Embed Size (px)

Citation preview

Athens (Greece)Bogota [Colombia]Brussels (Belgium)Buenos Aires (Argentina)Caracas (Venezuela)Lisbon (Portugal)London (United Kingdom)Madrid (Spain)Manila (Philippines)Milan (Italy)Mexico D.F. (Mexico)Munich (Germany) New Jersey (USA)Paris (France)Santiago de Chile [Chile]São Paulo [Brazil]Toronto [Canada] www.mapfrere.com

C

M

Y

CM

MY

CY

CMY

K

publi_mapfrere_260X70.ai 1 14/06/12 12:56publi_mapfrere_260X70.ai 1 14/06/12 12:56

MARKETNEWS,DATAANDINSIGHTALLDAY,EVERYDAY TUESDAY19JUNE2012

ISSUE3,627

New sustainability principlesto strengthen riskmanagement of insurers

Companies House

Big Interview

Reinsurancefuelsmodestgrowthforbrokers p9-12

Beardmore plansto double BMS’sbrokerage p4-5

IIS news

Regulator urgesfocus on dignityand protection p3

p8

Nearly30companiescommittoprojectlaunchedtodayinRio

2

NEWSwww.insuranceday.com| Tuesday 19 June 2012

Marketnews,dataandinsightallday,everydayInsuranceDay istheworld’sonlydailynewspaperfortheinternationalinsuranceandreinsuranceandriskindustries.ItsprimaryfocusisontheLondonmarketandwhataffectsit,concentratingonthekeyareasofcatastrophe,propertyandmarine,aviationandtransportation.It isavailableinprint,PDF,mobileandonlineversionsandisreadbymorethan10,000peopleinmorethan70countriesworldwide.

Firstpublishedin1995,InsuranceDayhasbecomethefavouritepublicationfortheLondonmarket,whichreliesonitsmixofnews,analysisanddatatokeepintouchwiththisfast-movingandvitallyimportantsector.Itsexperiencedandhighlyskilledinsurancewritersarewellknownandrespectedinthemarketandtheirinsightisbothcompellingandvaluable.

InsuranceDayalsoproducesanumberofmust-attendannualeventstocomplementitsdailyoutput.TheLondonandBermudasummitsareexclusivenetworkingconferencesforseniorexecutives;meanwhile, theLondonMarketAwardsrecogniseandcelebratetheverybestintheindustry.ThenewInsuranceTechnologyCongressprovidesauniquefocusonhowITishelpingtotransformtheLondonmarket.

FormoredetailonInsuranceDayandhowtosubscribeorattenditsevents,gotoinfo.insuranceday.com

InsuranceDay,119FarringdonRoad,LondonEC1R3DA

Editor:RichardBanks+44(0)[email protected]

Deputyeditor:ScottVincent+44(0)[email protected]

Seniorreporter:ChristopherMunro+44(0)[email protected]

Globalmarketseditor:GrahamVillage+44(0)[email protected]

Globalmarketseditor:RasaadJamie+44(0)[email protected]

Managingeditor:GregDobie+44(0)[email protected]

Commercialdirector:AndréaPratt+44(0)2070174708Salesdirector:AndrewStone+44(0)2070174027Senioraccountmanager:SarahDean+44(0)2070174122Senioraccountmanager:SirachYeboah+44(0)2070177670Senioraccountmanager:AndrewStone+44(0)2070174027Marketingmanager:RandeepPanesar+44(0)2070173809Keyaccountsmanager:VerityBlair+44(0)2070174998Subscriptions:LisaGambino+44(0)2033773873Headofproduction:MariaStewart+44(0)2070175819Advertisingproductionassistant:EmmaWix+44(0)2070175196Productioneditor:TobyHuntington+44(0)2070175705Subeditor:JessicaHills+44(0)2070175161Subeditor:AliMasud+44(0)2070175161Productionexecutive:ClaireBanks+44(0)2070175821Eventsmanager:NataliaKay+44(0)2070175173

Editorialfax:+44(0)2070174554Display/classifiedadvertisingfax:+44(0)2070174554Subscriptionsfax:+44(0)2070174097

Allstaffemail: [email protected]

InsuranceDay isaneditoriallyindependentnewspaperandopinionsexpressedarenotnecessarilythoseofInformaUKLtd.InformaUKLtddoesnotguaranteetheaccuracyoftheinformationcontainedinInsuranceDay,nordoesitacceptresponsibilityforerrorsoromissionsortheirconsequences.

ISSN1461-5541.RegisteredasanewspaperatthePostOffice.PublishedinLondonbyInformaUKLtd,MortimerHouse,37/41MortimerStreet,London,W1T3JH

PrintedbyNewsfaxInternational,Unit16,BowIndustrialPark,CarpentersRoad,LondonE152DZ

© Informa UK Ltd 2012.

Nopartofthispublicationmaybereproduced,storedinaretrievalsystem,ortransmittedinanyformorbyanymeanselectronic,mechanical,photographic,recordedorotherwisewithoutthewrittenpermissionofthepublisherofInsuranceDay.

Australia introducesstandard flood definition

A ustralia’s government hasenacted regulations that willintroduce a standard defini-tion of flood to insurance con-

tracts following 18 months of discussionswith the insurance sector.

According to the regulations, flood willbe used in insurance contracts to mean“the covering of normally dry land bywater that has escaped or been releasedfrom the normal confines of: any lake, orany river, creek or other natural water-course, whether or not altered or modi-fied; or any reservoir, canal, or dam”.

The influential Insurance Council ofAustralia (ICA), whose members repre-sent approximately 90% of the A$30bn-plus ($30bn) total premium income writ-ten each year by private sector generalinsurers in Australia, welcomed the gov-ernment move.

Yet itwasquicktopointoutmanycarri-ers had already adopted this definition,with other members well advanced intheir preparations, in the wake of publiccriticism of a number of carriers’ han-dling of the fallout from last year’s floodsin Queensland and Victoria.

Accordingtothegovernment,ambiguityover previous interpretations of the word“flood” in insurance policies has provenproblematic for consumers, with manyunsurewhethertheywerecoveredornot.

However, ICA chief executive, RobWhelan, advised the insurance-buyingpublic they would still need to assesswhether they needed flood coverage.

“Introducing a standard definitiondoes not mean they [consumers] haveflood cover if they have not purchased

the appropriate policy,” he cautioned.The regulations allow a two-year tran-

sitional period for insurers for productdisclosure statements to be updated, staffto be retrained and systems to bechanged, the government said.

However, they allow insurers to use thestandarddefinitionwithimmediateeffect.

Whelan said the regulations shouldserve as a reminder to all levels of govern-ment they should not overlook the impor-tance of protecting communities fromfloodrisks.

“The standard definition is one part ofa complex issue,” he added. “Insurancecan only help communities recover fromthe impact of floods. Governments areresponsible for protecting at-risk com-munities in the first place,” he added.

“Urgent investments in permanent,well-designed physical mitigation meas-ures – such as levees, barrages, flood gatesandimproveddrainage–arestillneeded.”

The ICA first attempted to introduce astandard flood definition into insurancecontracts four years ago but it wasrejected on anti-competition grounds bythe competition commission.

Insured losses from last year’s Queens-land floods totalled A$2.4bn, with almost60,000 claims received.

New reinsurance broker StoneHillpromises fresh approach to businessNewly launched StoneHill ReinsurancePartners is promising a fresh approachto reinsurance broking by servicing cli-ents’ needs without “fitting their need toan in-house product offering”, writesRichard Banks.

The new Minneapolis-based com-pany’s principals, experienced brokingfigures Dan Koshiol and Lindsay Ginter,have an established track record in theprofessional liability field but alsoboast strong relationships with a widearray of reinsurers and other servicefirms, which, they claim, will provide“broader access to services and capabil-

ities than the traditional intermediary”.Koshiol, whose 15-year career includes

stints at Guy Carpenter, John B Collins andEW Blanch, said: “We see a market needforabrokerwhowillsolelyinvesttimeandresources on their clients. As brokers con-solidate and look for additional revenuegrowth, some clients are being asked topurchase, at an added cost, products andservices that historically have beenincludedinthebrokeragerelationship.”

Ginter has also held positions at Collinsand EW Blanch and most recently man-aged a reinsurance captive for WellsFargo and Company.

“We see a market need for abroker who will solelyinvest time and resourceson their clients.”

Dan KoshiolStoneHill

Queenslandfloods:Amemberof theAustralianAirForce,helpsevacuatefloodvictims

AP Photo/Royal Australian Air Force,Leading Aircraftman Benjamin Evans

“The standard definition isone part of a complexissue... Insurance can onlyhelp communities recoverfrom the impact of floods.Governments areresponsible for protectingat-risk communities inthe first place”

Rob WhelanICA

Greg DobieManaging editor

Morenewsallday,everyday,atwww.insuranceday.com @

3

NEWSwww.insuranceday.com| Tuesday 19 June 2012

Brazil’s regulator urges insurance focuson dignity and environmental protection

B razil’s insurance regula-tor called for insuranceindustry innovation tohelp achieve the twin

goals of environmental protectionand human dignity in Latin Amer-ica’s largest nation.

In his address to the opening cer-emony of this year’s InternationalInsurance Society seminar, takingplace in Rio de Janeiro, LucianoPortal Santanna, superintendentof the Superintendência de Seg-uros Privados, said the interna-tional insurance sector has animportant role to play in the coun-try’s development.

“It is a happy coincidence thisevent is being held alongside theRio+20 conference. Today there is a

investmentoverthenextfouryears.”De Oliviera said there are a

number of social and demographicdevelopments that will aid devel-opment. “The economy is becom-ing more formal and income isbeing better distributed – a very

prosperous middle class is expand-ing,” he said.

“Investment and innovation areneeded to translate this into resultsfor the global insurance industry,but I’m sure the industry will beable to succeed in this task.”

Scott Vincent,Rio de JaneiroDeputy editor

Childrenoutsideasquat indowntownSaoPaulo: thebuildinglacks electricityandrunningwaterandisoccupiedbymanyhomeless families

AP Photo/Andre Penner

Morenewsallday,everyday,atwww.insuranceday.com @

consensus environmental protec-tion is a need for humanity. It mustalso be highlighted sustainabledevelopment does mean develop-ment,”hesaid.

“Another important principlewhich must be considered is thedignity of human beings. Wemust have a balance between allthese principles.

“Here in Brazil, we have millionsof people excluded from havingpowersupply–amostbasicneed.

“Intime,thesepeoplewillmovetoa consumption market and to dothis, investment in developmentthroughtechnologywillbeneeded.”

Santanna said it is important fortheindustrytoreflectonincentivesto make this happen.

“There must be ways to incentiv-ise so insurance can play an impor-tantrole inthedevelopmentofnewtechnologies,” he said.

