEvolute Group AG Tel. +41 44 515 97 00 [email protected]

PwC experts

External experts