Dyogo Henrique de Oliviera, sec-retary to the Ministry of Finance

with responsibility for insurance,said the Brazilian insurance sectorwill grow in line with the country’seconomic growth. “The moreincentives there are, the more peo-ple will buy insurance,” he said.

“TheBrazilianeconomyhasveryfavourable forecasts for the future.During the past 100 years, actualgrowth in the Brazilian economyhas averaged 4.8% each year,despite a 20-year period of lowgrowth during this time.

“Brazil today has a stable econ-omy at a macro-economic levelwith inflation under control. Wehave investment in development –our acceleration growth pro-gramme forecasts $1.3trn of

More IISnewsonline

4

BIGINTERVIEWwww.insuranceday.com| Tuesday 19 June 2012

‘Restructuring has provided greaterclarity and focus to the business’Oneof thepublicly statedobjectives ofCarlBeardmore’s tenure as chief executive ofBMS isto double the size of its brokerageby2015

Beardmore was appointed chief executive of BMS Associates inJune 2010 and heads both the UK and US operations. His primaryfocus is to lead the successful execution of BMS’s strategy:doubling the size of the broking business by 2015 and developingthe overall business proposition.

Beardmore has been actively involved with BMS for eight years,initially as a strategic adviser and from July 2008 as a non-executive director.

He has a wealth of experience, advising in the insurance marketsas well as running businesses in other industries. He has worked asa strategic adviser to leading players in the London insurancesector since 1997.

Beardmore began his career in the 1970s in the manufacturingindustries and moved on to establish his own strategic consultingbusiness in 1993.

Carl Beardmore CV

Rasaad JamieGlobal markets editor

F ew companies have beenso radically transformedin terms of both businessstrategy and structure as

specialist London market insur-ance group BMS over the past 18months. This process of change,which is still ongoing, is describedby Carl Beardmore, BMS’s chiefexecutive, as a “complete re-engi-neering” of the business which willchange the dynamics of the com-pany even more dramatically overthe next few years.

Although Beardmore, who wasappointed chief executive in June2010, is very much part of thechange, he was no stranger to theboard of BMS, having beeninvolved with the company for theprevious eight years, first as a stra-tegic adviser, then for the past twoyears as a non-executive director.

According to its results state-ment released last week, BMS gen-erated revenues of £53.2m($83.4m) last year through its fourbusiness divisions: reinsurance,wholesale insurance, specialtyinsurance and its Pioneer-branded underwriting platform.But 2010 (when the companypassed the £50m revenue markfor the first time in its 32-year his-tory) was clearly a critical time forBMS. Two years earlier, the board

least double the size of BMS’s bro-kerage to £100m by 2015.

Employee-ownedBMS is a largely employee-ownedbusiness in which a third-partyinvestor (AHJ Holdings) histori-cally held a 25% stake. When BMSwas originally formed in 1980, AHJacted as the umbrella organisationfor the company which, in effect,involved providing a guarantee ofsupport in the early days of BMS’sevolution. In return for that duty,AHJ acquired an ownership stakein BMS. For a whole host of rea-sons, Beardmore explains, theinvestment remained in placeright up to the time when he tookover as chief executive. “I felt oneof the first things we needed to dowas to re-acquire that sharehold-ing and make us 100% employee-owned and independent.”

In 2011, BMS reached agreementtoacquirethesharesownedbyAHJfor£8m.Thetransactionwasstruc-tured in two tranches. “During2011 and the first quarter of 2012,we acquired the first tranche of theAHJ holding and this share buy-back resulted in a reduction in netassets of £4.2m at the year end. Weintend to acquire the balance of theAHJ shares during 2013.”

Beardmore, whose originalbackground is financial account-ing, had previously worked in anumberofindustrialsectorsacrossa range of managerial roles includ-ing financial, operational, com-mercial, sales and marketing.Mainly working for multinationalcompanies, the experience pro-videdhimwithagroundinginmostof the key disciplines necessary forthe successful running of anyorganisation. In 1997, after aperiod of running his own busi-ness, he began working as a strate-gic adviser to a number ofcompanies in the London insur-ance market.

“The type of consulting we didwas to help with the strategic re-engineering of businesses, so I wasalways dealing in the boardroom.

of directors had agreed and begunto implement a more dynamic,aggressive business strategy.While BMS was recognised as ahighly reputable and credibleorganisation, it was also per-ceived as a little too pedestrian inits way of doing business. Cer-tainly, by 2010, the company didnot generate a great deal of excite-ment in the market.

Beardmore, then still acting as astrategic adviser, was asked tobecome a non-executive directoron the board of BMS. He says hetook on the position with the fullintention of fulfilling the tradi-tional non-executive role of con-structively challenging theexecution of the strategy. “Butwhat happened during that periodwas it became quite clear the newstrategy required a different formof leadership. At the beginning of2010, the board acknowledgedthings needed to be changed and,as a result of a combination of fac-tors – the board’s familiarity withme, my understanding of the strat-egy of the business, my previousroles as business leader either inother companies or for myself –led them to conclude there wassomebody already within thebusiness who could fulfil the roleof chief executive, whose familiar-ity with it would minimise anyinterruption in momentum,”Beardmore says.

Akey,publiclystatedobjectiveofthe new strategy and Beardmore’stenure as chief executive is to at

The London insurance world isquite small and we were workingwithonechiefexecutive inapartic-ularsectorwhohappenedtohaveachief executive friend in the insur-ance sector who had a problemgrowing their business. That wasquite literally how I came to beworking in insurance.

“But once I was working in thesector, it became really interestingbecause here was an industry thatseemed to have been doing thesame things the same way for an

awfully long time. And there wasthe rise of companies like Aon andGuyCarpenter,whichgrewrapidlythrough acquisition, and, as aresultof that, thepositionof thetra-ditional London correspondentbroker position was being threat-ened because these large brokerswere winning the business directlyfrom clients and then increasinglypushing it through their ownhouses into the London market. Itwas a situation that was creating alot of new dynamics in the market-

Rei

nsu

ran

ce

Sp

ecia

list

insu

ran

ce

Wh

ole

sale

insu

ran

ce

JHIn

tern

edia

ries

/JH

Insu

ran

ceS

erv

ices

/P

ion

eer

Un

der

wri

tin

g

Chart: The four pillars of BMS’s business

place, which companies were hav-ing to respond to. Many companieswere struggling to grow andexpand. Profitability was gettingharder to achieve. I thought itseemed like an ideal sector todeploy our talents of inspiringbusiness success.”

Decision-makingThe immediate challenge for BMS,which was founded in 1980, was toimprove the company’s perform-ance and manage costs at the busi-ness unit level. In 2010, thisinvolvedoneofthecompany’smostexperienced brokers, Hugo Craw-ley, moving from his position aschairman of the holding companyto chairman of the broking busi-ness. Indeed, a number of provenpractitioners moved from the mainboard on to the broking board andthefocusbecamefarmoreorientedtowardsimprovingperformanceatthebusinessunit level.

“We changed the way in whichdecisions were taken. Too many ofthe decisions were being made atthetopoftheorganisation.Tome, ifyou don’t delegate the decision-making to the appropriate levelswithin the business it slows thebusiness down, which inevitablymanifests itself in the form of slowcustomer service.

“One thing I know as a customermyself of many products and fromhaving spoken to customerswithin a number of different con-texts is they want fast and effec-tive responses, they want a timelyresponse, so you have to engineeryour business in a way wheredecisions can be made quickly sothe client feels the benefit of that.In our market, which is domi-nated by some very large players,being fast, nimble and flexible isan important differentiator.Without being disrespectful tosome of the bigger companies, alarge organisation tends to beslower to react and making deci-sions. So if we are more nimble,we can service clients more effi-ciently than the competition.”

Four pillarsThe key focus of the restructuring,which has absorbed £15m of invest-ment over the past 18 months, wasto divide the business into four pil-lars: reinsurance, which in 2010accounted for 57% of BMS’s overallrevenue; specialist insurance(26%); wholesale insurance (17%);andthefourthpillar,whichisrepre-sented by BMS’s two underwritingplatforms JH Intermediaries (JHI)in the UK and JH Insurance Services(JHIS) in the US and by the launch of

a managing general agency, Pio-neer Underwriting, in April 2011.The restructuring, Beardmore says,immediately provided a greaterclarity and focus to the business. Atpresent, the investment is focusedon the reinsurance platform in theUS, on the wholesale business andon establishing BMS’s underwrit-ingplatforms.

JHI and JHIS, he explains, werepart of the traditional Jensen &HastingsbusinessthatbecamepartofBMSafewyearspreviously.Bothbusinesses were heavily focusedon the construction sectors in theUK and in the US. “As we are allaware, from 2008 onwards whenthe world went pear-shaped, theconstruction sector was affecteddramatically. As a first action, wehad to re-engineer completelythose businesses which, throughno fault of their own, found the car-pet pulled from under their feet.What we have been doing is tryingto retain the profitable parts of thebusiness as well as those parts ofthe business we think have gotpotential in the long term. But to beabsolutely candid, these busi-nesses are now much reduced insize and they now form part of ourPioneer-branded underwritingplatform. They are still using theJHI and JHIS names but under theumbrella of Pioneer.”

Freeing up wholesaleThere was a notable investment inthe wholesale insurance divisionin2010,whenateamofbrokers, ledby Nick Cook, moved from Willis toBMS, where they merged with thecompany’s existing wholesaleteam. The result, Beardmore says,was the creation of a strong, highlyproductive unit that in the first 12months hit all its objectives interms of business generation. Thewholesale division, which focuseson traditional facultative lines ofbusiness, has also made a verystrong start to 2012.

“The wholesale team is nowempowered to act under its ownauthority and autonomy as oftenas it needs to. I think it is a greatexample of what happens whenyou get really good people, withgood strong leadership, and givethem the ability to act and not bur-den them with bureaucracy butjust tell them to go out there andplay well, but play hard. We felt ifwe allowed them the freedom andthe autonomy to express them-selves and optimise their skills-sets, this would manifest itself inbetter solutions, better serviceand better relationships for ourclients who, we hoped, as a result

theUSisgreaterthanthe57%identi-fied geographically; the exact figureis more like 80%. A significant vol-ume of US business is brought intothe London market by BMS in itsrole as a correspondent broker andconsequently the geographic ori-ginsofthebusinessisobscured.

“At the moment, we are veryfocusedontheUSandIthinkforthenext two or three years we will con-tinue to be that way, but as thewholesale side of the business –which focuses on areas like SouthAfrica, the Middle East, Asia andAustralasia – grows, that willchange. Our long-term ambition isto serve reinsurance clients glo-bally. To begin with, we are focus-ing on the areas we know very well,but over time we will take more of aglobal view. It is essential we dothis to achieve our vision of becom-ing the most compelling independ-ent broker of choice.”

Trusted adviserAccording to Beardmore, anotherkey objective is for BMS to be a trulytrusted adviser to clients. “It is aphrase that has been overused but Ibelieve we can live up to it betterthan anybody else. Virtually all ourclients, whatever the nature of theirbusiness, have a large amount ofcapitaltheyareputtingatrisktocre-ate and develop a sustainable busi-ness and they need truly trustedadvisers that will ensure their capi-talisprotectedtoitsoptimallevel,soonly the amount of capital they arewantingtoputatriskisexposed.”

According to Beardmore, BMS’sclients also need help in analysingboth the existing and future state oftheir businesses to ensure they aregetting the best return on their cap-ital. “That is what is being expectedof insurance brokers now. Typi-cally, when I sit down with clientsthey don’t want me to tell them weare great brokers or we can puttogether a very good insuranceprogrammeforthem.Asfaras theyare concerned, every other brokercan do that and we shouldn’t be sit-ting in front of them if we can’t.

“They are looking for added-value services to help them to sleepat night knowing their capital isprotectedandtheuseofthatcapitalis being optimised. So the protec-tion and optimisation of our cli-ents’ capital is right at the top mylist of priorities. A key ambition isfor our performance to please cli-ents so much they’re very quick toshare that with each other. Wewant them to say: ‘You should dealwith BMS, you can really trustthoseguystodeliverontheirprom-ise to help grow your business.’”n

Beardmoreon...Getting involved inthe industry“The London insurance world isquite small and[as a strategicadviser I was] working with onechief executive in a particularsector who happened to have achief executive friend in theinsurance sector who had aproblem growing theirbusiness. That was quiteliterally how I came to beworking in insurance.”

Strengthening thewholesale division“The wholesale team is nowempowered to act under its ownauthority and autonomy asoften as it needs to. I think it is agreat example of what happenswhen you get really good people,with good strong leadership,and give them the ability to actand not burden them withbureaucracy but just tell them togo out there and play well, butplay hard.”

Extending firms’geographical reach“Our long-term ambition is toserve reinsurance clientsglobally. To begin with, we arefocusing on the areas we knowvery well, but over time we willtake more of a global view. It isessential we do this to achieveour vision of becoming the mostcompelling independent brokerof choice.”

of our performance, wouldincreasingly choose us as theirprovider. And that is exactly whatis happening.”

Although BMS reported a pre-tax loss of £2.1m in 2011 (largely asa result the restructuring chargesand the cost of investing in its newstrategy), there has been anincrease in its underlying profita-bility. “We have started to winnew business with the brokers andproducers we have bought onboard. Then there is the new busi-ness we have won but which didnot have much of an impact on2011 but it is making an impact onour 2012 revenues. Looking at2012, we are predicting with someconfidence revenues will growclose to 25% and our underlyingprofitability will increase signifi-cantly. So 2011 was very much ayear of building, re-engineeringand investing in the business. Butthe fruits of those efforts will showquite radically in 2012.”

Business mixA key question in terms of BMS’sobjective of becoming a companywith a revenue of £100m by 2015 ishow the revenue split is likely tochange. Beardmore anticipates therevenue of the reinsurance divisionislikelytostaywithinthe50%to60%region, despite the level of invest-ment in this side of the business,which includes setting up offices intheUSandstrengtheningtheanalyt-ical and actuarial services on offer.“As the wholesale side of the busi-ness grows, that will become agreater percentage of the revenuethanit isat themoment.Bycontrast,the specialty side is likely to reducein percentage terms but not in per-formance because that will stay thesame.AndthenobviouslyasthePio-neerunderwritingagencydevelops,that will account for a greater per-centageofrevenue.”

It is envisaged the underwritingplatform will be a very strong con-tributor to the business by 2015.Indeed, as much as 10% to 13% ofBMS’s revenue at that time is pre-dicted to come from underwrit-ing. “But for me the strongestcontribution that underwritingplatform will make to the businessat that point is as part of our newbusiness model, which will com-bine our underwriting facilitiesand our traditional broking facili-ties to enable us to offer a uniqueservice to our clients, a servicethat will be extremely beneficialto their businesses.”

BMS, Beardmore says, is a veryUS-centricbusiness.Hesaystheper-centage of business sourced from

5www.insuranceday.com| Tuesday 19 June 2012

‘Restructuring has provided greaterclarity and focus to the business’Oneof thepublicly statedobjectives ofCarlBeardmore’s tenure as chief executive ofBMS isto double the size of its brokerageby2015

Beardmore was appointed chief executive of BMS Associates inJune 2010 and heads both the UK and US operations. His primaryfocus is to lead the successful execution of BMS’s strategy:doubling the size of the broking business by 2015 and developingthe overall business proposition.

Beardmore has been actively involved with BMS for eight years,initially as a strategic adviser and from July 2008 as a non-executive director.

He has a wealth of experience, advising in the insurance marketsas well as running businesses in other industries. He has worked asa strategic adviser to leading players in the London insurancesector since 1997.

Beardmore began his career in the 1970s in the manufacturingindustries and moved on to establish his own strategic consultingbusiness in 1993.

Carl Beardmore CV

Rasaad JamieGlobal markets editor

F ew companies have beenso radically transformedin terms of both businessstrategy and structure as

specialist London market insur-ance group BMS over the past 18months. This process of change,which is still ongoing, is describedby Carl Beardmore, BMS’s chiefexecutive, as a “complete re-engi-neering” of the business which willchange the dynamics of the com-pany even more dramatically overthe next few years.

Although Beardmore, who wasappointed chief executive in June2010, is very much part of thechange, he was no stranger to theboard of BMS, having beeninvolved with the company for theprevious eight years, first as a stra-tegic adviser, then for the past twoyears as a non-executive director.

According to its results state-ment released last week, BMS gen-erated revenues of £53.2m($83.4m) last year through its fourbusiness divisions: reinsurance,wholesale insurance, specialtyinsurance and its Pioneer-branded underwriting platform.But 2010 (when the companypassed the £50m revenue markfor the first time in its 32-year his-tory) was clearly a critical time forBMS. Two years earlier, the board

least double the size of BMS’s bro-kerage to £100m by 2015.

Employee-ownedBMS is a largely employee-ownedbusiness in which a third-partyinvestor (AHJ Holdings) histori-cally held a 25% stake. When BMSwas originally formed in 1980, AHJacted as the umbrella organisationfor the company which, in effect,involved providing a guarantee ofsupport in the early days of BMS’sevolution. In return for that duty,AHJ acquired an ownership stakein BMS. For a whole host of rea-sons, Beardmore explains, theinvestment remained in placeright up to the time when he tookover as chief executive. “I felt oneof the first things we needed to dowas to re-acquire that sharehold-ing and make us 100% employee-owned and independent.”

In 2011, BMS reached agreementtoacquirethesharesownedbyAHJfor£8m.Thetransactionwasstruc-tured in two tranches. “During2011 and the first quarter of 2012,we acquired the first tranche of theAHJ holding and this share buy-back resulted in a reduction in netassets of £4.2m at the year end. Weintend to acquire the balance of theAHJ shares during 2013.”

Beardmore, whose originalbackground is financial account-ing, had previously worked in anumberofindustrialsectorsacrossa range of managerial roles includ-ing financial, operational, com-mercial, sales and marketing.Mainly working for multinationalcompanies, the experience pro-videdhimwithagroundinginmostof the key disciplines necessary forthe successful running of anyorganisation. In 1997, after aperiod of running his own busi-ness, he began working as a strate-gic adviser to a number ofcompanies in the London insur-ance market.

“The type of consulting we didwas to help with the strategic re-engineering of businesses, so I wasalways dealing in the boardroom.

of directors had agreed and begunto implement a more dynamic,aggressive business strategy.While BMS was recognised as ahighly reputable and credibleorganisation, it was also per-ceived as a little too pedestrian inits way of doing business. Cer-tainly, by 2010, the company didnot generate a great deal of excite-ment in the market.

Beardmore, then still acting as astrategic adviser, was asked tobecome a non-executive directoron the board of BMS. He says hetook on the position with the fullintention of fulfilling the tradi-tional non-executive role of con-structively challenging theexecution of the strategy. “Butwhat happened during that periodwas it became quite clear the newstrategy required a different formof leadership. At the beginning of2010, the board acknowledgedthings needed to be changed and,as a result of a combination of fac-tors – the board’s familiarity withme, my understanding of the strat-egy of the business, my previousroles as business leader either inother companies or for myself –led them to conclude there wassomebody already within thebusiness who could fulfil the roleof chief executive, whose familiar-ity with it would minimise anyinterruption in momentum,”Beardmore says.

Akey,publiclystatedobjectiveofthe new strategy and Beardmore’stenure as chief executive is to at

The London insurance world isquite small and we were workingwithonechiefexecutive inapartic-ularsectorwhohappenedtohaveachief executive friend in the insur-ance sector who had a problemgrowing their business. That wasquite literally how I came to beworking in insurance.

“But once I was working in thesector, it became really interestingbecause here was an industry thatseemed to have been doing thesame things the same way for an

awfully long time. And there wasthe rise of companies like Aon andGuyCarpenter,whichgrewrapidlythrough acquisition, and, as aresultof that, thepositionof thetra-ditional London correspondentbroker position was being threat-ened because these large brokerswere winning the business directlyfrom clients and then increasinglypushing it through their ownhouses into the London market. Itwas a situation that was creating alot of new dynamics in the market-

Rei

nsu

ran

ce

Sp

ecia

list

insu

ran

ce

Wh

ole

sale

insu

ran

ce

JHIn

tern

edia

ries

/JH

Insu

ran

ceS

erv

ices

/P

ion

eer

Un

der

wri

tin

g

Chart: The four pillars of BMS’s business

place, which companies were hav-ing to respond to. Many companieswere struggling to grow andexpand. Profitability was gettingharder to achieve. I thought itseemed like an ideal sector todeploy our talents of inspiringbusiness success.”

Decision-makingThe immediate challenge for BMS,which was founded in 1980, was toimprove the company’s perform-ance and manage costs at the busi-ness unit level. In 2010, thisinvolvedoneofthecompany’smostexperienced brokers, Hugo Craw-ley, moving from his position aschairman of the holding companyto chairman of the broking busi-ness. Indeed, a number of provenpractitioners moved from the mainboard on to the broking board andthefocusbecamefarmoreorientedtowardsimprovingperformanceatthebusinessunit level.

“We changed the way in whichdecisions were taken. Too many ofthe decisions were being made atthetopoftheorganisation.Tome, ifyou don’t delegate the decision-making to the appropriate levelswithin the business it slows thebusiness down, which inevitablymanifests itself in the form of slowcustomer service.

“One thing I know as a customermyself of many products and fromhaving spoken to customerswithin a number of different con-texts is they want fast and effec-tive responses, they want a timelyresponse, so you have to engineeryour business in a way wheredecisions can be made quickly sothe client feels the benefit of that.In our market, which is domi-nated by some very large players,being fast, nimble and flexible isan important differentiator.Without being disrespectful tosome of the bigger companies, alarge organisation tends to beslower to react and making deci-sions. So if we are more nimble,we can service clients more effi-ciently than the competition.”

Four pillarsThe key focus of the restructuring,which has absorbed £15m of invest-ment over the past 18 months, wasto divide the business into four pil-lars: reinsurance, which in 2010accounted for 57% of BMS’s overallrevenue; specialist insurance(26%); wholesale insurance (17%);andthefourthpillar,whichisrepre-sented by BMS’s two underwritingplatforms JH Intermediaries (JHI)in the UK and JH Insurance Services(JHIS) in the US and by the launch of

a managing general agency, Pio-neer Underwriting, in April 2011.The restructuring, Beardmore says,immediately provided a greaterclarity and focus to the business. Atpresent, the investment is focusedon the reinsurance platform in theUS, on the wholesale business andon establishing BMS’s underwrit-ingplatforms.

JHI and JHIS, he explains, werepart of the traditional Jensen &HastingsbusinessthatbecamepartofBMSafewyearspreviously.Bothbusinesses were heavily focusedon the construction sectors in theUK and in the US. “As we are allaware, from 2008 onwards whenthe world went pear-shaped, theconstruction sector was affecteddramatically. As a first action, wehad to re-engineer completelythose businesses which, throughno fault of their own, found the car-pet pulled from under their feet.What we have been doing is tryingto retain the profitable parts of thebusiness as well as those parts ofthe business we think have gotpotential in the long term. But to beabsolutely candid, these busi-nesses are now much reduced insize and they now form part of ourPioneer-branded underwritingplatform. They are still using theJHI and JHIS names but under theumbrella of Pioneer.”

Freeing up wholesaleThere was a notable investment inthe wholesale insurance divisionin2010,whenateamofbrokers, ledby Nick Cook, moved from Willis toBMS, where they merged with thecompany’s existing wholesaleteam. The result, Beardmore says,was the creation of a strong, highlyproductive unit that in the first 12months hit all its objectives interms of business generation. Thewholesale division, which focuseson traditional facultative lines ofbusiness, has also made a verystrong start to 2012.

“The wholesale team is nowempowered to act under its ownauthority and autonomy as oftenas it needs to. I think it is a greatexample of what happens whenyou get really good people, withgood strong leadership, and givethem the ability to act and not bur-den them with bureaucracy butjust tell them to go out there andplay well, but play hard. We felt ifwe allowed them the freedom andthe autonomy to express them-selves and optimise their skills-sets, this would manifest itself inbetter solutions, better serviceand better relationships for ourclients who, we hoped, as a result

theUSisgreaterthanthe57%identi-fied geographically; the exact figureis more like 80%. A significant vol-ume of US business is brought intothe London market by BMS in itsrole as a correspondent broker andconsequently the geographic ori-ginsofthebusinessisobscured.

“At the moment, we are veryfocusedontheUSandIthinkforthenext two or three years we will con-tinue to be that way, but as thewholesale side of the business –which focuses on areas like SouthAfrica, the Middle East, Asia andAustralasia – grows, that willchange. Our long-term ambition isto serve reinsurance clients glo-bally. To begin with, we are focus-ing on the areas we know very well,but over time we will take more of aglobal view. It is essential we dothis to achieve our vision of becom-ing the most compelling independ-ent broker of choice.”

Trusted adviserAccording to Beardmore, anotherkey objective is for BMS to be a trulytrusted adviser to clients. “It is aphrase that has been overused but Ibelieve we can live up to it betterthan anybody else. Virtually all ourclients, whatever the nature of theirbusiness, have a large amount ofcapitaltheyareputtingatrisktocre-ate and develop a sustainable busi-ness and they need truly trustedadvisers that will ensure their capi-talisprotectedtoitsoptimallevel,soonly the amount of capital they arewantingtoputatriskisexposed.”

According to Beardmore, BMS’sclients also need help in analysingboth the existing and future state oftheir businesses to ensure they aregetting the best return on their cap-ital. “That is what is being expectedof insurance brokers now. Typi-cally, when I sit down with clientsthey don’t want me to tell them weare great brokers or we can puttogether a very good insuranceprogrammeforthem.Asfaras theyare concerned, every other brokercan do that and we shouldn’t be sit-ting in front of them if we can’t.

“They are looking for added-value services to help them to sleepat night knowing their capital isprotectedandtheuseofthatcapitalis being optimised. So the protec-tion and optimisation of our cli-ents’ capital is right at the top mylist of priorities. A key ambition isfor our performance to please cli-ents so much they’re very quick toshare that with each other. Wewant them to say: ‘You should dealwith BMS, you can really trustthoseguystodeliverontheirprom-ise to help grow your business.’”n

Beardmoreon...Getting involved inthe industry“The London insurance world isquite small and[as a strategicadviser I was] working with onechief executive in a particularsector who happened to have achief executive friend in theinsurance sector who had aproblem growing theirbusiness. That was quiteliterally how I came to beworking in insurance.”

Strengthening thewholesale division“The wholesale team is nowempowered to act under its ownauthority and autonomy asoften as it needs to. I think it is agreat example of what happenswhen you get really good people,with good strong leadership,and give them the ability to actand not burden them withbureaucracy but just tell them togo out there and play well, butplay hard.”

Extending firms’geographical reach“Our long-term ambition is toserve reinsurance clientsglobally. To begin with, we arefocusing on the areas we knowvery well, but over time we willtake more of a global view. It isessential we do this to achieveour vision of becoming the mostcompelling independent brokerof choice.”

of our performance, wouldincreasingly choose us as theirprovider. And that is exactly whatis happening.”

Although BMS reported a pre-tax loss of £2.1m in 2011 (largely asa result the restructuring chargesand the cost of investing in its newstrategy), there has been anincrease in its underlying profita-bility. “We have started to winnew business with the brokers andproducers we have bought onboard. Then there is the new busi-ness we have won but which didnot have much of an impact on2011 but it is making an impact onour 2012 revenues. Looking at2012, we are predicting with someconfidence revenues will growclose to 25% and our underlyingprofitability will increase signifi-cantly. So 2011 was very much ayear of building, re-engineeringand investing in the business. Butthe fruits of those efforts will showquite radically in 2012.”

Business mixA key question in terms of BMS’sobjective of becoming a companywith a revenue of £100m by 2015 ishow the revenue split is likely tochange. Beardmore anticipates therevenue of the reinsurance divisionislikelytostaywithinthe50%to60%region, despite the level of invest-ment in this side of the business,which includes setting up offices intheUSandstrengtheningtheanalyt-ical and actuarial services on offer.“As the wholesale side of the busi-ness grows, that will become agreater percentage of the revenuethanit isat themoment.Bycontrast,the specialty side is likely to reducein percentage terms but not in per-formance because that will stay thesame.AndthenobviouslyasthePio-neerunderwritingagencydevelops,that will account for a greater per-centageofrevenue.”

It is envisaged the underwritingplatform will be a very strong con-tributor to the business by 2015.Indeed, as much as 10% to 13% ofBMS’s revenue at that time is pre-dicted to come from underwrit-ing. “But for me the strongestcontribution that underwritingplatform will make to the businessat that point is as part of our newbusiness model, which will com-bine our underwriting facilitiesand our traditional broking facili-ties to enable us to offer a uniqueservice to our clients, a servicethat will be extremely beneficialto their businesses.”

BMS, Beardmore says, is a veryUS-centricbusiness.Hesaystheper-centage of business sourced from

6 www.insuranceday.com| Tuesday 19 June 2012

WORLD LOSS INTELLIGENCE/PROPERTY

TOMORROWINWORLDLOSSINTELLIGENCE:POLITICAL&TRADE

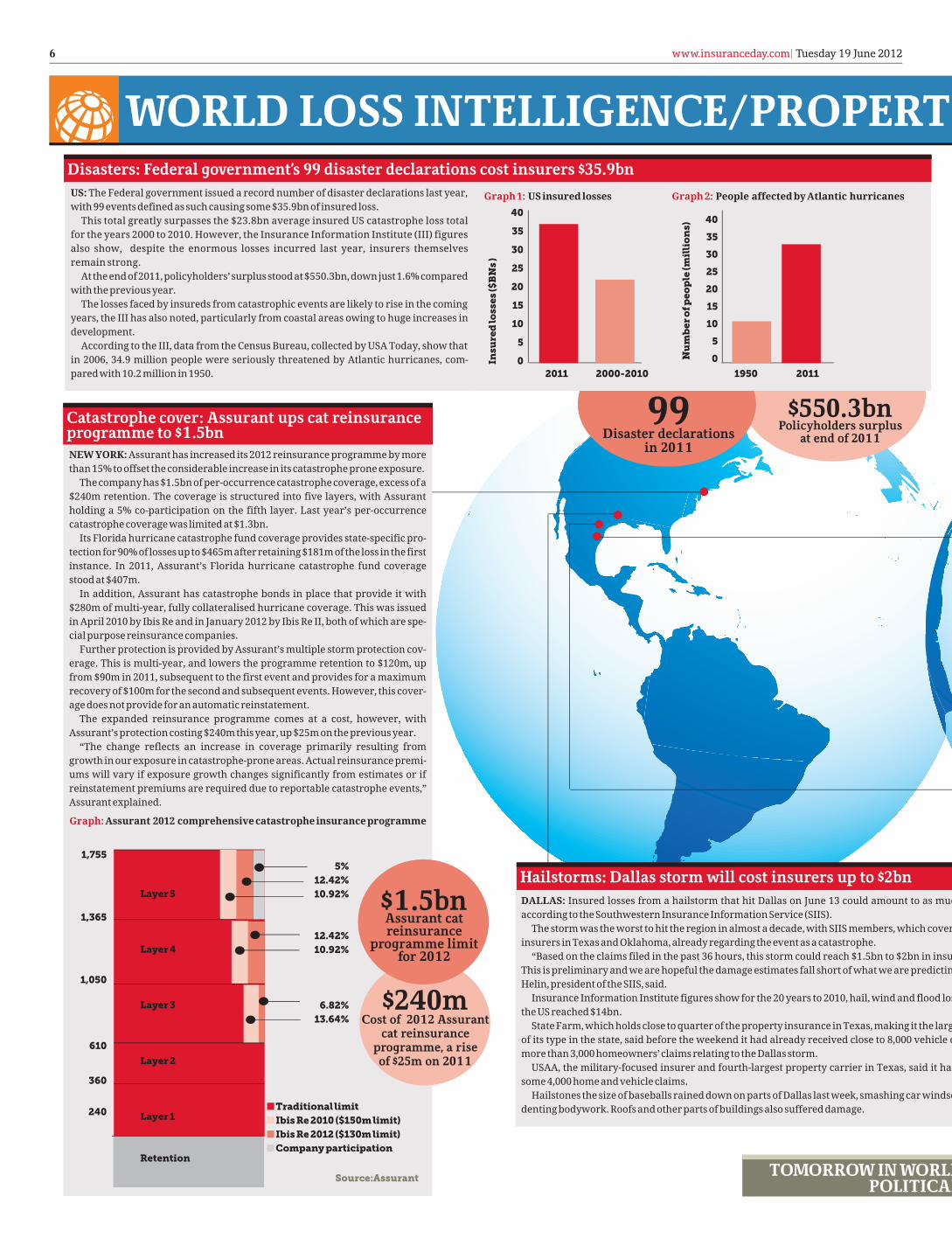

Hailstorms: Dallas stormwill cost insurers up to $2bnDALLAS: Insured losses from a hailstorm that hit Dallas on June 13 could amount to as much as $2bnaccording to the Southwestern Insurance Information Service (SIIS).

The storm was the worst to hit the region in almost a decade, with SIIS members, which covers propertyinsurers in Texas and Oklahoma, already regarding the event as a catastrophe.

“Based on the claims filed in the past 36 hours, this storm could reach $1.5bn to $2bn in insured losses.This is preliminary and we are hopeful the damage estimates fall short of what we are predicting,” SandraHelin, president of the SIIS, said.

Insurance Information Institute figures show for the 20 years to 2010, hail, wind and flood losses acrossthe US reached $14bn.

State Farm, which holds close to quarter of the property insurance in Texas, making it the largest carrierof its type in the state, said before the weekend it had already received close to 8,000 vehicle claims andmore than 3,000 homeowners’ claims relating to the Dallas storm.

USAA, the military-focused insurer and fourth-largest property carrier in Texas, said it had receivedsome 4,000 home and vehicle claims.

Hailstones the size of baseballs rained down on parts of Dallas last week, smashing car windscreens anddenting bodywork. Roofs and other parts of buildings also suffered damage.

NEW YORK: Assurant has increased its 2012 reinsurance programme by morethan 15% to offset the considerable increase in its catastrophe prone exposure.

Thecompanyhas$1.5bnofper-occurrencecatastrophecoverage,excessofa$240m retention. The coverage is structured into five layers, with Assurantholding a 5% co-participation on the fifth layer. Last year’s per-occurrencecatastrophe coverage was limited at $1.3bn.

Its Florida hurricane catastrophe fund coverage provides state-specific pro-tectionfor90%oflossesupto$465mafterretaining$181moftheloss inthefirstinstance. In 2011, Assurant’s Florida hurricane catastrophe fund coveragestood at $407m.

In addition, Assurant has catastrophe bonds in place that provide it with$280m of multi-year, fully collateralised hurricane coverage. This was issuedin April 2010 by Ibis Re and in January 2012 by Ibis Re II, both of which are spe-cial purpose reinsurance companies.

Further protection is provided by Assurant’s multiple storm protection cov-erage. This is multi-year, and lowers the programme retention to $120m, upfrom $90m in 2011, subsequent to the first event and provides for a maximumrecovery of $100m for the second and subsequent events. However, this cover-age does not provide for an automatic reinstatement.

The expanded reinsurance programme comes at a cost, however, withAssurant’s protection costing $240m this year, up $25m on the previous year.

“The change reflects an increase in coverage primarily resulting fromgrowth in our exposure in catastrophe-prone areas. Actual reinsurance premi-ums will vary if exposure growth changes significantly from estimates or ifreinstatement premiums are required due to reportable catastrophe events,”Assurant explained.

Catastrophe cover: Assurant ups cat reinsuranceprogramme to $1.5bn

Disasters: Federal government’s 99 disaster declarations cost insurers $35.9bnUS: The Federal government issued a record number of disaster declarations last year,with 99 events defined as such causing some $35.9bn of insured loss.

This total greatly surpasses the $23.8bn average insured US catastrophe loss totalfor the years 2000 to 2010. However, the Insurance Information Institute (III) figuresalso show, despite the enormous losses incurred last year, insurers themselvesremain strong.

Attheendof2011,policyholders’surplusstoodat$550.3bn,downjust1.6%comparedwith the previous year.

The losses faced by insureds from catastrophic events are likely to rise in the comingyears, the III has also noted, particularly from coastal areas owing to huge increases indevelopment.

According to the III, data from the Census Bureau, collected by USA Today, show thatin 2006, 34.9 million people were seriously threatened by Atlantic hurricanes, com-pared with 10.2 million in 1950.

40

35

30

25

20

15

10

5

0Insu

red

loss

es($

BN

s)

2011 2000-2010

40

35

30

25

20

15

10

5

0Nu

mb

ero

fpeo

ple

(mil

lio

ns)

1950 2011

Graph 1: US insured losses Graph 2: People affected by Atlantic hurricanes

Graph:Assurant 2012 comprehensivecatastropheinsuranceprogramme

1,755

1,365

1,050

610

360

240

Layer 5

Layer 4

Layer 3

Layer 2

Layer 1

Retention

nTraditional limitnIbis Re 2010 ($150m limit)nIbis Re 2012 ($130m limit)nCompany participation

5%12.42%10.92%

12.42%10.92%

6.82%13.64%

Source:Assurant

$240mCost of 2012 Assurant

cat reinsuranceprogramme, a riseof $25m on 2011

$1.5bnAssurant catreinsurance

programme limitfor 2012

99Disaster declarations

in 2011

$550.3bnPolicyholders surplus

at end of 2011

7www.insuranceday.com| Tuesday 19 June 2012

WORLD LOSS INTELLIGENCE/PROPERTY

TOMORROWINWORLDLOSSINTELLIGENCE:POLITICAL&TRADE

Hailstorms: Dallas stormwill cost insurers up to $2bnDALLAS: Insured losses from a hailstorm that hit Dallas on June 13 could amount to as much as $2bnaccording to the Southwestern Insurance Information Service (SIIS).

The storm was the worst to hit the region in almost a decade, with SIIS members, which covers propertyinsurers in Texas and Oklahoma, already regarding the event as a catastrophe.

“Based on the claims filed in the past 36 hours, this storm could reach $1.5bn to $2bn in insured losses.This is preliminary and we are hopeful the damage estimates fall short of what we are predicting,” SandraHelin, president of the SIIS, said.

Insurance Information Institute figures show for the 20 years to 2010, hail, wind and flood losses acrossthe US reached $14bn.

State Farm, which holds close to quarter of the property insurance in Texas, making it the largest carrierof its type in the state, said before the weekend it had already received close to 8,000 vehicle claims andmore than 3,000 homeowners’ claims relating to the Dallas storm.

USAA, the military-focused insurer and fourth-largest property carrier in Texas, said it had receivedsome 4,000 home and vehicle claims.

Hailstones the size of baseballs rained down on parts of Dallas last week, smashing car windscreens anddenting bodywork. Roofs and other parts of buildings also suffered damage.

Wildfires: Nine states suffer from fires with costs continuing to riseCOLORADO, NEW MEXICO: Nine separate states continue to sufferfrom the effect of wildfires although the neighbouring states of Colo-rado and New Mexico have been faring the worst.

InColorado, themostnotableblazewas theHighParkfire,whichwasignited by a lightning strike last week to the west of Fort Collins, AonBenfield said.

The fire has been burning in an area where 70% of trees had beenkilled by mountain pine beetles, with the blaze having charred at least49,760 acres. More than 100 homes and other buildings have been dam-aged or destroyed in Rist Canyon, Paradise Park, Stove Prairie, PoudreCanyon, Old Flowers, Stratton Park, Kings Canyon and Cloudy Pass.

Hundreds of residents have been forced to evacuate their homes. Sofar, one person has been killed after her cabin was engulfed in flamesand the total cost of fighting the fire has reached $3m.

New Mexico has suffered several recent fires, the most damaging ofwhich was the Little Bear Fire. This blaze erupted on June 4 afterlightning struck dry vegetation. Close to 40,000 acres have alreadyburned downand 224 residential structures and 10 outbuildings havebeen destroyed.

In addition, the Whitewater Baldy Complex Fire has now been burn-ing for more than a month, with the blaze now thought to be 75% con-tained. More than 290,127 acres of land have been scorched, with thecause of this fire also thought to be lightning. Total costs to fight this firehave reached $22.6m.

FRANCE: Switzerland-based loss modeller Perils has once again reduced its industry loss estimate fromwindstorm Joachim, this time by an additional €4m ($5.1m).

Joachim struck western and northern Europe from December 15 and 17, 2011, and in January Perilsestimatedtheinsuredlossat€300m.Thatestimatewaslaterreducedto€289mandhasnowbeencutfur-ther to €285m. Perils will issue a fourth loss estimate on December 15.

The loss figures do not include the impact on France’s CatNat government scheme.The windstorm caused power cuts in more than 300,000 homes in France, with strong winds causing

significantdamage.Somecoastalareasalsosufferedflooding,withtheareasofGironde,Charente-Mari-time, Vendee, Loire-Atlantique, Morbihan and Finistère particularly affected.

The French Federation of Insurance Companies has estimated the storm could generate 80,000 to120,000 claims at a total cost ranging from €180m to €250m.

As well as France, Joachim also caused insured losses in Germany and Switzerland.

European windstorm cluster: Perils revises Joachim estimate downwards

Hurricane Carlotta: AIR anticipatesminimal insured losses

MEXICO: Insured losses from hurricane Carlotta are not expected to be particularly significantwith the storm quickly dissipating over the country’s more mountainous terrain.

Carlotta, the third named storm of the Pacific hurricane season, made landfall on Fridayevening as a category-one storm near the Oaxacan town of Puerto Escondido, some 200 milessouth-east of Acapulco.

Although maximum sustained winds reached 90 mph at landfall, AIR Worldwide “does notexpect significant insured losses from Carlotta”, the catastrophe-modelling company said.

“Carlotta was a relatively small hurricane at landfall, with hurricane-force winds extendinglessthan30milesfromtheeye,”DrTimDoggett,principalscientistatAIR,said.“Asaresult,dam-aging winds affected only a small portion of the coast.”

Local reports said trees and billboards were blown down and windows that had not beenboarded up were shattered by flying debris. AIR also said the metal roofs of some commercialbuildings peeled off, with informally built homes suffering more serious structural damage. Upto 50% of residential structures are thought to be constructed without a building permit andthese are unlikely to be insured.

Thestormpassedtothenorthofthe330,000barrels-per-dayoilrefineryfacilityatSalinaCruz,the largest installation of its type in Mexico; the refinery remained open. At the same time, nodamage has been reported in the popular resort city of Acapulco.

$1.5bnto $2bnEstimated cost

of storm

3,000Homeowners’claims receivedby State Farm

USWildfires innumbers

49,760 acresCharred by the fires at High Park

100Homes and other buildings damaged ordestroyed by by the High Park Fires

290,127 acresScorched by the

Whitewater Baldy Complex Fire

40,000 acresburnt at the Little Bear Fire

€285mRevised estimatedinsured loss from

windstormJoachim

8

RIO+20PREVIEWwww.insuranceday.com| Tuesday 19 June 2012

New sustainability principlesto strengthen riskmanagement of insurers

O n the eve of the Rio+20conference, the Princi-ples for SustainableInsurance (PSI) will be

presented and signed in Brazil byclose to 30 insurance companiestoday. The signatories will enterinto a commitment to systemati-cally and increasingly apply sus-tainability criteria in theirday-to-day business. This sounds alot easier than it is. But all sidesstand to benefit from the new prin-ciples: society, because of its impli-cations in terms of responsiblecorporate decision-making, andthe signatory insurers, whose riskmanagement will thus be furtherstrengthened.

In subscribing to the PSI of theUnited Nations EnvironmentalProgramme Finance Initiative(UNEP FI), the signatories are tak-ing the commitment to sustaina-bility inherent in the very conceptof insurance a stage further. Insur-ance is essentially a promise givento the customer regarding thefuture. First, insurance companiesare a stabilising factor – becausethe risks are shared among many,the extreme financial impact onthe individual is reduced. Second,insurance mitigates lossesbecause the risks are quantifiedvia the rating process, which effec-tively puts a price tag on them. Inother words, reducing the risklowers the premium. Last but notleast, by underwriting risks, insur-ers facilitate progress and innova-tive insurance concepts helppromote the development and dif-fusion of new technologies.

This can be seen from the wayengineering insurance evolved.When the industrial revolutiongot under way in the 19th century,fire insurance alone was no longersufficient to cover the productionfacilities. The machines were gen-erally steam-driven andextremely costly. Steps had to betaken to prevent breakdown andexplosion to protect the workforceand minimise financial loss. Engi-

neers began carrying out routineinspections of the machines andinstructing the workforce on howto operate them. Armed with theexperience gained by the engi-neers, the insured and the insur-ers got together to develop newcovers. Ultimately, it became pos-sible to cover material damageand business interruption as indi-vidual risks. All this helpedfacilitate the necessary capital-in-tensive investment in modernmachinery, and thus the indus-trial revolution itself.

The latest example showing howinsurers promote sustainability isrenewable energy. They supportthis technological transformationby providing the experience andexpertise required to develop newinsurance concepts. By way of anexample, the geothermal energysector benefits from explorationrisk insurance, which covers theextremely high costs involved ifexploratory drilling is unsuccess-ful. Similarly, insurance againstreduced photovoltaic output facili-tates the funding and planning ofmajor projects.

Insurers seek solutions to press-ing global issues because theyaffect their core business. Climateand demographic change andoverstretched healthcare systemsare among the many issues ana-lysed by insurers as emergingrisks, relevant to their business.Thus, the industry performs anearly-warning function for societyas a whole. Munich Re, forinstance, began drawing attentionto the threat of climate change asearly as the 1970s. And we con-tinue to be actively involved in thedebate on this issue.

Where major social issues areconcerned, insurers research thecauses of loss and apply theirfindings to loss prevention andproduct development. The list ofnew, sustainability-based prod-ucts and initiatives is a long oneand the approaches vary. Insur-ers can apply premium discountsto encourage drivers to opt forlow-carbon vehicles. Unit-linkedpension funds can be tailored toclients’ ethical, social and ecologi-cal concerns. Special crop insur-ance systems help farmers

protect themselves againstdrought and other effects of cli-mate change, while public-private partnerships are a keyfactor in the close collaborationnecessary between farmers, stateand insurers. What these productdevelopments have in common isthey can be seen as small stepsforward in solving the challengesfaced by society. Munich Re has“gone the extra mile” by collabo-rating with the Desertec Founda-tion to launch an industrialinitiative designed to realise theDesertec vision. Now comprisingsome 55 companies and partners,Dii GmbH is promoting the visionof a sustainable energy supplyfrom the deserts of the MiddleEast and north Africa region.

All these examples show sustain-ability is very much of concern toinsurers, and indeed, fundamentalto their business model. Awarenessoftheissuesinvolvedwillbefurtherboosted by the adoption of the PSI.The world in which we live is com-plex, interconnected, global andfast moving. To ensure we can con-tinue to operate within a secureenvironment, we have to have areliable framework. That is pre-cisely what the PSI will be withregard to the ecological, social andgovernance (ESG) issues faced byinsurers. The principles are not a

checklist but a first step in gettingthe process moving in the rightdirection.Eachindividualcompanywillhavetodraftbindingguidelinesimplementing the PSI along thevalue chain. Consequently, riskanalysis will be extended to com-prise all types of risk, includingsome never previously consideredthat could nevertheless involvelong-termlossanddamage.

This will bring challenges andopportunities. In some cases, itmay mean risks can only be under-written subject to strict limits. Inany event, greater awareness ofsustainability issues will have theeffect of mitigating expected lossesandcouldalsoincreasedemandforinnovative insurance solutions. Atthe same time, we will have to exer-cise caution in applying the princi-ples, and take due account of thelegitimate needs of investors, cli-ents, employees and the public.

By acting responsibly, the insur-ance sector, with its global pre-mium volume of more than $4trnand $24trn in investments, can be ahighly effective role model. TheUNEP FI’s Principles for Responsi-ble Investment (PRI) published in2006, demonstrated just how suc-cessful a voluntary, transparency-based initiative can be. Theyaddress the issue of how sustain-ability concerns can be included ininvestmentdecisions.ThePRIhavenow been accepted and applied bymore than 1,000 companies andinstitutions investing a total ofsome $30trn. Munich Re was alsoamong the founding signatories.

In signing the UNEP FI’s PSI prin-ciples, insurers will agree to takeaccount of ESG considerationsalong the entire value chain. Thismeans systematically incorporat-ing ecological, social and corporategovernance issues into our activi-ties with all stakeholders (clients,business partners, employees,investors, analysts and supervi-sory authorities). In keeping withtheseprinciples,companieswillsetthemselves individual objectivesand formulate specific actionplans. They will have to report reg-ularlyontheirprogress inapplyingthe principles. In short, insurersare about to embark on a process ofongoing improvement.n

Astrid ZwickMunich Re 55

Companies that havejoined the Dii, a privateindustry consortium

working towards enablingthe Desertec vision

1,000+Companies that haveapplied the UNEP FI’s

Principles for ResponsibleInvestment, published

in 2006

Sustainability is very much of concernto insurers, and indeed, fundamental totheir business model. Awareness of theissues involved will be further boostedby the adoption of the PSI.

9www.insuranceday.com| Tuesday 19 June 20128

COMPANIESHOUSEwww.insuranceday.com| Tuesday 11 October 2011

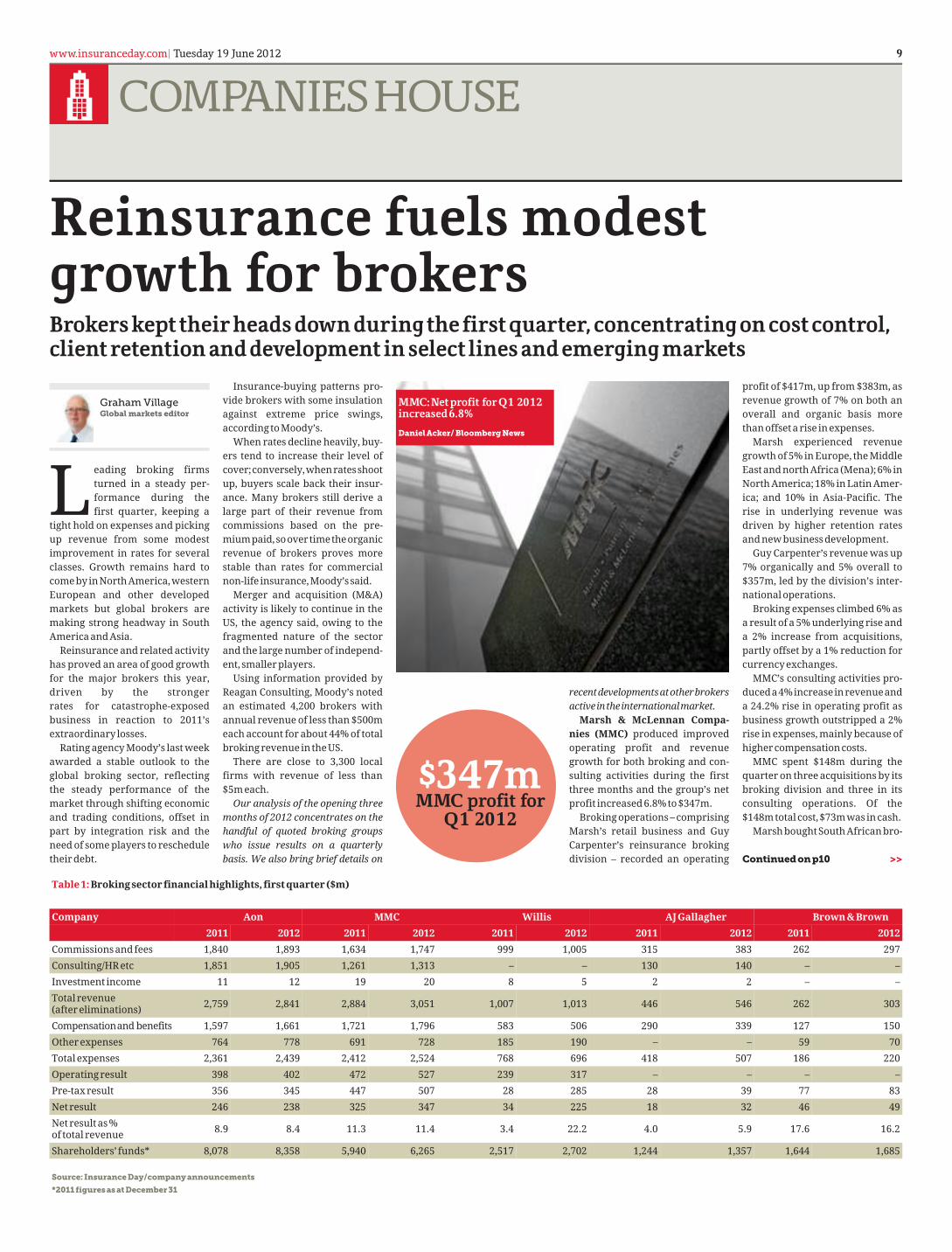

Reinsurance fuels modestgrowth for brokers

L eading broking firmsturned in a steady per-formance during thefirst quarter, keeping a

tight hold on expenses and pickingup revenue from some modestimprovement in rates for severalclasses. Growth remains hard tocomebyinNorthAmerica,westernEuropean and other developedmarkets but global brokers aremaking strong headway in SouthAmerica and Asia.

Reinsurance and related activityhas proved an area of good growthfor the major brokers this year,driven by the strongerrates for catastrophe-exposedbusiness in reaction to 2011’sextraordinary losses.

Rating agency Moody’s last weekawarded a stable outlook to theglobal broking sector, reflectingthe steady performance of themarket through shifting economicand trading conditions, offset inpart by integration risk and theneed of some players to rescheduletheir debt.

Insurance-buying patterns pro-vide brokers with some insulationagainst extreme price swings,according to Moody’s.

When rates decline heavily, buy-ers tend to increase their level ofcover;conversely,whenratesshootup, buyers scale back their insur-ance. Many brokers still derive alarge part of their revenue fromcommissions based on the pre-miumpaid,soovertimetheorganicrevenue of brokers proves morestable than rates for commercialnon-life insurance,Moody’ssaid.

Merger and acquisition (M&A)activity is likely to continue in theUS, the agency said, owing to thefragmented nature of the sectorand the large number of independ-ent, smaller players.

Using information provided byReagan Consulting, Moody’s notedan estimated 4,200 brokers withannual revenue of less than $500meach account for about 44% of totalbroking revenue in the US.

There are close to 3,300 localfirms with revenue of less than$5m each.

Our analysis of the opening threemonths of 2012 concentrates on thehandful of quoted broking groupswho issue results on a quarterlybasis. We also bring brief details on

recentdevelopmentsatotherbrokersactiveintheinternationalmarket.

Marsh & McLennan Compa-nies (MMC) produced improvedoperating profit and revenuegrowth for both broking and con-sulting activities during the firstthree months and the group’s netprofit increased 6.8% to $347m.

Broking operations – comprisingMarsh’s retail business and GuyCarpenter’s reinsurance brokingdivision – recorded an operating

profit of $417m, up from $383m, asrevenue growth of 7% on both anoverall and organic basis morethan offset a rise in expenses.

Marsh experienced revenuegrowth of 5% in Europe, the MiddleEast and north Africa (Mena); 6% inNorth America; 18% in Latin Amer-ica; and 10% in Asia-Pacific. Therise in underlying revenue wasdriven by higher retention ratesand new business development.

Guy Carpenter’s revenue was up7% organically and 5% overall to$357m, led by the division’s inter-national operations.

Broking expenses climbed 6% asa result of a 5% underlying rise anda 2% increase from acquisitions,partly offset by a 1% reduction forcurrency exchanges.

MMC’s consulting activities pro-duceda4%increaseinrevenueanda 24.2% rise in operating profit asbusiness growth outstripped a 2%rise in expenses, mainly because ofhighercompensationcosts.

MMC spent $148m during thequarter on three acquisitions by itsbroking division and three in itsconsulting operations. Of the$148m total cost, $73m was in cash.

MarshboughtSouthAfricanbro-

Brokerskepttheirheadsdownduringthefirstquarter,concentratingoncostcontrol,clientretentionanddevelopmentinselect linesandemergingmarkets

GrahamVillageGlobal markets editor

Table 1: Broking sector financial highlights, first quarter ($m)

Company Aon MMC Willis AJ Gallagher Brown & Brown2011 2012 2011 2012 2011 2012 2011 2012 2011 2012

Commissions and fees 1,840 1,893 1,634 1,747 999 1,005 315 383 262 297Consulting/HR etc 1,851 1,905 1,261 1,313 – – 130 140 – –Investment income 11 12 19 20 8 5 2 2 – –Total revenue(after eliminations) 2,759 2,841 2,884 3,051 1,007 1,013 446 546 262 303

Compensationand benefits 1,597 1,661 1,721 1,796 583 506 290 339 127 150Other expenses 764 778 691 728 185 190 – – 59 70Total expenses 2,361 2,439 2,412 2,524 768 696 418 507 186 220Operating result 398 402 472 527 239 317 – – – –Pre-tax result 356 345 447 507 28 285 28 39 77 83Net result 246 238 325 347 34 225 18 32 46 49Net result as %of total revenue 8.9 8.4 11.3 11.4 3.4 22.2 4.0 5.9 17.6 16.2

Shareholders’ funds* 8,078 8,358 5,940 6,265 2,517 2,702 1,244 1,357 1,644 1,685

Source: Insurance Day/company announcements

*2011 figures as at December 31

Continued on p10 >>

MMC:Netprofit forQ1 2012increased6.8%

Daniel Acker/ Bloomberg News

$347mMMC profit for

Q1 2012

10

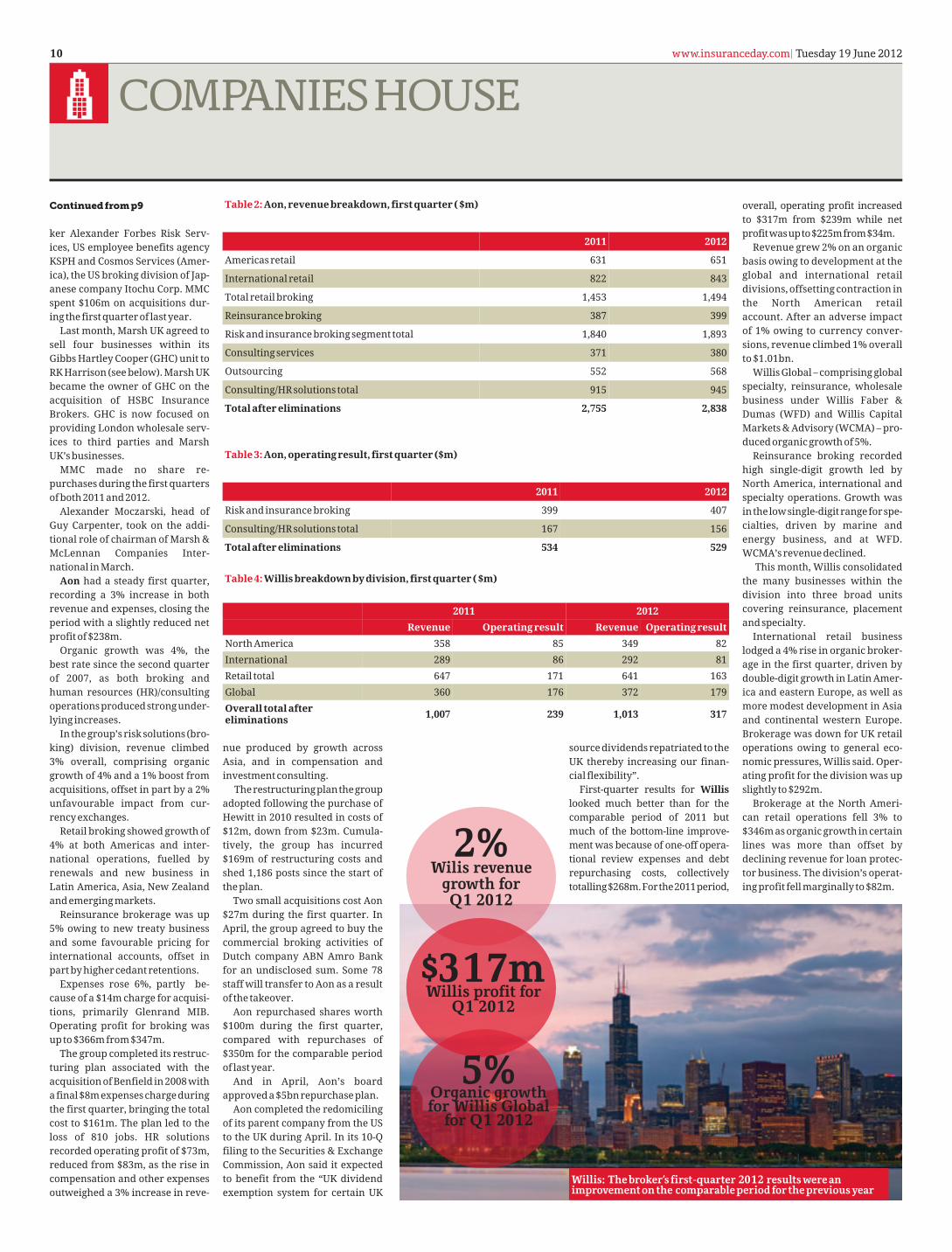

COMPANIESHOUSEwww.insuranceday.com| Tuesday 19 June 2012

nue produced by growth acrossAsia, and in compensation andinvestment consulting.

Therestructuringplanthegroupadopted following the purchase ofHewitt in 2010 resulted in costs of$12m, down from $23m. Cumula-tively, the group has incurred$169m of restructuring costs andshed 1,186 posts since the start ofthe plan.

Two small acquisitions cost Aon$27m during the first quarter. InApril, the group agreed to buy thecommercial broking activities ofDutch company ABN Amro Bankfor an undisclosed sum. Some 78staff will transfer to Aon as a resultof the takeover.

Aon repurchased shares worth$100m during the first quarter,compared with repurchases of$350m for the comparable periodof last year.

And in April, Aon’s boardapproved a $5bn repurchase plan.

Aon completed the redomicilingof its parent company from the USto the UK during April. In its 10-Qfiling to the Securities & ExchangeCommission, Aon said it expectedto benefit from the “UK dividendexemption system for certain UK

ker Alexander Forbes Risk Serv-ices, US employee benefits agencyKSPH and Cosmos Services (Amer-ica), the US broking division of Jap-anese company Itochu Corp. MMCspent $106m on acquisitions dur-ing the first quarter of last year.

Last month, Marsh UK agreed tosell four businesses within itsGibbs Hartley Cooper (GHC) unit toRK Harrison (see below). Marsh UKbecame the owner of GHC on theacquisition of HSBC InsuranceBrokers. GHC is now focused onproviding London wholesale serv-ices to third parties and MarshUK’s businesses.

MMC made no share re-purchases during the first quartersof both 2011 and 2012.

Alexander Moczarski, head ofGuy Carpenter, took on the addi-tional role of chairman of Marsh &McLennan Companies Inter-national in March.

Aon had a steady first quarter,recording a 3% increase in bothrevenue and expenses, closing theperiod with a slightly reduced netprofit of $238m.

Organic growth was 4%, thebest rate since the second quarterof 2007, as both broking andhuman resources (HR)/consultingoperationsproducedstrongunder-lying increases.

In the group’s risk solutions (bro-king) division, revenue climbed3% overall, comprising organicgrowth of 4% and a 1% boost fromacquisitions, offset in part by a 2%unfavourable impact from cur-rency exchanges.

Retail broking showed growth of4% at both Americas and inter-national operations, fuelled byrenewals and new business inLatin America, Asia, New Zealandand emerging markets.

Reinsurance brokerage was up5% owing to new treaty businessand some favourable pricing forinternational accounts, offset inpart by higher cedant retentions.

Expenses rose 6%, partly be-cause of a $14m charge for acquisi-tions, primarily Glenrand MIB.Operating profit for broking wasup to $366m from $347m.

The group completed its restruc-turing plan associated with theacquisition of Benfield in 2008 withafinal$8mexpenseschargeduringthe first quarter, bringing the totalcost to $161m. The plan led to theloss of 810 jobs. HR solutionsrecorded operating profit of $73m,reduced from $83m, as the rise incompensation and other expensesoutweighed a 3% increase in reve-

source dividends repatriated to theUK thereby increasing our finan-cial flexibility”.

First-quarter results for Willislooked much better than for thecomparable period of 2011 butmuch of the bottom-line improve-ment was because of one-off opera-tional review expenses and debtrepurchasing costs, collectivelytotalling$268m.Forthe2011period,

overall, operating profit increasedto $317m from $239m while netprofitwasupto$225mfrom$34m.

Revenue grew 2% on an organicbasis owing to development at theglobal and international retaildivisions, offsetting contraction inthe North American retailaccount. After an adverse impactof 1% owing to currency conver-sions, revenue climbed 1% overallto $1.01bn.

Willis Global – comprising globalspecialty, reinsurance, wholesalebusiness under Willis Faber &Dumas (WFD) and Willis CapitalMarkets & Advisory (WCMA) – pro-duced organic growth of 5%.

Reinsurance broking recordedhigh single-digit growth led byNorth America, international andspecialty operations. Growth wasinthelowsingle-digitrangeforspe-cialties, driven by marine andenergy business, and at WFD.WCMA’s revenue declined.

This month, Willis consolidatedthe many businesses within thedivision into three broad unitscovering reinsurance, placementand specialty.

International retail businesslodged a 4% rise in organic broker-age in the first quarter, driven bydouble-digit growth in Latin Amer-ica and eastern Europe, as well asmore modest development in Asiaand continental western Europe.Brokerage was down for UK retailoperations owing to general eco-nomic pressures, Willis said. Oper-ating profit for the division was upslightly to $292m.

Brokerage at the North Ameri-can retail operations fell 3% to$346m as organic growth in certainlines was more than offset bydeclining revenue for loan protec-tor business. The division’s operat-ing profit fell marginally to $82m.

Table 2: Aon, revenue breakdown, first quarter ( $m)

2011 2012

Americas retail 631 651

International retail 822 843

Total retail broking 1,453 1,494

Reinsurance broking 387 399

Risk and insurance broking segment total 1,840 1,893

Consulting services 371 380

Outsourcing 552 568

Consulting/HR solutions total 915 945

Total after eliminations 2,755 2,838

Table 3: Aon, operating result, first quarter ($m)

2011 2012

Risk and insurance broking 399 407

Consulting/HR solutions total 167 156

Total after eliminations 534 529

Continued from p9

Willis: Thebroker’s first-quarter 2012 resultswereanimprovementonthe comparableperiodforthepreviousyear

Table 4: Willis breakdown by division, first quarter ( $m)

2011 2012Revenue Operating result Revenue Operating result

North America 358 85 349 82International 289 86 292 81Retail total 647 171 641 163Global 360 176 372 179Overall total aftereliminations 1,007 239 1,013 317

2%Wilis revenuegrowth forQ1 2012

$317mWillis profit for

Q1 2012

5%Organic growthfor Willis Globalfor Q1 2012

Brown & Brown, based in Flor-ida, recorded a 15.4% increase inrevenue in the first quarter, risingto $302.5m from $262.2m for thesame period of last year.

However, the group’s account islikely to develop considerably fol-lowing the acquisition in Januaryof Arrowhead General InsuranceAgency, a national programmemanager and one of the largest USmanaging general agents. Arrow-head accounted for the bulk of the$41.5m core brokerage that acqui-sitions brought Brown & Brownduring the first quarter.

The group’s core brokerage(excluding contingent commis-sions and profit commission) forthe 2012 period was split retail56.3%, national programmes19.9%, wholesale 14.2% and serv-ices 9.6%. The quarter was animportant one, Brown & Brownsaid, as it marked the first time fol-lowing 20 consecutive quarters thefirmachievedpositivegrowthinitscore organic broking account.

The small positive growth, of0.9%, stemmed from stabilisingexposure units in the middle-market economy and slight rises inpremium rates.

However, in its core retail divi-sion, the group recorded contrac-tion of 0.7% on an organic basis,although revenue increased 6%overall owing to the effect of acqui-sitions. Brown & Brown posted netprofit of $49.4m, up 6.8%.

US broking group Amwins has

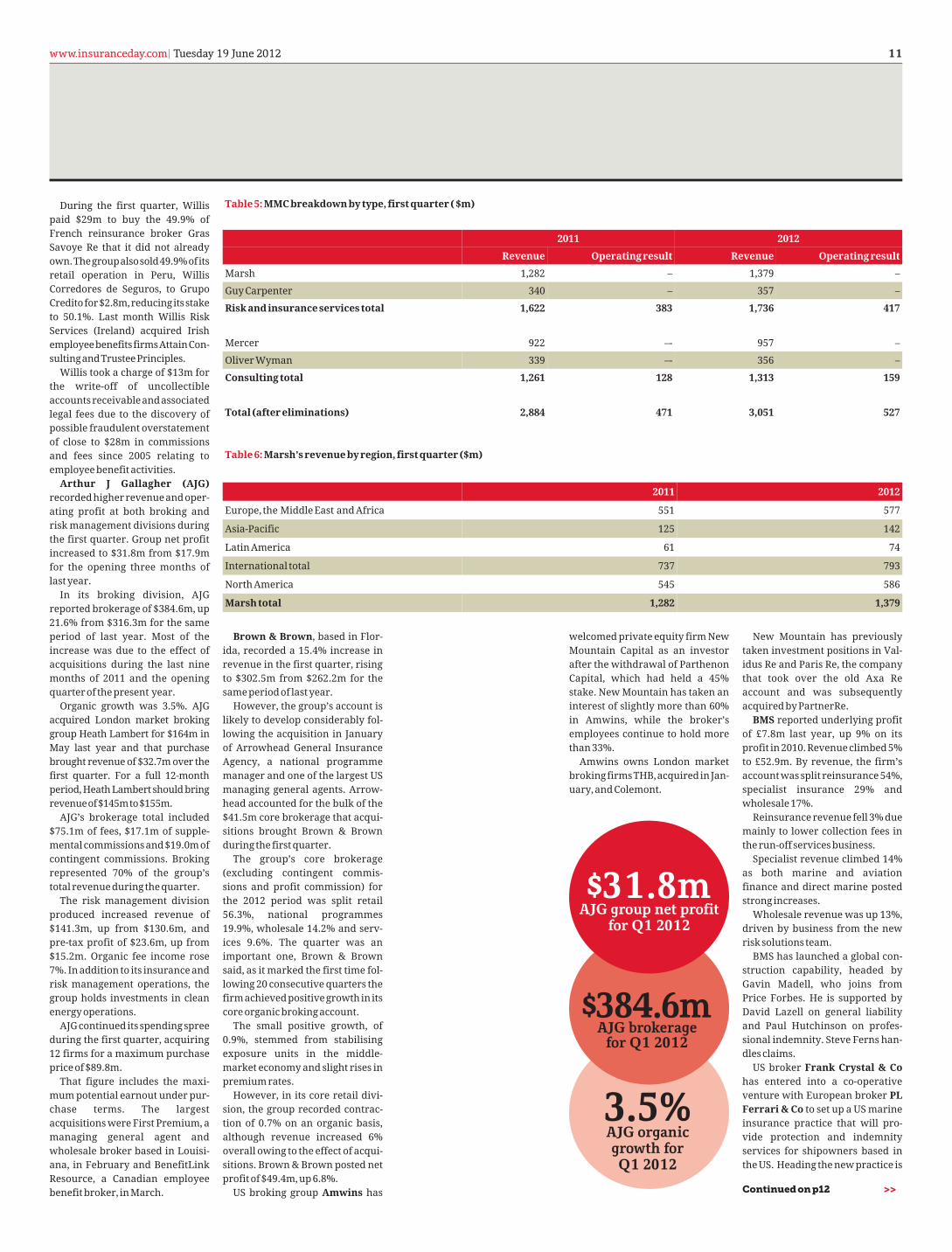

During the first quarter, Willispaid $29m to buy the 49.9% ofFrench reinsurance broker GrasSavoye Re that it did not alreadyown.Thegroupalsosold49.9%ofitsretail operation in Peru, WillisCorredores de Seguros, to GrupoCreditofor$2.8m,reducingitsstaketo 50.1%. Last month Willis RiskServices (Ireland) acquired IrishemployeebenefitsfirmsAttainCon-sultingandTrusteePrinciples.

Willis took a charge of $13m forthe write-off of uncollectibleaccountsreceivableandassociatedlegal fees due to the discovery ofpossible fraudulent overstatementof close to $28m in commissionsand fees since 2005 relating toemployee benefit activities.

Arthur J Gallagher (AJG)recordedhigherrevenueandoper-ating profit at both broking andrisk management divisions duringthe first quarter. Group net profitincreased to $31.8m from $17.9mfor the opening three months oflast year.

In its broking division, AJGreported brokerage of $384.6m, up21.6% from $316.3m for the sameperiod of last year. Most of theincrease was due to the effect ofacquisitions during the last ninemonths of 2011 and the openingquarter of the present year.

Organic growth was 3.5%. AJGacquired London market brokinggroup Heath Lambert for $164m inMay last year and that purchasebrought revenue of $32.7m over thefirst quarter. For a full 12-monthperiod, Heath Lambert should bringrevenueof$145mto$155m.

AJG’s brokerage total included$75.1m of fees, $17.1m of supple-mentalcommissionsand$19.0mofcontingent commissions. Brokingrepresented 70% of the group’stotal revenue during the quarter.

The risk management divisionproduced increased revenue of$141.3m, up from $130.6m, andpre-tax profit of $23.6m, up from$15.2m. Organic fee income rose7%. In addition to its insurance andrisk management operations, thegroup holds investments in cleanenergy operations.

AJG continued itsspendingspreeduring the first quarter, acquiring12 firms for a maximum purchaseprice of $89.8m.

That figure includes the maxi-mum potential earnout under pur-chase terms. The largestacquisitions were First Premium, amanaging general agent andwholesale broker based in Louisi-ana, in February and BenefitLinkResource, a Canadian employeebenefit broker, in March.

Table 6: Marsh’s revenue by region, first quarter ($m)

2011 2012

Europe, the Middle East and Africa 551 577

Asia-Pacific 125 142

Latin America 61 74

International total 737 793

North America 545 586

Marsh total 1,282 1,379

Table 5: MMC breakdown by type, first quarter ( $m)

2011 2012

Revenue Operating result Revenue Operating result

Marsh 1,282 – 1,379 –

Guy Carpenter 340 – 357 –

Risk and insurance services total 1,622 383 1,736 417

Mercer 922 –- 957 –

Oliver Wyman 339 –- 356 –

Consulting total 1,261 128 1,313 159

Total (after eliminations) 2,884 471 3,051 527

Continued on p12 >>

$384.6mAJG brokeragefor Q1 2012

$31.8mAJG group net profit

for Q1 2012

3.5%AJG organicgrowth forQ1 2012